Failure to settle outstanding premiums before the grace period expiration will result in an official cancellation notice. This document serves as formal notification that your coverage is being terminated due to non-payment, affecting your legal protection and benefits. Understanding these timelines is crucial to maintaining active policies. To assist with your formal correspondence, below are some ready to use template.

Image cover: Policy Termination and Grace Period Expiration: Official Notice Templates

Letter Samples List

- Grace Period Expiration and Official Policy Cancellation Letter

- Final Notice of Grace Period Expiration and Cancellation Letter

- Life Insurance Grace Period Expiration Cancellation Letter

- Commercial Policy Grace Period Expiration and Termination Letter

- Auto Insurance Official Cancellation and Grace Period Letter

- Notice of Coverage Cancellation and Grace Period Expiration Letter

- Health Insurance Grace Period Expiration and Cancellation Letter

- Overdue Premium Grace Period Expiration and Cancellation Letter

- Property Insurance Grace Period Expiration Official Cancellation Letter

- Final Grace Period Expiration and Official Cancellation Letter

- Business Insurance Policy Cancellation and Grace Period Letter

- Unpaid Premium Grace Period Expiration and Cancellation Letter

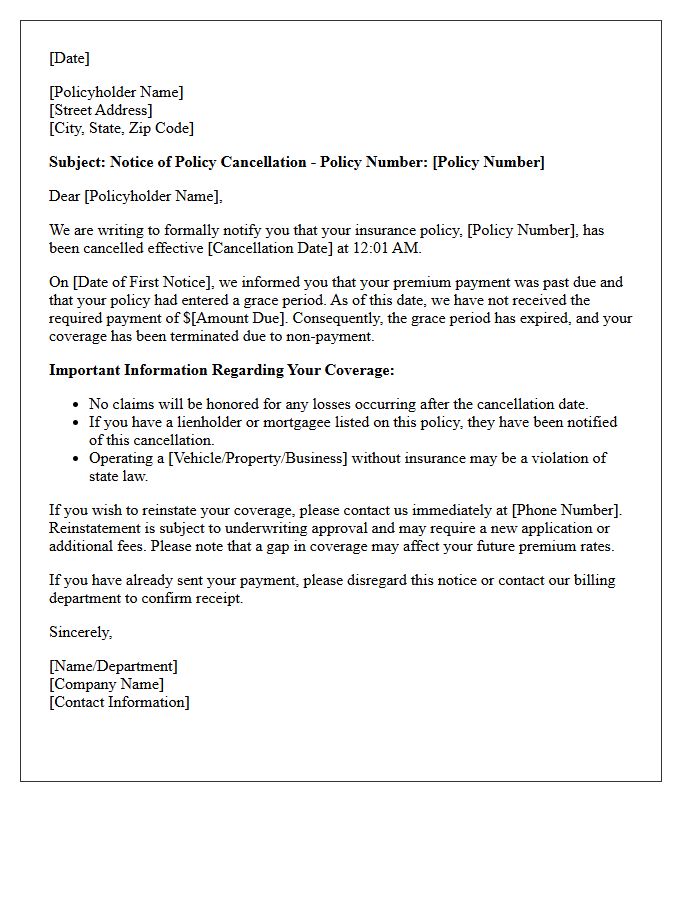

