A Notice of Adverse Action is a mandatory document required by the Fair Credit Reporting Act (FCRA) when a consumer's credit report negatively impacts their application for credit, insurance, or employment. This legal notice ensures transparency and protects consumer rights by explaining the reasons for the denial. To help you comply with federal regulations, below are some ready to use template.

Image cover: Official FCRA Adverse Action Notice Templates and Compliance Guide

Letter Samples List

- Auto Insurance Premium Increase Adverse Action Letter

- Homeowners Policy Denial Fair Credit Reporting Act Letter

- Life Insurance Coverage Declination Notice Letter

- Renters Insurance Application Rejection Letter

- Insurance Policy Cancellation Consumer Report Letter

- Commercial Auto Underwriting Denial Notice Letter

- Personal Umbrella Policy Rate Adjustment Letter

- Motor Vehicle Report Adverse Action Notification Letter

- Comprehensive Loss Underwriting Exchange Report Denial Letter

- Credit-Based Insurance Score Rate Increase Letter

- Property Insurance Tier Downgrade Adverse Action Letter

- High-Risk Auto Insurance Coverage Rejection Letter

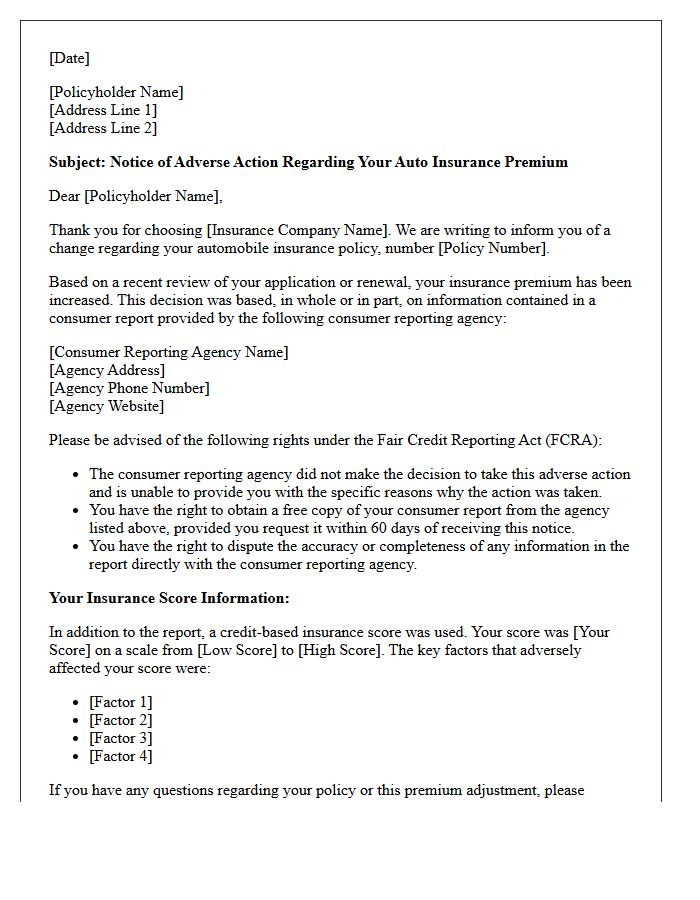

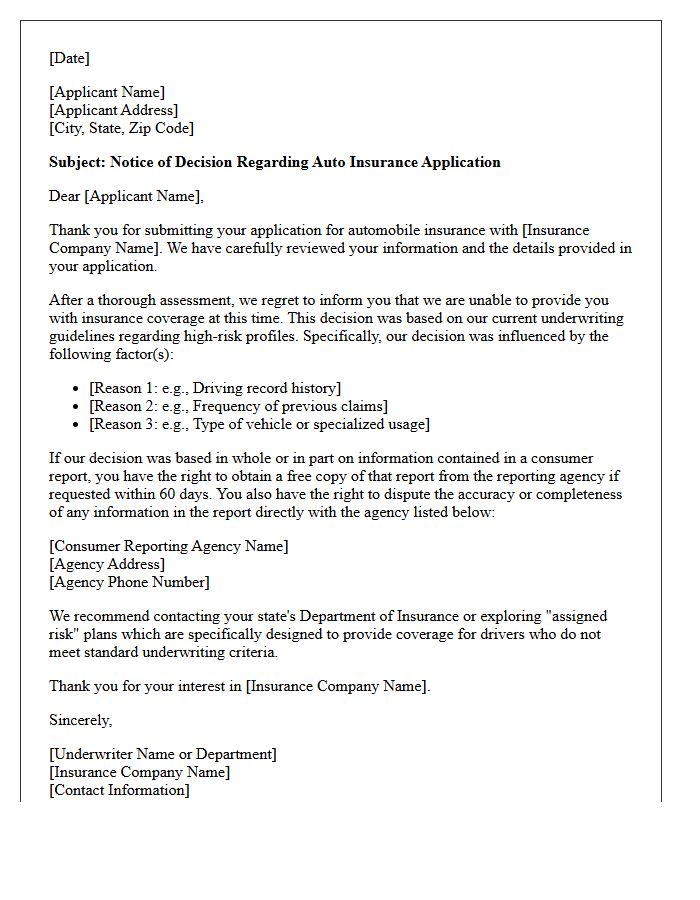

Auto Insurance Premium Increase Adverse Action Letter

An Adverse Action Letter is a mandatory notice sent by insurers when your auto insurance premium increases based on your credit report. Under the Fair Credit Reporting Act, companies must disclose if your financial history negatively impacted your rate. This document identifies the specific credit reporting agency used and provides instructions on how to obtain a free copy of your report. Reviewing this letter is essential to ensure your data is accurate and to understand the risk factors influencing your insurance costs.

