A Primary and Non-Contributory Endorsement is a critical insurance provision that determines the order of coverage when multiple policies apply to a claim. It ensures that the specific policy responds first without seeking contribution from other available insurance. This protects higher-tier parties from unnecessary loss history and financial liability. Below are some ready to use template.

Image cover: Essential Guide and Templates for Primary and Non-Contributory Endorsement Notices

Letter Samples List

- Primary and Non-Contributory Endorsement Request Letter

- Notice of Primary and Non-Contributory Endorsement Approval Letter

- Certificate Holder Endorsement Confirmation Letter

- Underwriter Primary and Non-Contributory Submission Letter

- Client Explanation of Non-Contributory Endorsement Letter

- Subcontractor Primary Endorsement Requirement Letter

- Notice of Missing Non-Contributory Endorsement Letter

- Policy Renewal Primary and Non-Contributory Endorsement Letter

- Endorsement Premium Invoice and Notice Letter

- Vendor Primary and Non-Contributory Compliance Letter

- General Contractor Endorsement Verification Letter

- Notice of Non-Contributory Endorsement Rejection Letter

- Additional Insured Primary Endorsement Status Letter

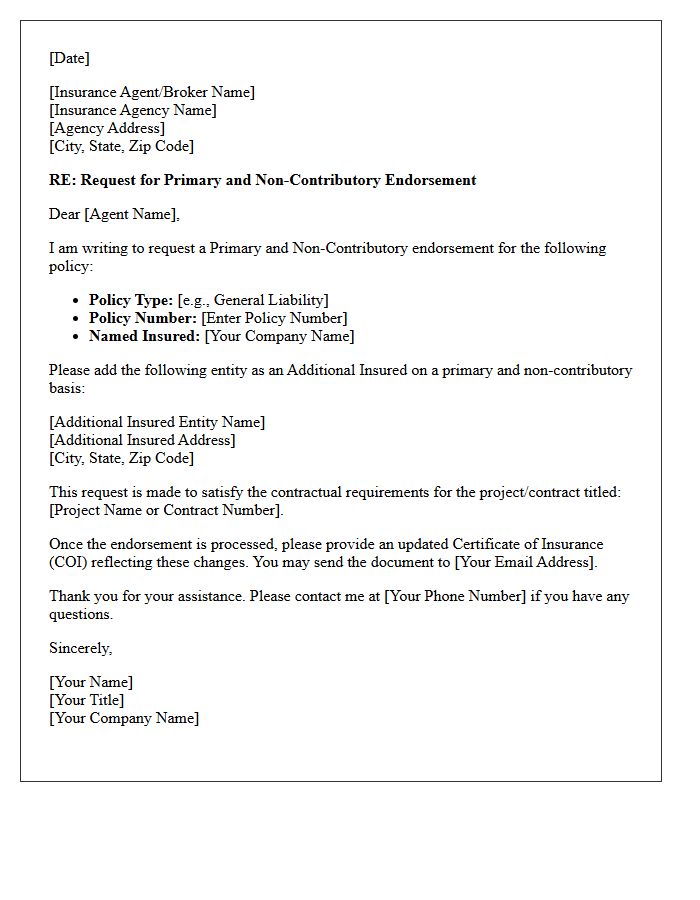

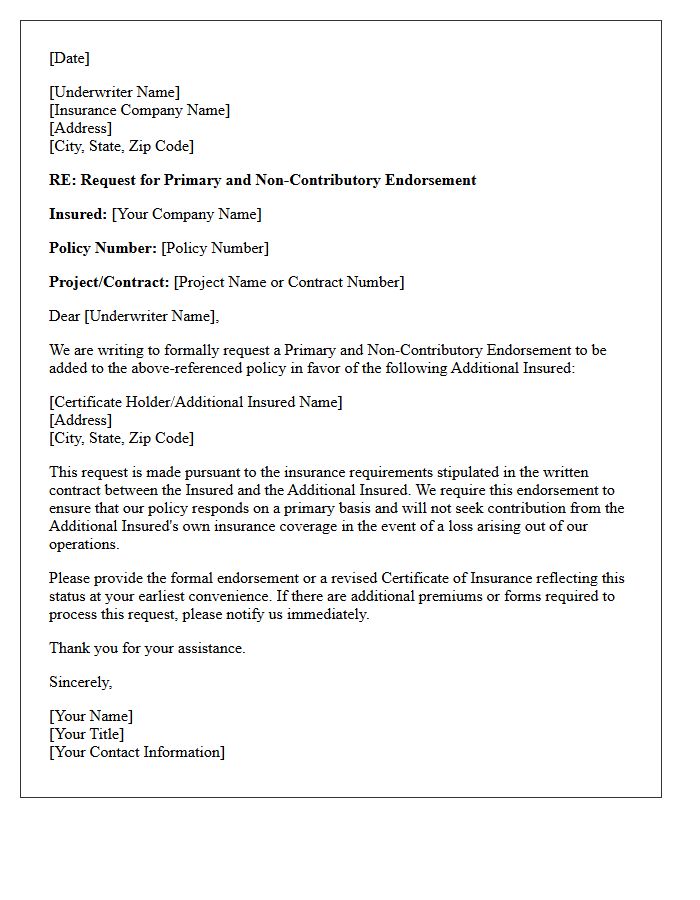

Primary and Non-Contributory Endorsement Request Letter

