Streamline your insurance process with a Workers Compensation Officer Exclusion Endorsement Request. This formal document allows corporate executives to opt out of coverage, potentially reducing premium costs for the business. Understanding the legal requirements and filing procedures is essential for compliance. To simplify your paperwork and ensure accuracy, below are some ready to use template.

Image cover: Formal Request Templates for Workers' Compensation Officer Exclusion Endorsements

Letter Samples List

- Initial Workers Compensation Officer Exclusion Endorsement Request Letter

- Urgent Follow-Up Letter for Officer Exclusion Endorsement Processing

- Missing Signatures Notification Letter for Officer Exclusion Form

- Executive Officer Exclusion Endorsement Carrier Submission Letter

- Client Confirmation Letter for Workers Compensation Officer Exclusion

- State-Specific Corporate Officer Exclusion Request Letter

- Annual Renewal Letter for Officer Exclusion Endorsement Verification

- Limited Liability Company Member Exclusion Request Letter to Underwriter

- Revised Payroll Adjustment Letter Due to Officer Exclusion

- Insurance Agency Cover Letter for Officer Exclusion Endorsement

- Acknowledgment Letter of Approved Officer Exclusion Endorsement

- Carrier Rejection Inquiry Letter Regarding Officer Exclusion Endorsement

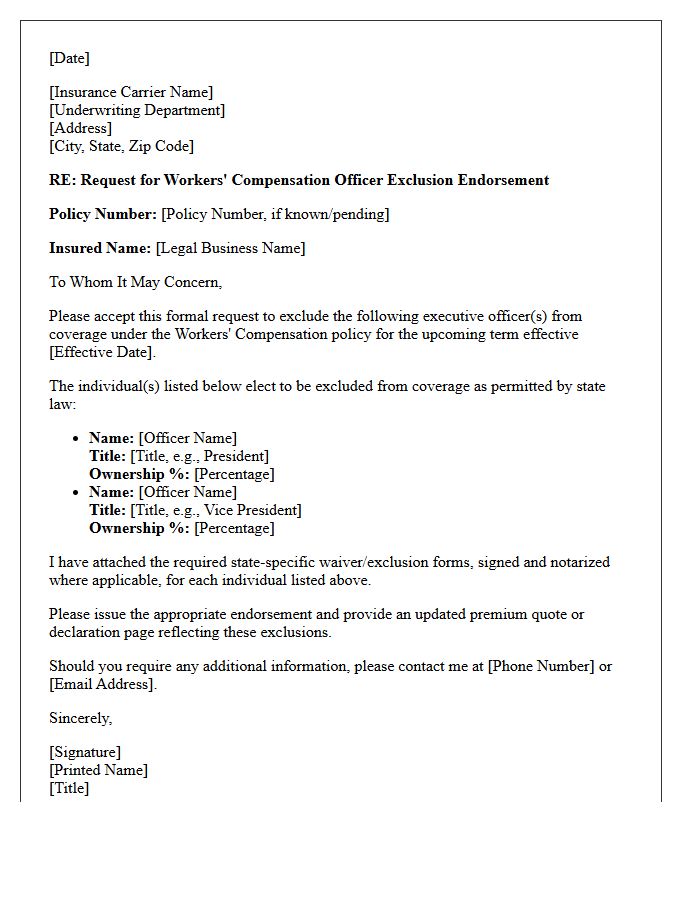

Initial Workers Compensation Officer Exclusion Endorsement Request Letter

An Officer Exclusion Endorsement Request Letter is a formal document used to opt-out specific corporate leaders from Workers Compensation coverage. This request must clearly identify the officers by name and title to ensure they are legally excluded from the policy payroll and benefits. Submitting this letter is essential for reducing insurance premiums when executives maintain alternative health or disability coverage. To be valid, the letter must comply with state-specific regulations and be signed by the authorized individuals seeking the exclusion prior to the policy effective date.