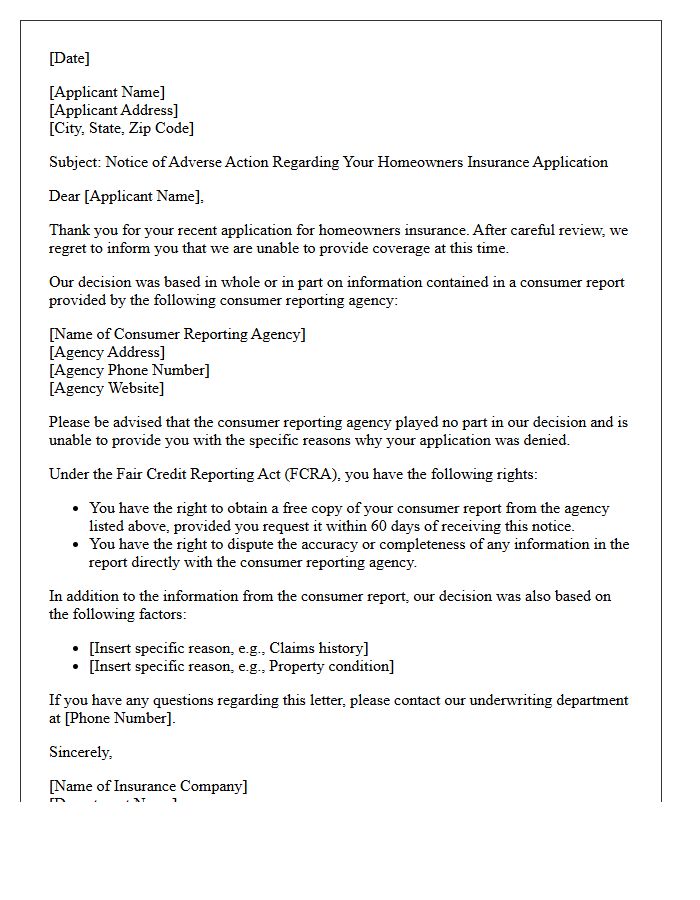

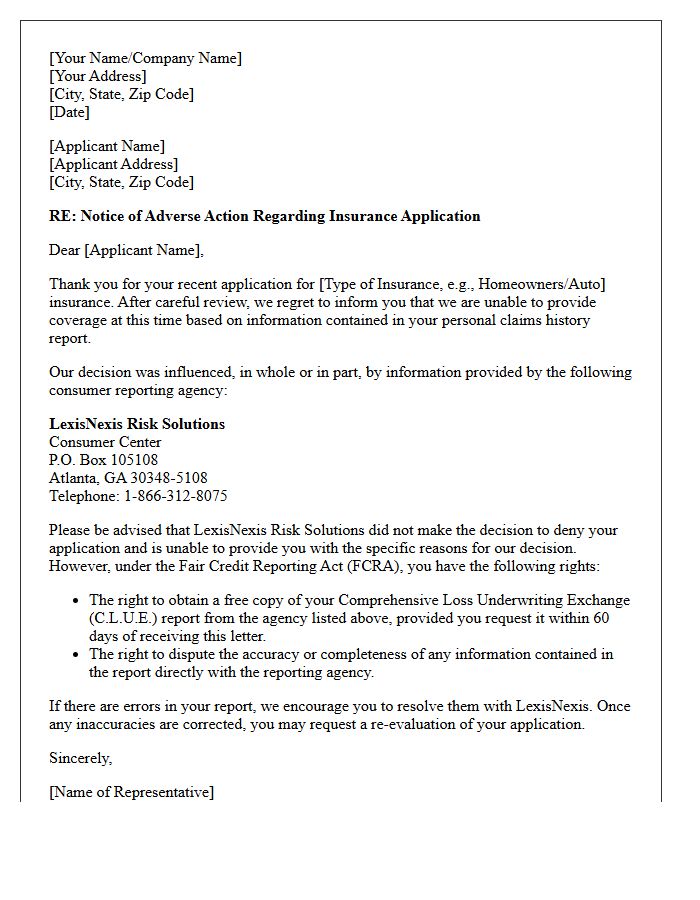

Homeowners Policy Denial Fair Credit Reporting Act Letter

When an insurer rejects your application based on external data, they must issue a Fair Credit Reporting Act (FCRA) letter. This adverse action notice is mandatory if information from a consumer reporting agency, such as a credit score or claims history report (CLUE), influenced the decision. You have the right to request a free copy of the underlying report to ensure its accuracy. Reviewing this document is essential to identify incorrect data or identity theft that may be unfairly increasing your premiums or preventing coverage approval.

