Managing overdue accounts requires professional communication to maintain positive client relationships. A Late Payment Grace Period Notice serves as a friendly reminder, offering clients a short window to settle their debts before penalties apply. This approach encourages timely resolution while preserving trust and future business opportunities. To help you streamline your billing process, below are some ready to use template options.

Image cover: Professional Grace Period Notice Templates for Overdue Payments

Letter Samples List

- Initial Auto Insurance Late Payment Grace Period Notice Letter

- Standard Life Insurance Premium Grace Period Letter

- Final Grace Period Expiration Warning Letter for Homeowners Insurance

- Commercial Policy Late Payment Grace Period Advisory Letter

- Health Insurance Premium Past Due Grace Period Letter

- General Agency Grace Period Notice and Reinstatement Letter

- Friendly Reminder Grace Period Letter for Long Term Care Insurance

- Urgent Premium Payment Required Grace Period Extension Letter

- Workers Compensation Policy Grace Period Alert Letter

- Notice of Pending Cancellation and Grace Period Letter

- Umbrella Policy Late Premium Grace Period Notification Letter

- Agency Client Retention and Grace Period Payment Letter

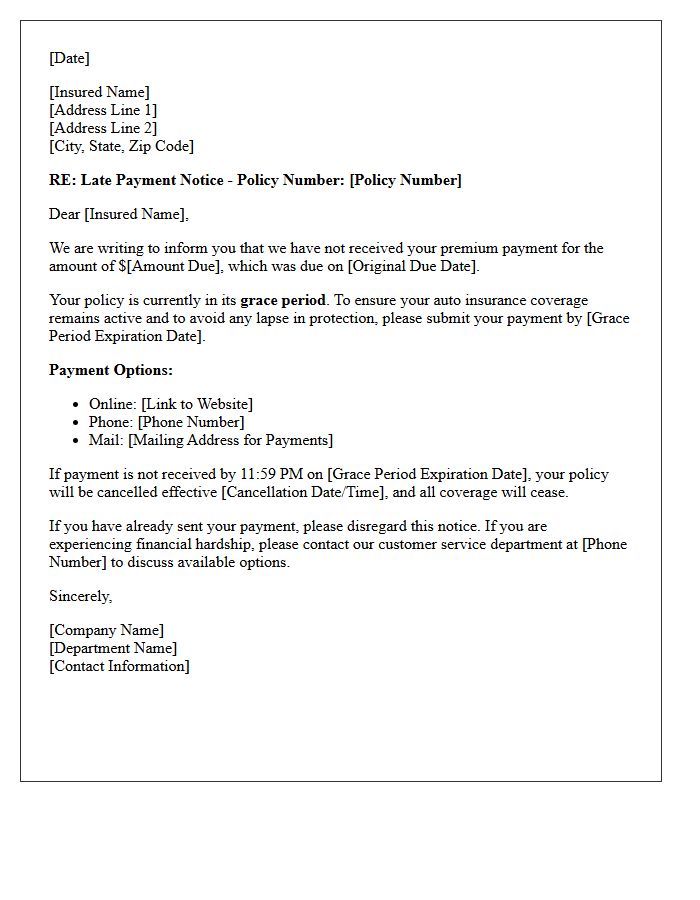

Initial Auto Insurance Late Payment Grace Period Notice Letter

An Initial Auto Insurance Late Payment Grace Period Notice Letter serves as a formal alert that your premium is overdue. This legal notification outlines the specific grace period, which is the additional time granted to pay before your policy faces cancellation. It is crucial to settle the balance immediately to avoid a lapse in coverage, which can lead to higher future rates and legal penalties. Always verify the termination date mentioned to ensure your vehicle remains continuously protected under your active insurance agreement.