A primary and non-contributory endorsement request letter is a formal document sent to an insurer to prioritize a specific policy. It ensures that your insurance coverage responds first in the event of a claim, without seeking a financial contribution from the additional insured's policy. This contractual requirement is essential for managing liability risks and fulfilling indemnification obligations. By formalizing this request, you protect business partners from shared losses, ensuring your policy provides the primary layer of protection for covered incidents during the project or contract term.

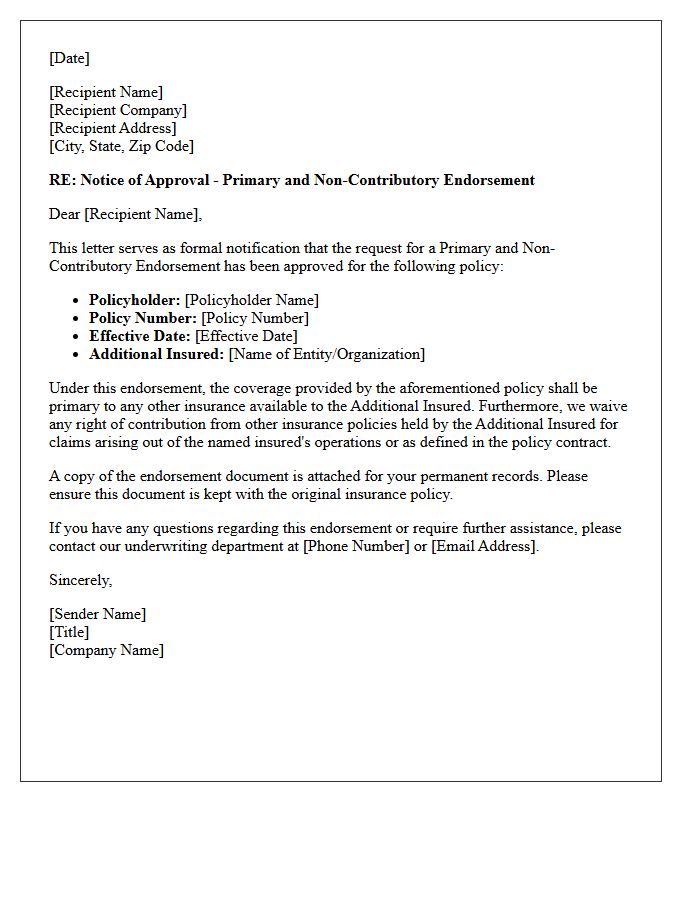

Notice of Primary and Non-Contributory Endorsement Approval Letter

A Notice of Primary and Non-Contributory Endorsement Approval Letter confirms that a policyholder's insurance acts as the primary coverage during a claim. This document ensures that the policy pays out first, before any other available insurance, without seeking contribution from the additional insured's own policy. It is a critical requirement in commercial contracts to transfer risk effectively and protect partners from financial liability. Obtaining this letter validates that the specific endorsement has been officially reviewed and approved by the carrier, providing essential proof of compliance with contractual insurance obligations.

