An Addition of Named Insured Endorsement Letter is a formal request to extend your policy's liability coverage to another party. This legal amendment ensures the added entity receives the same protections and rights as the primary policyholder. Clearly outlining the relationship and effective date is essential for valid processing. To simplify your correspondence, below are some ready to use template options.

Image cover: Official Request Templates for Adding a Named Insured to Your Policy

Letter Samples List

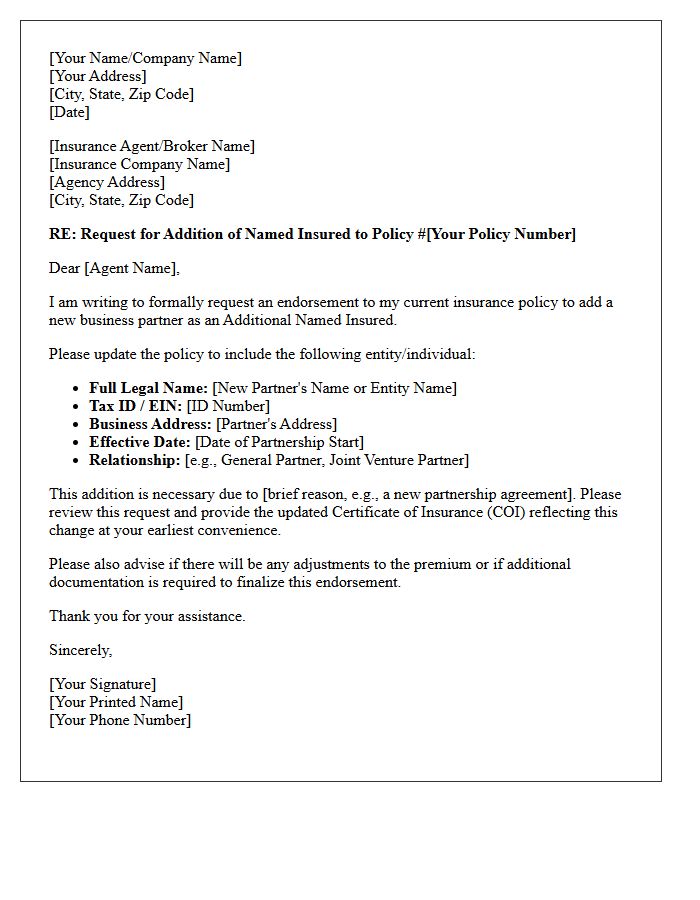

- Addition Of Named Insured Endorsement Letter For New Business Partner

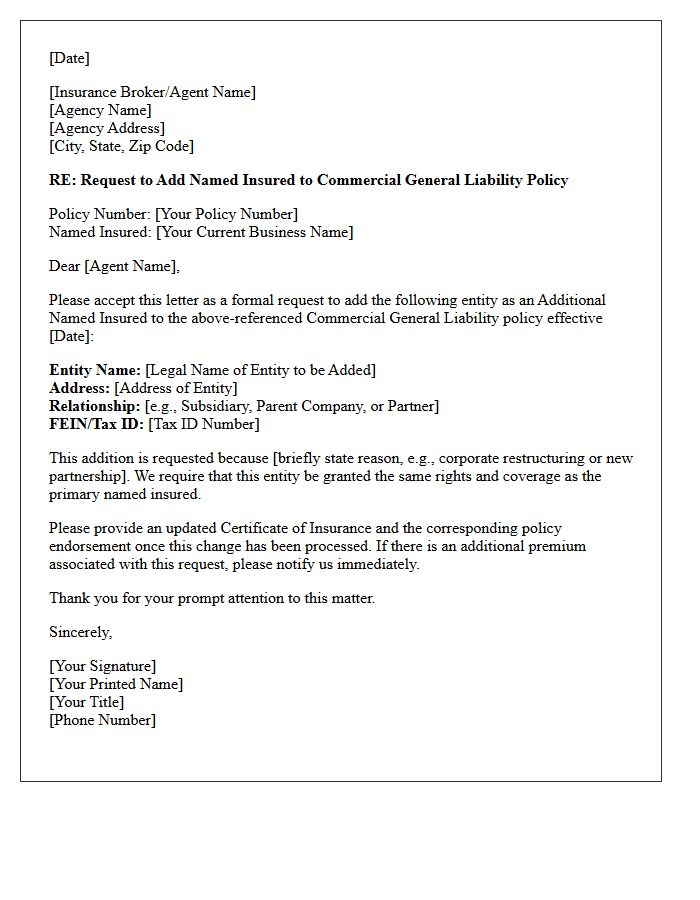

- Commercial General Liability Addition Of Named Insured Endorsement Letter

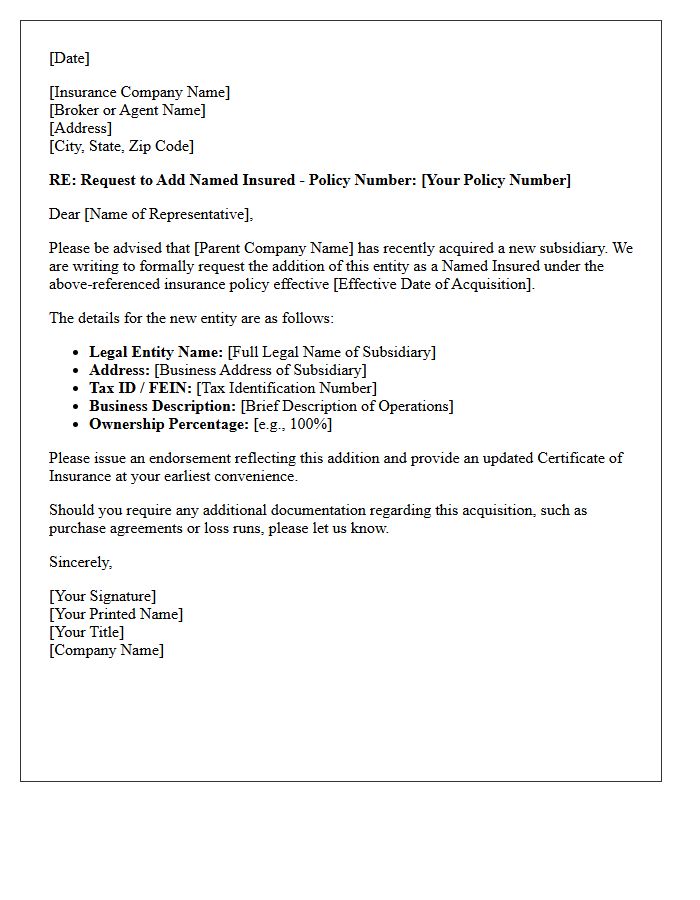

- Addition Of Named Insured Endorsement Letter For Newly Acquired Subsidiary

- Personal Auto Addition Of Named Insured Endorsement Letter For Spouse

- Addition Of Named Insured Endorsement Letter For Corporate Parent Company

- Commercial Property Addition Of Named Insured Endorsement Letter For Trust

- Addition Of Named Insured Endorsement Letter For Joint Venture Agreement

- Workers Compensation Addition Of Named Insured Endorsement Letter

- Addition Of Named Insured Endorsement Letter For Property Management Company

- Cyber Liability Addition Of Named Insured Endorsement Letter For Affiliate

- Addition Of Named Insured Endorsement Letter For Merged Corporate Entity

- Errors And Omissions Addition Of Named Insured Endorsement Letter For Contractor

Addition Of Named Insured Endorsement Letter For New Business Partner

When forming a strategic alliance, issuing an Addition of Named Insured Endorsement Letter is critical for risk management. This legal document modifies an existing insurance policy to extend full coverage benefits to a new business partner. It ensures that all parties share the same liability protections and defense costs under a single policy. Properly documenting this endorsement prevents gaps in coverage, maintains contractual compliance, and safeguards shared assets against unforeseen claims during collaborative operations. Always verify that the endorsement specifically names the entity to validate their insured status.

Commercial General Liability Addition Of Named Insured Endorsement Letter

A Commercial General Liability Addition of Named Insured Endorsement is a critical legal amendment that extends full policy benefits to another entity. Unlike a standard certificate, this endorsement letter legally modifies the insurance contract, granting the new party equal rights to defense and indemnity. It is essential for protecting subsidiaries or business partners against shared liabilities. Verifying the specific language ensures that the coverage is primary and non-contributory, preventing gaps in protection during legal disputes or third-party claims. Always confirm the effective date to maintain continuous liability coverage.

