A term life insurance policy lapse notification informs policyholders that their coverage has ended due to unpaid premiums. Failing to address these alerts can result in a loss of financial protection for your beneficiaries. Understanding grace periods and reinstatement options is essential to maintaining your security. To help you manage this communication effectively, below are some ready to use template.

Image cover: Essential Term Life Insurance Lapse Notice Templates and Samples

Letter Samples List

- Official Term Life Policy Lapse Notification Letter

- Missed Premium Payment And Pending Lapse Letter

- Grace Period Expiration Warning Letter

- Final Term Life Policy Termination Letter

- Term Life Policy Reinstatement Opportunity Letter

- Outstanding Premium Balance Due Letter

- Insurance Agent Policy Lapse Follow-Up Letter

- Secondary Addressee Lapse Warning Letter

- Returned Payment And Pending Lapse Letter

- Evidence Of Insurability Request Letter

- Lapsed Policy Status Confirmation Letter

- Post-Lapse Insurance Options Letter

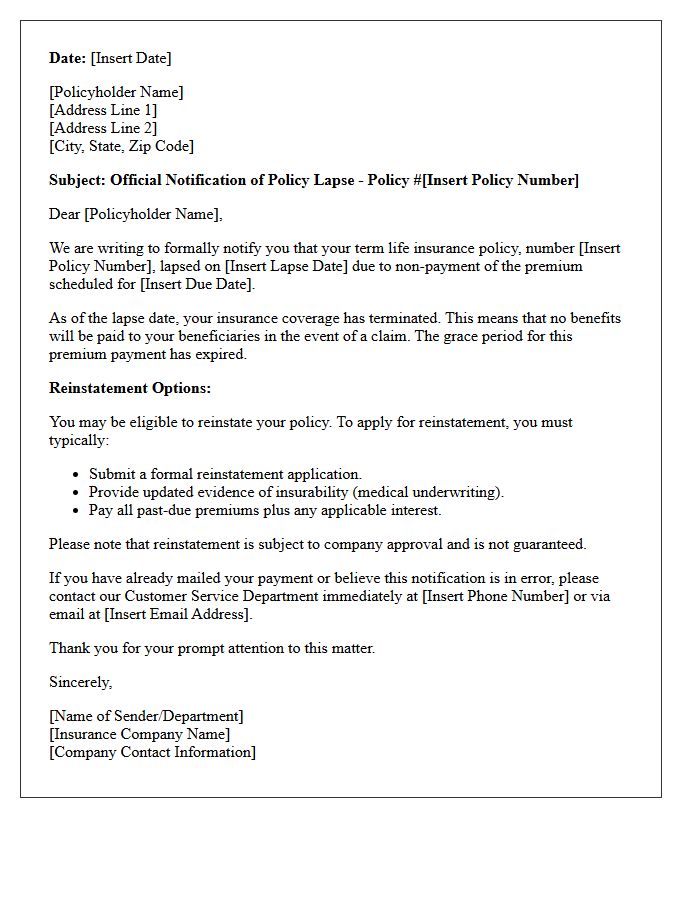

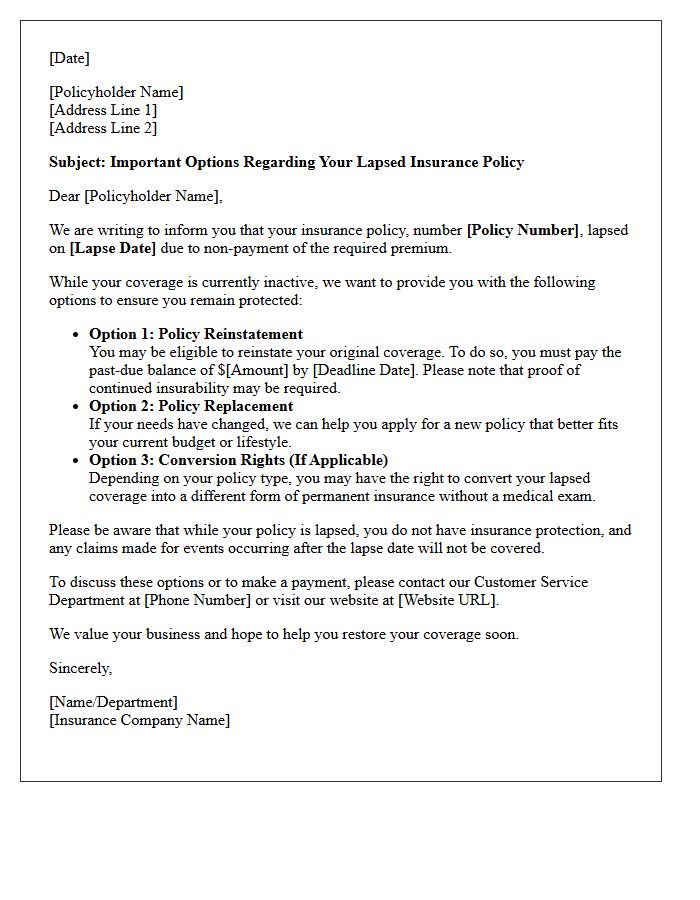

Official Term Life Policy Lapse Notification Letter