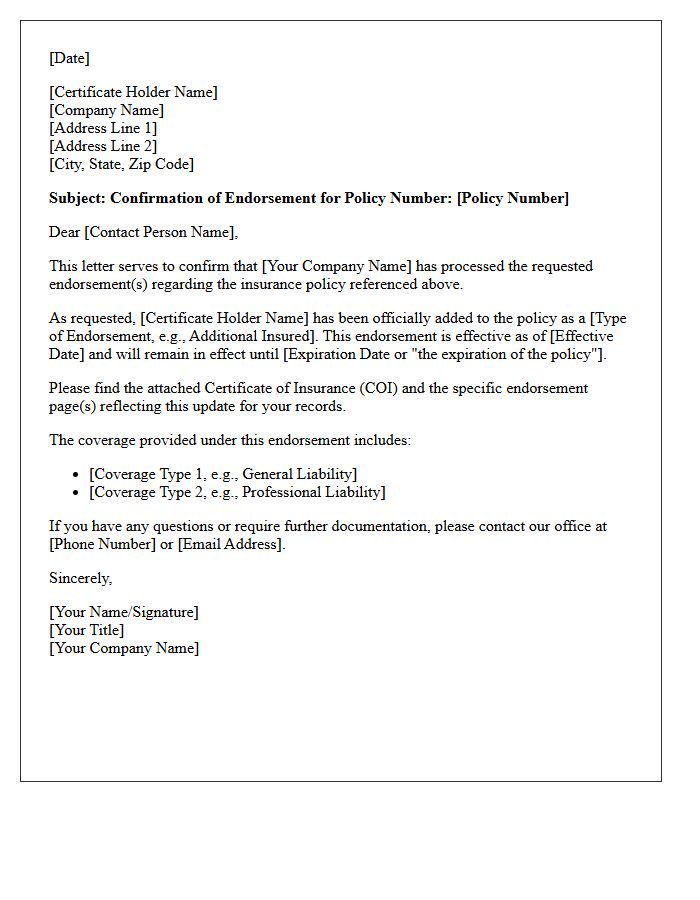

Certificate Holder Endorsement Confirmation Letter

A Certificate Holder Endorsement Confirmation Letter serves as official proof that a specific party is formally recognized under an insurance policy. The Certificate Holder receives this document to verify that the insurance company has processed the necessary endorsement to provide coverage or notification rights. This letter is crucial for contractual compliance, ensuring that liability protection is active and that the holder will be informed of policy cancellations or material changes, confirming the insurer's legal commitment to the third party.

Underwriter Primary and Non-Contributory Submission Letter

An Underwriter Primary and Non-Contributory Submission Letter is a formal request to an insurance carrier to modify policy priority. It ensures the policyholder's coverage responds first in a claim, without seeking contribution from the additional insured's own insurance. This document is essential for fulfilling contractual requirements in construction or service agreements. Clear language must be used to confirm that the coverage is primary and any other available insurance is non-contributory, effectively shifting liability and protecting the partner's financial interests during a loss.

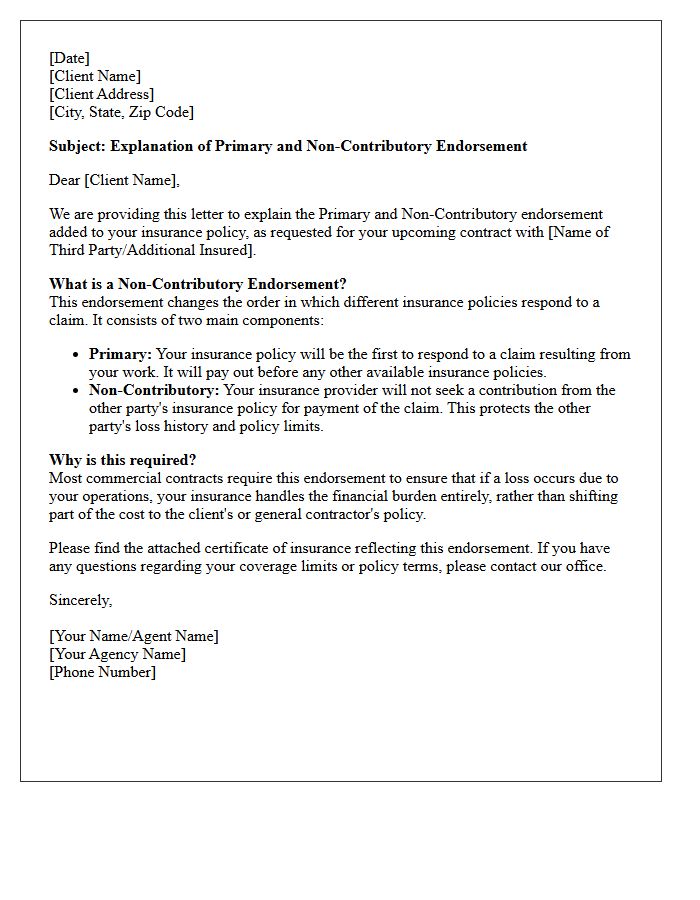

Client Explanation of Non-Contributory Endorsement Letter

A Non-Contributory Endorsement is a crucial insurance provision ensuring that your policy pays out first without seeking contribution from other coverage. This letter serves as a formal guarantee to your client that your primary insurance will cover potential claims exclusively. By including this endorsement, you protect your client's loss history and minimize their financial risk during a shared project. It establishes a clear priority of coverage, making your business more competitive and compliant with standard contractual insurance requirements in most professional industries.