Addition Of Named Insured Endorsement Letter For Newly Acquired Subsidiary

The Addition of Named Insured Endorsement is a critical document that extends liability coverage to a newly acquired subsidiary. It ensures the parent company's insurance policy recognizes the new entity as a protected party, preventing significant coverage gaps during mergers or acquisitions. Policyholders must provide timely written notification to the insurer to trigger this endorsement. Failure to formalize this addition can leave the subsidiary's assets and operations exposed to uninsured legal claims and financial losses. Always verify the effective date to maintain continuous protection across all corporate branches.

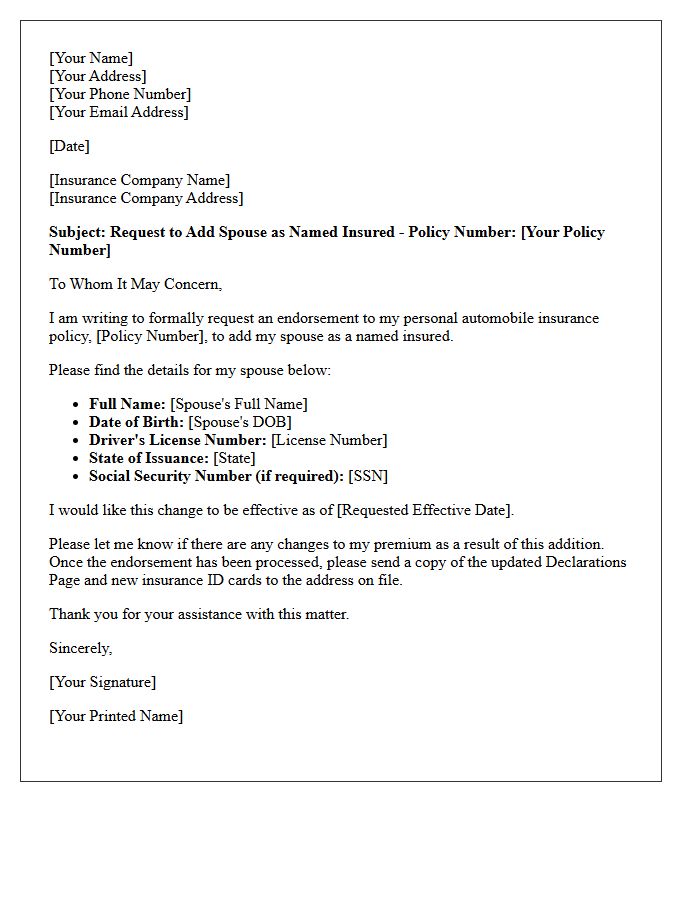

Personal Auto Addition Of Named Insured Endorsement Letter For Spouse

A personal auto policy amendment adds a spouse as a named insured to ensure comprehensive coverage. This endorsement is crucial because it grants the spouse equal rights, such as policy management and direct liability protection. Without being explicitly named, a spouse may face limitations regarding coverage extensions or notice of cancellations. Sending a formal endorsement letter ensures the insurance carrier updates the declarations page, maintaining seamless financial protection for both drivers under a single shared policy. Always verify that both individuals meet the underwriting requirements to avoid potential gaps in protection.

