Receiving a Notice of Coverage Lapse during an incident date indicates that your insurance policy was inactive when the loss occurred. This critical document affects claim eligibility and legal compliance regarding financial responsibility. Understanding the specific timing of your policy cancellation is essential for resolving disputes or seeking reinstatement. To assist your response, below are some ready to use template.

Image cover: Insurance Coverage Gaps: Incident Date Notification Templates and Samples

Letter Samples List

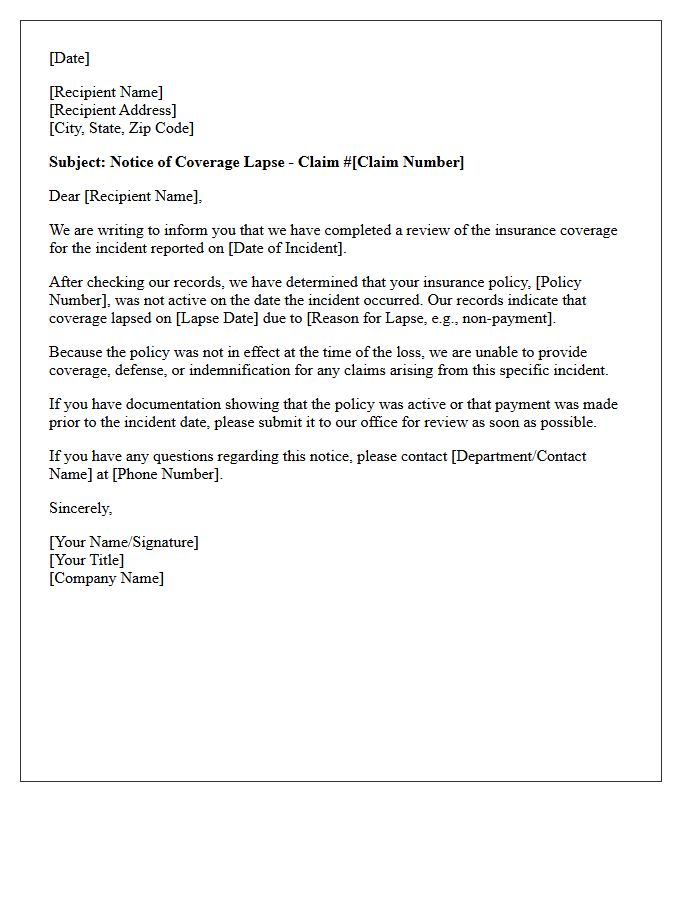

- Notice of Coverage Lapse During Incident Date Letter

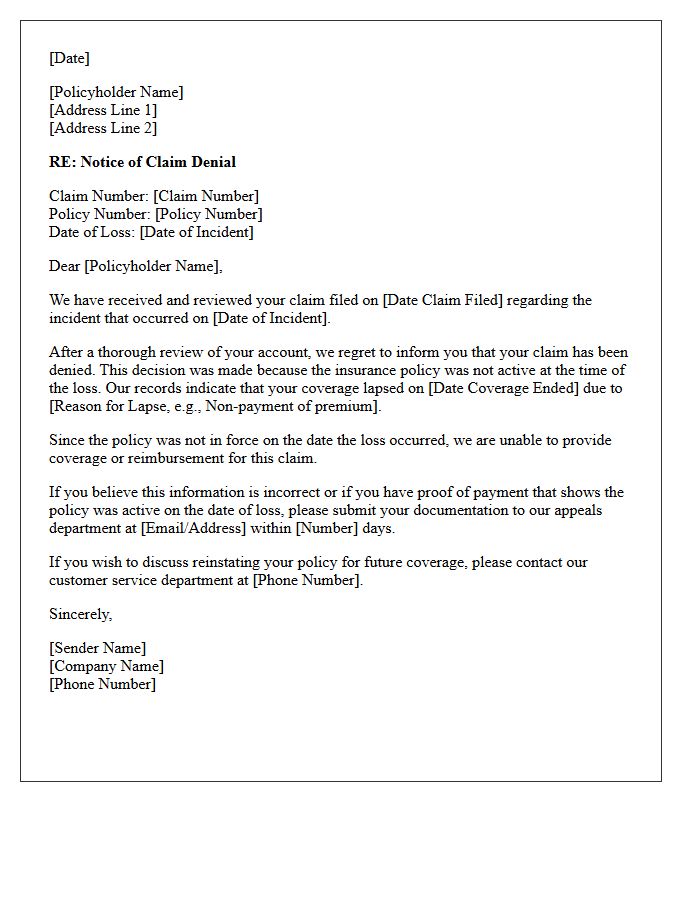

- Claim Denial Letter Due to Lapsed Coverage

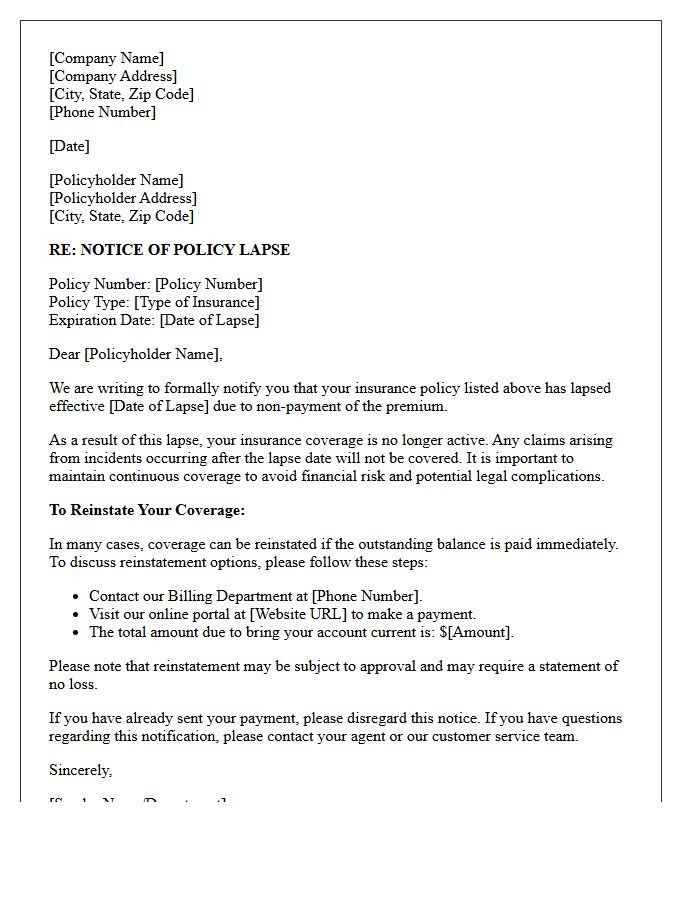

- Insurance Policy Lapse Notification Letter

- Incident Date Outside Active Coverage Letter

- Coverage Expiration Prior to Incident Letter

- Notice of Uninsured Incident Date Letter

- Policy Cancellation and Incident Overlap Letter