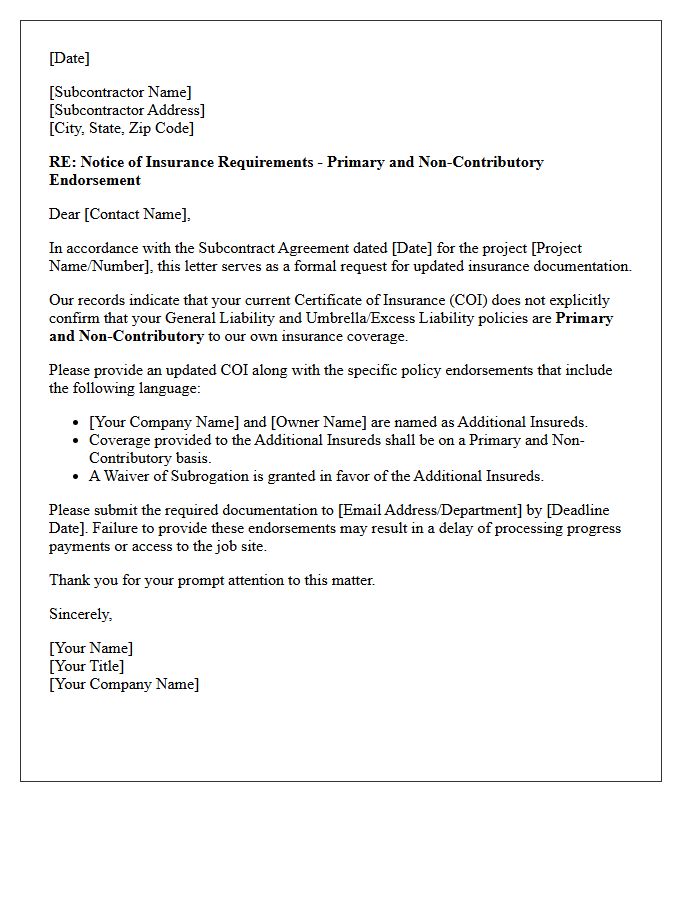

Subcontractor Primary Endorsement Requirement Letter

A Subcontractor Primary Endorsement Requirement Letter is a formal document ensuring a subcontractor's insurance remains the primary coverage in case of a claim. It mandates that the subcontractor's policy pays first, preventing the general contractor's insurance from being exhausted prematurely. This letter typically requires a Primary and Non-Contributory endorsement to be filed with the certificate of insurance. Properly documenting this requirement is essential for effective risk management and protecting the hiring party from financial liability arising from third-party operations or onsite accidents.