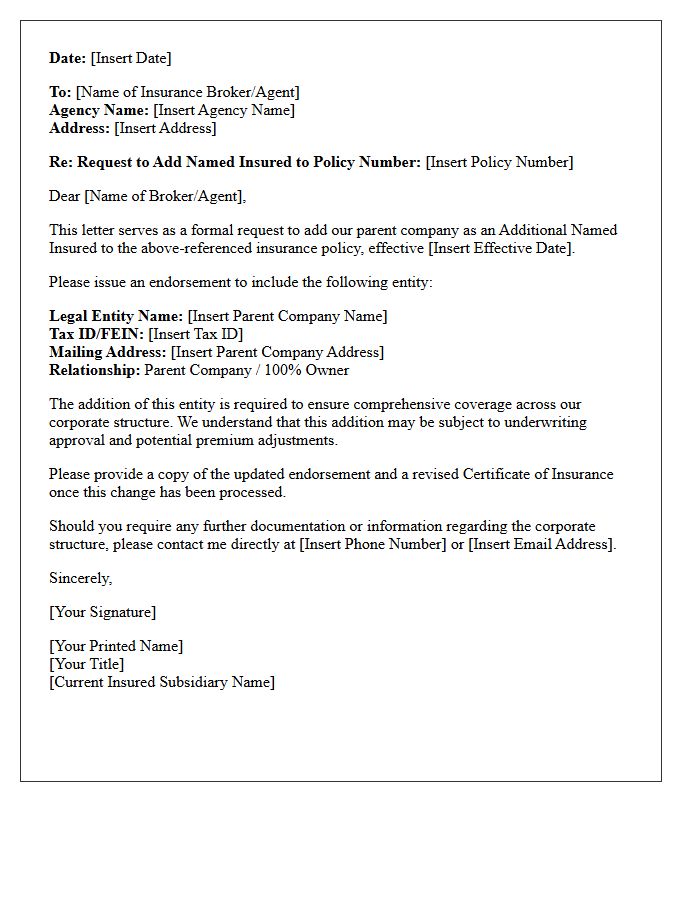

Addition Of Named Insured Endorsement Letter For Corporate Parent Company

An Addition of Named Insured Endorsement is a critical legal amendment that extends comprehensive liability coverage from a subsidiary's policy to its corporate parent company. This letter ensures the parent entity receives the same defense and indemnity protections as the primary policyholder. It is essential for maintaining corporate risk management and satisfying contractual requirements. By formalizing this relationship, businesses prevent coverage gaps and ensure that the ultimate holding company is shielded from financial losses arising from the subsidiary's operations or localized legal liabilities.

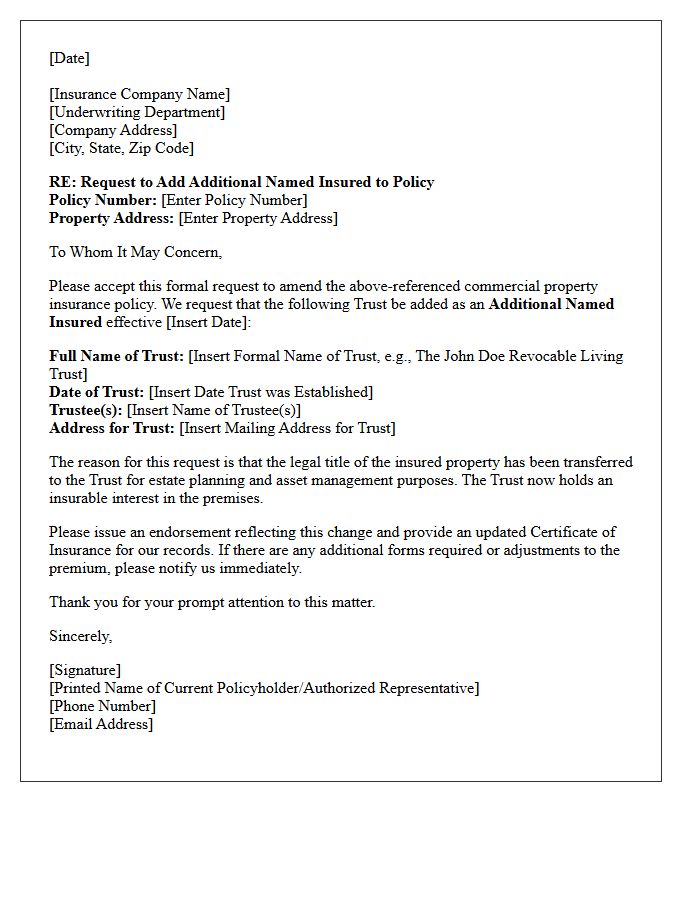

Commercial Property Addition Of Named Insured Endorsement Letter For Trust

When transferring commercial property into a trust, a Named Insured Endorsement is essential to maintain seamless liability and property coverage. This formal letter requests the insurer to add the trust entity and its trustees as additional insureds. Properly updating the policy prevents coverage gaps, ensuring the trust receives the same legal protections as the original owner. It is crucial to provide the full legal name of the trust and effective dates to guarantee that claims involving trust-held assets remain valid and fully indemnified under the existing insurance contract.

