Enhance your customer retention and provide comprehensive protection by offering Critical Illness coverage to your existing health insurance clients. This cross-sell strategy helps bridge the gap between medical expenses and lost income during health crises. Strengthening client loyalty starts with proactive communication and personalized solutions. To help you get started, below are some ready to use template.

Image cover: Protecting Your Future: Critical Illness Insurance Options for Valued Policyholders

Letter Samples List

- Health Insurance Client Critical Illness Cross-Sell Letter

- Financial Protection and Critical Illness Cross-Sell Letter

- Out of Pocket Expenses Critical Illness Coverage Letter

- Family Security and Critical Illness Insurance Letter

- Annual Policy Review Critical Illness Cross-Sell Letter

- Heart Attack and Cancer Critical Illness Protection Letter

- Health Insurance Gap Critical Illness Proposal Letter

- Existing Client Critical Illness Exclusive Offer Letter

- Peace of Mind Critical Illness Policy Upgrade Letter

- Medical Risk Awareness Critical Illness Cross-Sell Letter

- Rising Healthcare Costs Critical Illness Advisory Letter

- High Deductible Plan Critical Illness Supplement Letter

- Open Enrollment Critical Illness Addition Letter

- Focus on Recovery Critical Illness Benefit Letter

Health Insurance Client Critical Illness Cross-Sell Letter

A health insurance cross-sell letter for critical illness coverage must emphasize financial protection against life-altering diagnoses like cancer or stroke. Start by acknowledging the client's current policy to build trust, then highlight the coverage gap left by standard medical plans. Focus on the lump-sum payment feature, which provides immediate cash for non-medical expenses and lost income. Clear calls-to-action and simplified enrollment steps are essential to improve conversion rates. Ultimately, the message should shift the focus from basic healthcare to comprehensive wealth preservation during a medical crisis.

Financial Protection and Critical Illness Cross-Sell Letter

A financial protection cross-sell letter is a strategic tool designed to offer critical illness coverage to existing policyholders. This communication highlights the risk of unexpected health crises and provides a safety net for medical costs or lost income. By addressing gaps in current plans, the letter emphasizes financial security and long-term stability. The goal is to provide a seamless insurance upgrade that ensures clients are fully protected against life-altering diagnoses, offering peace of mind through comprehensive and personalized risk management solutions tailored to individual needs.

Out of Pocket Expenses Critical Illness Coverage Letter

An Out of Pocket Expenses Critical Illness Coverage Letter is a vital document confirming your insurance provider will reimburse non-medical costs associated with a severe diagnosis. It outlines specific limits for travel, lodging, and caregiver support not covered by standard health plans. Understanding these provisions ensures financial stability during recovery by bridging the gap between medical bills and daily living costs. Always verify the claim submission requirements and benefit triggers to maximize your policy's utility during a health crisis.