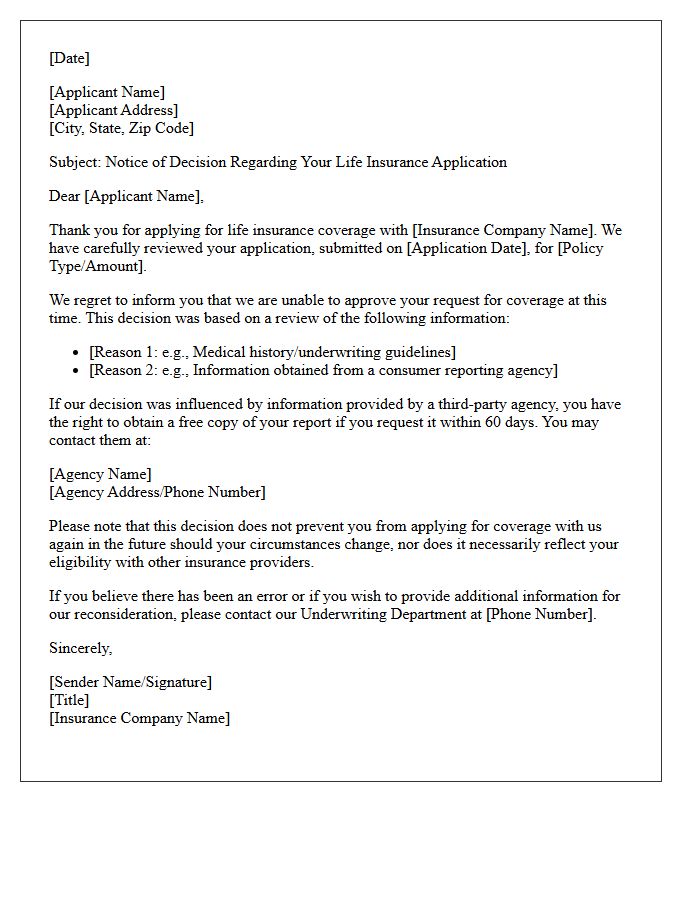

Life Insurance Coverage Declination Notice Letter

A Life Insurance Coverage Declination Notice Letter informs an applicant that their request for a policy was denied. The most common reason for adverse underwriting involves high-risk medical conditions or lifestyle factors. It is crucial to review the letter for the specific denial reason provided by the insurer. Under the Fair Credit Reporting Act, you have the right to dispute inaccuracies in your medical records. If denied, consider applying for simplified issue or guaranteed acceptance policies, which do not require a medical exam to provide essential financial protection.