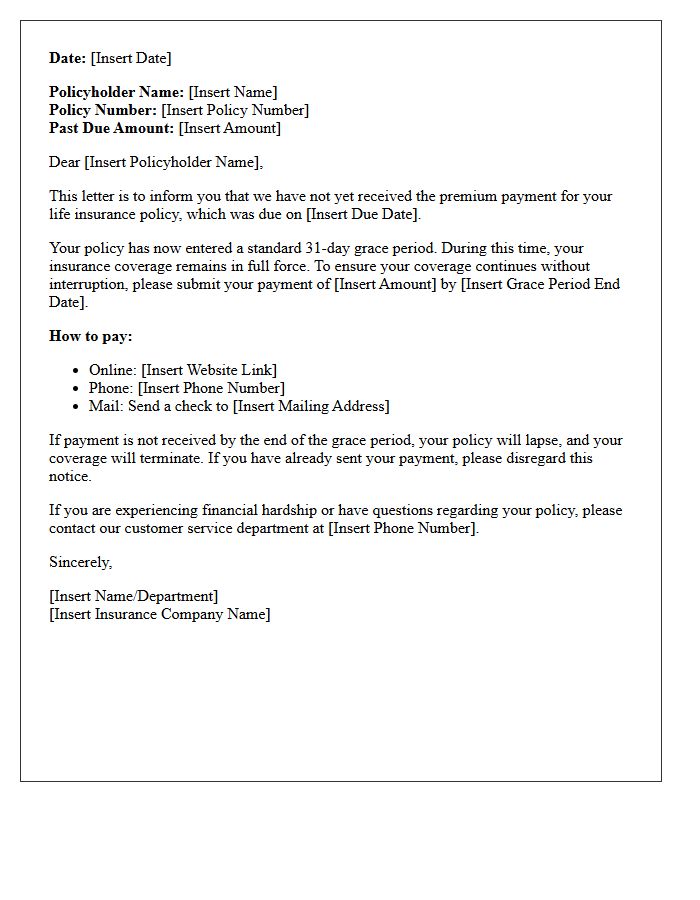

Standard Life Insurance Premium Grace Period Letter

The Standard Life Insurance Premium Grace Period Letter is a formal notice sent to policyholders when a payment is missed. It informs you that your coverage remains active during a statutory grace period, typically lasting 30 to 31 days. This document outlines the final deadline to settle the outstanding balance to prevent a policy lapse. Receiving this letter is a critical warning; failing to pay before the period expires results in the loss of death benefits and potentially requires a complex medical reinstatement process.

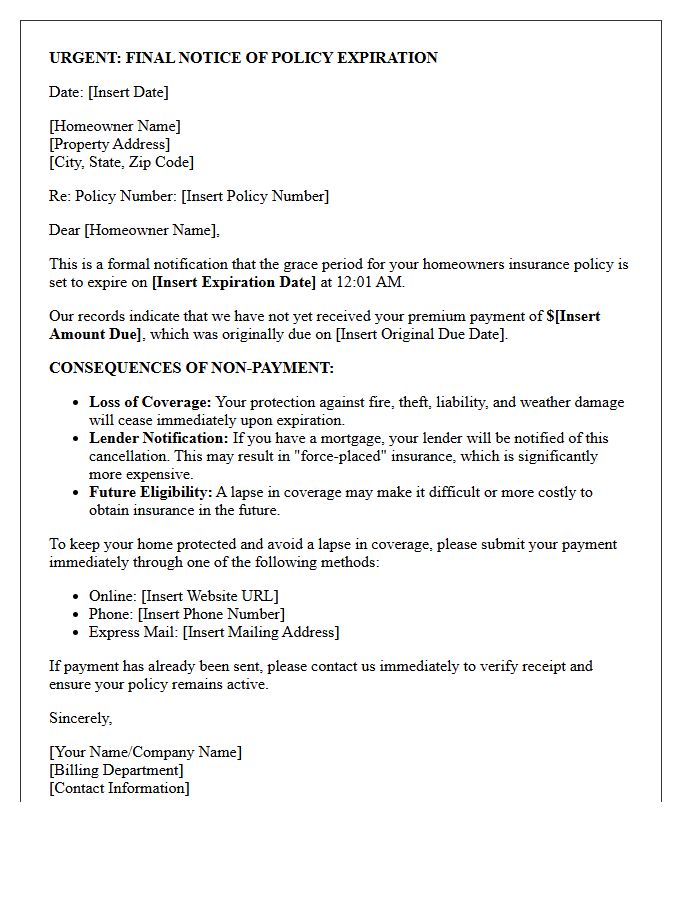

Final Grace Period Expiration Warning Letter for Homeowners Insurance

A final grace period expiration warning letter is a critical notice from your insurer. It serves as your last opportunity to settle an unpaid premium before your homeowners insurance policy faces permanent cancellation. If coverage lapses, you lose financial protection against disasters and risk being in default of your mortgage agreement. To avoid a forced-placed policy or higher future rates, you must submit the required payment immediately. Always contact your agent to confirm receipt and ensure your property remains continuously insured without any gap in protection.

Commercial Policy Late Payment Grace Period Advisory Letter

A Commercial Policy Late Payment Grace Period Advisory Letter is a formal notification informing policyholders of an upcoming or missed premium deadline. It highlights the grace period, which is the specific duration coverage remains active before a policy lapses due to non-payment. This document serves as a critical legal notice to prevent unintended termination of business insurance. Understanding the payment terms and final expiration date mentioned in the letter is essential to maintain continuous protection and avoid costly reinstatements or gaps in essential liability coverage.