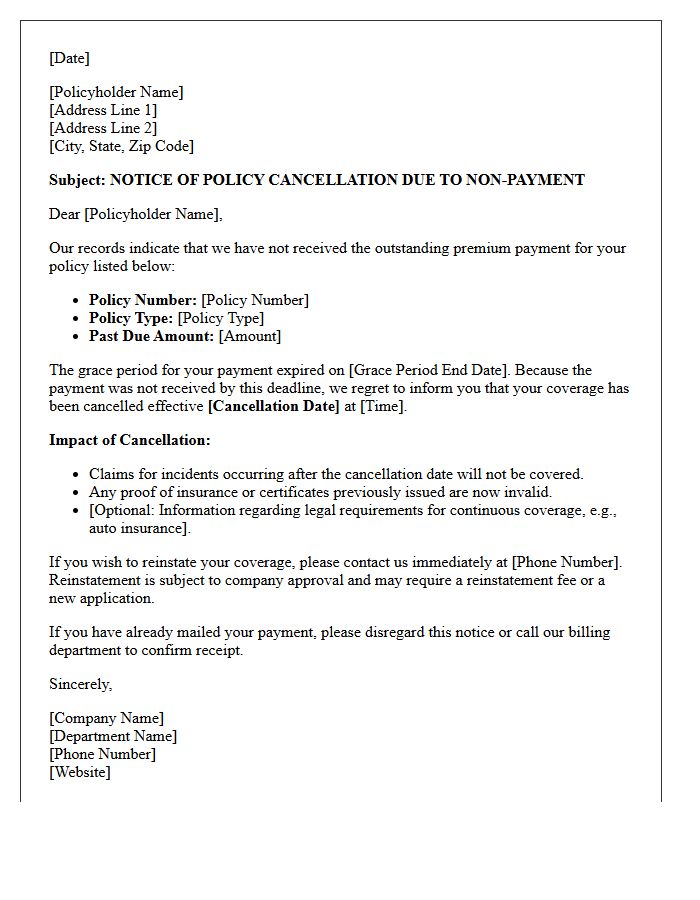

Grace Period Expiration and Official Policy Cancellation Letter

The Grace Period Expiration signifies the final deadline to settle overdue premiums before coverage lapses. Once this window closes, insurers issue an Official Policy Cancellation Letter, formally terminating the contract. This document serves as legal notice that protection has ended, potentially leaving you liable for full costs during any uninsured interval. To maintain continuous coverage and avoid reinstatement penalties, you must act before the grace period ends. Reviewing your policy's specific terms is essential to understanding your rights and the exact timing of a permanent policy termination.

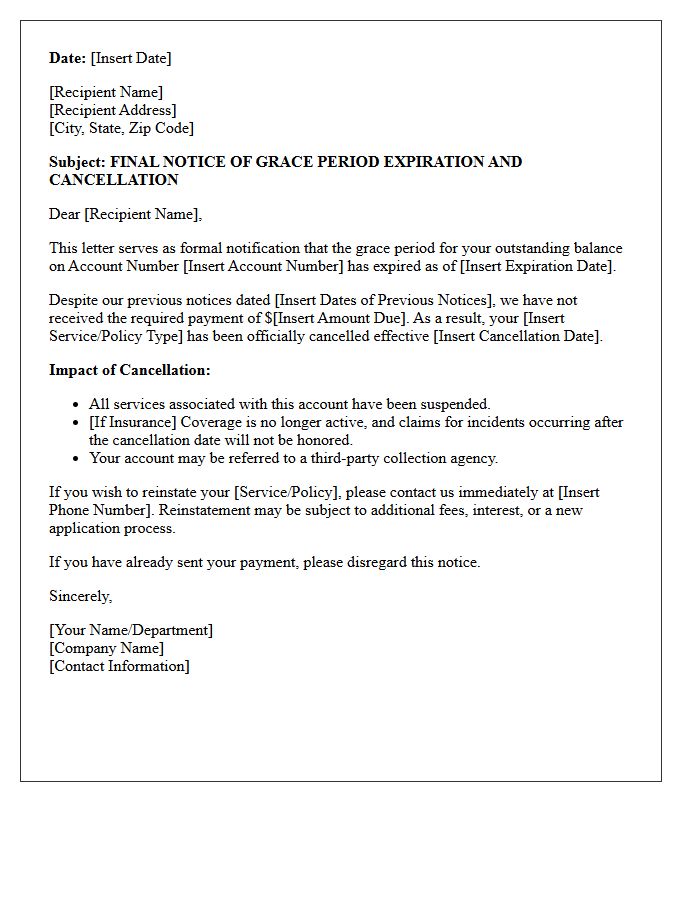

Final Notice of Grace Period Expiration and Cancellation Letter

A Final Notice of Grace Period Expiration is a critical legal alert indicating that your insurance coverage or service is about to terminate due to unpaid premiums. This document serves as the last warning before a policy cancellation occurs. To prevent a lapse in protection and potential financial loss, you must settle the outstanding balance immediately. Once the specified deadline passes, the contract becomes void, and reinstating coverage may require a new application or higher costs. Always verify the termination date to maintain continuous eligibility.