An Official Term Life Policy Lapse Notification Letter is a critical alert from your insurer. It warns that your coverage has terminated due to unpaid premiums. To avoid losing your financial safety net, you must act during the grace period, which is usually thirty days. This document outlines the specific steps required for reinstatement, which may include paying back premiums or providing new evidence of insurability. Ignoring this notice results in a permanent loss of benefits, leaving beneficiaries unprotected if an unexpected tragedy occurs.

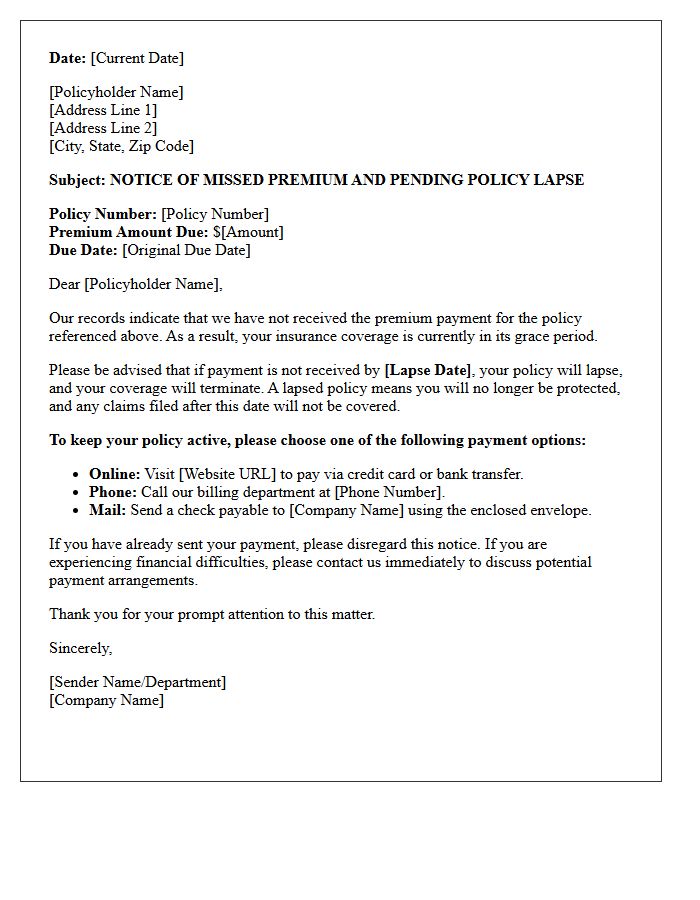

Missed Premium Payment And Pending Lapse Letter

Receiving a pending lapse letter means your insurance coverage is at risk due to a missed premium payment. To prevent a total loss of benefits, you must act during the grace period, which is the final window allowed to pay the overdue balance. If payment is not received by the specified deadline, the policy will terminate, leaving you without protection. Contact your insurer immediately to confirm the outstanding amount and explore reinstatement options to ensure your financial security remains intact and uninterrupted.