Health Insurance Premium Past Due Grace Period Letter

Receiving a grace period letter means your health insurance premium is past due. Under the Affordable Care Act, individuals receiving subsidies typically have a 90-day window to pay outstanding balances before coverage is terminated. However, those without subsidies may only have 30 days. During this time, your insurer may pend claims. To avoid a permanent loss of coverage and potential tax penalties, you must pay the full amount owed before the deadline specified in the notice. Acting quickly ensures continuous access to medical services and prevents policy cancellation.

General Agency Grace Period Notice and Reinstatement Letter

A General Agency Grace Period Notice informs policyholders of an overdue premium, granting a specific timeframe to pay before coverage lapses. If payment is missed, the policy terminates, requiring a Reinstatement Letter to restore protection. This formal request often necessitates a statement of good health or proof of insurability. Acting promptly during the grace period is essential to avoid a gap in coverage and ensure continuous financial security without the need for new underwriting or increased premium rates.

Friendly Reminder Grace Period Letter for Long Term Care Insurance

A friendly reminder letter notifies policyholders that a premium payment is overdue. This document initiates a mandatory grace period, typically lasting 30 to 65 days, ensuring your coverage remains active while you resolve the balance. To prevent a permanent policy lapse, it is crucial to update payment details or designate a third party for secondary notifications. Reviewing this notice immediately protects your long-term care insurance benefits, ensuring financial security and continued access to essential healthcare services when you need them most.

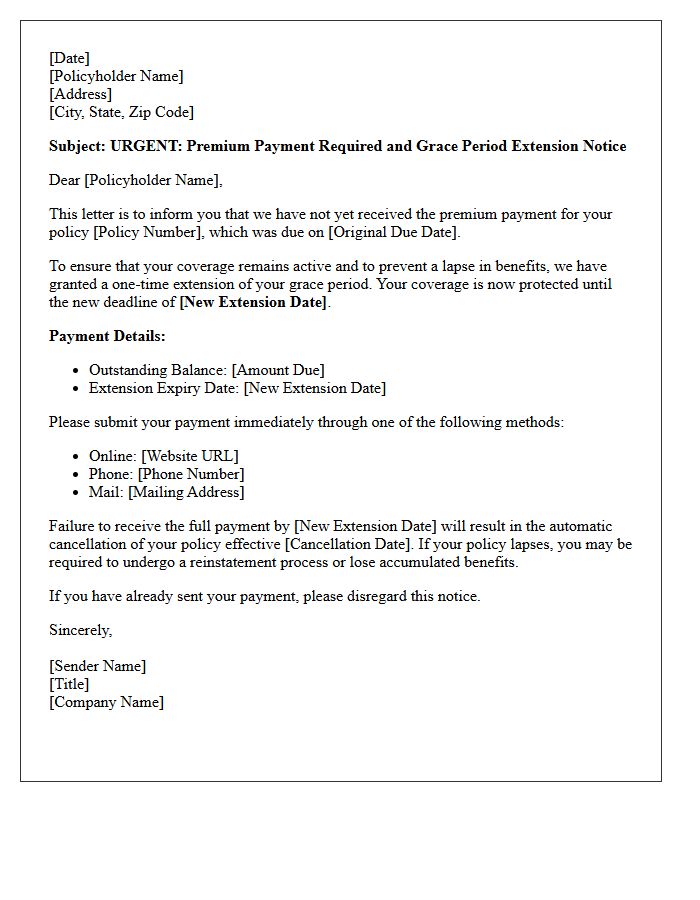

Urgent Premium Payment Required Grace Period Extension Letter

An Urgent Premium Payment Required notice informs policyholders that their insurance coverage is at risk of cancellation due to overdue balances. To prevent a lapse in protection, a Grace Period Extension Letter may be issued, providing additional time beyond the original deadline to settle the debt. It is vital to pay the outstanding amount immediately within this extended timeframe to maintain active policy benefits and avoid legal or financial gaps. Always confirm the specific extension dates to ensure your continuous coverage remains secure and uninterrupted.

