A reinstatement offer provides a vital opportunity for policyholders to restore lapsed coverage without undergoing a full new application process. Understanding the specific requirements and deadlines is essential to maintaining continuous protection after an unexpected cancellation. Learn how to navigate this process effectively to ensure your insurance remains active. Below are some ready to use templates.

Image cover: Winning Back Lapsed Policyholders: Reinstatement Offer Letters and Templates

Letter Samples List

- Auto Insurance Policy Reinstatement Offer Letter

- Homeowners Insurance Cancellation Reinstatement Letter

- Commercial Liability Policy Reinstatement Offer Letter

- Life Insurance Grace Period Reinstatement Letter

- Health Insurance Cancellation Reinstatement Offer Letter

- Lapsed Policy Reinstatement Offer Letter

- Premium Non-Payment Cancellation Reinstatement Letter

- Workers Compensation Policy Reinstatement Offer Letter

- Renters Insurance Post-Cancellation Reinstatement Letter

- Business Owners Policy Reinstatement Offer Letter

- General Property Insurance Reinstatement Letter

- Umbrella Insurance Policy Reinstatement Offer Letter

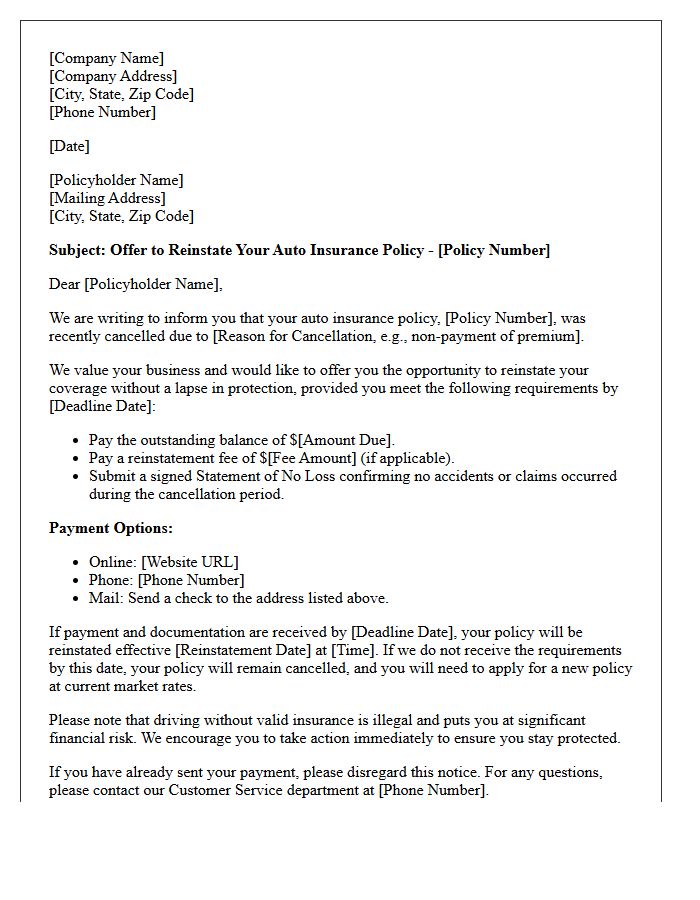

Auto Insurance Policy Reinstatement Offer Letter

An auto insurance policy reinstatement offer letter is a formal notice from your provider allowing you to reactivate lapsed coverage. This document typically outlines specific conditions, such as paying overdue premiums and potential late fees by a strict deadline. It is crucial to understand whether the reinstatement includes a gap in coverage, which could leave you legally vulnerable. Responding promptly ensures you maintain continuous financial protection and avoid high-risk driver classifications. Always verify if your benefits and rates remain unchanged before signing the agreement.

