An Impending Lapse Notice is a formal notification sent to policyholders when an insurance policy is at risk of cancellation due to non-payment of premiums. It serves as a final warning to settle outstanding balances before coverage terminates. To help you maintain compliance and clear communication, below are some ready to use templates.

Image cover: Final Notice: Essential Payment Remainder Templates and Samples to Prevent Policy Lapse

Letter Samples List

- Initial Impending Lapse Warning Letter

- Grace Period Expiration Notice Letter

- Urgent Premium Non-Payment Reminder Letter

- Final Policy Cancellation Warning Letter

- Life Insurance Policy Lapse Pending Letter

- Auto Insurance Premium Default Notice Letter

- Impending Lapse and Reinstatement Option Letter

- Final Premium Payment Demand Letter

- Account Suspension and Impending Lapse Letter

- Courtesy Premium Past Due Reminder Letter

- Agency Follow-Up on Impending Lapse Letter

- Overdue Premium Impending Lapse Letter

- Impending Loss of Coverage Notice Letter

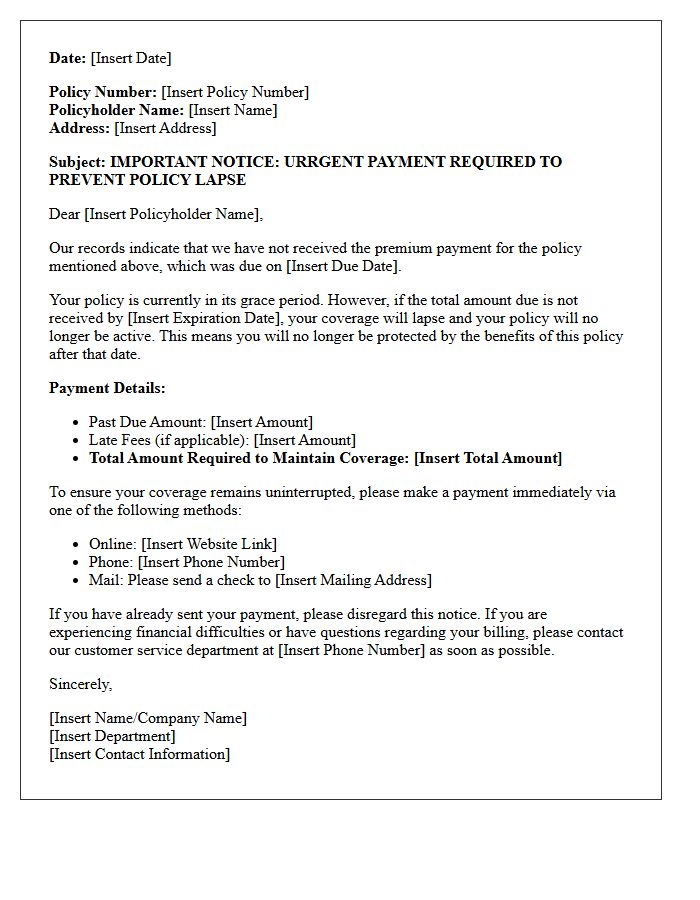

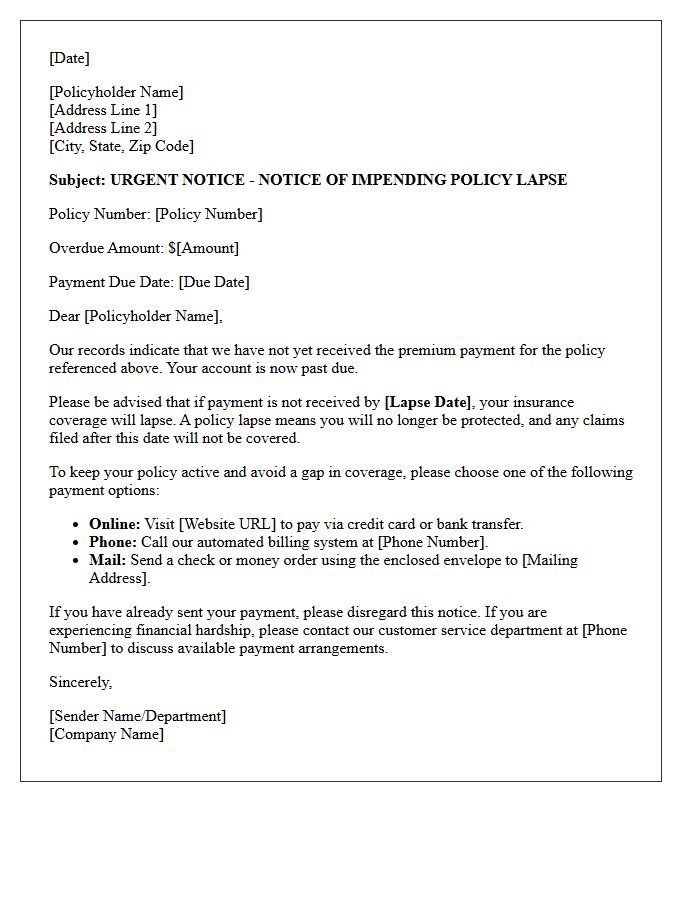

Initial Impending Lapse Warning Letter

