Receiving a Business Owner Policy Impending Lapse Notice means your essential commercial coverage is at risk due to missed premiums. To prevent a gap in protection and potential legal liabilities, immediate action is required to reinstate your insurance. Understanding how to communicate with insurers or clients is vital during this grace period. Below are some ready to use template options.

Image cover: Professional Business Owner's Policy Lapse Notices: Editable Templates and Samples

Letter Samples List

- Business Owner Policy Impending Lapse First Warning Letter

- Business Owner Policy Impending Lapse Final Notice Letter

- Business Owner Policy Impending Lapse Grace Period Letter

- Business Owner Policy Impending Lapse Past Due Premium Letter

- Business Owner Policy Impending Lapse Action Required Letter

- Business Owner Policy Impending Lapse Missing Document Letter

- Business Owner Policy Impending Lapse Declined Payment Letter

- Business Owner Policy Impending Lapse Agent Follow-Up Letter

- Business Owner Policy Impending Lapse Coverage Termination Letter

- Business Owner Policy Impending Lapse Reinstatement Option Letter

- Business Owner Policy Impending Lapse Audit Non-Compliance Letter

- Business Owner Policy Impending Lapse Last Chance Letter

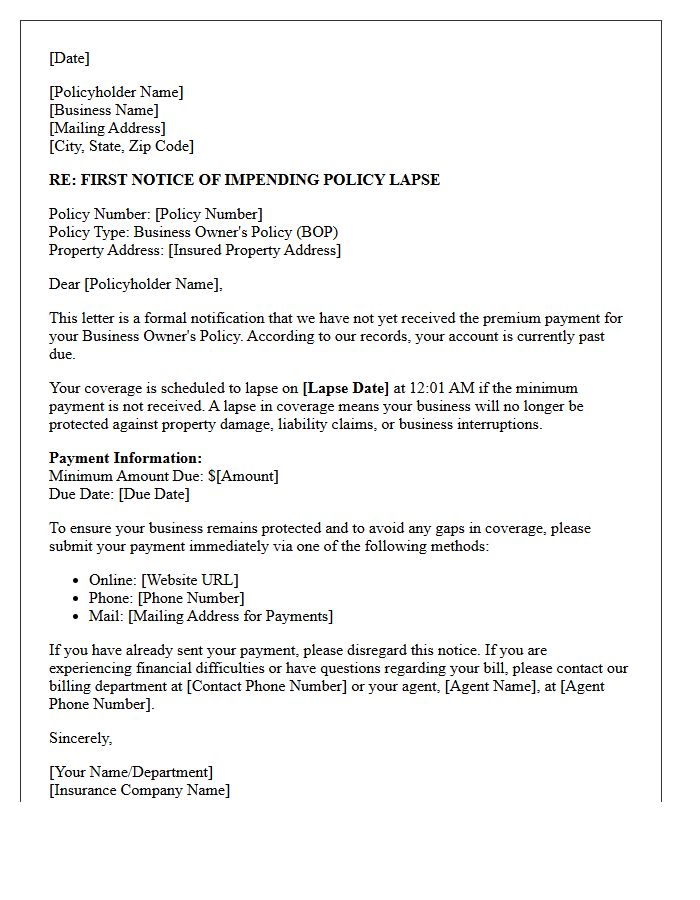

Business Owner Policy Impending Lapse First Warning Letter

A Business Owner Policy (BOP) impending lapse warning is a critical notice indicating that your commercial insurance coverage is at risk due to non-payment. This letter serves as your final opportunity to settle outstanding premiums before protection is terminated. A lapse can result in legal non-compliance, financial vulnerability to claims, and higher future rates. To maintain continuous coverage, you must remit payment immediately within the specified grace period. Ignoring this notice may lead to a permanent cancellation, leaving your business assets and operations completely uninsured against unforeseen liabilities.