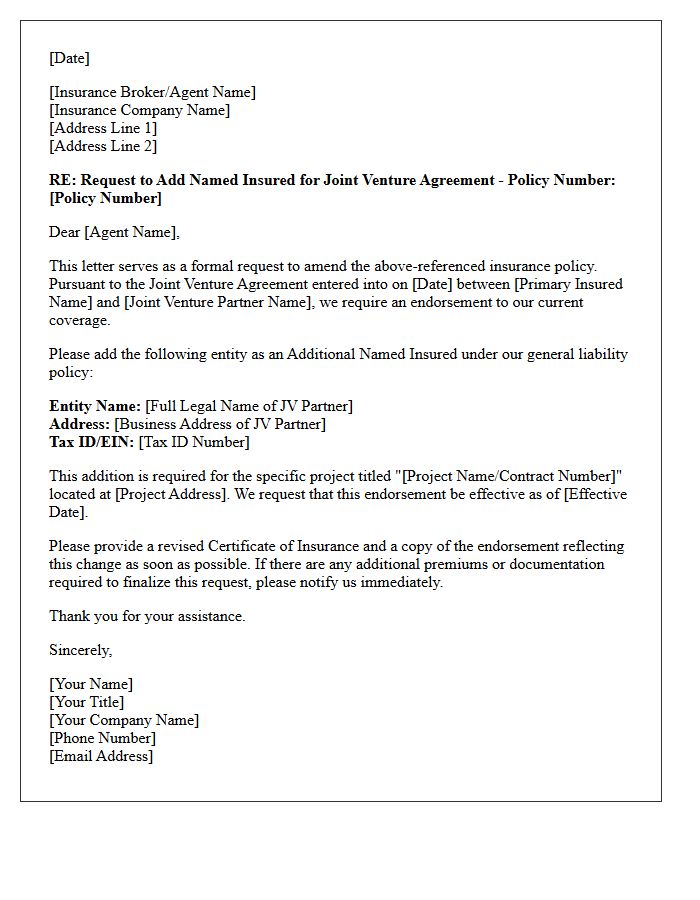

Addition Of Named Insured Endorsement Letter For Joint Venture Agreement

An Addition of Named Insured Endorsement is a critical amendment to a general liability policy within a joint venture. This letter formally extends comprehensive coverage to all partners involved in the specific project. It ensures that every legal entity in the agreement receives the same liability protection and defense rights as the primary policyholder. Securing this endorsement is essential to prevent coverage gaps, maintain contractual compliance, and shield individual assets from shared operational risks. Always verify that the endorsement language explicitly references the Joint Venture Agreement to guarantee full legal indemnification.

Workers Compensation Addition Of Named Insured Endorsement Letter

A Workers Compensation Addition of Named Insured Endorsement is a formal legal amendment that extends policy coverage to include additional business entities under a single primary policy. This letter ensures that all listed subsidiaries or affiliates receive the same liability protections and benefits as the main policyholder. It is vital for maintaining regulatory compliance and preventing coverage gaps during audits. Proper documentation confirms that the insurer recognizes the new entity, thereby protecting the entire corporate structure from unforeseen workplace injury claims and potential legal liabilities.

Addition Of Named Insured Endorsement Letter For Property Management Company

An Addition of Named Insured Endorsement is a vital legal document that extends full liability and property coverage from a landlord's insurance policy to the property management company. Unlike a standard additional insured status, this designation grants the manager equal rights and protections under the policy. It ensures the manager is defended against third-party lawsuits and property damage claims arising from daily operations. Securing this endorsement is a contractual necessity to mitigate financial risks and ensure seamless indemnification for the management firm while overseeing the owner's investment assets.

Cyber Liability Addition Of Named Insured Endorsement Letter For Affiliate

A Cyber Liability Addition of Named Insured Endorsement is a formal amendment that extends your insurance coverage to include an affiliate or subsidiary. This letter confirms that the added entity shares the same policy protections against data breaches and digital threats. It is crucial to ensure the affiliate's specific risk profile is disclosed to prevent coverage gaps. Once the underwriter approves the request, the endorsement ensures that both the parent company and the affiliate are legally recognized as Named Insureds, providing comprehensive financial protection for shared digital assets and network security liabilities.