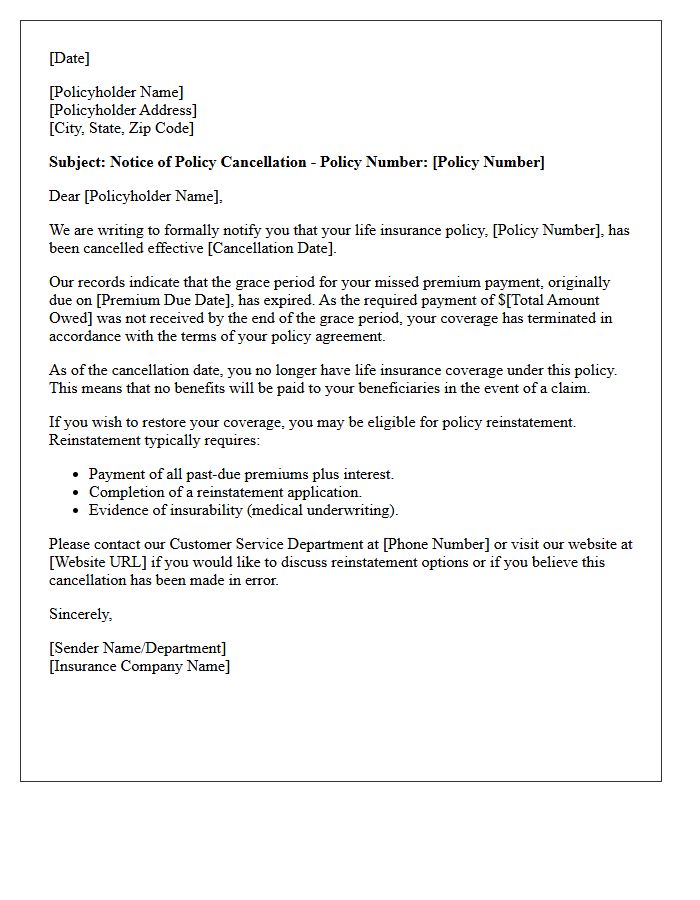

Life Insurance Grace Period Expiration Cancellation Letter

A life insurance grace period expiration cancellation letter is a critical notice informing policyholders that their coverage has ended due to non-payment. Before a policy terminates, insurers provide a grace period, typically thirty days, to settle overdue premiums. If the balance remains unpaid, the contract is officially canceled, resulting in a loss of death benefits. To restore protection, you must act quickly by requesting reinstatement, which may require a new medical exam or evidence of insurability. Always contact your provider immediately to discuss payment options and prevent a permanent lapse in coverage.