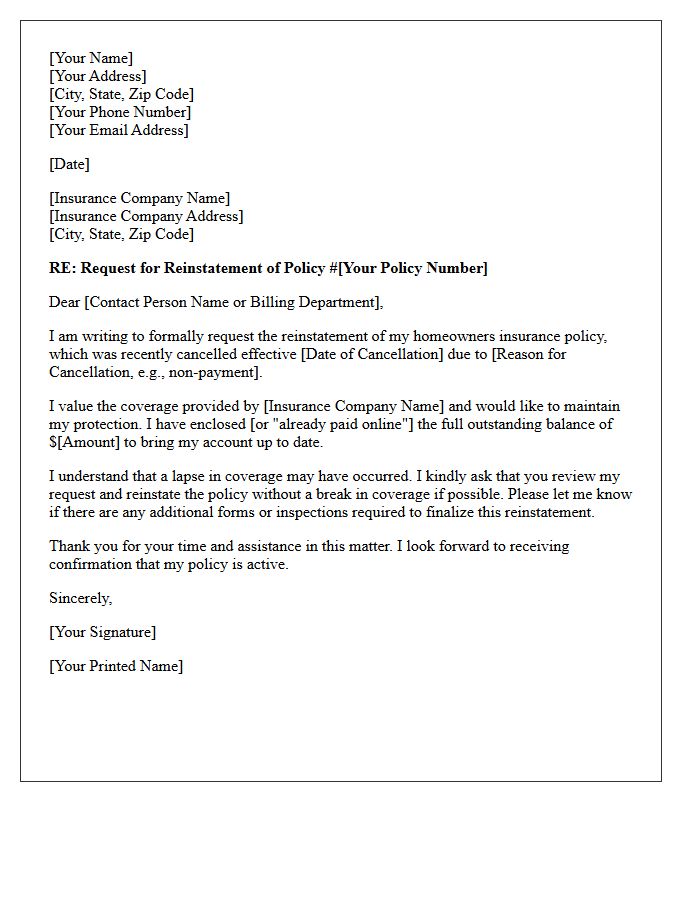

Homeowners Insurance Cancellation Reinstatement Letter

A homeowners insurance reinstatement letter is a formal request to restore coverage after a policy has been cancelled, usually due to non-payment. To ensure reinstatement, you must promptly submit the required payment and sign a "statement of no loss" to confirm no incidents occurred during the gap. Acting quickly is essential to avoid higher premiums or being labeled a high-risk client. Always contact your agent immediately to discuss specific carrier requirements and prevent a permanent lapse in coverage that leaves your property unprotected.