Renters Insurance Application Rejection Letter

Receiving a renters insurance application rejection letter often stems from high-risk factors like a poor credit score, prior claims history, or unacceptable property conditions. Federal law requires insurers to provide an Adverse Action Notice if credit data influenced the decision. To move forward, review the letter carefully to identify the specific denial reason and verify your CLUE report for inaccuracies. Improving your credit standing or seeking specialized high-risk coverage providers are effective ways to secure protection for your personal belongings after an initial denial.

Insurance Policy Cancellation Consumer Report Letter

An Insurance Policy Cancellation Consumer Report Letter is a formal notification issued when a provider terminates coverage based on data from a consumer reporting agency. Under the Fair Credit Reporting Act, insurers must provide an adverse action notice explaining the specific reasons for cancellation, such as claims history or credit scores. This document is essential for transparency, allowing policyholders to dispute inaccuracies and understand how their personal data impacts insurance eligibility and premiums. Reviewing this letter promptly helps maintain continuous protection and ensures your financial profile remains accurate.

Commercial Auto Underwriting Denial Notice Letter

A Commercial Auto Underwriting Denial Notice is a legal document issued by an insurer explaining why a business vehicle policy application was rejected. Key reasons often include a poor Loss Runs history, high-risk driver profiles, or operating in restricted industries. It is essential to review the specific Adverse Action reasons cited to address safety gaps or data inaccuracies. Under the Fair Credit Reporting Act, businesses may have the right to dispute information used in the decision. Understanding these factors helps companies improve their risk profile for future insurance placements.

Personal Umbrella Policy Rate Adjustment Letter

A Personal Umbrella Policy Rate Adjustment Letter notifies policyholders of changes to their insurance premiums. This communication typically outlines adjustments based on updated risk assessments, inflation, or broader market trends. It is essential to review the letter to understand how these changes impact your liability coverage limits. If the new premium affects your budget, contact your agent to discuss deductible options or potential discounts. Maintaining this extra layer of protection ensures your assets remain shielded against major lawsuits or catastrophic claims despite fluctuating costs.

