Receiving a full claim denial based on specific policy exclusions can be devastating. Insurance companies often cite fine-print limitations to avoid payouts for damage or liability. Understanding these contractual boundaries is essential for challenging a provider's decision effectively and protecting your financial rights. To help you appeal, below are some ready to use templates.

Image cover: Insurance Claim Denial Templates: Navigating Policy Exclusion Notices

Letter Samples List

- Full Claim Denial Letter Based on Policy Exclusions

- Notice of Claim Denial Letter Due to Policy Exclusions

- Official Letter of Full Claim Denial Under Excluded Coverage

- Insurance Claim Rejection Letter Regarding Policy Exclusions

- Complete Claim Denial Letter Subject to Policy Exclusions

- Determination Letter for Full Claim Denial by Policy Exclusion

- Formal Insurance Claim Denial Letter for Excluded Perils

- Total Claim Denial Letter Based on Standard Policy Exclusions

- Coverage Decision Letter Denying Claim for Policy Exclusions

- Final Determination Letter of Full Claim Denial Due to Exclusions

- Policy Exclusion and Full Claim Denial Letter

- Standard Letter of Claim Denial for Uncovered Policy Exclusions

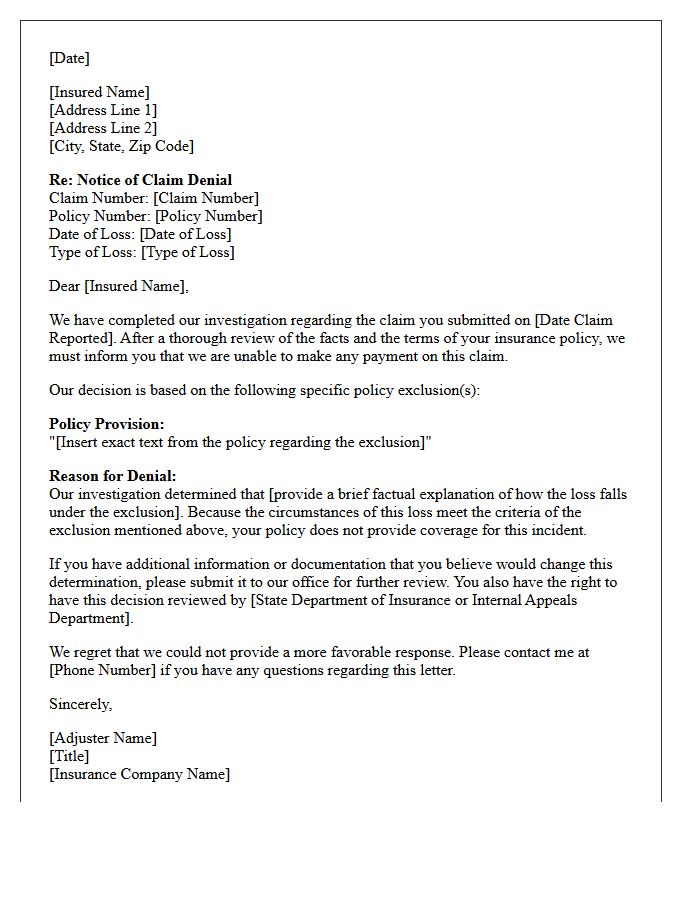

Full Claim Denial Letter Based on Policy Exclusions

Receiving a full claim denial letter based on policy exclusions means the insurer has determined the specific cause of loss is not covered. It is crucial to carefully review the exclusion clauses cited in the document and compare them against your original policy language. You have the right to request a detailed explanation or file an appeal if you believe the provision was applied incorrectly. Understanding these policy exclusions is vital for identifying potential coverage gaps or determining if legal professional intervention is necessary to dispute the insurance company's decision.

Notice of Claim Denial Letter Due to Policy Exclusions

A Notice of Claim Denial Letter informs policyholders that their insurance provider will not cover a specific loss. This decision is primarily based on policy exclusions, which are specific conditions or circumstances listed in the contract where coverage does not apply. It is crucial to review the denial reason carefully and compare it against your original policy language. If you disagree with the insurer's interpretation, you have the legal right to file an appeal or provide additional evidence to demonstrate that the exclusion was applied incorrectly to your situation.