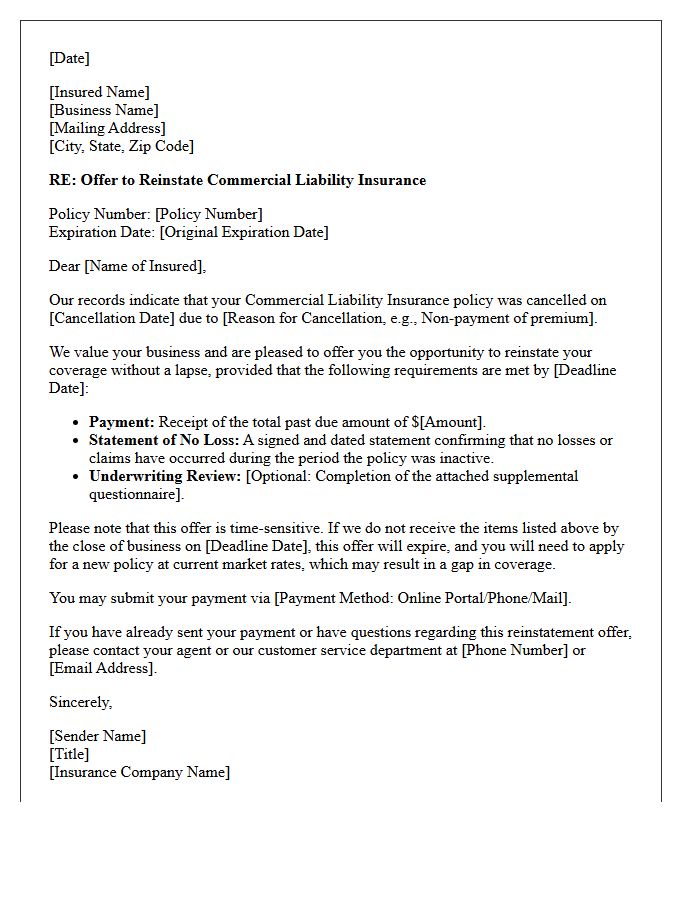

Commercial Liability Policy Reinstatement Offer Letter

A Commercial Liability Policy Reinstatement Offer Letter is a formal notification from an insurer providing an opportunity to reactivate lapsed coverage. It typically outlines the specific conditions required to restore the policy, such as settling outstanding premiums and submitting a "no loss" statement. Acting promptly is essential to avoid a permanent gap in protection, which can lead to increased legal exposure and higher future costs. Always review the deadline mentioned in the letter to ensure your business remains legally compliant and financially shielded from potential liability claims.

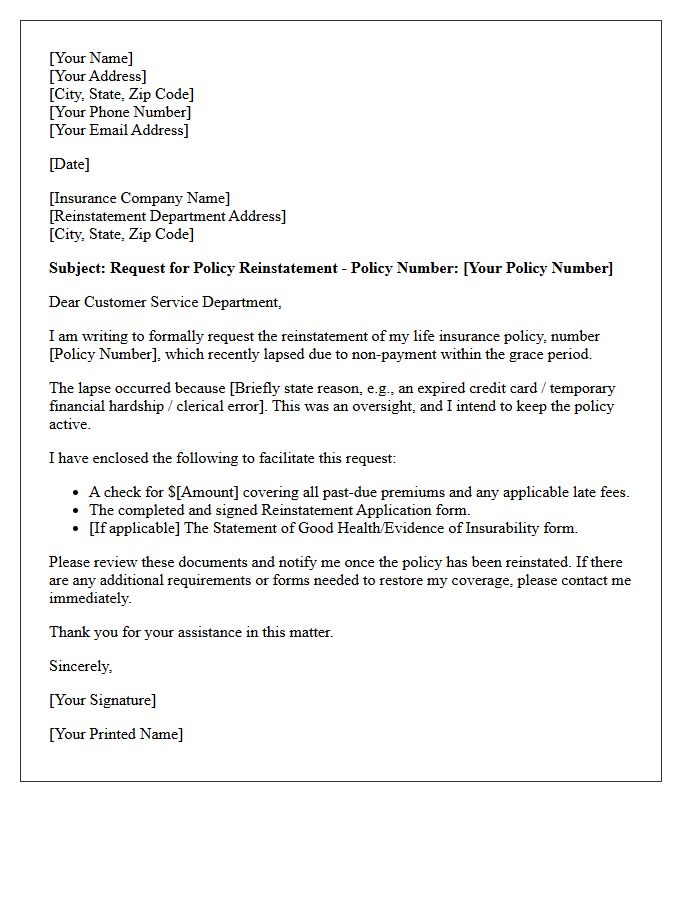

Life Insurance Grace Period Reinstatement Letter

A reinstatement letter is a formal request to restore a lapsed life insurance policy after the grace period has expired. This brief window, typically 30 days, allows for late payments without penalty. If coverage terminates, the insurer requires this written application and often a new medical declaration to assess risk. To successfully reinstate, you must pay all overdue premiums plus interest. Acting quickly is essential to regain death benefit protection without undergoing the full underwriting process required for a brand-new policy.