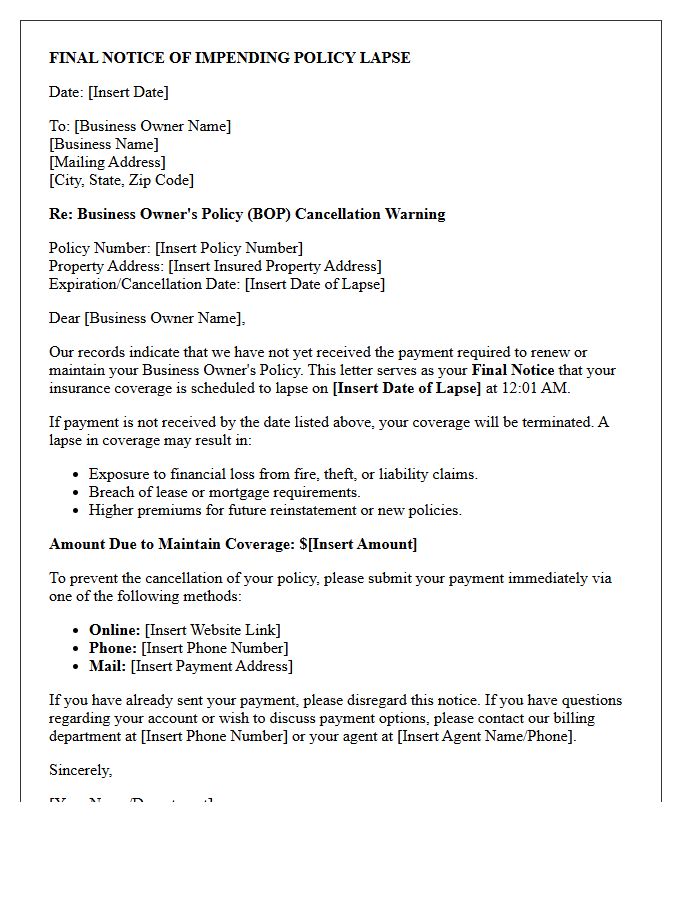

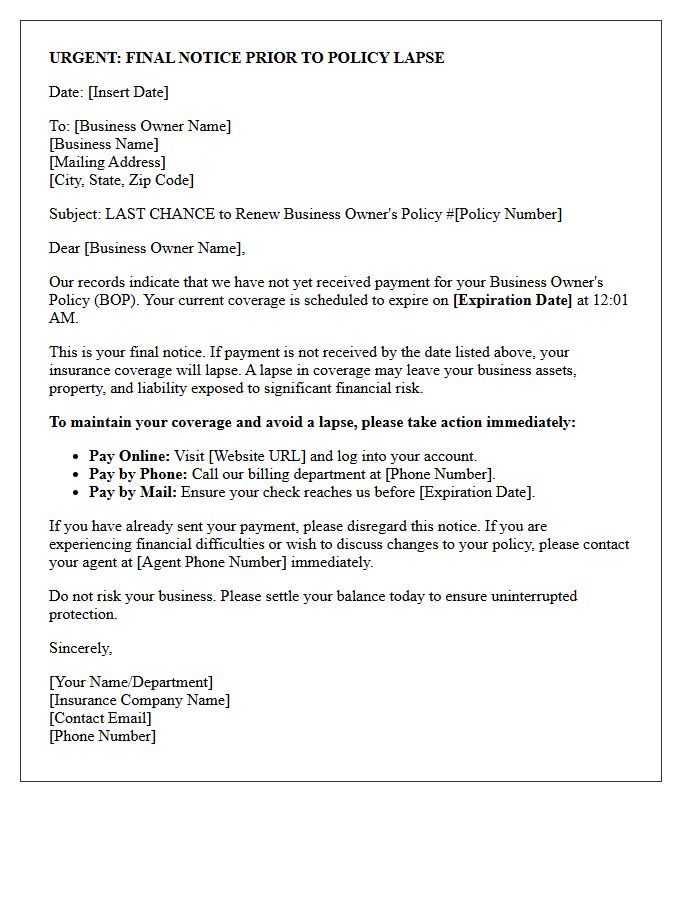

Business Owner Policy Impending Lapse Final Notice Letter

A Business Owner Policy Impending Lapse Final Notice Letter is a critical warning that your commercial insurance is about to terminate due to non-payment. This document signifies the end of your grace period and requires immediate action to maintain protection. If the premium remains unpaid by the specified deadline, your coverage will officially expire, leaving your assets vulnerable to lawsuits and property damage. To prevent a costly coverage gap, you must contact your insurer immediately to settle the balance and ensure your business remains legally compliant and fully insured.