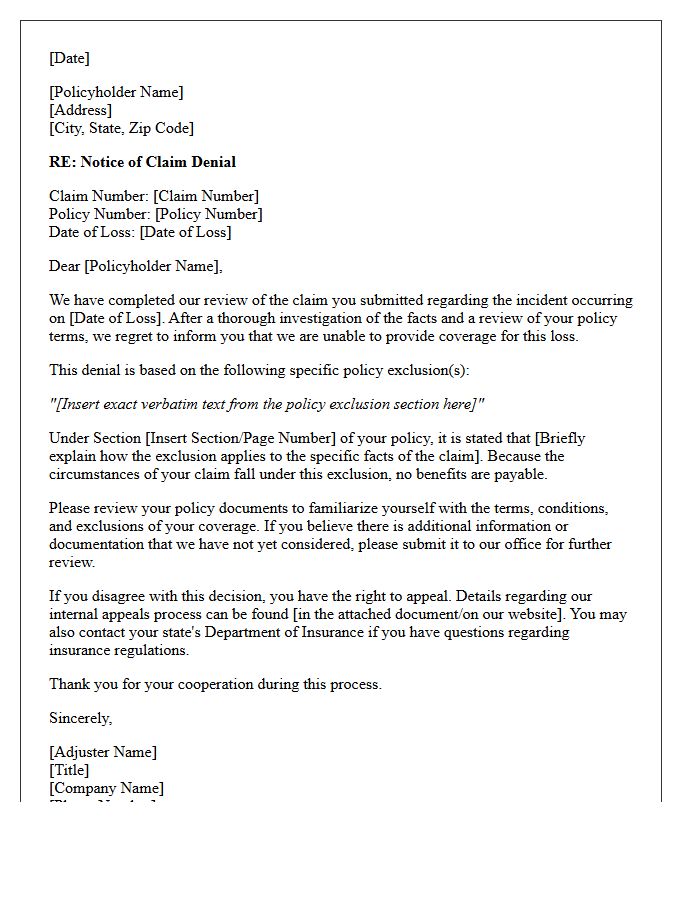

Official Letter of Full Claim Denial Under Excluded Coverage

An official letter of full claim denial under excluded coverage signifies that your insurance provider has formally rejected your request for reimbursement. This legal document specifies that the loss event falls under policy exclusions, meaning the specific risk is explicitly not covered by your contract. It is crucial to review the cited clauses and compare them against your policy language. If you disagree with the assessment, you must follow the outlined appeals process within the mandated timeframe to dispute the insurer's decision and protect your contractual rights.

Insurance Claim Rejection Letter Regarding Policy Exclusions

Receiving an insurance claim rejection letter citing policy exclusions means the insurer has determined the specific event or damage is not covered under your contract. To respond effectively, you must carefully compare the denial reason against your original policy documentation. Common exclusions include wear and tear, intentional acts, or specific high-risk perils. If you believe the exclusion was applied incorrectly or the language is ambiguous, you have the legal right to file a formal appeal or provide additional evidence to challenge the company's decision and seek a secondary review.

Complete Claim Denial Letter Subject to Policy Exclusions

Receiving a complete claim denial letter means your insurance provider has formally refused payment for a loss based on specific policy exclusions. These clauses define events or conditions not covered under your contract. It is critical to review the cited exclusion sections to verify if the insurer's interpretation is accurate. Policyholders have a legal right to appeal this decision by submitting supplemental evidence or clarifying facts. Understanding these limitations helps you determine if the denial was wrongful or if the incident falls outside your purchased protection boundaries.

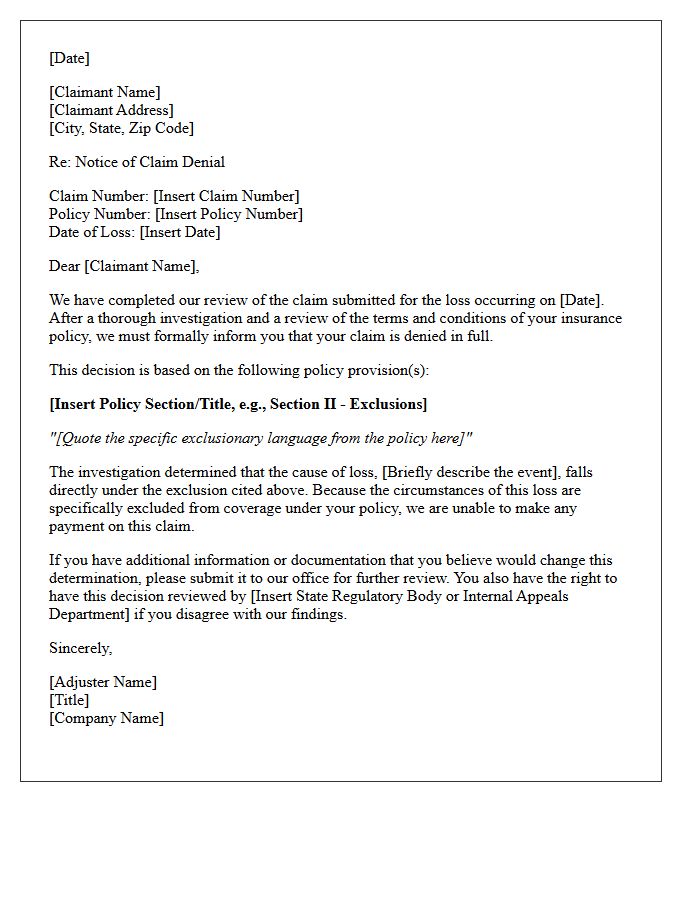

Determination Letter for Full Claim Denial by Policy Exclusion

A Determination Letter for a full claim denial signifies that your insurance provider will not cover a loss because the incident falls under a specific policy exclusion. This formal notice outlines the legal and contractual reasons for the rejection, citing the precise language within your agreement. It is crucial to review these cited exclusions immediately to verify their applicability. You have the right to challenge this decision by filing a formal appeal or providing additional evidence to prove the exclusion was incorrectly applied to your specific situation.