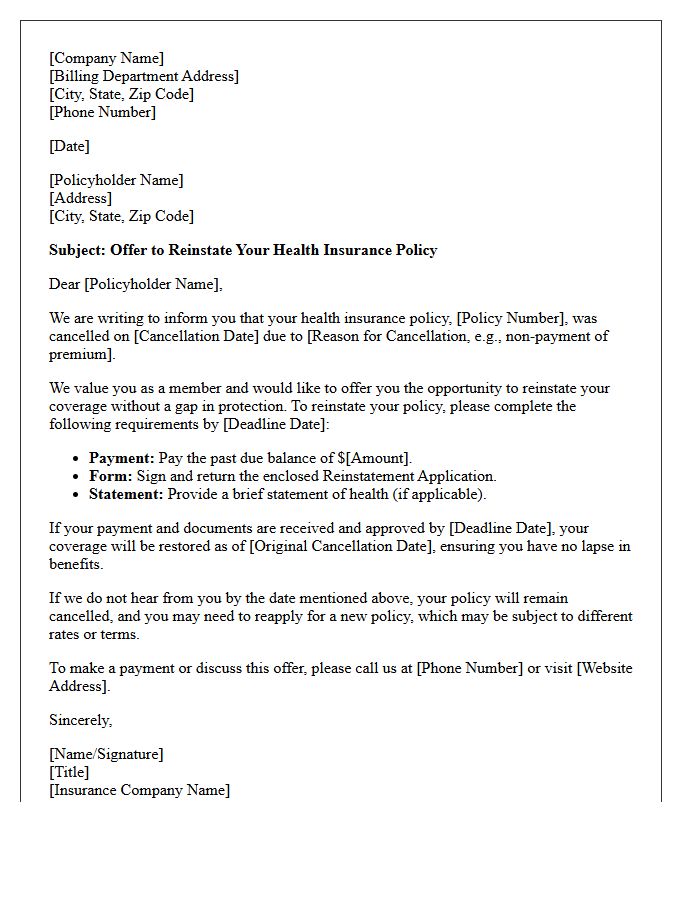

Health Insurance Cancellation Reinstatement Offer Letter

A health insurance reinstatement offer letter is a formal notice allowing you to restore lapsed coverage after a cancellation due to non-payment. To maintain continuous protection, you must strictly follow the deadline and payment instructions specified. Missing this window often results in a permanent loss of benefits and the need to reapply for a new policy. Always verify the reinstatement conditions, as you must typically pay all overdue premiums in full to successfully reactivate your plan without a gap in medical coverage.