Addition Of Named Insured Endorsement Letter For Merged Corporate Entity

The Addition of Named Insured Endorsement is critical for maintaining seamless liability protection following a corporate merger. This legal document formally extends the existing policy coverage to include the merged corporate entity as a primary insured party. Failing to issue this endorsement can lead to significant gaps in coverage and denied claims for actions involving the newly integrated firm. It ensures that all legal liabilities and operational risks of the combined organization are recognized by the carrier, preserving financial security and regulatory compliance across the entire enterprise.

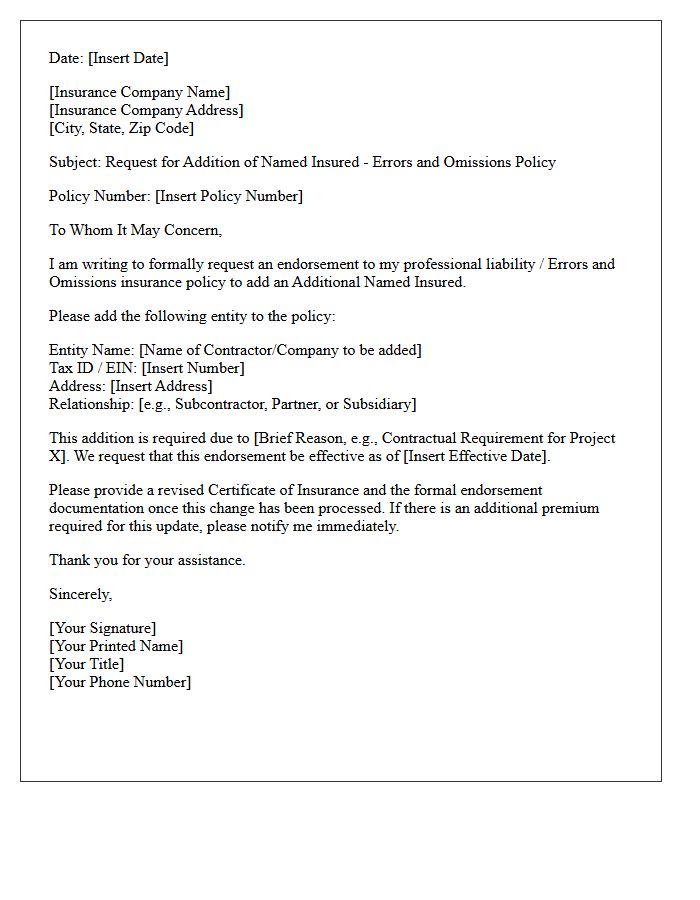

Errors And Omissions Addition Of Named Insured Endorsement Letter For Contractor

An Errors and Omissions (E&O) Addition of Named Insured Endorsement is a vital legal document that extends professional liability coverage to specific parties. For contractors, this letter modifies the policy to include additional entities, such as project owners or subcontractors, under their existing insurance protections. This ensures all named parties are shielded against financial losses resulting from professional negligence, mistakes, or service failures. Obtaining this endorsement is often a mandatory contractual requirement to mitigate risk and provide comprehensive indemnity during complex construction projects.

What is an Addition of Named Insured Endorsement Letter?

An Addition of Named Insured Endorsement Letter is a formal document issued by an insurance provider that amends an existing policy to include an additional person or entity as a named insured, granting them the same rights and coverage as the original policyholder.

When is a Named Insured Endorsement required for a business?

This endorsement is typically required during mergers, acquisitions, or when forming subsidiaries, ensuring that all related corporate entities are legally protected under a single liability or property insurance policy.

How does adding a named insured differ from adding an additional insured?

Adding a "Named Insured" provides full policy benefits, including coverage for direct losses and the authority to make policy changes, whereas an "Additional Insured" typically receives limited protection only for specific vicarious liability arising from the primary policyholder's actions.

What information must be included in a request for this endorsement?

The request should include the current policy number, the full legal name of the entity being added, their Tax Identification Number (TIN), their relationship to the primary insured, and the effective date for the coverage to begin.

Does adding a named insured via endorsement increase premium costs?

Yes, adding a named insured often increases the premium because it expands the insurer's exposure to risk across multiple parties, though the exact cost depends on the new entity's claims history and business operations.

Comments