- Letter of Claim Rejection for Lapsed Policy

- Non-Covered Incident Date Notification Letter

- Grace Period Expiration and Incident Letter

- Letter Explaining Coverage Lapse on Date of Loss

- Premium Non-Payment and Incident Date Letter

- Inactive Policy Status on Date of Loss Letter

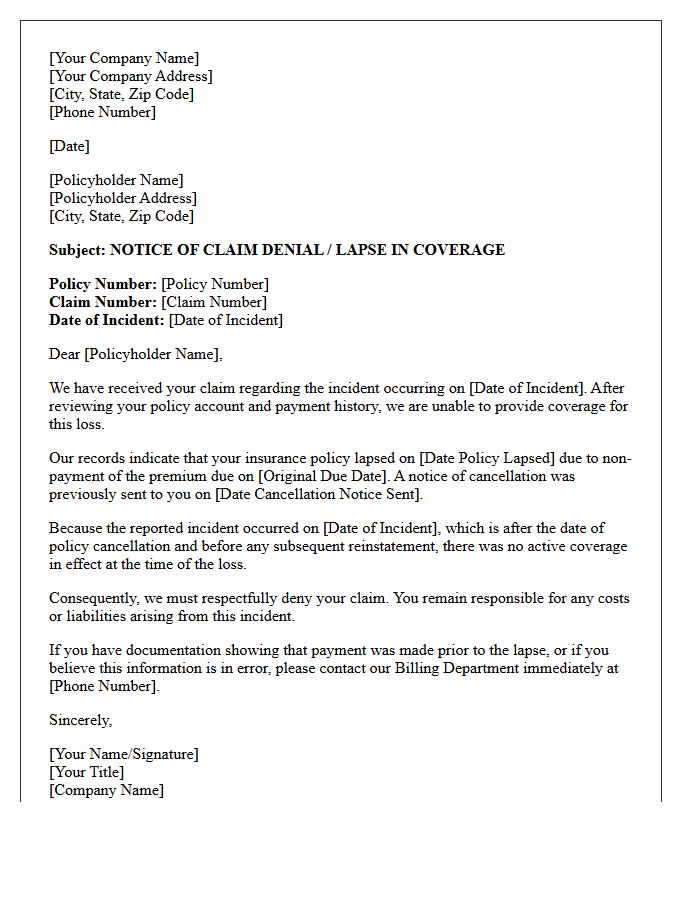

Notice of Coverage Lapse During Incident Date Letter

A Notice of Coverage Lapse during an incident date is a critical document indicating that your insurance policy was inactive when a loss occurred. Receiving this letter means the insurer may deny your claim because premiums were unpaid or the term expired. It is essential to verify your payment history and check for any grace period provisions immediately. Timely action is required to resolve potential coverage gaps and avoid personal financial liability for damages sustained during the uninsured period. Always maintain continuous protection to ensure legal and financial security.