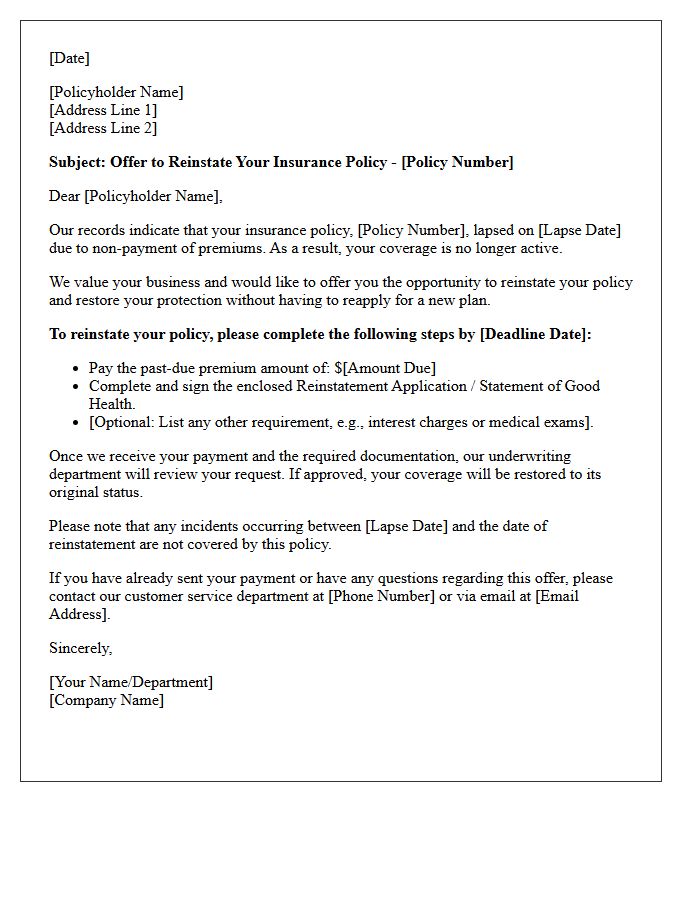

Lapsed Policy Reinstatement Offer Letter

A Lapsed Policy Reinstatement Offer Letter is a formal notice from an insurer providing a final opportunity to restore coverage after it has expired due to non-payment. This document outlines the specific requirements, such as paying overdue premiums and any applicable late fees, within a strict deadline. It is crucial to act quickly to avoid a permanent loss of protection or the need for a new medical exam. Reviewing this offer ensures you maintain continuous financial security without the higher costs often associated with starting a brand-new policy.

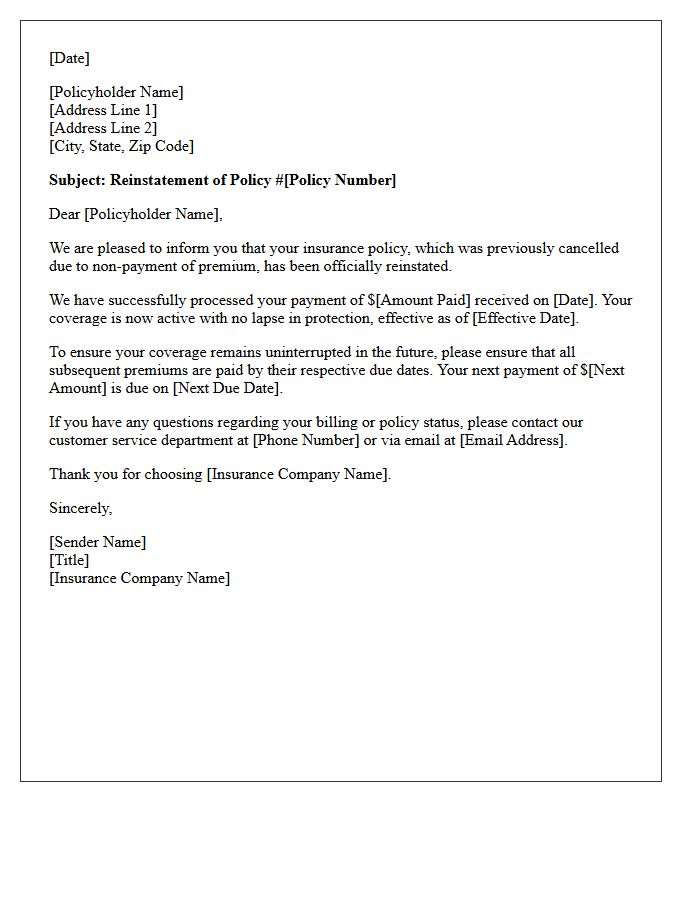

Premium Non-Payment Cancellation Reinstatement Letter

A Premium Non-Payment Cancellation Reinstatement Letter is a formal request sent to an insurer to restore a lapsed policy. After coverage terminates due to missed payments, this document expresses your intent to settle the outstanding balance. The most critical factor is the reinstatement period, which is the limited timeframe allowed to rectify the default. Approval often requires a statement of no losses during the gap. Timely submission is essential to avoid permanent loss of protection and to ensure continuous insurance coverage without facing higher future premiums.