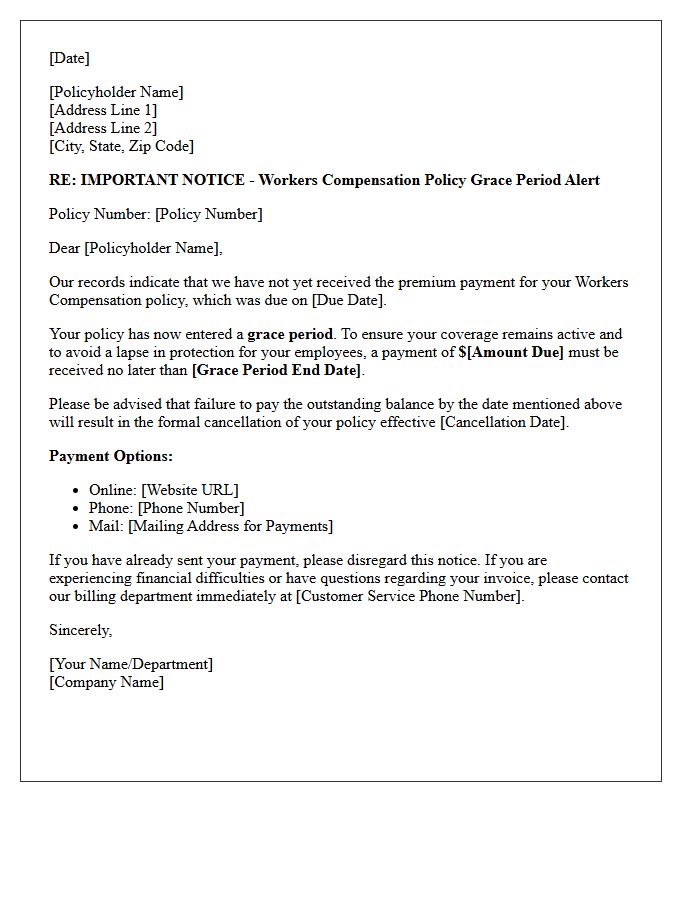

Workers Compensation Policy Grace Period Alert Letter

A Workers Compensation Policy Grace Period Alert Letter serves as a critical final notice regarding overdue premiums. This document warns employers that their insurance coverage is at risk of immediate cancellation due to non-payment. It is essential to settle the outstanding balance before the specified deadline to maintain legal compliance and protect employees. Failing to act during this window can lead to a lapse in coverage, resulting in severe state penalties, personal liability for workplace injuries, and significantly higher future insurance rates. Always prioritize payment to ensure continuous business protection.

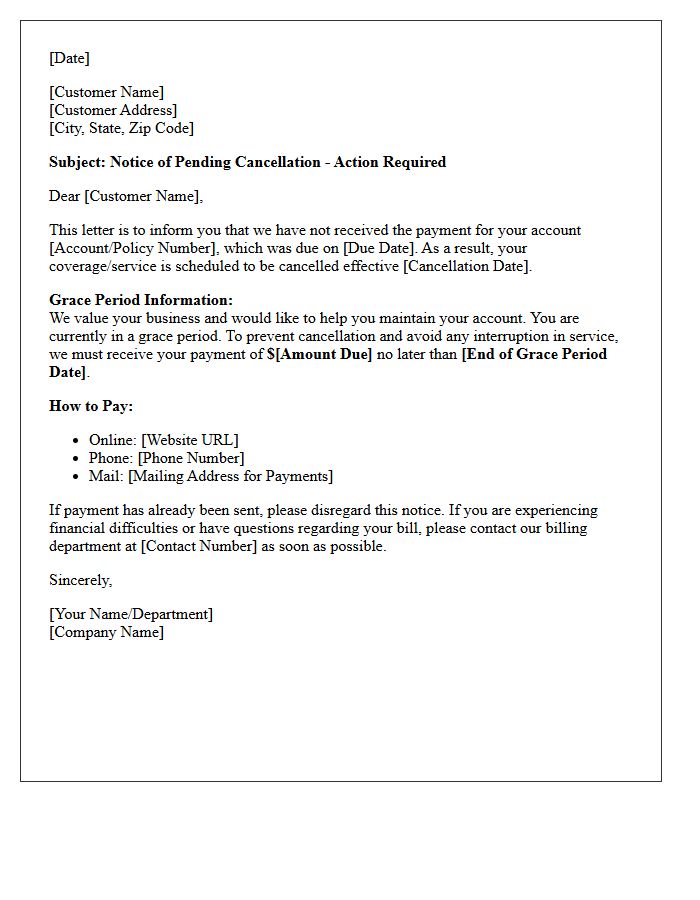

Notice of Pending Cancellation and Grace Period Letter

A Notice of Pending Cancellation is a formal alert indicating your insurance coverage will terminate due to unpaid premiums. It marks the start of a grace period, which is a state-mandated timeframe allowing you to settle the balance without losing protection. To prevent a lapse in coverage and potential financial risk, you must ensure payment is received before the specified deadline. Reviewing this document immediately is essential to understand the exact termination date and avoid the legal consequences of being uninsured.