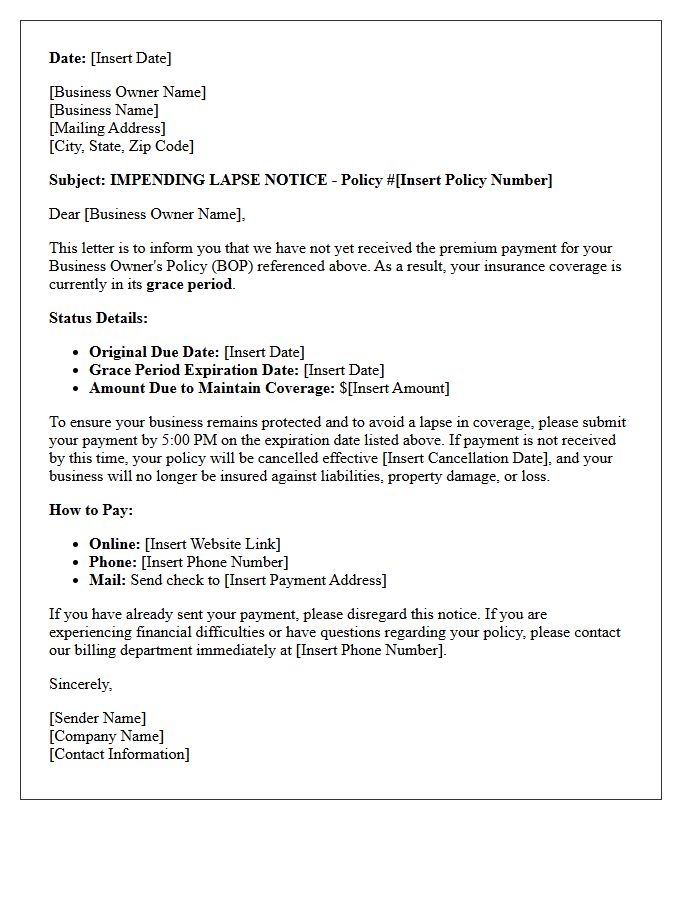

Business Owner Policy Impending Lapse Grace Period Letter

A Business Owner Policy (BOP) lapse notice is a critical legal warning sent when a premium payment is overdue. This letter defines a grace period, offering a final window to submit funds before coverage terminates. To avoid a lapse in coverage, which creates significant financial liability and legal risk, policyholders must pay the balance immediately. Reinstating a policy after it expires is often more expensive and difficult. Always review the expiration date listed in the notice to ensure your business remains continuously protected against unforeseen claims.

Business Owner Policy Impending Lapse Past Due Premium Letter

Receiving a Business Owner Policy Impending Lapse notice is a critical warning that your coverage is at risk due to a past due premium. This letter indicates that failure to pay the outstanding balance by the specified deadline will result in a total loss of protection for your property and liability. To avoid a lapse, which can lead to higher future rates and legal vulnerability, you must remit payment immediately. Reinstatement is not guaranteed once the cancellation date passes, making prompt communication with your insurance provider essential to maintain continuous business security.

Business Owner Policy Impending Lapse Action Required Letter

A Business Owner Policy Impending Lapse Action Required Letter is a critical notice from your insurer indicating that your coverage is at risk of cancellation. This typically occurs due to non-payment of premiums or failure to provide required underwriting documentation. To prevent a gap in protection, you must take immediate action by paying the outstanding balance or submitting the requested information before the specified expiration date. Maintaining active coverage is essential to safeguard your assets and ensure continuous business liability protection against unforeseen risks and legal claims.

Business Owner Policy Impending Lapse Missing Document Letter

A Business Owner Policy (BOP) notice regarding an impending lapse due to a missing document is a critical warning that your commercial insurance is at risk of cancellation. To maintain continuous coverage, you must immediately submit the specific forms or underwriting information requested. Failure to comply results in a protection gap, leaving your assets vulnerable to lawsuits and property damage. Always verify the deadline and contact your agent to confirm receipt, ensuring your business remains legally compliant and financially protected against unforeseen liabilities.