An Initial Impending Lapse Warning Letter is a critical formal notice from an insurance provider signaling that a policy is at risk of cancellation due to unpaid premiums. This document serves as a final opportunity to maintain coverage before the grace period expires. It outlines the specific outstanding balance, the final payment deadline, and the consequences of a total lapse in protection. Acting immediately upon receipt is essential to avoid a permanent loss of benefits or the need for a costly policy reinstatement process.

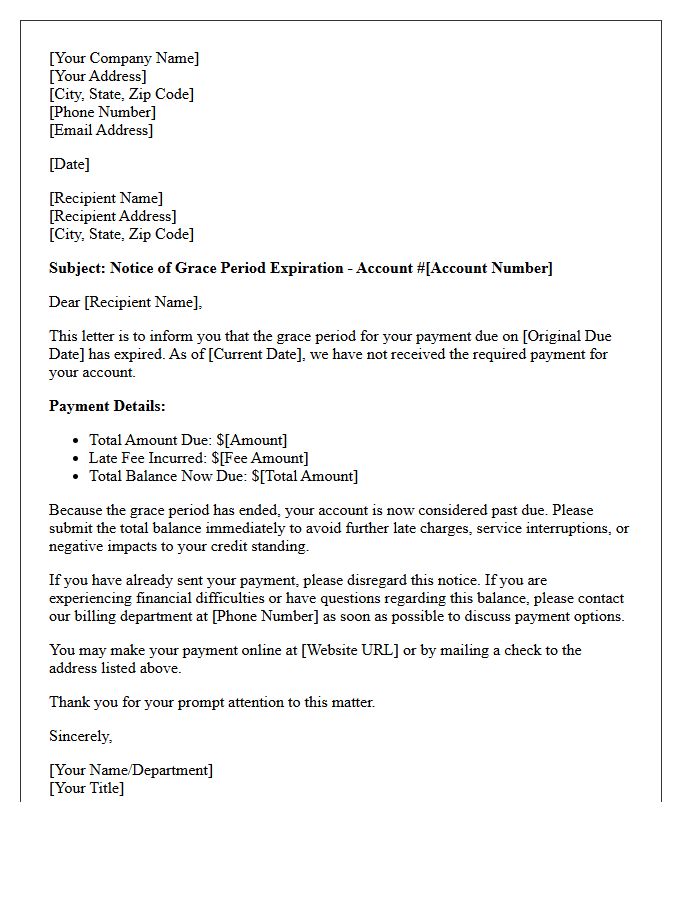

Grace Period Expiration Notice Letter

A Grace Period Expiration Notice Letter is a critical formal notification sent to policyholders or borrowers. It serves as a final warning that the extension period for an overdue payment is ending. Failing to act before the deadline typically results in coverage cancellation or a loan default. This document clearly states the exact termination date and the outstanding balance required to maintain active status. Reviewing this letter immediately is essential to avoid financial penalties or a lapse in protection, ensuring your accounts remain in good standing.