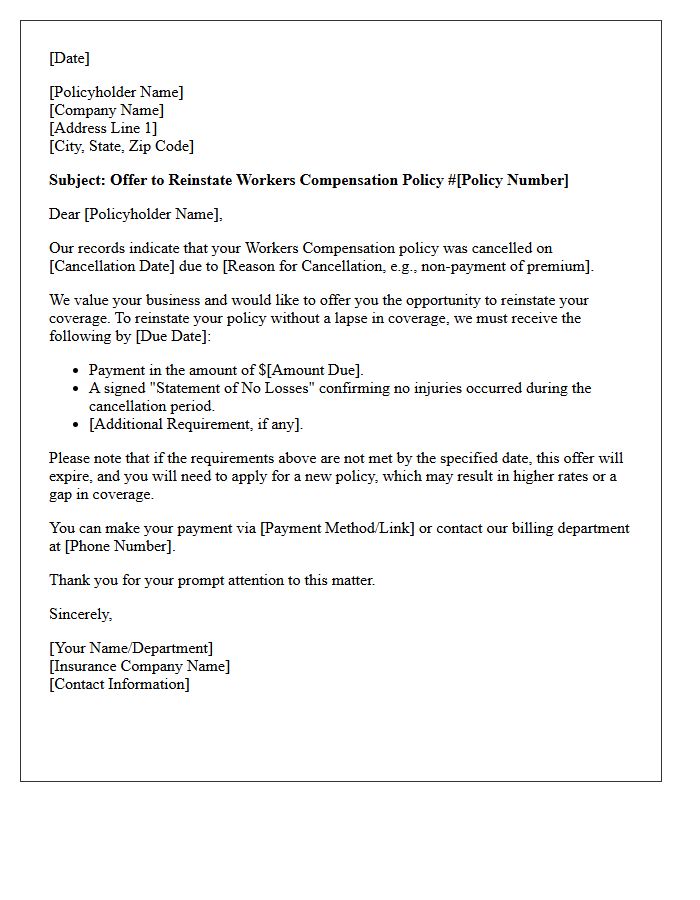

Workers Compensation Policy Reinstatement Offer Letter

A Workers Compensation Policy Reinstatement Offer Letter is a formal notice from an insurer providing terms to reactivate a cancelled policy. It typically outlines outstanding premiums, applicable fees, and a specific deadline for payment to avoid a permanent gap in coverage. Employers must act quickly, as signing this letter and submitting payment ensures continuous protection for employees and maintains legal compliance. Failure to respond may lead to severe legal penalties and personal liability for workplace injury claims during the uninsured period.