Business Owner Policy Impending Lapse Declined Payment Letter

A Business Owner Policy (BOP) notice regarding an impending lapse due to a declined payment is a critical legal warning. This letter signifies that your insurance coverage will terminate on a specific date unless the outstanding balance is settled immediately. A lapse in coverage exposes your company to significant financial liability and legal risks. To maintain protection, you must verify your payment information and contact your carrier to ensure continuous coverage reinstatement before the expiration deadline mentioned in the document.

Business Owner Policy Impending Lapse Agent Follow-Up Letter

A Business Owner Policy (BOP) lapse notice requires immediate action to maintain continuous liability and property coverage. This agent follow-up letter serves as a critical warning that missed premiums will result in a termination of benefits. Business owners must prioritize payment to avoid out-of-pocket losses and potential legal non-compliance. Contacting your insurance professional during this grace period is essential to explore reinstatement options and prevent a permanent break in protection. Act now to ensure your company remains resilient against unforeseen operational risks and financial vulnerabilities.

Business Owner Policy Impending Lapse Coverage Termination Letter

A Business Owner Policy (BOP) termination letter serves as a final legal notice that your commercial insurance is impending lapse due to non-payment or underwriting changes. This document specifies the exact date coverage ends, leaving your assets vulnerable to risks. To maintain protection, you must immediately address the outstanding premium or rectify compliance issues before the deadline. Ignoring this notice results in a coverage gap, which can lead to higher future rates and legal liability. Acting quickly ensures continuous business continuity and financial security.

Business Owner Policy Impending Lapse Reinstatement Option Letter

A Business Owner Policy (BOP) reinstatement option letter is a critical notice issued when coverage is at risk due to non-payment. This document outlines the impending lapse of your commercial insurance and provides a specific window to restore protection. To maintain continuous coverage, the policyholder must fulfill the reinstatement requirements, typically involving immediate payment of the outstanding premium. Ignoring this letter results in a gap in liability and property protection, potentially leading to higher future rates or a total loss of coverage for your business assets.

Business Owner Policy Impending Lapse Audit Non-Compliance Letter

Receiving a notice regarding a Business Owner Policy Impending Lapse due to audit non-compliance is a critical warning. This letter indicates your insurance coverage will terminate because mandatory payroll or revenue documentation was not submitted. To prevent a lapse in protection, you must immediately provide the requested financial records to the carrier. Failure to comply leads to policy cancellation, potential surcharges, and difficulty securing future coverage. Prioritize completing the premium audit to maintain your liability and property insurance standing and avoid costly business disruptions.

Business Owner Policy Impending Lapse Last Chance Letter

A Business Owner Policy (BOP) lapse letter is a critical legal notice indicating your commercial insurance is about to expire due to non-payment. This last chance notification serves as a final warning to settle outstanding premiums before coverage terminates. Allowing a lapse exposes your company to significant financial liability and property risks. To maintain continuous protection and avoid higher future rates, you must contact your insurer immediately to make a payment. Restoring your policy now ensures your business continuity remains secure and compliant with professional requirements.

What is a Business Owner Policy (BOP) Impending Lapse Notice?

An impending lapse notice is a formal communication from your insurance carrier warning that your Business Owner Policy is at risk of cancellation, typically due to non-payment of premiums or failure to meet underwriting requirements.

How long do I have to prevent my business insurance from lapsing?

The grace period varies by state law and provider, but most notices provide a 10 to 30-day window from the mailing date to settle outstanding balances before coverage officially terminates.

What are the consequences of letting my Business Owner Policy lapse?

A lapse in coverage leaves your business vulnerable to lawsuits and property damage claims, creates a "high-risk" insurance history that increases future premiums, and may violate your commercial lease or loan agreements.

Can I renew my BOP insurance after it has already lapsed?

Once a policy has lapsed, you may need to apply for reinstatement, which often requires a "no loss" statement confirming no claims occurred during the gap. However, some insurers may require you to purchase an entirely new policy at current market rates.

How can I resolve an impending lapse notice immediately?

The fastest way to resolve a lapse notice is to pay the past-due premium online or via phone through your agent. Ensure you receive a payment confirmation and a formal rescission of the cancellation notice to guarantee your coverage remains active.

Comments