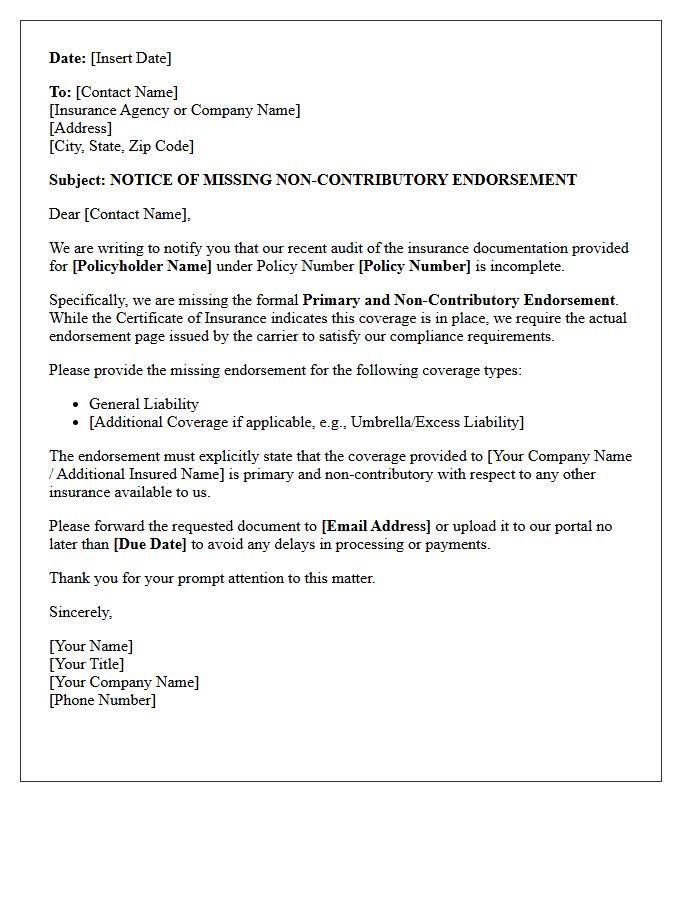

Notice of Missing Non-Contributory Endorsement Letter

A Notice of Missing Non-Contributory Endorsement Letter indicates that your insurance policy lacks a critical compliance document. This endorsement ensures that your coverage pays first without seeking contribution from other policies. It is a mandatory requirement for many commercial contracts and leases. Failing to provide this letter can result in breach of contract, delayed payments, or project site removal. You must contact your insurance broker immediately to issue the formal endorsement and satisfy the specific indemnity obligations requested by your certificate holder or client.

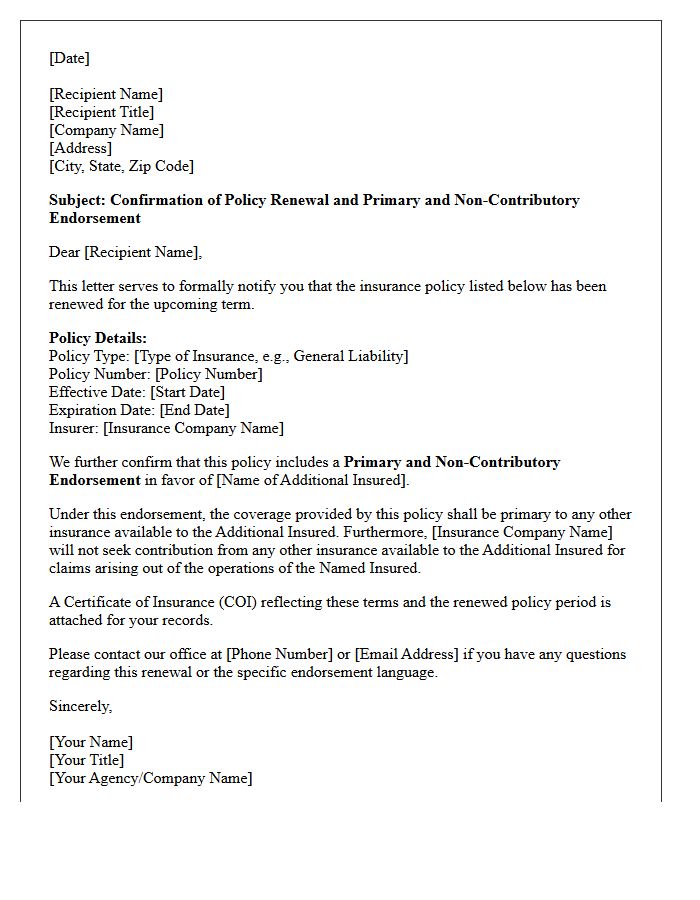

Policy Renewal Primary and Non-Contributory Endorsement Letter

A Primary and Non-Contributory Endorsement is a critical document issued during policy renewal to clarify the order of insurance coverage. This letter confirms that your policy will respond first to a claim, while the additional insured's policy remains secondary. It effectively prevents your insurer from seeking contribution from the other party's coverage for shared liabilities. Securing this endorsement is essential for maintaining contractual compliance in business agreements, ensuring that you fulfill specific indemnification requirements and protect partners from financial loss during the new policy term.

