Receiving a Partial Claim Denial can be confusing for policyholders. This guide explains how to interpret your coverage explanation letter, identifying why specific portions of your claim were rejected while others were approved. Understanding these insurance decisions is crucial for filing effective appeals. To simplify your response process, below are some ready to use template.

Image cover: Professional Guide to Partial Claim Denials: Coverage Explanation Templates and Letter Samples

Letter Samples List

- Auto Collision Depreciation Partial Claim Denial and Coverage Explanation Letter

- Roof Replacement Cosmetic Exclusion Partial Claim Denial and Coverage Explanation Letter

- Out-Of-Network Medical Provider Partial Denial and Coverage Explanation Letter

- Water Damage Remediation Limit Exceeded Partial Denial and Coverage Explanation Letter

- Auto Rental Reimbursement Cap Partial Claim Denial and Coverage Explanation Letter

- Homeowners Personal Property Depreciation Partial Denial and Coverage Explanation Letter

- Business Interruption Loss Partial Claim Denial and Coverage Explanation Letter

- Pre-Existing Health Condition Partial Denial and Coverage Explanation Letter

- Workers Compensation Treatment Partial Claim Denial and Coverage Explanation Letter

- Hail Damage Policy Limit Partial Denial and Coverage Explanation Letter

- Specialty Equipment Valuation Partial Claim Denial and Coverage Explanation Letter

- General Liability Excluded Damages Partial Denial and Coverage Explanation Letter

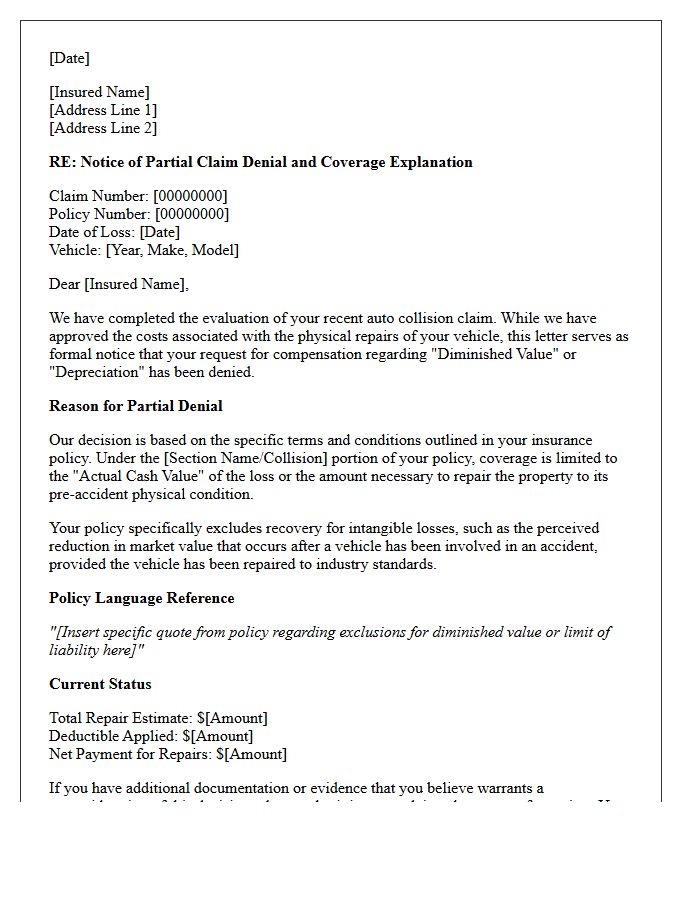

Auto Collision Depreciation Partial Claim Denial and Coverage Explanation Letter

An Auto Collision Depreciation Partial Claim Denial letter explains why an insurer refuses to pay the full Actual Cash Value of a vehicle. This typically occurs when a coverage explanation identifies pre-existing damage, excessive wear, or unrelated mechanical issues that reduce the settlement amount. Understanding the specific exclusion clauses and depreciation calculations in your policy is essential to challenging these adjustments. Always review the itemized list of deductions to ensure the insurer is not unfairly devaluing your asset based on inaccurate market data or betterment charges applied during repairs.