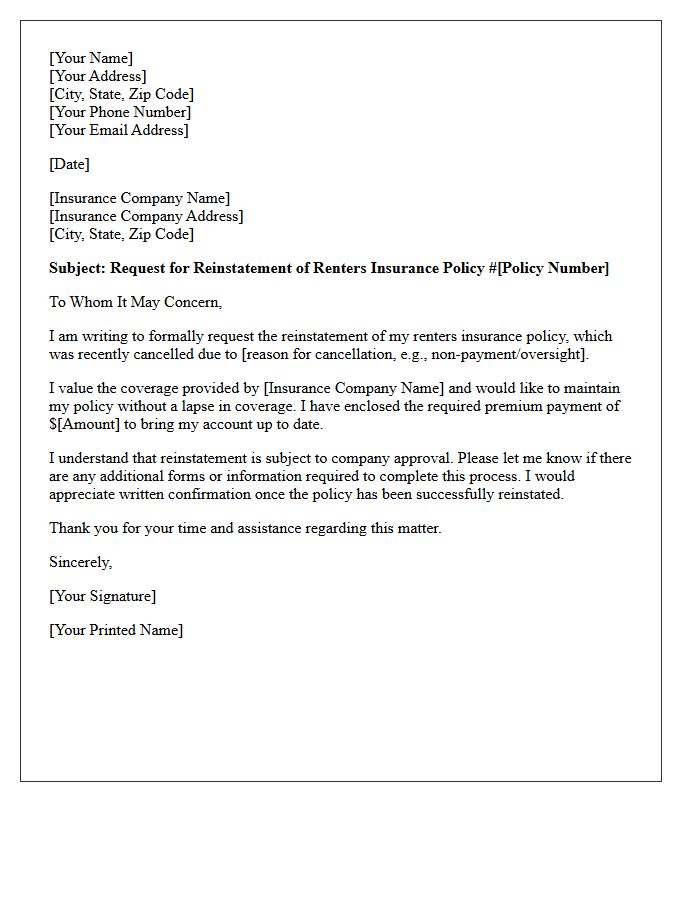

Renters Insurance Post-Cancellation Reinstatement Letter

A Renters Insurance Post-Cancellation Reinstatement Letter is a formal request sent to an insurer to restore a policy after it has lapsed. To ensure successful reinstatement, the policyholder must typically provide a statement of no losses, confirming no claims occurred during the gap in coverage. Acting quickly is essential, as most companies have strict reinstatement windows. Including the full outstanding premium payment with the letter increases the likelihood of approval. Once processed, it ensures continuous liability protection and property coverage without the need for a new, potentially more expensive policy.

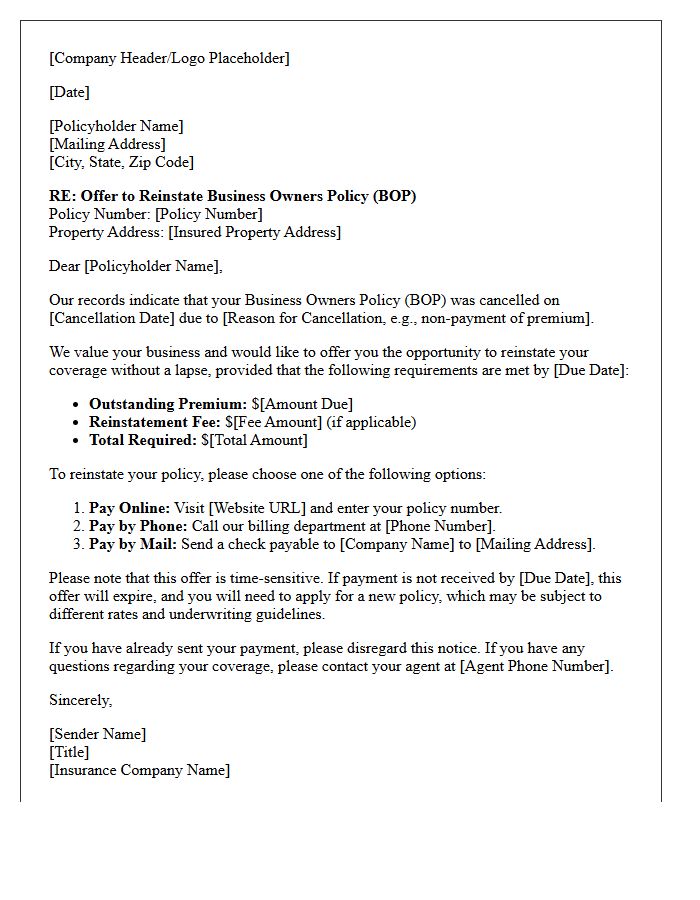

Business Owners Policy Reinstatement Offer Letter

A Business Owners Policy (BOP) Reinstatement Offer Letter is a formal notice sent by an insurer after a policy has lapsed, typically due to non-payment. This document outlines the specific conditions required to restore coverage without a gap. To successfully reinstate your insurance, you must remit the outstanding premium by the deadline specified. Reviewing this letter promptly is critical to maintaining continuous liability protection and property coverage, ensuring your small business remains legally compliant and financially protected against unforeseen risks and operational interruptions.