Formal Insurance Claim Denial Letter for Excluded Perils

A formal insurance claim denial letter for excluded perils serves as a legal notice that your policy does not cover specific types of loss. To contest this, you must carefully review the Exclusion Clause cited in the document. It is crucial to examine your policy language to ensure the insurer is correctly interpreting the event. If you believe the denial is wrongful, gather evidence and submit a written appeal or consult a professional. Understanding your coverage limitations is the first step in resolving disputes regarding unpaid property or liability claims.

Total Claim Denial Letter Based on Standard Policy Exclusions

Receiving a total claim denial letter means your insurance provider has refused payment based on specific standard policy exclusions. These clauses identify uncovered risks, such as wear and tear, intentional damage, or catastrophic events like floods. It is vital to carefully review the cited policy language to verify accuracy. If the denial seems unjust, you have the legal right to file a formal appeal or seek a third-party appraisal. Always document all communications and maintain a copy of your full policy to challenge the insurer's interpretation effectively.

Coverage Decision Letter Denying Claim for Policy Exclusions

A coverage decision letter denying a claim based on policy exclusions signifies that your insurer will not pay for the loss. It is critical to review the specific exclusion clauses cited in the document to ensure they align with your policy's terms. If you believe the exclusion was applied incorrectly or the language is ambiguous, you have the right to appeal the decision. Act quickly, as there are strict deadlines for submitting supplemental evidence or initiating a formal dispute process to potentially overturn the denial.

Final Determination Letter of Full Claim Denial Due to Exclusions

A final determination letter signals the formal end of the appeals process, confirming a Full Claim Denial. This legal notice states that the insurance provider will not pay for services because they fall under specific policy exclusions. These exclusions are predefined conditions or treatments not covered by your plan. Receiving this letter means you have exhausted internal remedies, making it the final administrative decision. Carefully review the listed exclusion codes to determine if you should pursue external independent reviews or legal action to contest the insurer's interpretation of your policy language.

Policy Exclusion and Full Claim Denial Letter

Receiving a full claim denial letter often stems from a specific policy exclusion, which is a provision identifying scenarios not covered by your insurance contract. It is critical to review the cited exclusion carefully to ensure the insurer interpreted the facts correctly. If the denial seems unjust, you have the right to appeal the decision by providing supplemental evidence or clarifying policy language. Understanding these limitations before an incident occurs helps manage expectations, as exclusions are legally binding clauses that define the precise boundaries of your insurance coverage and financial protection.

Standard Letter of Claim Denial for Uncovered Policy Exclusions

A standard Letter of Claim Denial notifies a policyholder that their insurance request is rejected due to specific uncovered policy exclusions. This document serves as a formal explanation, citing exact contractual language that limits coverage. It is essential to verify that the cited limitations align with your actual policy terms. If you disagree, the letter typically outlines appeal procedures or steps for external review. Understanding these exclusions helps policyholders determine if the denial was justified or if legal recourse is necessary to challenge the insurer's decision.

What is a full claim denial based on policy exclusions?

A full claim denial based on policy exclusions occurs when an insurance company refuses to pay a claim because the specific cause of loss or circumstances of the event are explicitly listed as non-covered items within the insurance contract's "Exclusions" section.

How can I dispute a claim denial if the insurer cites a policy exclusion?

To dispute a denial, you should first review your policy's Declarations Page and the specific exclusion clause cited in your denial letter. If the insurer has misinterpreted the facts of your loss or if the exclusion language is ambiguous, you can file a formal internal appeal supported by evidence, such as photos, expert reports, or repair estimates.

What are the most common policy exclusions used to deny insurance claims?

Common exclusions that lead to full claim denials include "wear and tear," lack of maintenance, intentional acts, earth movement (earthquakes), nuclear hazards, and specific high-risk activities or items that were not disclosed at the time the policy was issued.

Can an insurance company deny a claim based on an exclusion not mentioned in my policy?

No, an insurance company cannot legally deny a claim based on an exclusion that is not clearly written in your signed policy. Under the principle of "contract of adhesion," any ambiguity in the exclusion language is typically interpreted in favor of the policyholder, not the insurer.

Does a "full claim denial" mean I have no further options for recovery?

A full claim denial is not necessarily the final word. If an internal appeal is unsuccessful, you can file a complaint with your state's Department of Insurance, seek independent appraisal, or consult with a policyholder attorney to determine if the insurer acted in bad faith or applied the exclusion incorrectly.

Comments