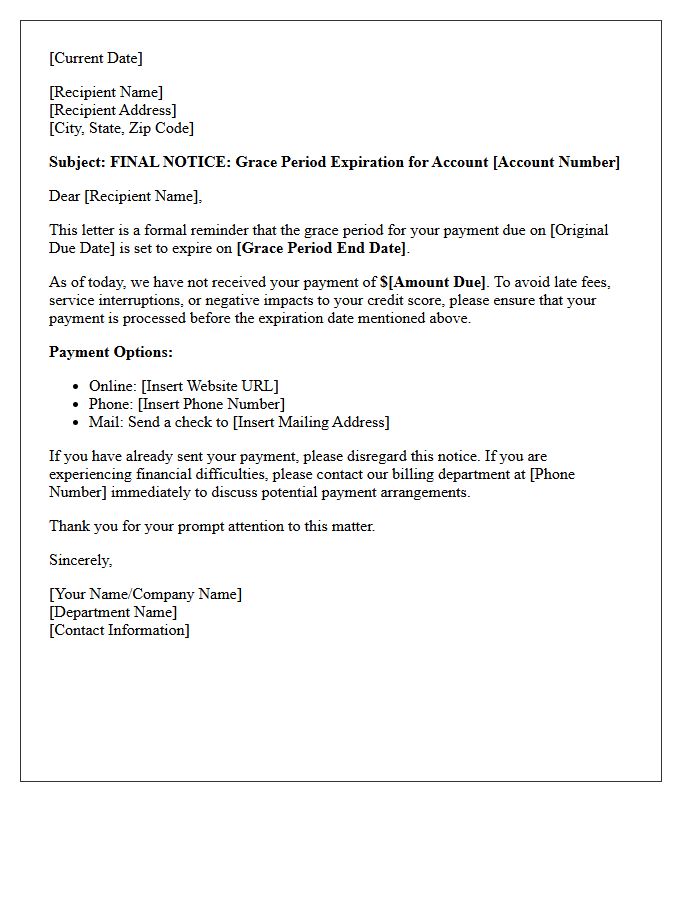

Grace Period Expiration Warning Letter

A Grace Period Expiration Warning Letter is a critical formal notice sent to policyholders or borrowers. It serves as a final reminder that the payment deadline has passed and the additional time allowed to settle the debt is ending. Receiving this notification is vital because failure to act immediately will result in a coverage lapse or loan default. To maintain your benefits and avoid financial penalties, you must ensure funds are received before the specified termination date. Always verify the remaining balance and payment methods to secure your standing.