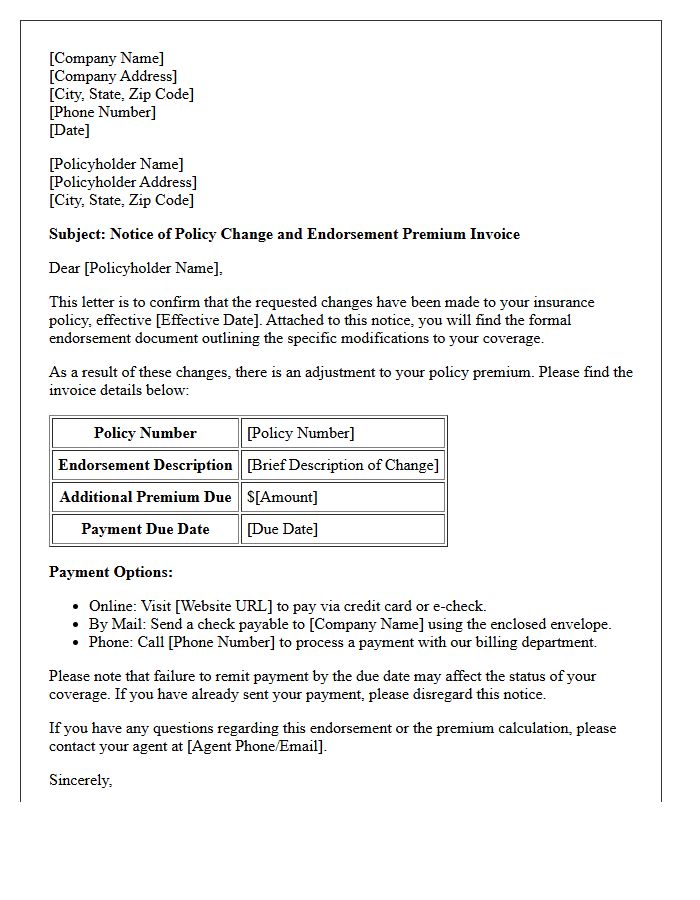

Endorsement Premium Invoice and Notice Letter

An Endorsement Premium Invoice is a formal billing statement issued when a mid-term policy change increases your insurance costs. This document details the additional amount due following adjustments like adding coverage or updating assets. Accompanying this is the Endorsement Notice Letter, which explains the specific policy modifications and your new payment obligations. Reviewing these documents promptly is essential to ensure continuous protection and avoid policy cancellation due to non-payment. Always verify that the reflected changes accurately match your requested updates to maintain valid and effective insurance coverage.

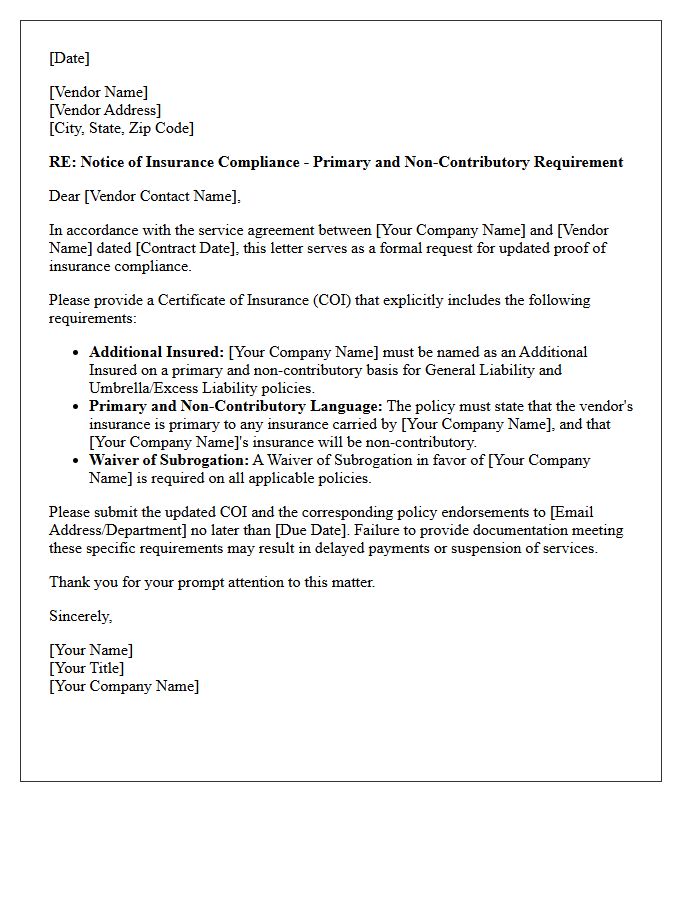

Vendor Primary and Non-Contributory Compliance Letter

A Primary and Non-Contributory compliance letter confirms that a vendor's insurance policy will pay first during a claim, without seeking contribution from the client's own coverage. This endorsement is essential for risk transfer, ensuring the hiring party remains protected from financial liability caused by the vendor's actions. It simplifies the claims process and upholds contractual indemnification requirements. Providing this documentation is a standard prerequisite for business compliance, protecting your company's loss history and maintaining professional insurance standards across all active projects.