Claim Denial Letter Due to Lapsed Coverage

Receiving a claim denial letter due to lapsed coverage means your insurance provider refused payment because the policy was inactive at the time of the incident. This typically occurs after a missed premium payment and the subsequent expiration of the grace period. To resolve this, immediately review your policy's effective dates and payment history. If the cancellation was an error, you must file a formal insurance appeal quickly. Maintaining consistent payments is essential to ensure continuous protection and avoid personal financial liability for expensive claims or medical bills.

Insurance Policy Lapse Notification Letter

An Insurance Policy Lapse Notification Letter is a formal notice sent by carriers when coverage terminates due to non-payment. Receiving this written alert is critical because it signals the end of financial protection and legal compliance. To prevent a permanent coverage gap, policyholders must act immediately during the specified grace period to pay outstanding premiums. Failure to respond may lead to higher future rates, reinstatement requirements, or total loss of benefits. Always verify the effective date of cancellation to ensure you remain legally insured and protected from liability.

Incident Date Outside Active Coverage Letter

An Incident Date Outside Active Coverage Letter is a formal notice from an insurance provider stating that a submitted claim occurred before or after the policy's effective period. This document signifies a denial of benefits because the specific event did not happen while the contract was active. To address this, policyholders should verify their coverage dates and confirm if a transition period or prior acts coverage applies. This letter is crucial for understanding why a claim was rejected based on temporal eligibility requirements.

Coverage Expiration Prior to Incident Letter

A Coverage Expiration Prior to Incident Letter is a formal notice from an insurance provider stating that your policy lapsed before the reported loss occurred. This document signifies a denial of benefits because no active contract existed at the time of the accident. Receiving this means the insurer will not pay for damages or provide legal defense. It is crucial to verify your payment history and effective dates immediately to ensure the company did not make a processing error regarding your protection window.

Notice of Uninsured Incident Date Letter

A Notice of Uninsured Incident Date Letter is a formal notification from an insurer or authority stating that a vehicle lacked valid insurance coverage on a specific date. Receiving this document is critical because it often precedes legal penalties, fines, or license suspension. To resolve the issue, you must provide proof of insurance that was active during the timeframe mentioned or pay the required compliance fees immediately. Ignoring this letter can lead to the permanent loss of driving privileges and increased future premiums.

Policy Cancellation and Incident Overlap Letter

A Policy Cancellation and Incident Overlap Letter is a critical document used to resolve coverage disputes when an insurance claim occurs near the termination date. It clarifies whether an incident happened during the active policy period or after its expiration. This letter serves as formal evidence to determine liability between sequential insurers. Providing precise dates and timestamps is essential to prevent a denial of coverage, ensuring that the responsible provider manages the claim and avoids legal ambiguity during transitions between different insurance carriers.

Letter of Claim Rejection for Lapsed Policy

A Letter of Claim Rejection for Lapsed Policy signifies that an insurance provider has formally denied a payout. This occurs because the policyholder failed to pay premiums within the grace period, resulting in a loss of coverage. It is vital to verify the exact cancellation date and ensure the insurer provided proper notification of default before the lapse. If you believe the policy was active or payments were made, you must submit an appeal with proof of payment to challenge the insurer's decision and potentially reinstate your financial protection.

Non-Covered Incident Date Notification Letter

A Non-Covered Incident Date Notification Letter is a formal document issued by an insurer informing a policyholder that a specific claim occurred outside the active policy period. This notice clarifies that the carrier holds no liability for damages occurring before the inception or after the expiration of coverage. It is crucial to verify the date of loss against your policy documents immediately. Receiving this letter typically results in a denial of benefits, meaning the policyholder is financially responsible for all related costs and legal defenses associated with the incident.

Grace Period Expiration and Incident Letter

A grace period expiration marks the final deadline to resolve a compliance or payment issue before penalties apply. Once this window closes, an incident letter is formally issued to document the breach. This notice serves as a critical record of non-compliance, potentially affecting your legal standing or credit score. To avoid severe consequences, you must address the requirements before the cutoff date. Monitoring these timelines ensures you maintain good standing and prevents formal disciplinary actions or service interruptions within professional or financial agreements.

Letter Explaining Coverage Lapse on Date of Loss

A letter explaining a coverage lapse on the date of loss is a critical document for insurance claims. It must verify the exact policy status, including missed premium payments or expiration dates. When a loss occurs without active protection, insurers typically issue a formal denial of coverage. To contest this, policyholders should provide proof of payment or evidence of administrative errors. Understanding the specific grace period or reinstatement terms is essential for determining if the claim can still be legally honored despite the recorded gap in protection.