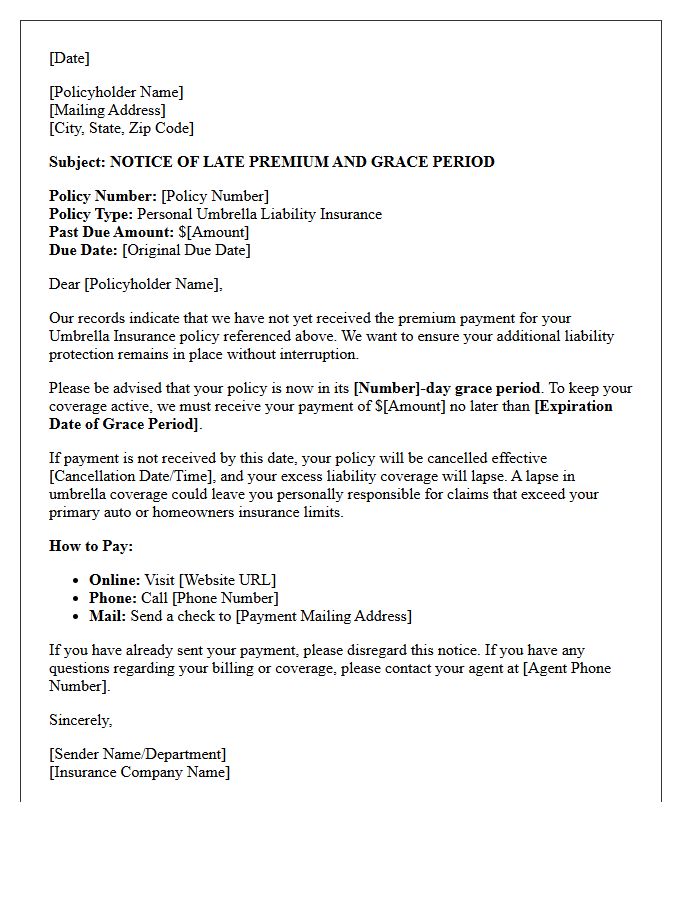

Umbrella Policy Late Premium Grace Period Notification Letter

An Umbrella Policy Late Premium Grace Period Notification Letter serves as a formal warning that your excess liability coverage is at risk of cancellation due to non-payment. This document outlines the grace period, which is the specific timeframe allowed to submit payment before the policy terminates. It is crucial to act immediately, as a lapse in coverage can leave your primary assets exposed to massive legal claims. Ensure you verify the termination date and payment instructions to maintain your financial protection and prevent a permanent gap in your insurance history.

Agency Client Retention and Grace Period Payment Letter

An Agency Client Retention Letter is a strategic communication designed to prevent churn by reinforcing service value. When a payment is missed, including a grace period notice is essential for maintaining professional rapport. This letter should clearly outline the extended deadline, outstanding balance, and available payment methods to ensure business continuity. By offering a flexible timeline before suspending services, agencies demonstrate empathy and build long-term loyalty, effectively reducing involuntary turnover while securing necessary revenue through proactive and transparent client management.

What is a late payment grace period?

A late payment grace period is a specified window of time after the official due date during which a payment can be submitted without incurring late fees or negative credit reporting. This period acts as a buffer for customers to settle their accounts before penalties are applied.

How long is the standard grace period for late payments?

The length of a grace period varies by industry and contract, but typically ranges from 5 to 15 calendar days. For example, many mortgage lenders provide a 15-day window, while credit card issuers and utility providers may offer shorter periods or none at all depending on local regulations.

Will a payment made during the grace period affect my credit score?

Generally, payments made within the grace period will not impact your credit score. Most creditors only report delinquencies to credit bureaus once the payment is a full 30 days past the original due date, regardless of the internal grace period for late fees.

Are late fees charged if I pay within the grace period?

No, the primary purpose of a grace period is to waive late fees. As long as the full payment is received and processed before the grace period expires, you will not be charged a penalty; however, interest may still accrue on the balance during this time for certain types of loans.

What happens if I miss the deadline of the grace period?

Once the grace period expires, the payment is considered officially delinquent. This usually results in the immediate assessment of late fees, a potential increase in interest rates (penalty APR), and the risk of the account being reported as late to credit agencies if it remains unpaid for 30 days.

Comments