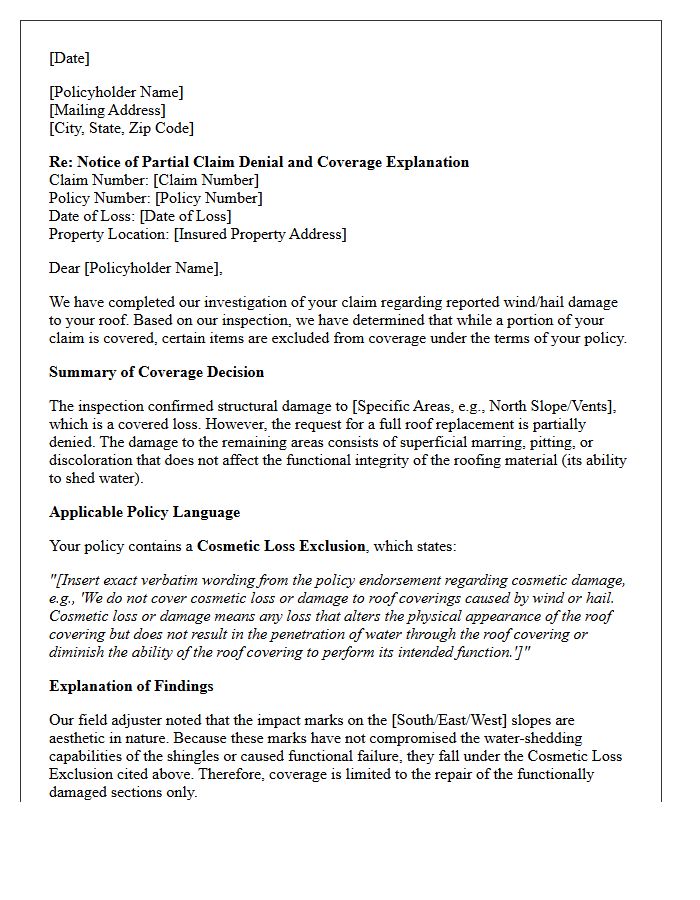

Roof Replacement Cosmetic Exclusion Partial Claim Denial and Coverage Explanation Letter

A Roof Replacement Cosmetic Exclusion allows insurers to deny claims for aesthetic damage, such as minor dents or scratches that do not impair functional performance. If you receive a partial claim denial, the coverage explanation letter will specify that while structural integrity is intact, surface-level imperfections are excluded under your policy terms. Homeowners must distinguish between functional damage, which compromises the roof's lifespan, and cosmetic marring. Reviewing your policy for specific exclusion endorsements is essential to understand why full replacement costs were not approved during the adjustment process.