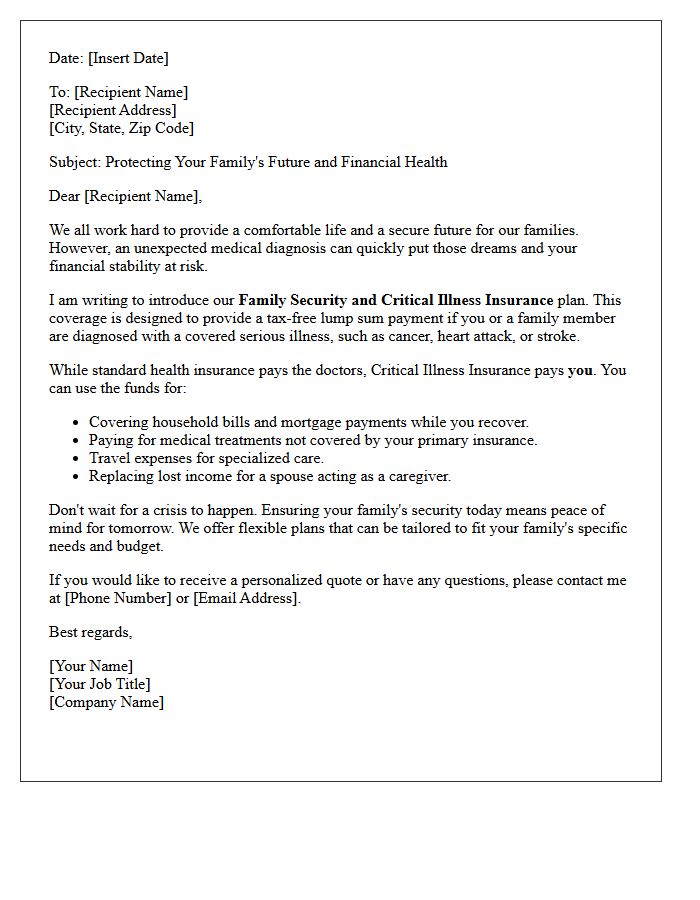

Family Security and Critical Illness Insurance Letter

A Family Security and Critical Illness Insurance Letter provides financial protection by offering a lump-sum payment upon the diagnosis of a covered life-threatening condition. This ensures your loved ones can manage medical expenses and daily costs during recovery. It is essential to review the specific policy exclusions and waiting periods outlined in your document. Having this coverage guarantees long-term stability, allowing you to focus on health rather than debt. Always verify the beneficiary details to ensure your family remains secure during unexpected medical emergencies.

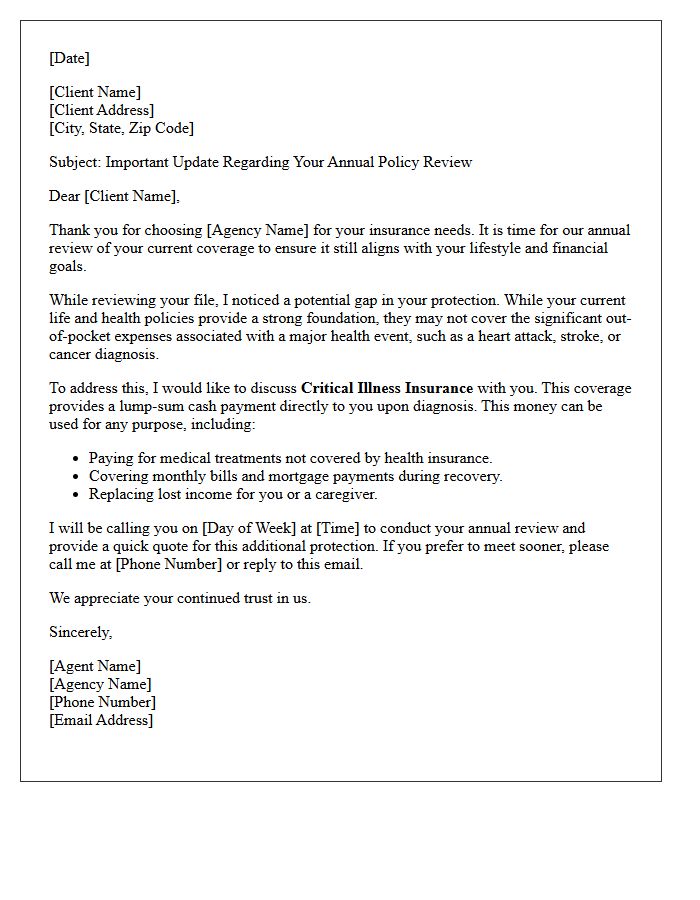

Annual Policy Review Critical Illness Cross-Sell Letter

An Annual Policy Review offers a strategic opportunity to strengthen client protection through a Critical Illness Cross-Sell Letter. This communication highlights potential coverage gaps during life transitions, demonstrating proactive risk management. By emphasizing how supplemental benefits provide financial security during a health crisis, agents can increase policyholder retention and drive revenue. A well-crafted letter transforms a routine administrative check-in into a personalized value proposition, ensuring clients remain fully insured against unforeseen medical expenses while building long-term professional trust.