Premium Non-Payment and Incident Date Letter

A Premium Non-Payment and Incident Date Letter is a critical formal notice sent by insurers when a coverage lapse occurs due to missed payments. Its primary purpose is to confirm whether an insurance policy was active on a specific incident date. If the premium was not paid prior to the loss, the insurer may legally deny the claim. Policyholders must verify the effective cancellation date and payment grace periods to determine if protection remains valid. Timely resolution is essential to avoid permanent loss of protection and potential financial liability for damages.

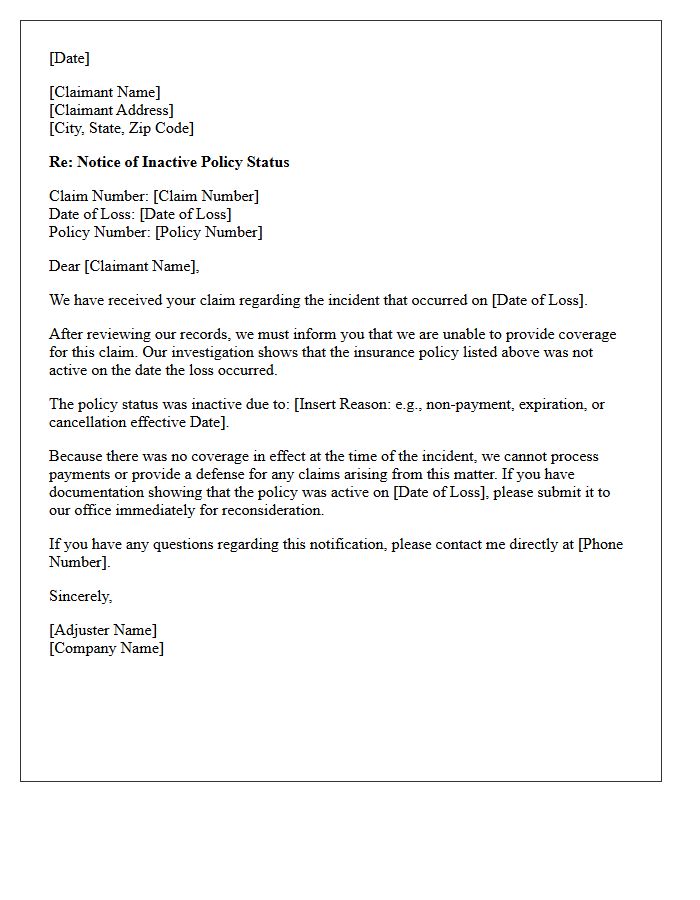

Inactive Policy Status on Date of Loss Letter

An Inactive Policy Status on Date of Loss Letter is a formal notification from an insurance provider stating that coverage was not in force when an incident occurred. This typically happens due to policy cancellation, non-payment of premiums, or expiration before the loss date. Receiving this document means the insurer will likely deny the claim, shifting financial liability to the policyholder. It is crucial to verify the effective dates and payment history immediately to identify potential administrative errors or potential gaps in protection that may require legal or professional appeal.

What is a Notice of Coverage Lapse during an incident date?

A Notice of Coverage Lapse during an incident date is a formal notification from an insurance provider stating that your policy was inactive or expired at the exact time an accident or loss occurred. This means the insurer is not contractually obligated to pay for damages or legal liabilities associated with that specific event.

Can an insurance claim be denied if the lapse occurred on the day of the incident?

Yes, if the incident occurred even a few hours after the policy expiration time (typically 12:01 AM of the expiration date) or before a reinstatement payment was processed, the insurer can legally deny the claim. Coverage must be active and in-force at the precise timestamp of the incident for a claim to be valid.

What are the most common reasons for receiving a coverage lapse notice?

The most common reasons include non-payment of premiums by the due date, failure to renew a policy before its expiration, or the insurance company canceling the policy due to a breach of terms or material misrepresentation. In some cases, it may also result from a banking error that caused a scheduled payment to fail.

Is it possible to appeal a denied claim due to a coverage lapse?

You can appeal if you can provide documented proof that the lapse notice is erroneous. Examples include evidence of a processed payment before the deadline, a bank statement showing the funds were transferred, or proof that the insurance company failed to send a legally required "Intent to Cancel" notice according to state regulations.

What should I do if I receive a lapse notice for an active incident?

First, verify the exact date and time of the incident against your policy's effective dates. If the lapse is accurate, you may be held personally liable for all damages. You should contact your insurance agent immediately to discuss reinstatement options to prevent future lapses, though this will generally not provide retroactive coverage for the incident in question.

Comments