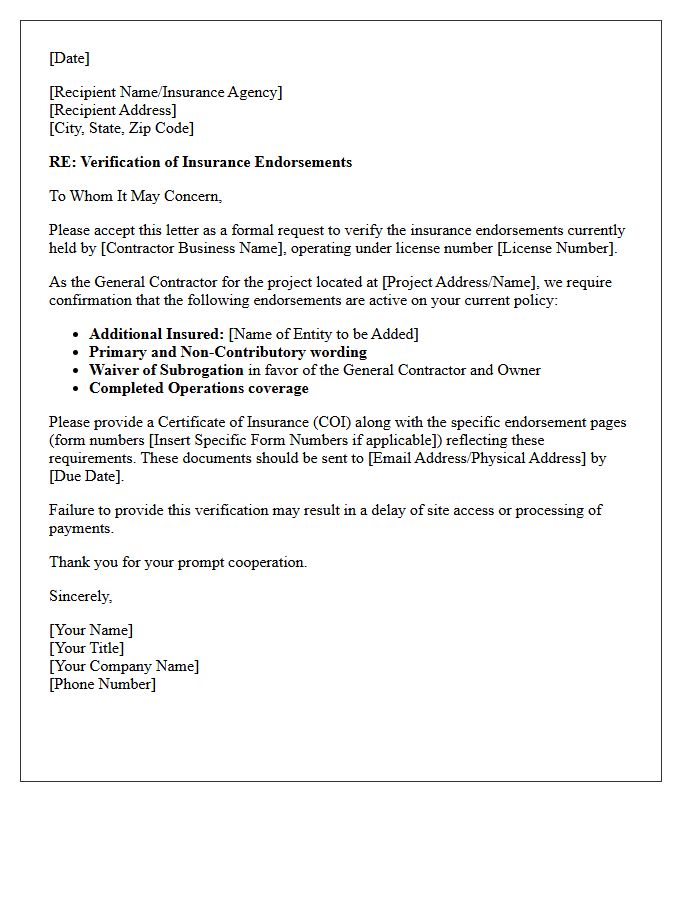

General Contractor Endorsement Verification Letter

A General Contractor Endorsement Verification Letter serves as official proof that a professional holds valid liability insurance and specific trade certifications. This document confirms that a contractor's policy includes an endorsement to perform specific work, protecting clients from financial risk. Before starting any project, homeowners should request this letter to verify coverage limits and ensure the contractor is legally authorized by their insurance provider to operate. This verification step is essential for risk mitigation, ensuring safety compliance and professional accountability throughout the construction process.

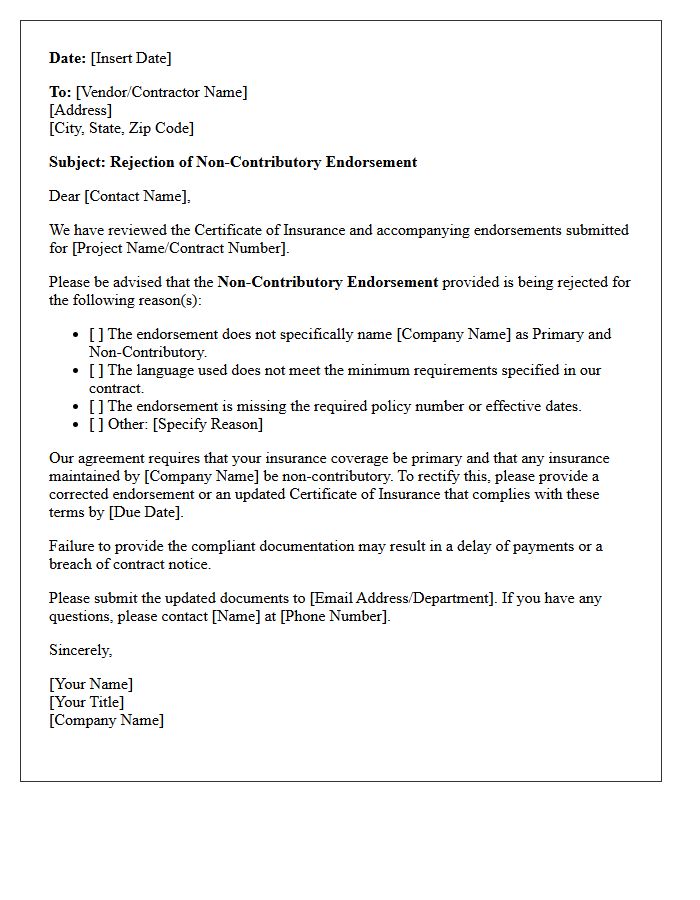

Notice of Non-Contributory Endorsement Rejection Letter

A Notice of Non-Contributory Endorsement Rejection Letter is a formal notification from an insurance carrier stating they cannot fulfill a request for primary and non-contributory status. This rejection typically occurs when the policy language or specific risk guidelines prevent the insurer from waiving their right to seek contribution from other available coverage. It is critical for contractors to review these letters immediately, as failing to secure this endorsement may result in a breach of contract with a client or general contractor, leading to potential legal and financial liabilities.