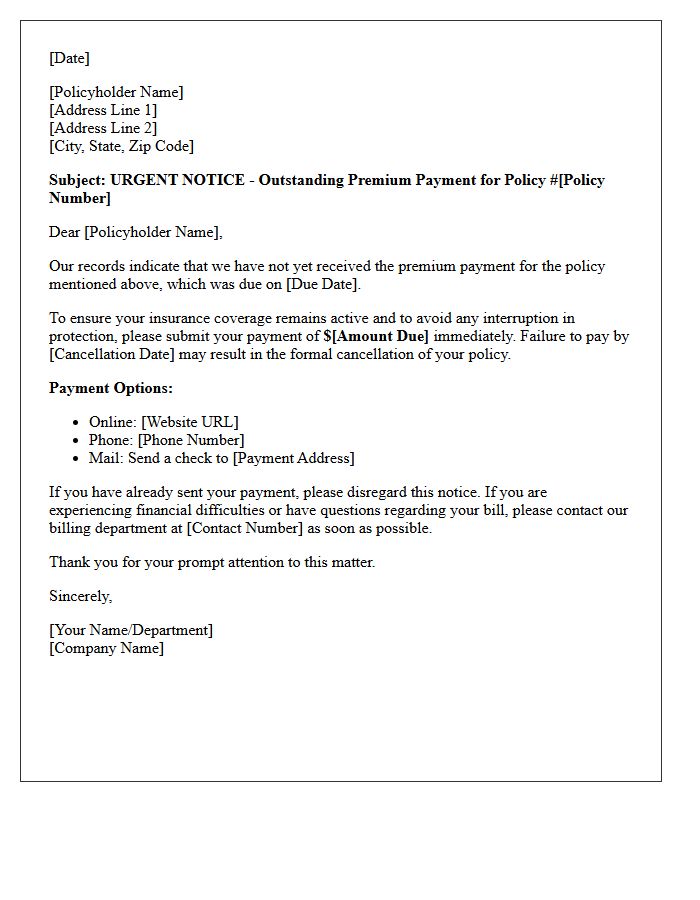

Urgent Premium Non-Payment Reminder Letter

An Urgent Premium Non-Payment Reminder Letter serves as a formal notification that an insurance policy is at risk of cancellation due to overdue balances. This document is a final warning, detailing the exact amount owed and the grace period deadline to prevent a lapse in coverage. It is crucial to respond immediately to avoid losing financial protection or facing higher future rates. Always verify payment methods and contact your provider to ensure continuous protection and confirm that your policy remains active and compliant.

Final Policy Cancellation Warning Letter

A Final Policy Cancellation Warning Letter is a legal notification issued by an insurer before terminating coverage. It serves as a last chance for policyholders to resolve outstanding issues, such as unpaid premiums or missing documentation. Receiving this letter indicates that your protection will cease on a specific effective date unless immediate action is taken. To prevent a lapse in coverage, which can lead to higher future rates and financial liability, you must contact your agent or make the required payment before the stated deadline expires.

Life Insurance Policy Lapse Pending Letter

A Life Insurance Policy Lapse Pending Letter is a formal notice warning that your coverage is at risk due to unpaid premiums. It signifies the start of a grace period, typically 30 days, during which you must pay the balance to keep the policy active. If the deadline passes without payment, the contract terminates, and beneficiaries lose the death benefit. To prevent permanent loss of protection, contact your insurer immediately to settle the outstanding amount or discuss reinstatement options before the policy officially lapses.

Auto Insurance Premium Default Notice Letter

An Auto Insurance Premium Default Notice is a formal warning issued when a policyholder fails to pay their premium by the due date. Receiving this letter signifies an imminent risk of policy cancellation, which can lead to a lapse in coverage and legal penalties. To maintain protection, you must pay the outstanding balance within the specified grace period. Failure to act results in a Notice of Cancellation, potentially increasing future rates and leaving you financially vulnerable in the event of an accident or vehicle damage.

Impending Lapse and Reinstatement Option Letter

An Impending Lapse and Reinstatement Option Letter is a formal notification from an insurer warning that your policy will expire due to non-payment. This notice provides a grace period, allowing you to settle outstanding premiums before coverage terminates. Importantly, it outlines specific reinstatement options, detailing the steps required to restore a lapsed policy, such as paying late fees or submitting a health statement. Acting promptly on this letter is essential to prevent a permanent loss of protection and ensure continuous insurance coverage without needing to reapply for a new policy.

Final Premium Payment Demand Letter

A Final Premium Payment Demand Letter serves as a critical legal notice from an insurer regarding overdue balances. It acts as a formal warning that your policy is at risk of termination unless immediate payment is made. This document outlines the exact amount owed, the deadline for submission, and the consequences of non-payment, such as a permanent lapse in coverage. Receiving this letter indicates the end of the standard grace period, making it the final opportunity to maintain your protection and avoid potential liability risks or policy reinstatement fees.

Account Suspension and Impending Lapse Letter

An Account Suspension and Impending Lapse Letter is a critical formal notice indicating that your insurance coverage or service is at risk due to non-payment. This document serves as a final warning before your policy officially expires. To avoid a total loss of protection, you must pay the outstanding balance by the specified grace period deadline. Ignoring this letter results in a coverage gap, potentially leading to higher future premiums or the permanent termination of your contract. Immediate action is required to maintain your active status and financial security.

Courtesy Premium Past Due Reminder Letter

A Courtesy Premium Past Due Reminder Letter serves as a critical notification that an insurance payment is overdue. This formal notice helps policyholders avoid a coverage lapse by providing a grace period to settle the balance. It typically outlines the exact amount owed, the final payment deadline, and the potential consequences of non-payment. Receiving this letter is a vital opportunity to maintain continuous protection and ensure your policy remains active without legal or financial interruptions.