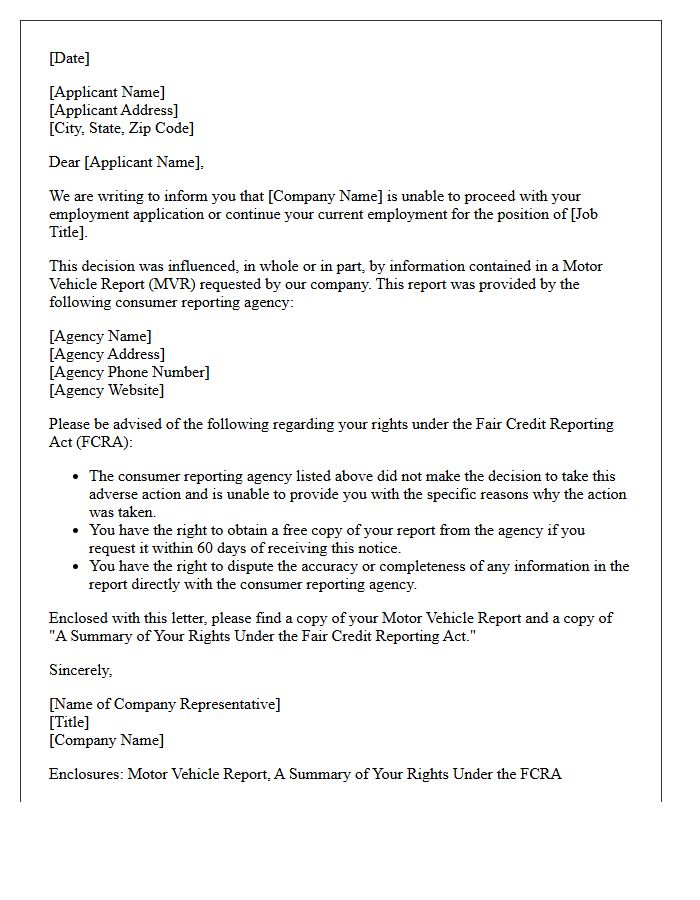

Motor Vehicle Report Adverse Action Notification Letter

A Motor Vehicle Report Adverse Action Notification Letter is a legal requirement under the Fair Credit Reporting Act (FCRA). If an employer or insurer denies an application based on a driving record, they must provide this formal notice. The letter informs the individual of the negative decision, identifies the consumer reporting agency used, and explains their right to dispute inaccuracies. Providing this document is a critical step in maintaining legal compliance and ensuring transparency during the background screening process to protect applicant rights.

Comprehensive Loss Underwriting Exchange Report Denial Letter

A Comprehensive Loss Underwriting Exchange (CLUE) denial letter informs you that an insurance company declined coverage or increased premiums based on your claims history. Managed by LexisNexis, this report contains seven years of personal property and auto data. Receiving a denial means specific risk factors or prior losses influenced their decision. You are legally entitled to a free copy of your CLUE report under the Fair Credit Reporting Act to verify accuracy. Reviewing it allows you to dispute errors or outdated information that may unfairly impact your insurability and rates.

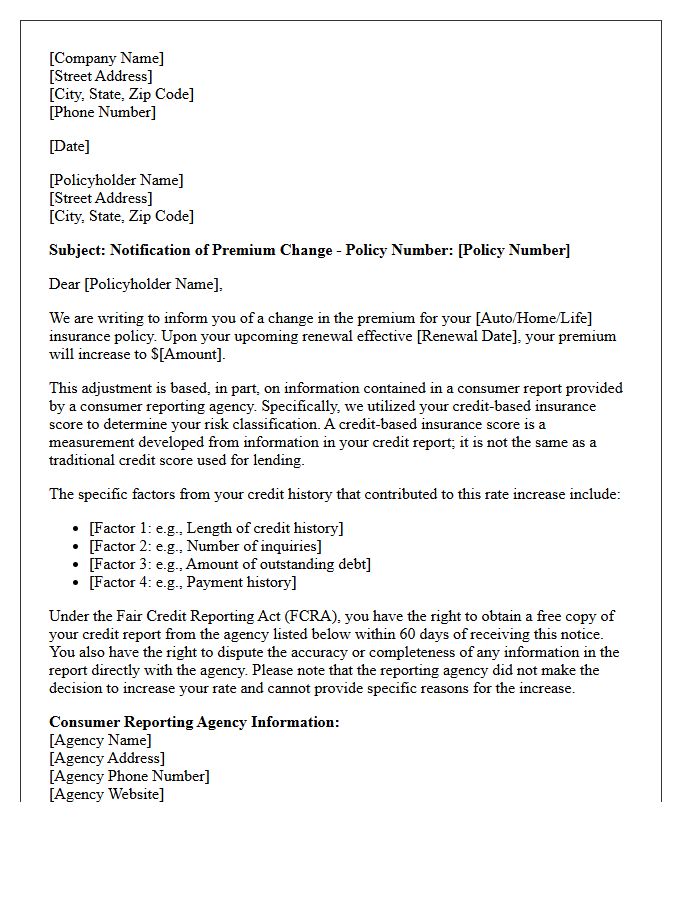

Credit-Based Insurance Score Rate Increase Letter

A credit-based insurance score rate increase letter notifies policyholders that their premiums have risen due to underwriting data linked to their financial history. This notice, required by the Fair Credit Reporting Act, explains that insurers use credit patterns to predict risk levels. It is important to review your credit report for inaccuracies, as improving your score can lead to lower future premiums. Receiving this letter does not mean your credit was rejected, but rather that it did not meet the threshold for the lowest possible insurance pricing tier.