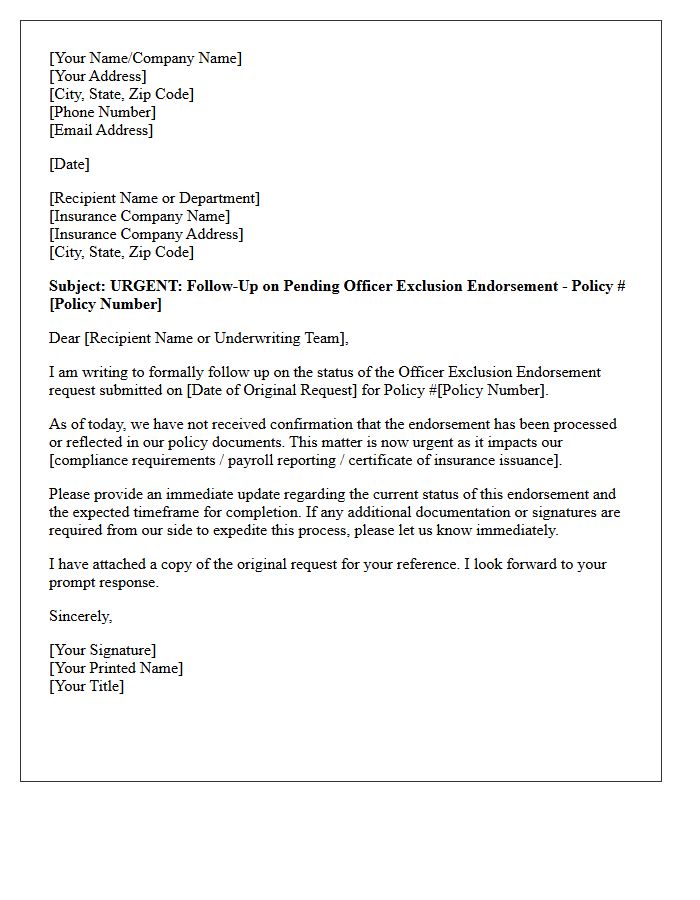

Urgent Follow-Up Letter for Officer Exclusion Endorsement Processing

An urgent follow-up letter is essential to expedite Officer Exclusion Endorsement processing with your insurance carrier. This formal request ensures that specific executive officers are legally excluded from workers' compensation coverage, directly impacting your premium calculations and policy accuracy. Delays in processing can lead to overbilling or compliance gaps. Clearly state the policy number, effective date, and the names of excluded individuals to ensure the endorsement is applied immediately. Timely communication serves as critical documentation to confirm your business is not paying unnecessary costs for exempt personnel.

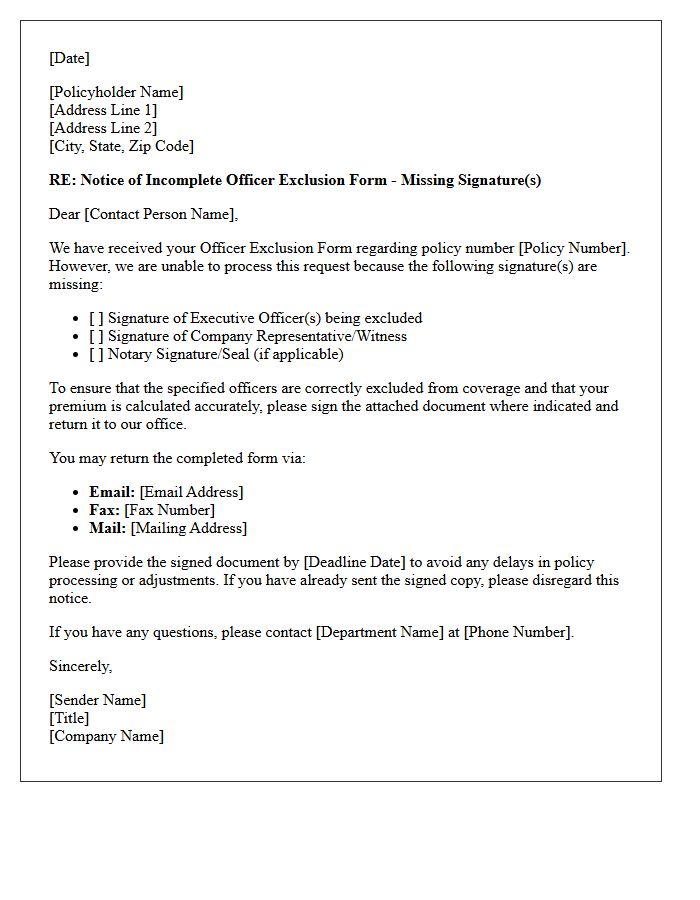

Missing Signatures Notification Letter for Officer Exclusion Form

A Missing Signatures Notification Letter indicates that your Officer Exclusion Form is incomplete. To legally exclude executive officers from workers' compensation coverage, all required parties must sign the document. Failure to provide these signatures promptly can lead to processing delays or the automatic inclusion of officers in the policy, resulting in higher premiums. Always review the letter to identify which signatures are missing and return the corrected form to your insurance provider to ensure compliance and accurate billing for your business entity.