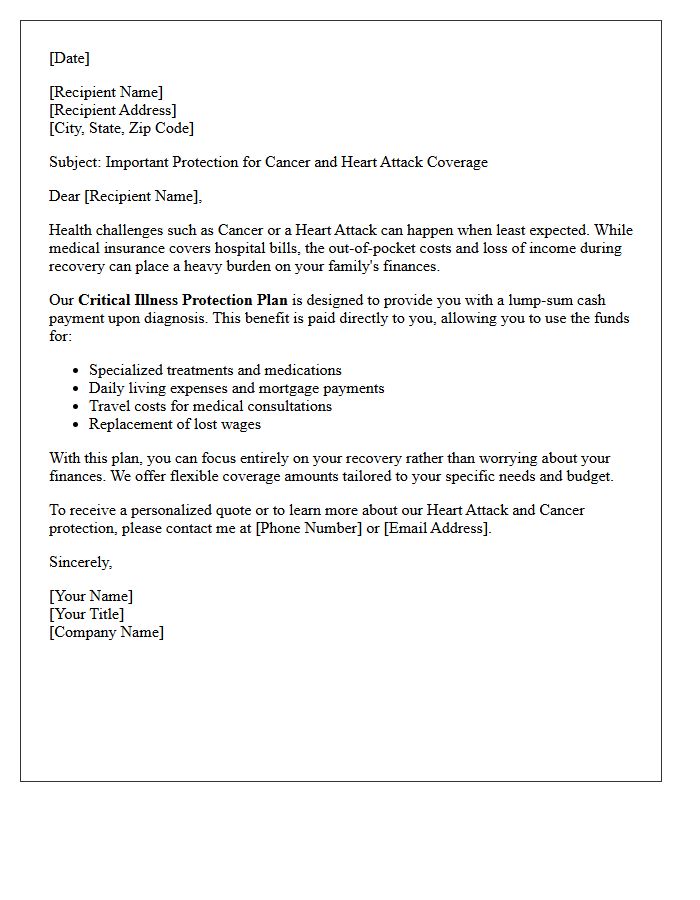

Heart Attack and Cancer Critical Illness Protection Letter

A Critical Illness Protection Letter provides a lump-sum cash payment upon the diagnosis of life-threatening conditions like heart attack or cancer. Unlike standard health insurance, this benefit is paid directly to the policyholder to cover non-medical costs, such as mortgage payments, lost income, or specialized recovery care. It ensures financial stability during a health crisis, allowing patients to focus entirely on recuperation without the burden of debt. Understanding the specific definitions and waiting periods within your policy is essential to guarantee comprehensive coverage when you need it most.

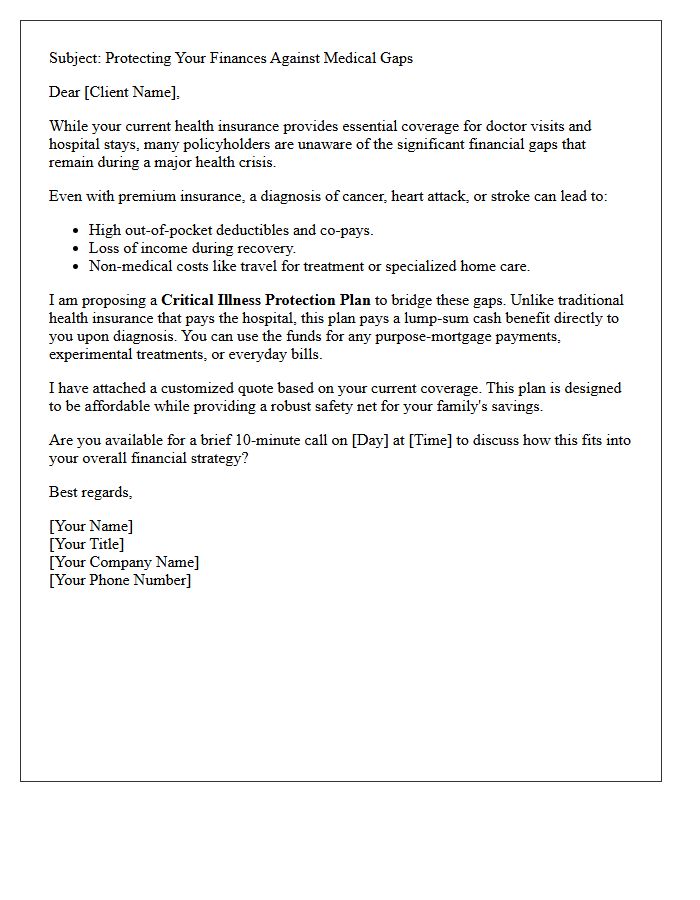

Health Insurance Gap Critical Illness Proposal Letter

A health insurance gap proposal highlights why standard coverage is insufficient for major medical events. This letter emphasizes how critical illness insurance provides a lump-sum cash benefit upon diagnosis of life-altering conditions like cancer or stroke. Unlike traditional plans, these funds cover non-medical costs, including mortgage payments and lost wages. By addressing the financial vulnerability caused by high deductibles, the proposal offers a strategic solution to ensure total recovery without depleting personal savings. It is a vital tool for achieving comprehensive financial security during a health crisis.