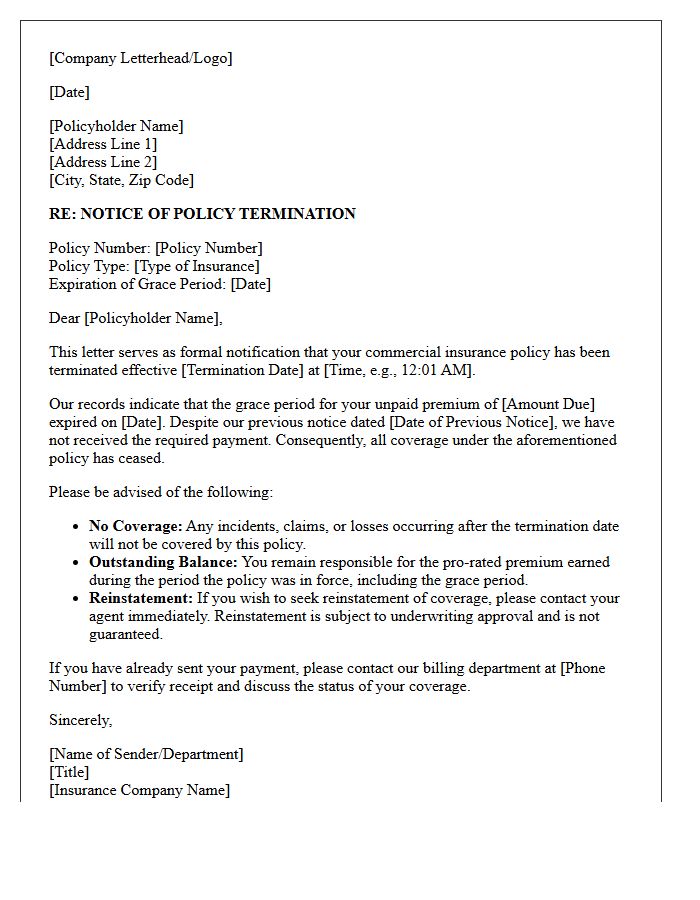

Commercial Policy Grace Period Expiration and Termination Letter

The Commercial Policy Grace Period Expiration signifies the final deadline for premium payment before coverage lapses. If payment is not received within this window, the insurer issues a Termination Letter, formally ending the contract. This notice is critical because it details the exact date and time protection ceases. To avoid a coverage gap and potential liability risks, businesses must settle outstanding balances immediately. Once terminated, reinstating a policy often requires a new application and higher premiums. Always monitor notice periods to maintain continuous business insurance compliance.

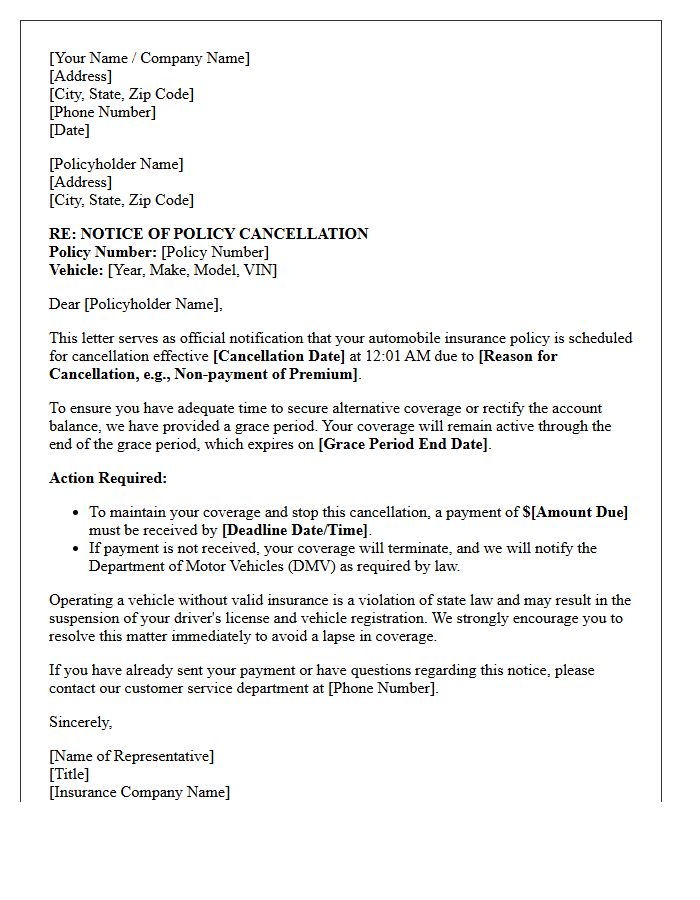

Auto Insurance Official Cancellation and Grace Period Letter

An official auto insurance cancellation notice serves as a formal legal warning that your coverage will terminate on a specific date. It is crucial to monitor the grace period, which is the short timeframe provided by state law or policy terms to pay overdue premiums and avoid a lapse in coverage. To prevent legal penalties or higher future rates, you must respond immediately. Always verify the exact effective date of termination to ensure your vehicle remains continuously insured and legally compliant during any transition between providers.