Executive Officer Exclusion Endorsement Carrier Submission Letter

An Executive Officer Exclusion Endorsement carrier submission letter is a formal request to remove specific corporate officers from workers' compensation coverage. This document must clearly identify the individuals by name and title to ensure payroll audits reflect accurate premium calculations. Properly executed letters prevent overpayment and formalize legal liability exemptions. It is essential to include the effective date and follow state-specific regulatory guidelines to ensure the endorsement is legally binding and recognized by the insurance carrier during the policy term.

Client Confirmation Letter for Workers Compensation Officer Exclusion

A Client Confirmation Letter for Workers' Compensation Officer Exclusion is a formal document used to verify that specific corporate officers or owners have elected to waive their coverage under a policy. This letter serves as legal evidence for insurance carriers, ensuring that payroll for excluded individuals is not included in premium calculations. It is crucial to understand that by signing, officers forfeit their right to medical benefits and lost wages if injured on the job. Accurate documentation is essential for audit compliance and preventing unexpected premium adjustments during the policy term.

State-Specific Corporate Officer Exclusion Request Letter

A State-Specific Corporate Officer Exclusion Request Letter is a formal document used to opt out of workers' compensation coverage. Business owners and executives use this to reduce premium costs by declaring they will not claim benefits. Requirements vary by jurisdiction, often requiring specific statutory language and notarization. Filing this letter correctly ensures legal compliance while protecting the company from unnecessary insurance expenses. It is crucial to verify your state's department of labor regulations to ensure the waiver is valid and legally binding for your specific corporate structure.

Annual Renewal Letter for Officer Exclusion Endorsement Verification

The Annual Renewal Letter is a critical document used to confirm the Officer Exclusion Endorsement on your workers' compensation policy. This verification ensures that specific executive officers or owners remain legally excluded from coverage to reduce premium costs. It is essential to review the listed individuals for accuracy, sign the form, and return it by the specified deadline. Failure to respond may result in the insurance carrier automatically including those officers in your payroll audit, leading to unexpected and increased premium charges for your business.