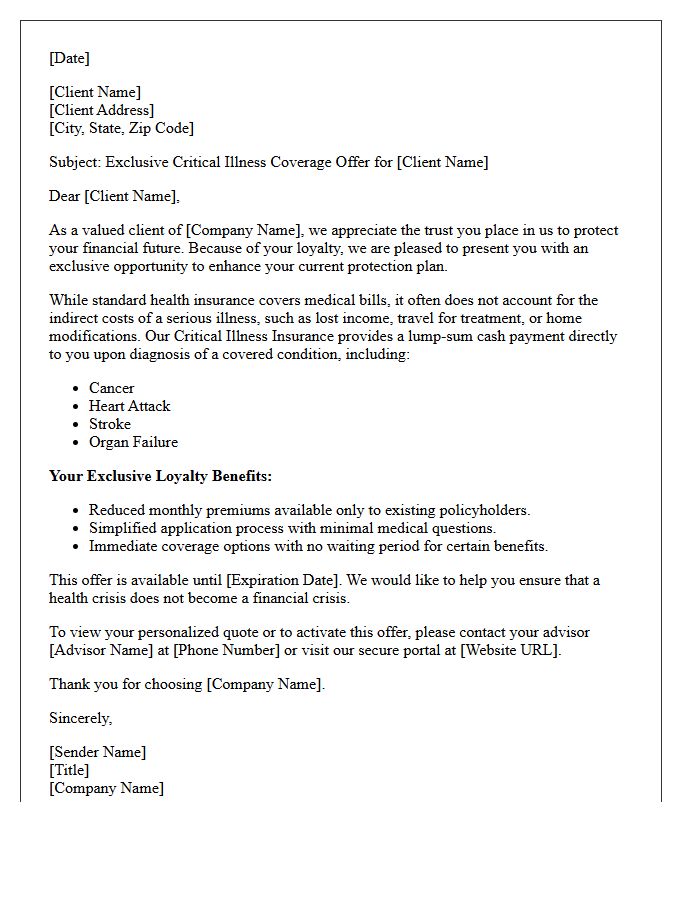

Existing Client Critical Illness Exclusive Offer Letter

The Existing Client Critical Illness Exclusive Offer Letter is a specialized invitation providing policyholders with a guaranteed opportunity to enhance their financial protection. This limited-time promotion often features preferential premium rates and simplified underwriting, allowing you to increase coverage without extensive medical exams. It is designed to bridge the protection gap for life-threatening conditions like cancer or heart disease. Reviewing this document promptly is essential, as the exclusive benefits and discounted pricing are typically subject to strict deadlines tailored specifically for loyal, pre-existing members of the insurance provider.

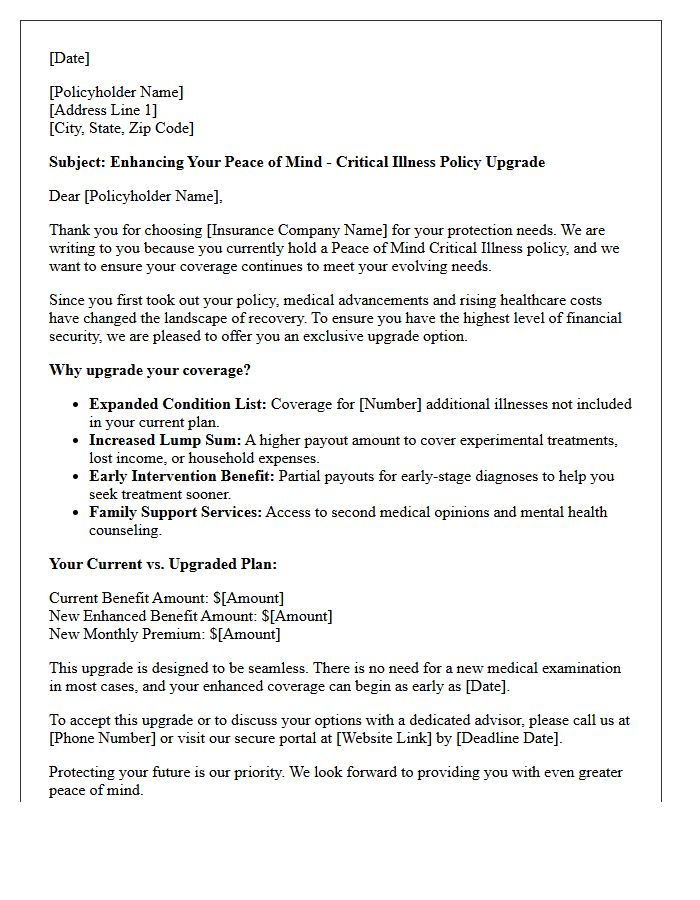

Peace of Mind Critical Illness Policy Upgrade Letter

A Peace of Mind Critical Illness Policy Upgrade Letter is a formal notification offering enhanced coverage options for your existing insurance. It is crucial to review these documents as they often include new protections for modern medical conditions and increased benefit amounts. This upgrade ensures your financial security remains robust against rising healthcare costs. Carefully compare the premium adjustments against the expanded safety net to maintain optimal financial protection. Responding promptly allows you to secure comprehensive health safeguards without the need for entirely new medical underwriting in many cases.