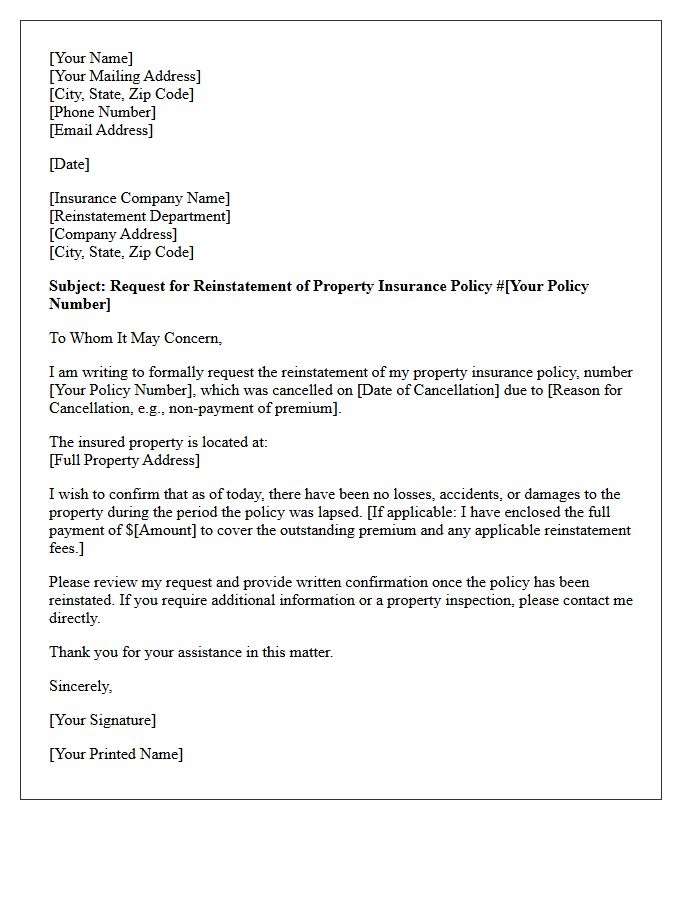

General Property Insurance Reinstatement Letter

A General Property Insurance Reinstatement Letter is a formal request to reactivate a cancelled policy. It typically requires the policyholder to clear outstanding premiums and provide a Statement of No Loss, confirming no claims occurred during the lapse period. Timely submission is critical to restore continuous coverage protection for physical assets. Once approved by the insurer, the reinstatement notice officially voids the cancellation, ensuring the property remains insured against risks like fire, theft, or natural disasters without needing a completely new policy application.

Umbrella Insurance Policy Reinstatement Offer Letter

An Umbrella Insurance Policy Reinstatement Offer Letter is a formal notice allowing you to restore lapsed liability coverage. It typically outlines the unpaid premiums, applicable late fees, and the specific deadline to respond. This document is critical because it offers a path to maintain extra protection against catastrophic claims without undergoing full new underwriting. To ensure continuous security, you must settle the outstanding balance and confirm no losses occurred during the gap. Promptly signing this offer preserves your financial safety net and prevents permanent policy termination.

What is a reinstatement offer following a policy cancellation?

A reinstatement offer is a formal proposal from your insurance provider to restore your coverage to active status after it has been cancelled due to non-payment or other policy violations. This offer typically requires the policyholder to meet specific conditions, such as paying outstanding premiums or providing a statement of no losses, to bridge the gap in coverage.

How do I accept a reinstatement offer for my insurance policy?

To accept a reinstatement offer, you must satisfy the requirements outlined in the notice by the specified deadline. This usually involves paying the full past-due balance, including any late fees or reinstatement penalties, and signing a "Statement of No Loss" to confirm that no claims occurred during the lapse period.

Is there a deadline for responding to a reinstatement offer?

Yes, reinstatement offers are time-sensitive and include a strict expiration date. If you fail to submit the required payments and documentation by this deadline, the offer becomes void, and you may be required to apply for a brand-new policy, which could result in higher premiums or a denial of coverage.

Will my premium increase after a policy reinstatement?

In most cases, a standard reinstatement restores your original policy terms and rates. However, if the reinstatement includes a gap in coverage, your "continuous insurance" discount may be removed, or your risk profile may be reassessed, which could lead to a premium increase upon the next renewal period.

What is the difference between a reinstatement with a lapse and a reinstatement without a lapse?

A reinstatement without a lapse (backdated) means your coverage is restored as if it never ended, providing protection for events that occurred during the payment delay. A reinstatement with a lapse means your coverage is only active from the moment the requirements are met, leaving a period of time where you had no insurance protection.

Comments