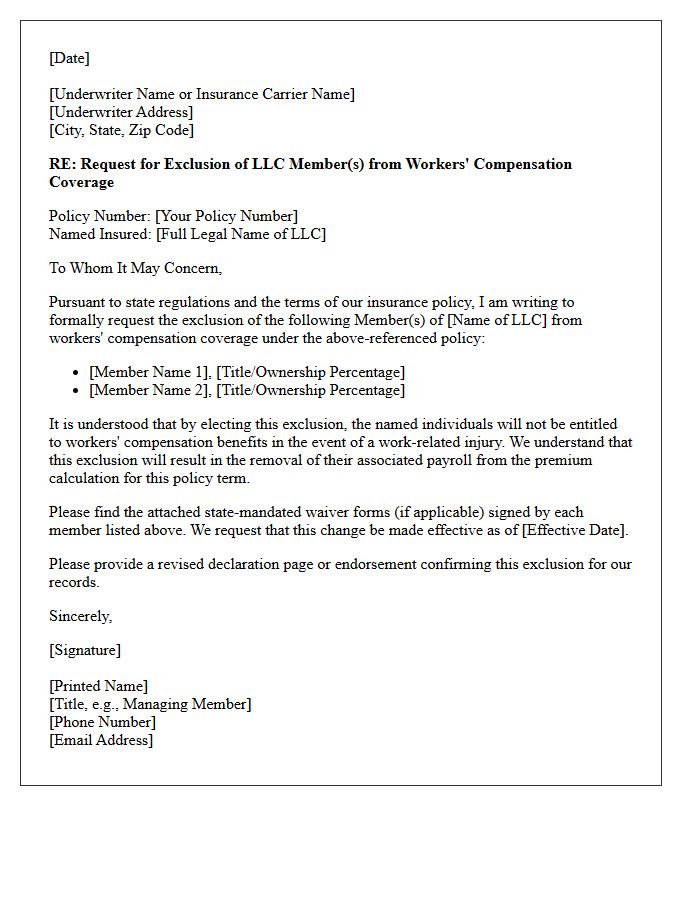

Limited Liability Company Member Exclusion Request Letter to Underwriter

A Limited Liability Company Member Exclusion Request Letter is a formal document sent to an insurance underwriter to remove specific owners from workers' compensation coverage. This request is essential for LLC members who wish to reduce premium costs by opting out of personal protection. The letter must clearly state the member's name, ownership percentage, and formal intent to waive benefits. Underwriters require this written notice to adjust policy payroll audits and ensure legal compliance with state regulations regarding executive officer exemptions and liability limits.

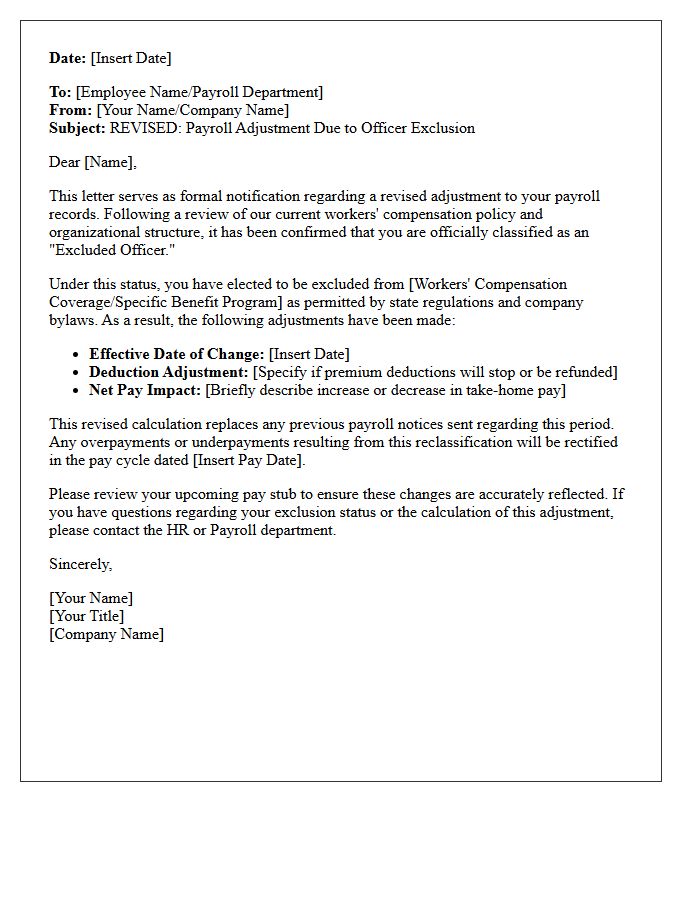

Revised Payroll Adjustment Letter Due to Officer Exclusion

A revised payroll adjustment letter is critical when an officer exclusion occurs, officially removing executives from workers' compensation coverage. This document ensures premium accuracy by notifying the insurer to adjust payroll audits and billing cycles. Organizations must provide clear documentation to verify the officer's status and effective date of removal. Promptly issuing this letter prevents overpayment and maintains compliance with state regulations, ensuring that labor costs reflect only covered personnel. Timely communication with your provider guarantees that financial records align with the updated policy scope.