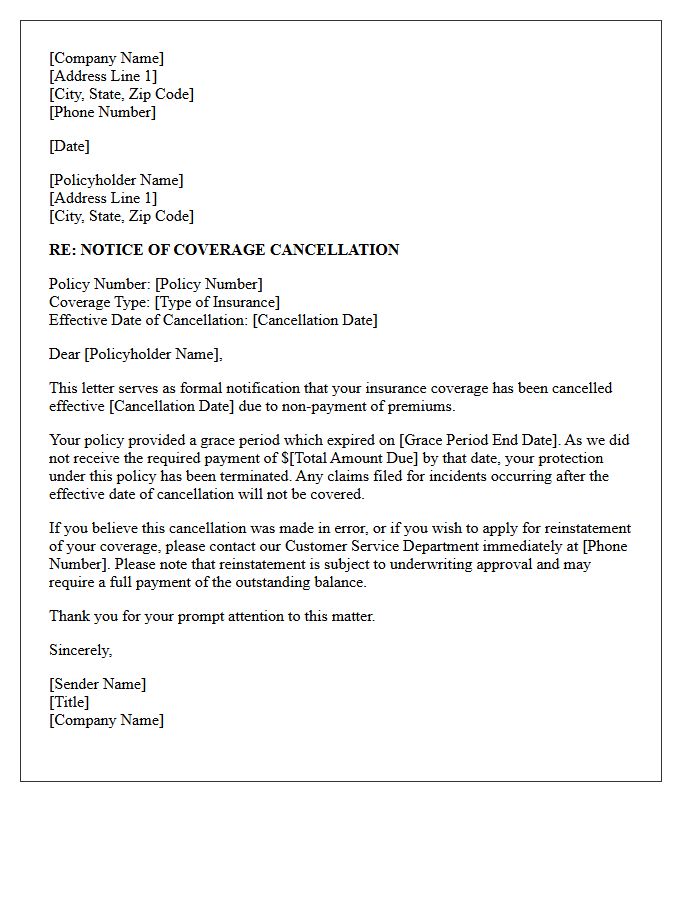

Notice of Coverage Cancellation and Grace Period Expiration Letter

A Notice of Coverage Cancellation and Grace Period Expiration Letter is a formal document notifying policyholders that their insurance coverage has terminated. It signifies that the grace period-the extra time allowed to pay an overdue premium-has officially ended without payment. Once this letter is issued, the policy is no longer active, leaving the individual without financial protection. To regain protection, you must contact your insurer immediately to discuss potential reinstatement options or policy restoration requirements before the gap in coverage becomes permanent.

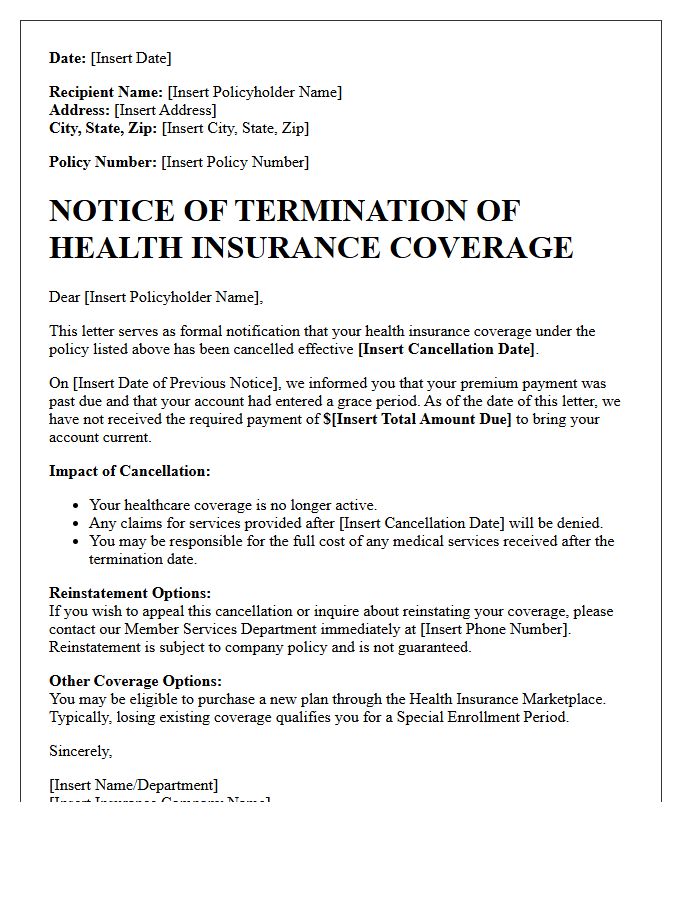

Health Insurance Grace Period Expiration and Cancellation Letter

A health insurance grace period provides extra time to pay overdue premiums before coverage ends. If you fail to pay by the expiration date, the insurer will issue a cancellation letter, officially terminating your policy. Once canceled, you lose access to benefits and may face a gap in coverage until the next open enrollment. It is crucial to monitor notices and pay balances promptly to avoid a loss of protection. Reinstatement is not guaranteed after a termination for non-payment, potentially leaving you responsible for all medical costs.