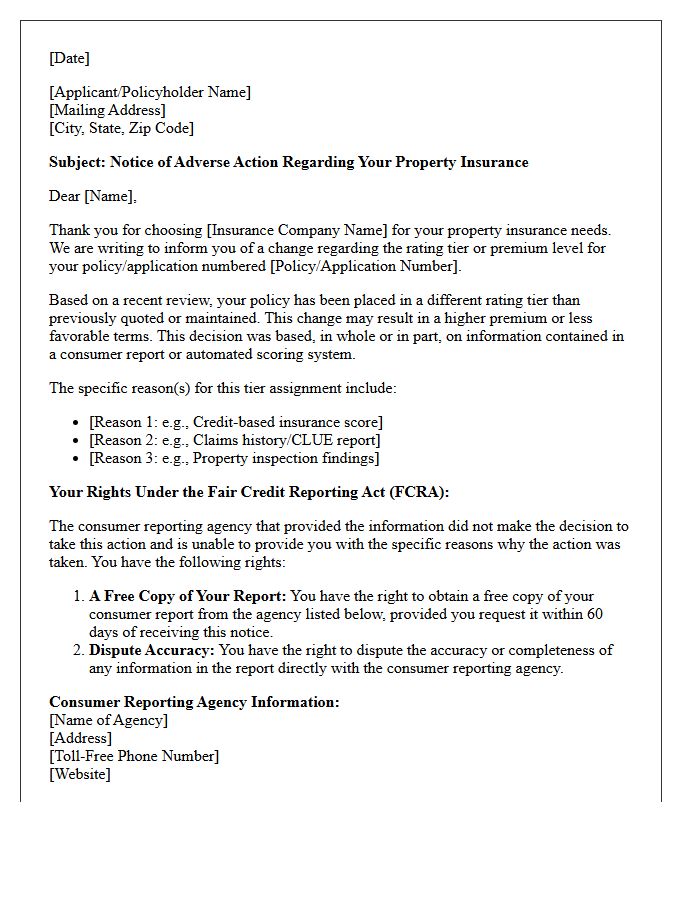

Property Insurance Tier Downgrade Adverse Action Letter

A Property Insurance Tier Downgrade Adverse Action Letter is a formal notice sent when an insurer places you in a higher-priced risk tier based on information in your consumer report. Under the Fair Credit Reporting Act, companies must disclose if your credit history or claims data resulted in less favorable premiums. This letter is crucial because it allows you to request a free copy of your report to verify accuracy. Reviewing these details is essential to ensure that erroneous data isn't unfairly increasing your insurance costs.

High-Risk Auto Insurance Coverage Rejection Letter

Receiving a high-risk auto insurance coverage rejection letter means an insurer has declined your application due to factors like a poor driving record, frequent claims, or non-payment history. This formal notice must legally state the specific reasons for denial. If rejected, you should verify the accuracy of your CLUE report and driving record. To secure legal protection, look for specialized non-standard carriers or explore assigned risk pools through your state's automobile insurance plan. Act quickly to avoid a coverage lapse, which can further increase future premiums.

What is a Notice of Adverse Action under the Fair Credit Reporting Act?

A Notice of Adverse Action is a formal communication required by the FCRA when a lender, employer, or business denies an application or takes a negative action against a consumer based on information found in a consumer report.

What information must be included in an FCRA adverse action notice?

The notice must include the name, address, and phone number of the consumer reporting agency that provided the report, a statement that the agency did not make the negative decision, and a notification of the consumer's right to obtain a free copy of the report and dispute its accuracy.

Why did I receive an adverse action notice after applying for credit?

You received this notice because the creditor used information from your credit report-such as a low credit score, late payments, or high debt levels-as a reason to deny your application or offer less favorable terms.

Can an adverse action notice be delivered verbally?

While the FCRA allows for oral or electronic notification, most businesses provide written notices to ensure compliance and provide the consumer with a clear record of the specific credit reporting agency used and their legal rights.

How long do I have to request a free credit report after receiving an adverse action notice?

Under the Fair Credit Reporting Act, you have 60 days from the date you receive the adverse action notice to request a free copy of your consumer report from the agency cited in the letter.

Comments