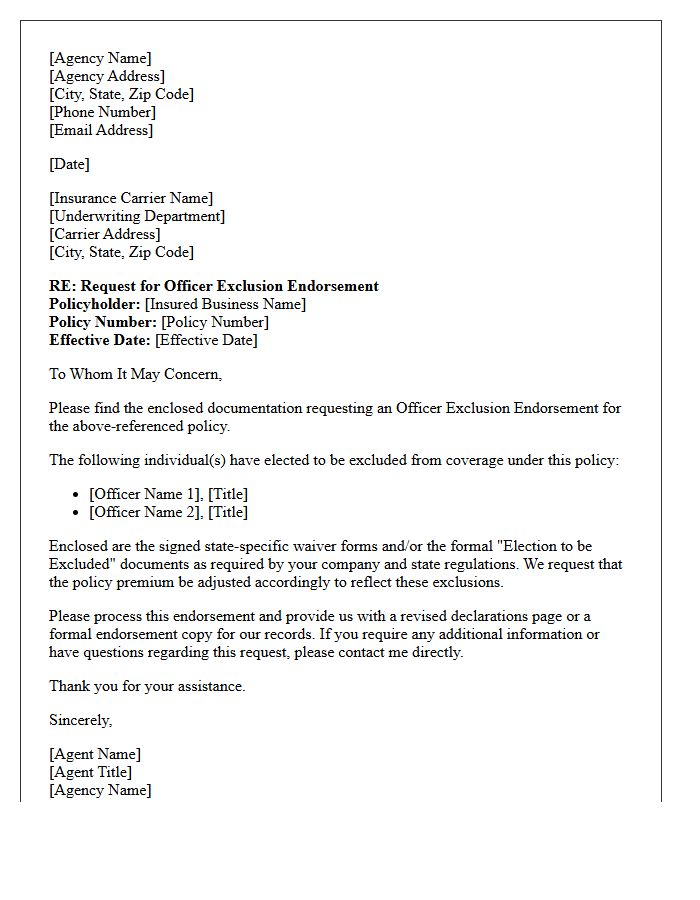

Insurance Agency Cover Letter for Officer Exclusion Endorsement

When drafting an insurance agency cover letter for an Officer Exclusion Endorsement, clearly specify the names and titles of the executives opting out of workers' compensation. This document acts as a formal instruction for the carrier to modify the policy. It is crucial to highlight that excluded officers will not receive benefits in the event of a workplace injury. Ensure the letter matches the legal entity name and includes the effective date to prevent audit discrepancies. Professional clarity ensures the exclusion is applied correctly, potentially reducing overall premium costs for the business.

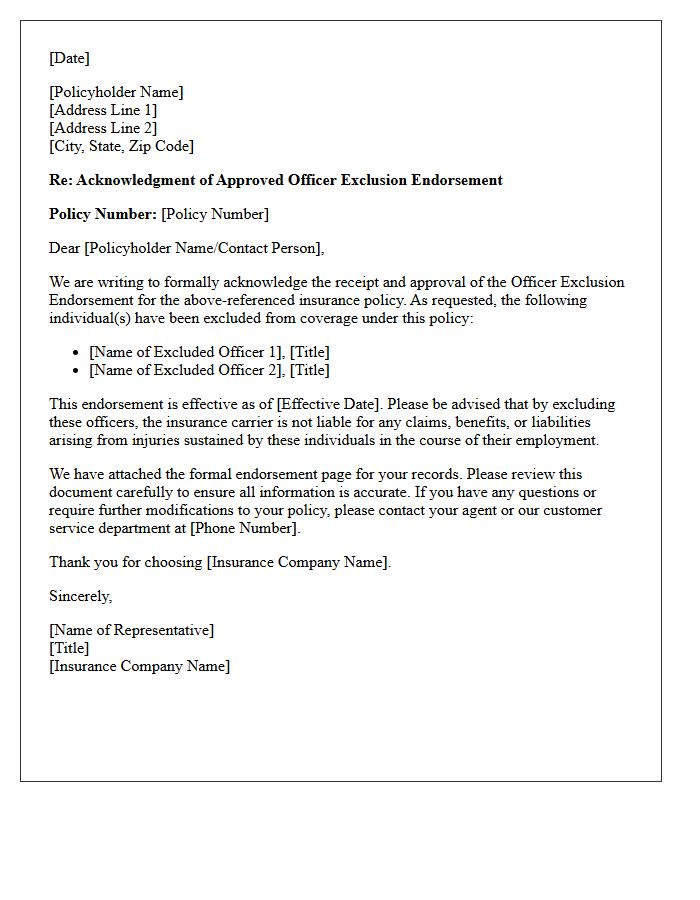

Acknowledgment Letter of Approved Officer Exclusion Endorsement

An Acknowledgment Letter of Approved Officer Exclusion Endorsement is a critical legal document confirming that specific corporate officers are officially excluded from workers' compensation coverage. By signing this letter, the company acknowledges that these individuals will not receive benefits in the event of a work-related injury. This endorsement is essential for policy accuracy and can significantly reduce premium costs. It serves as formal proof for insurers and regulatory bodies that the waived coverage meets state-specific requirements and has been legally finalized within the insurance contract.