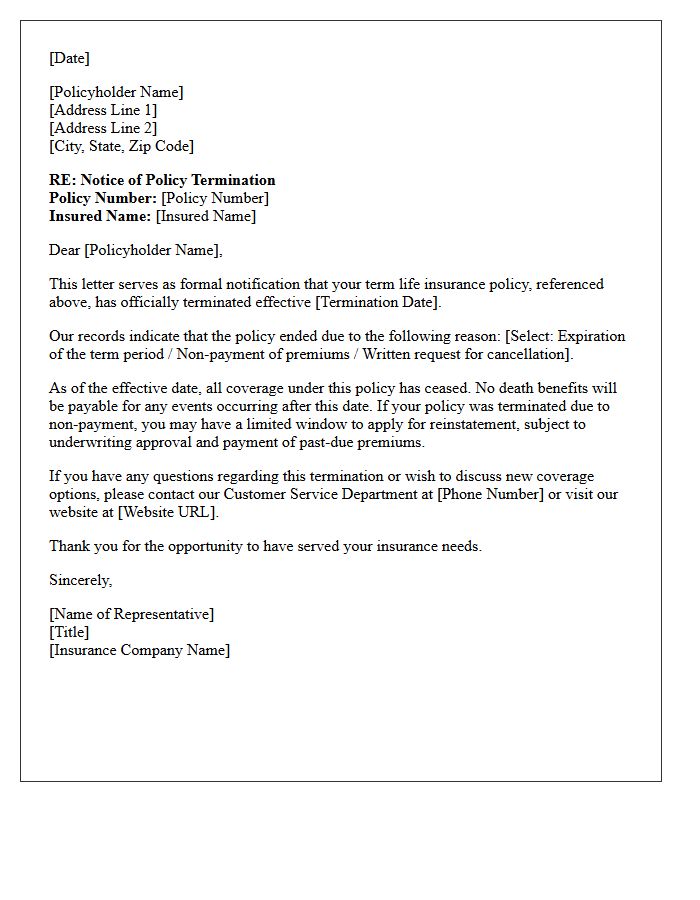

Final Term Life Policy Termination Letter

A Final Term Life Policy Termination Letter is a formal notification confirming that your life insurance coverage has officially ended. This document typically specifies the expiration date and confirms that death benefits are no longer payable. It is crucial to review this letter immediately to understand if the policy lapsed due to non-payment or reached its natural term limit. To maintain financial security, beneficiaries should verify if any conversion options exist, allowing them to transition into a permanent policy without a new medical exam before the final deadline.

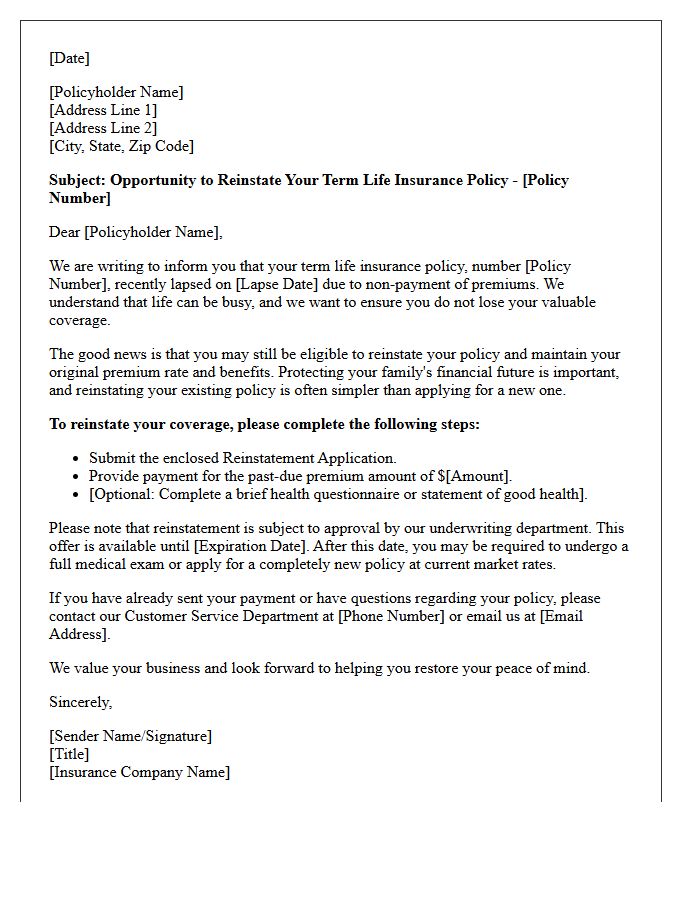

Term Life Policy Reinstatement Opportunity Letter

A Term Life Policy Reinstatement Opportunity Letter is a formal notice sent by insurers after a coverage lapse. It informs policyholders of the chance to restore their life insurance protection without purchasing a new plan. To regain coverage, you must typically pay all overdue premiums and may need to provide updated proof of insurability. Acting promptly on this reinstatement offer is essential, as it allows you to maintain original premium rates and avoid the higher costs often associated with aging or changes in your medical history.