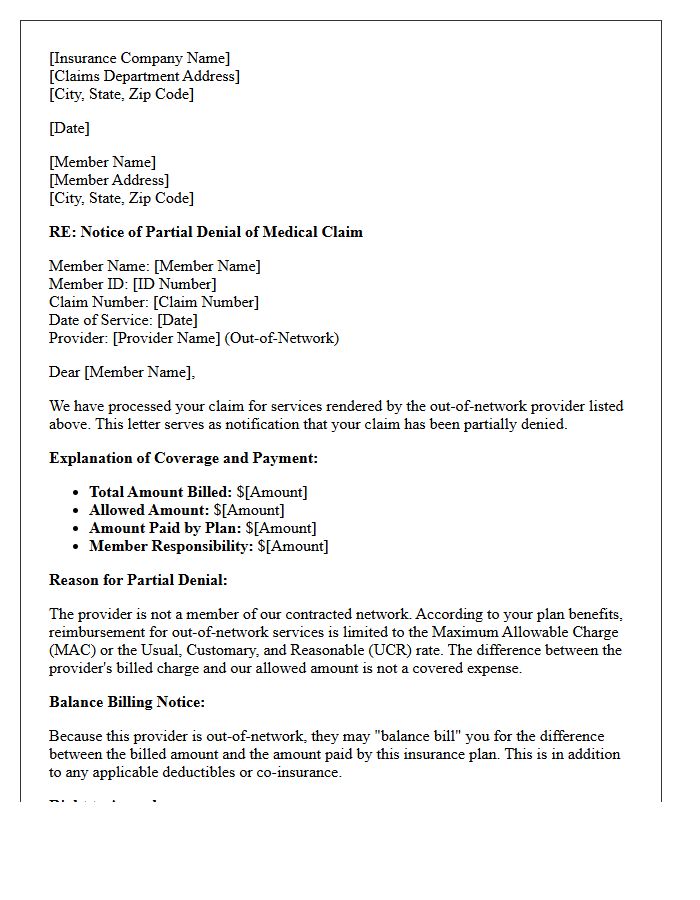

Out-Of-Network Medical Provider Partial Denial and Coverage Explanation Letter

An Out-Of-Network Medical Provider Partial Denial and Coverage Explanation Letter is a formal document from your insurer detailing why a claim was not fully paid. It often cites Allowed Amounts as the primary reason for reduced reimbursement. The letter explains the difference between the provider's billed charges and the insurance company's set rate. Understanding this Explanation of Benefits is crucial because patients may be responsible for the remaining balance, a practice known as balance billing, unless protected by specific state or federal consumer laws.

Water Damage Remediation Limit Exceeded Partial Denial and Coverage Explanation Letter

A Partial Denial letter occurs when a water damage claim surpasses your policy's specific Remediation Limit. Insurance policies often cap restoration costs for mold, fungus, or moisture extraction. Once this financial ceiling is reached, the insurer stops payment, leaving the homeowner responsible for additional costs. Carefully review the "Coverage Explanation" section to identify the exact sub-limits applied. Understanding these boundaries is essential for managing contractor expenses and ensuring that your claim remains within the indemnity thresholds defined by your insurance contract to avoid unexpected out-of-pocket liabilities.

Auto Rental Reimbursement Cap Partial Claim Denial and Coverage Explanation Letter

Receiving a partial claim denial letter for auto rental reimbursement typically occurs when your expenses exceed the daily or total coverage limits specified in your policy. The reimbursement cap is the maximum amount your insurer pays per day. If you choose a vehicle class more expensive than your policy allowance, or if repairs exceed the authorized timeframe, you are responsible for the remaining balance. Always review the coverage explanation to understand your specific daily rate and maximum benefit duration to avoid unexpected out-of-pocket costs during vehicle repairs.

Homeowners Personal Property Depreciation Partial Denial and Coverage Explanation Letter

A claim letter explains why an insurer applied depreciation to your personal property, resulting in a partial denial of the full replacement cost. This document details the difference between Actual Cash Value (ACV) and the total cost to buy new items. To recover withheld funds, you must typically provide receipts proving you actually replaced the goods. Understanding the Recoverable Depreciation clause is essential, as it outlines specific deadlines and requirements to secure your final payment and maximize your insurance coverage benefits after a loss.

Business Interruption Loss Partial Claim Denial and Coverage Explanation Letter

A partial claim denial letter occurs when an insurer approves only specific portions of a business interruption claim. This formal document explains the coverage limitations based on policy exclusions or a failure to prove actual financial loss directly caused by a covered peril. It is crucial to review the cited policy language and specific calculation methods used by the adjuster. Understanding these legal justifications allows policyholders to provide additional evidence or challenge the valuation through formal appeals to recover their full entitled benefits.

Pre-Existing Health Condition Partial Denial and Coverage Explanation Letter

A Pre-Existing Health Condition Partial Denial letter explains why specific medical expenses are excluded from your policy. It clarifies that while general coverage is active, treatments related to pre-existing conditions identified during underwriting are denied for a set period. Carefully review the waiting period and the specific diagnosis listed to ensure accuracy. If the exclusion is based on incorrect medical history, you have the right to appeal the decision by providing clinical evidence. Understanding these limitations is essential for managing out-of-pocket costs and navigating your healthcare benefits effectively.

Workers Compensation Treatment Partial Claim Denial and Coverage Explanation Letter

A Notice of Partial Denial is a critical document explaining which medical treatments or body parts are excluded from your claim. If you receive a Coverage Explanation Letter, review it immediately for the specific legal or medical reasons cited for the rejection. You have a limited timeframe to file an Adjudication of Claim or request an independent medical evaluation to dispute the decision. Understanding these documents is essential for ensuring your medical benefits remain active and that insurance carriers are held accountable for all work-related injuries.

Hail Damage Policy Limit Partial Denial and Coverage Explanation Letter

A coverage explanation letter clarifies why an insurer issued a partial denial of a hail damage claim. It typically distinguishes between functional damage and cosmetic issues, often citing a policy limit or specific exclusions like wear and tear. Policyholders must review the declarations page to understand how depreciation or specific endorsements affect the payout. If disagreement arises regarding the scope of repairs, homeowners should request a re-inspection or invoke the appraisal clause to challenge the insurer's assessment of the actual cash value versus replacement costs.