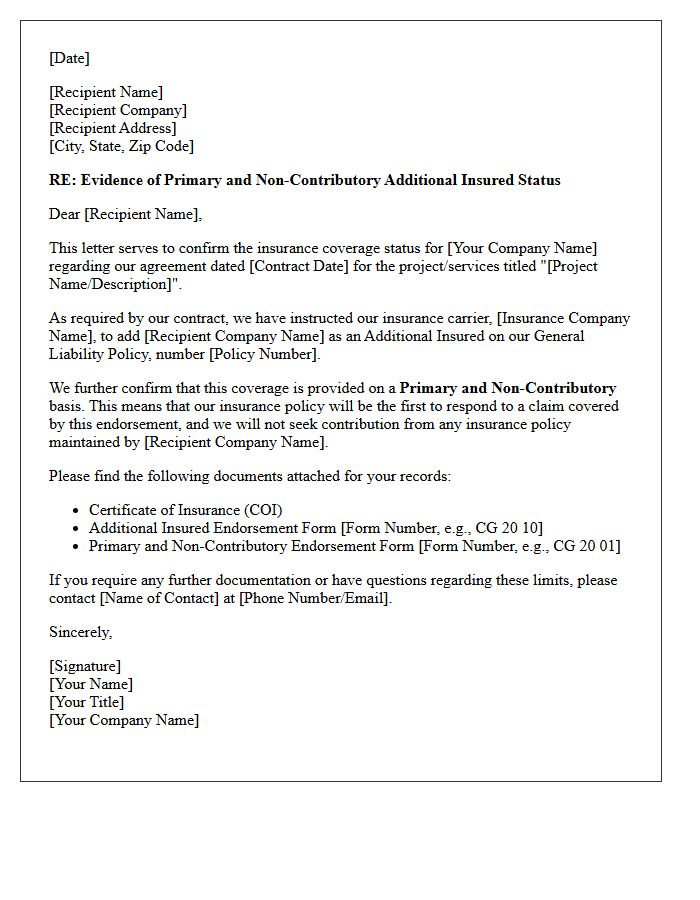

Additional Insured Primary Endorsement Status Letter

An Additional Insured Primary Endorsement Status Letter confirms that a policyholder's insurance takes precedence during a claim. It formalizes Primary and Non-Contributory status, ensuring the additional insured's own policy remains untouched until the primary coverage is exhausted. This document is vital for contractual compliance, as it prevents subrogation and shifts financial liability away from the hiring party. Without this verified status, a business may face unintended exposure to legal costs and losses that should have been covered by the contractor's primary policy.

What is a Primary and Non-Contributory Endorsement?

A Primary and Non-Contributory Endorsement is a commercial insurance provision that establishes a specific policy as the first to pay in the event of a claim (primary) and prevents that policy from seeking contribution from other available insurance policies (non-contributory).

How does a Primary and Non-Contributory clause work in a contract?

When this clause is active, the policyholder's insurance carrier agrees to cover the full cost of a claim up to the policy limit without asking the additional insured's own insurance provider to share the costs or participate in the settlement.

Why do contractors require Primary and Non-Contributory Endorsements?

Project owners and general contractors require this endorsement to protect their own loss history. By ensuring the subcontractor's policy is primary, the hiring party avoids using their own insurance coverage for claims arising from the subcontractor's operations.

What is the difference between Primary and Non-Contributory vs. Waiver of Subrogation?

While often used together, they serve different purposes: Primary and Non-Contributory determines the order of payment for a claim, whereas a Waiver of Subrogation prevents an insurance company from seeking recovery (reimbursement) from a third party after the claim has been paid.

Is a Primary and Non-Contributory Endorsement mandatory?

It is not legally mandated by the state, but it is a standard contractual requirement in the construction and real estate industries. Most Certificates of Insurance (COI) will not be accepted by a hiring client unless this specific endorsement notice is documented.

Comments