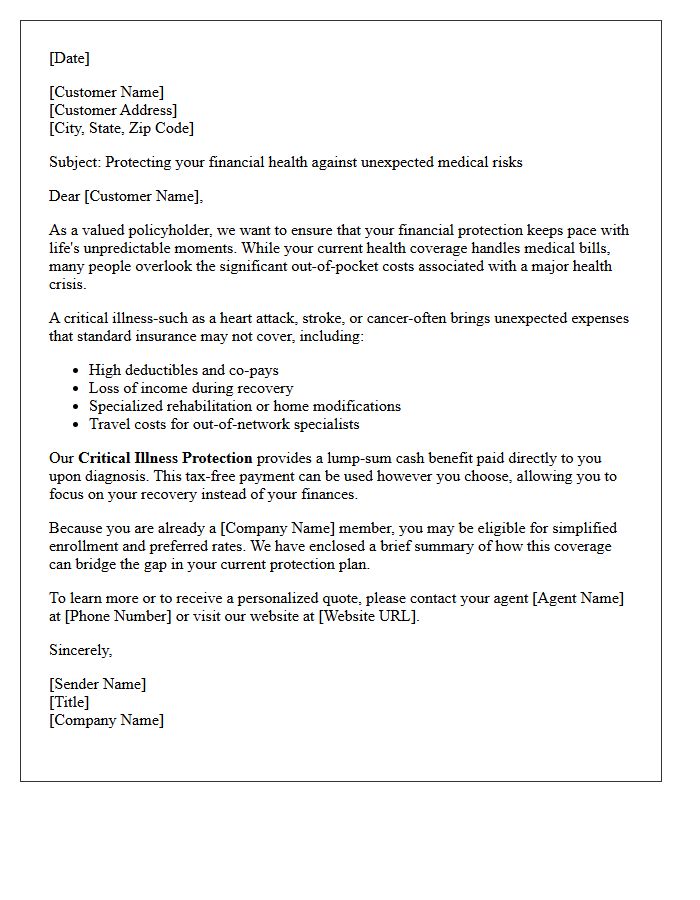

Medical Risk Awareness Critical Illness Cross-Sell Letter

A medical risk awareness letter is a strategic cross-sell tool designed to educate clients about potential financial gaps. It highlights how a critical illness policy provides a necessary lump-sum benefit upon diagnosis of life-altering conditions like cancer or heart attack. By focusing on risk mitigation, the communication emphasizes that standard health insurance often fails to cover non-medical costs and lost income. This targeted approach improves financial protection for policyholders while increasing retention and portfolio diversification for providers through proactive education on health-related financial vulnerabilities.