Overdue Premium Grace Period Expiration and Cancellation Letter

An Overdue Premium Grace Period Expiration and Cancellation Letter serves as a formal notification that your insurance coverage is terminating due to non-payment. Once the grace period expires, the policy is legally cancelled, leaving you without financial protection. It is critical to act before the effective date listed in the letter to avoid a lapse in coverage. Reinstating a cancelled policy often requires a new application, higher premiums, or a statement of health. Always prioritize payment or contact your insurer immediately to discuss potential reinstatement options before the deadline passes.

Property Insurance Grace Period Expiration Official Cancellation Letter

Receiving an official cancellation letter signifies that your insurance coverage has ended due to non-payment after the grace period expired. This document confirms you no longer have financial protection against property damages or liability claims. To avoid a permanent lapse in coverage, which often leads to higher future premiums and limited carrier options, you must contact your insurer immediately. Reinstatement may be possible if payment is made quickly, but a notice of cancellation typically triggers a notification to your mortgage lender, potentially resulting in forced-placed insurance.

Final Grace Period Expiration and Official Cancellation Letter

The Final Grace Period Expiration marks the definitive deadline for payment before policy termination. If payment is not received by this cutoff, the insurer issues an Official Cancellation Letter, formally ending your coverage. To maintain continuous protection and avoid a lapse, you must settle outstanding premiums before the expiration date noted in your notice. Once cancelled, reinstating a policy may require a new application or higher premiums. Always verify the effective date of cancellation to understand when your legal benefits and protections officially cease.

Business Insurance Policy Cancellation and Grace Period Letter

A Business Insurance Cancellation Letter formally notifies an insurer to terminate coverage. It must include the policy number and effective end date to prevent unintended lapses. Most policies feature a grace period, typically 10 to 30 days, allowing a window to pay premiums before coverage officially terminates. Always request a written confirmation of the cancellation and any applicable premium refunds. Timely communication ensures you maintain continuous protection and avoid financial penalties while transitioning between providers or adjusting your company's operational needs.

Unpaid Premium Grace Period Expiration and Cancellation Letter

An Unpaid Premium Grace Period Expiration and Cancellation Letter is a formal notice sent by insurers when a policyholder fails to pay their premium by the due date. This document confirms the end of the grace period, resulting in the immediate termination of coverage. It is crucial to understand that after this cancellation date, you no longer have financial protection against risks. To avoid a lapse, policyholders must settle outstanding balances before the expiration deadline. Reinstating a canceled policy often requires new underwriting or higher costs.

What is the difference between a grace period expiration and an official cancellation notice?

A grace period expiration marks the end of the extra time allowed to make a payment without penalty, while an official cancellation notice is a formal legal document stating that the policy or service is being terminated due to non-payment.

Can I prevent policy termination after the grace period has expired?

In many cases, you can prevent termination by paying the full outstanding balance immediately upon receiving the official cancellation notice; however, this depends on the specific terms of your contract and state regulations.

When does an official cancellation notice typically get sent?

An official cancellation notice is generally dispatched within 24 to 48 hours after the grace period expires, providing a final effective date for when coverage or services will officially cease.

What is the typical timeframe for a grace period before cancellation begins?

While timeframes vary by industry and state law, most insurance and service contracts provide a grace period of 15 to 30 days before the official cancellation process is initiated.

Will an official cancellation notice affect my credit score or future insurability?

Yes, receiving an official cancellation notice for non-payment can lead to a lapse in coverage, which may result in higher premiums in the future or a decrease in your credit score if the debt is sent to collections.

Comments