Specialty Equipment Valuation Partial Claim Denial and Coverage Explanation Letter

A Specialty Equipment Valuation letter explains why an insurance payout was lower than expected, often resulting in a partial claim denial. This document details specific coverage limitations, such as depreciation, policy sub-limits, or exclusions for high-value items. It is essential to review the valuation methodology used to determine the actual cash value versus replacement cost. Understanding these justifications allows policyholders to identify potential errors in appraisal or provide additional documentation to dispute the settlement amount and ensure fair compensation for specialized assets.

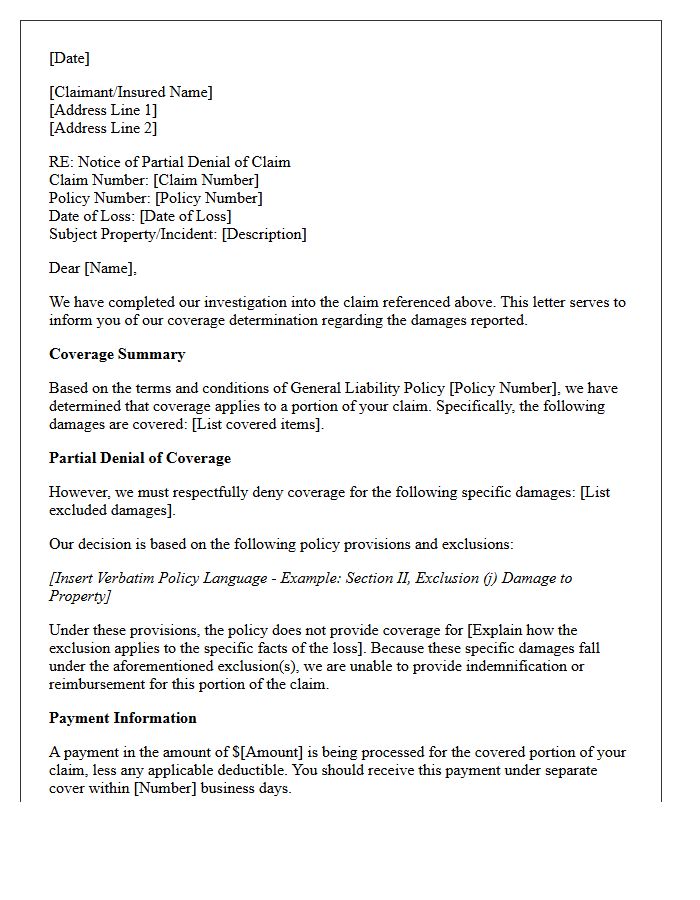

General Liability Excluded Damages Partial Denial and Coverage Explanation Letter

A partial denial letter clarifies that while some claims are covered, specific General Liability Excluded Damages are rejected based on policy terms. It is essential to verify the specific exclusions cited, such as intentional acts, contractual liabilities, or professional errors. This document serves as a formal Coverage Explanation Letter, detailing the insurer's legal rationale and your remaining obligations. Reviewing the Reservation of Rights section is critical, as it outlines how the insurer manages the defense while disputing certain costs, ensuring you understand the boundaries of your financial protection.

What is a partial claim denial?

A partial claim denial occurs when an insurance provider agrees to pay for certain portions of a claim while rejecting others based on specific policy exclusions, limits, or non-covered services.

How do I read a Coverage Explanation Letter?

A Coverage Explanation Letter (or Explanation of Benefits) details the total amount billed, the portion approved for payment, and the specific codes or reasons explaining why certain line items were denied or adjusted.

Why was part of my insurance claim denied?

Common reasons for partial denials include services deemed not medically necessary, charges exceeding the "Usual, Customary, and Reasonable" (UCR) rates, applied deductibles, or specific policy exclusions.

Can I appeal a partial claim denial?

Yes, you have the right to appeal any denied portion of a claim by submitting a formal letter of appeal along with supporting documentation, such as medical records or evidence of policy coverage, within the timeframe specified in your denial letter.

What should I do if my coverage explanation is unclear?

If the explanation codes in your letter are vague, contact your insurance provider's claims department to request a detailed breakdown of the denial and ask for the specific section of your policy language that supports their decision.

Comments