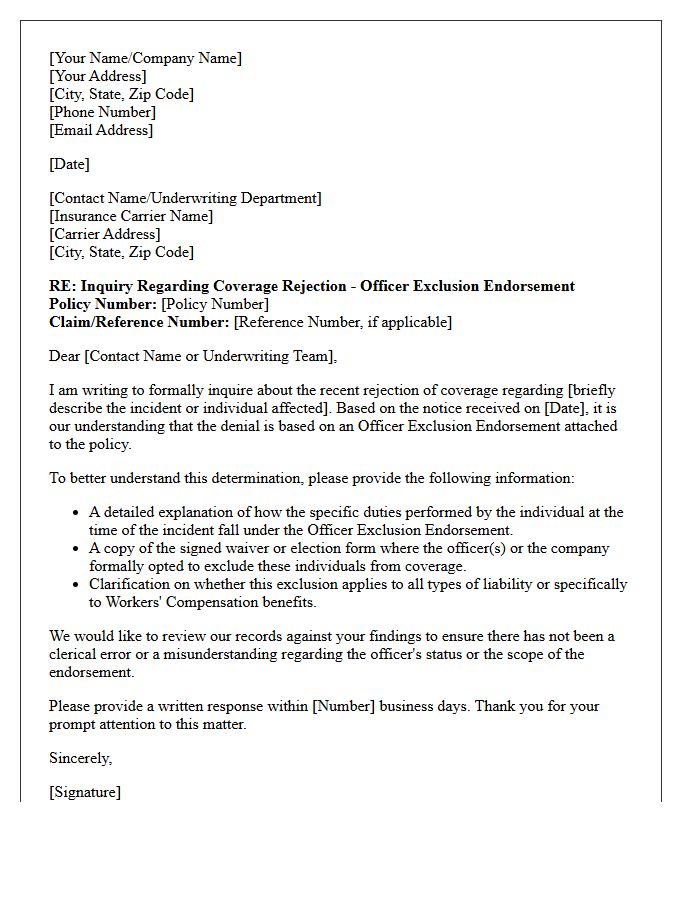

Carrier Rejection Inquiry Letter Regarding Officer Exclusion Endorsement

A Carrier Rejection Inquiry Letter addresses why an Officer Exclusion Endorsement was applied to a policy. This document is essential for workers' compensation transparency, as it formally requests the insurer to justify the removal of executive coverage. Understanding this rejection is vital for risk management, ensuring that corporate officers are aware of their lack of protection during workplace injuries. Business owners use this inquiry to challenge incorrect classifications or to seek alternative coverage options, maintaining compliance with state labor laws while protecting key leadership assets.

What is a Workers' Compensation Officer Exclusion Endorsement?

An Officer Exclusion Endorsement is a formal amendment to a workers' compensation policy that removes specific corporate officers, partners, or members from coverage, meaning the insurer is not liable for their work-related injuries.

Who is eligible to request an Officer Exclusion Endorsement?

Eligibility typically extends to executive officers, sole proprietors, partners, or LLC members who own a specific percentage of the company (often 10% or more) as defined by individual state labor laws and insurance regulations.

How do I submit a Workers' Comp Officer Exclusion Endorsement Request?

To request an exclusion, you must submit a signed state-approved waiver form or a formal written request to your insurance carrier, clearly identifying the individuals to be excluded and their ownership titles.

Does excluding an officer reduce workers' compensation premiums?

Yes, excluding an officer removes their payroll from the premium calculation, which generally reduces the overall cost of the workers' compensation policy; however, those individuals will have no medical or indemnity protection under the policy.

Can an Officer Exclusion Endorsement be reversed during a policy term?

Yes, most carriers allow you to rescind an exclusion endorsement by submitting a written request to add the officer back to the coverage, which will result in a pro-rated premium increase based on their estimated annual payroll.

Comments