Agency Follow-Up on Impending Lapse Letter

An Agency Follow-Up on Impending Lapse Letter is a critical communication sent to policyholders before insurance coverage expires. This notice serves as a final reminder to secure renewal or payment, preventing a dangerous gap in protection. It highlights the exact expiration date and necessary steps to maintain active status. Timely response is essential because a coverage lapse can lead to higher premiums, legal penalties, or rejected claims. Always verify the payment deadline with your agent immediately upon receipt to ensure continuous financial security and avoid policy termination.

Overdue Premium Impending Lapse Letter

An Overdue Premium Impending Lapse Letter is a formal notice sent by insurance companies when a payment is missed. This document serves as a final warning that your coverage is at risk of termination. It typically outlines the specific grace period remaining and the exact amount required to keep the policy active. To prevent a total loss of protection, policyholders must settle the outstanding balance before the lapse date specified. Promptly addressing this notice ensures continuous financial security and avoids the difficult process of policy reinstatement or medical underwriting.

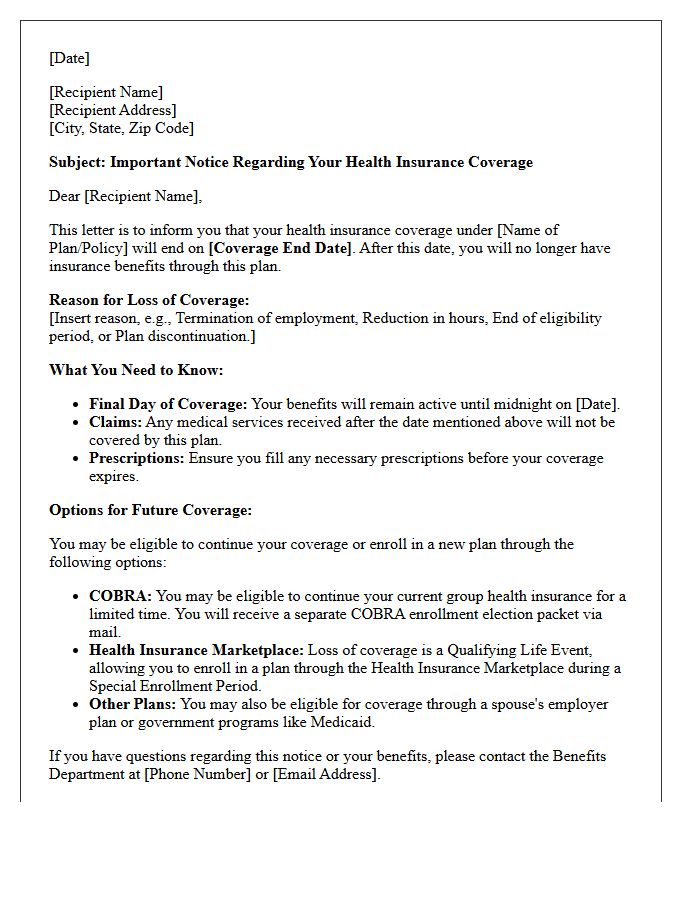

Impending Loss of Coverage Notice Letter

An Impending Loss of Coverage Notice Letter is a critical document informing you that your health insurance will soon end. Receiving this notice triggers a Special Enrollment Period, allowing you to sign up for a new plan outside of standard dates. It typically outlines the specific termination date and the reason for the cancellation, such as job loss or eligibility changes. To avoid a gap in protection, you must act quickly to explore Marketplace options or COBRA coverage before your current policy expires.

What is an Impending Lapse Notice for non-payment?

An Impending Lapse Notice is a formal notification sent by an insurance provider warning the policyholder that their coverage is at risk of being cancelled due to overdue premiums. It serves as a final reminder to make a payment before the policy officially terminates.

How long do I have to pay after receiving a lapse notice?

The timeframe varies by state law and insurance company, but it typically includes a grace period of 10 to 30 days from the date the notice was issued. The specific "Cancellation Effective Date" will be listed on the notice as the final deadline for payment.

Will my insurance coverage remain active during the lapse notice period?

Yes, your insurance coverage remains active during the grace period specified in the notice. However, if the outstanding balance is not paid by the deadline, coverage will cease retroactively or on the specified cancellation date, leaving you unprotected.

What happens if my insurance policy lapses?

If a policy lapses, you lose your insurance protection, which can lead to financial liability for claims, legal penalties for driving uninsured, and higher future premiums. Additionally, a lapse in coverage may result in being labeled a "high-risk" client by future insurers.

Can I reinstate my policy after it has lapsed for non-payment?

Reinstatement is often possible but not guaranteed. You may be required to pay all past-due premiums, a reinstatement fee, and sign a "Statement of No Loss" confirming no claims occurred during the lapsed period. Some insurers may require you to apply for a brand-new policy instead.

Comments