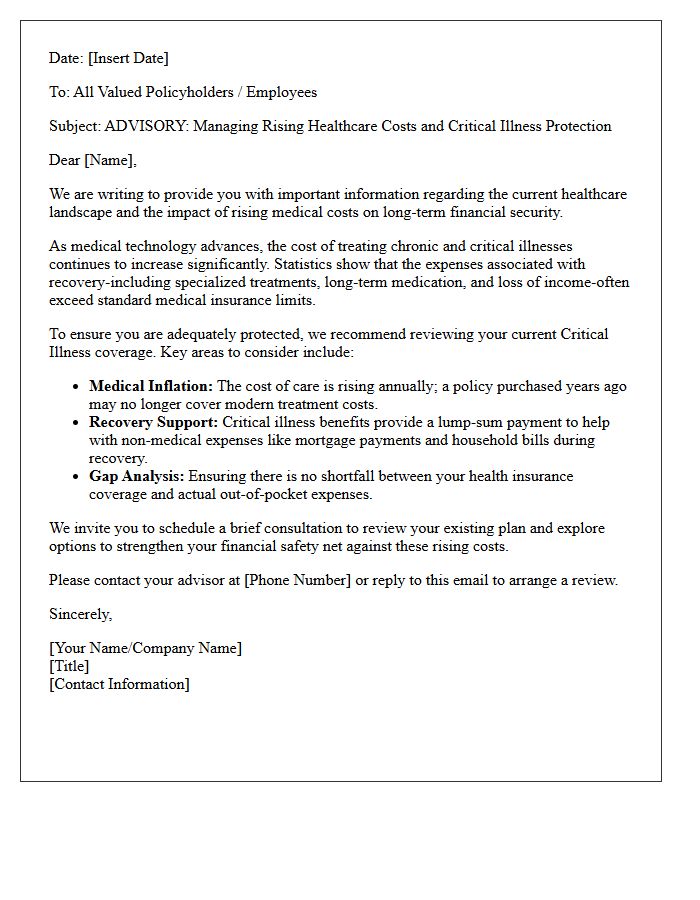

Rising Healthcare Costs Critical Illness Advisory Letter

The Rising Healthcare Costs Critical Illness Advisory Letter serves as a vital notification regarding escalating medical expenses. It highlights the financial vulnerability associated with chronic conditions and life-threatening diagnoses. This document outlines how inflation and advanced treatments impact insurance premiums and out-of-pocket limits. Understanding this advisory is essential for risk management, ensuring individuals maintain adequate coverage to prevent medical debt. By reviewing these updates, policyholders can adjust their supplemental protection strategies to safeguard personal assets against the growing economic burden of long-term healthcare delivery and specialized recovery services.

High Deductible Plan Critical Illness Supplement Letter

A High Deductible Plan Critical Illness Supplement Letter is a vital document used to verify supplemental coverage for specific health events. Since high deductible plans have significant out-of-pocket costs, this letter confirms an additional policy is active to provide lump-sum cash benefits upon diagnosis of serious conditions like cancer or heart attack. It ensures that financial protection is in place to cover the deductible gap, protecting your savings during a medical crisis. Always keep this official notification with your primary insurance records for streamlined claims processing.

Open Enrollment Critical Illness Addition Letter

An Open Enrollment Critical Illness Addition Letter notifies employees of the opportunity to supplement their benefits package. This document highlights the voluntary insurance coverage designed to provide lump-sum cash payments upon diagnosis of specific life-threatening conditions like cancer or heart attacks. Understanding these supplemental benefits is essential during the enrollment window, as they help cover out-of-pocket medical costs and daily expenses. Carefully review the policy limits and premium rates to ensure financial protection against unexpected health crises before the deadline expires.

Focus on Recovery Critical Illness Benefit Letter

The Recovery Critical Illness Benefit Letter serves as official verification of your insurance claim approval. This document confirms the lump-sum payment issued to support financial stability during recuperation. It outlines the specific illness covered, the total benefit amount, and any potential impacts on future policy coverage. Retaining this letter is essential for personal financial records and tax documentation purposes. Ensure all personal details and diagnosis information align with your medical records to guarantee a smooth distribution of funds during your recovery journey.

What is critical illness insurance and how does it supplement my existing health plan?

Critical illness insurance provides a tax-free, lump-sum cash payment upon the diagnosis of a covered condition, such as cancer, heart attack, or stroke. While your standard health insurance pays doctors and hospitals for medical treatments, this coverage pays you directly to help cover lost income, high deductibles, or experimental treatments not covered by your primary policy.

Why should I consider a critical illness policy if I already have comprehensive health insurance?

Even with comprehensive health insurance, a major medical emergency can lead to significant out-of-pocket costs and lifestyle disruptions. Critical illness insurance fills the financial gap by providing funds for non-medical expenses like mortgage payments, childcare, or specialized transportation, ensuring that a physical recovery doesn't result in financial ruin.

Which specific medical conditions are covered under this policy?

The policy typically covers life-altering diagnoses including, but not limited to, invasive cancer, heart attack, stroke, major organ transplants, and end-stage renal failure. For a complete list of covered conditions and specific definitions, please refer to your personalized benefit summary included with this letter.

How can I use the lump-sum payout if my claim is approved?

There are no restrictions on how you use your benefit payout. Once the lump sum is issued, you have full control over the funds. You may use them to pay off your health insurance deductible, cover household bills during your recovery, or pay for out-of-network specialists and rehabilitation services.

Will adding this coverage increase my monthly premium significantly?

Critical illness insurance is designed to be an affordable addition to your existing health portfolio. Because the coverage is supplemental, premiums are often much lower than primary health insurance. Your specific rate will be based on your age and the amount of coverage you select, and it can often be conveniently bundled with your current health insurance billing.

Comments