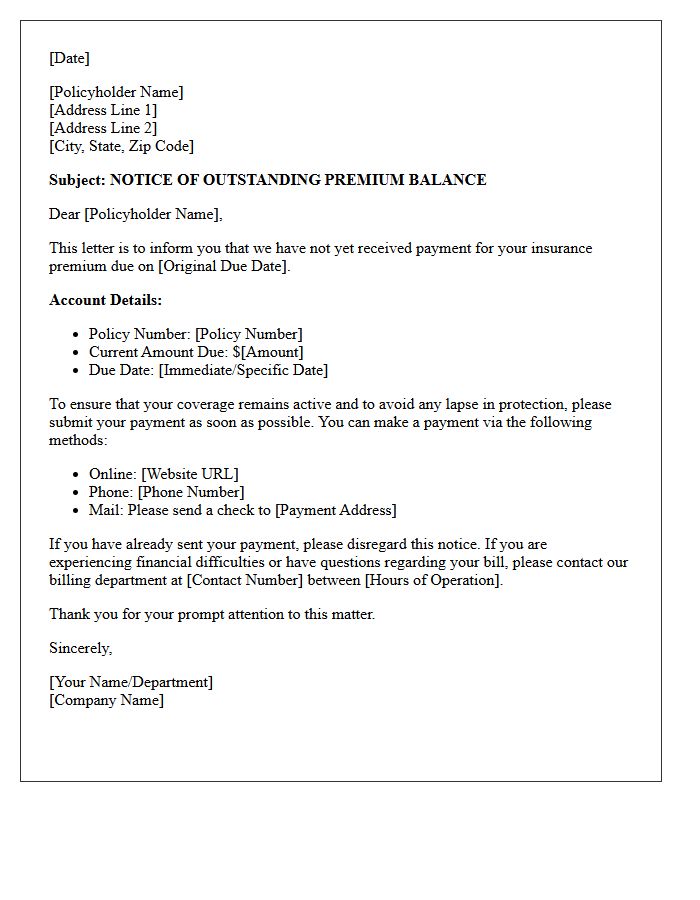

Outstanding Premium Balance Due Letter

An Outstanding Premium Balance Due Letter is a formal notice from an insurance provider indicating that a payment is late. This document serves as a critical warning that your coverage is at risk of cancellation. It typically outlines the exact amount owed, the original due date, and the final deadline to prevent a lapse in protection. To maintain continuous security and avoid policy termination, you must settle the arrears immediately. Reviewing this notice ensures you understand the grace period and any potential late fees applied to your account.

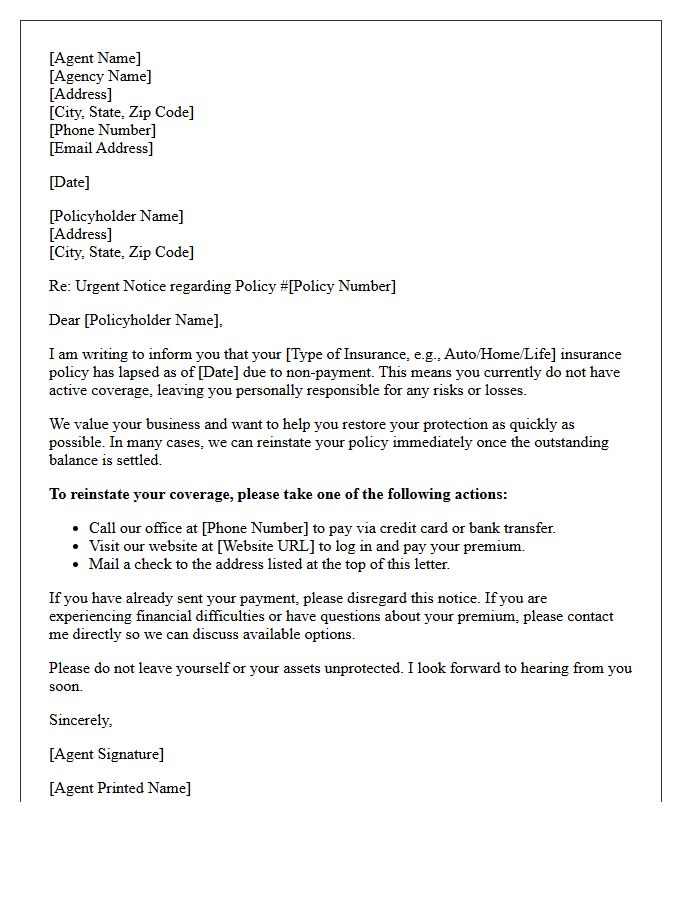

Insurance Agent Policy Lapse Follow-Up Letter

An insurance agent policy lapse follow-up letter is a critical retention tool designed to notify clients that their coverage has expired. This formal communication highlights the reinstatement process and the urgent risks of remaining uninsured. By clearly outlining payment options and grace period deadlines, agents can effectively recover lost premiums. A well-structured letter emphasizes continuous protection and provides direct contact information to resolve billing issues, ensuring long-term client loyalty and mitigating potential financial liability for the policyholder.

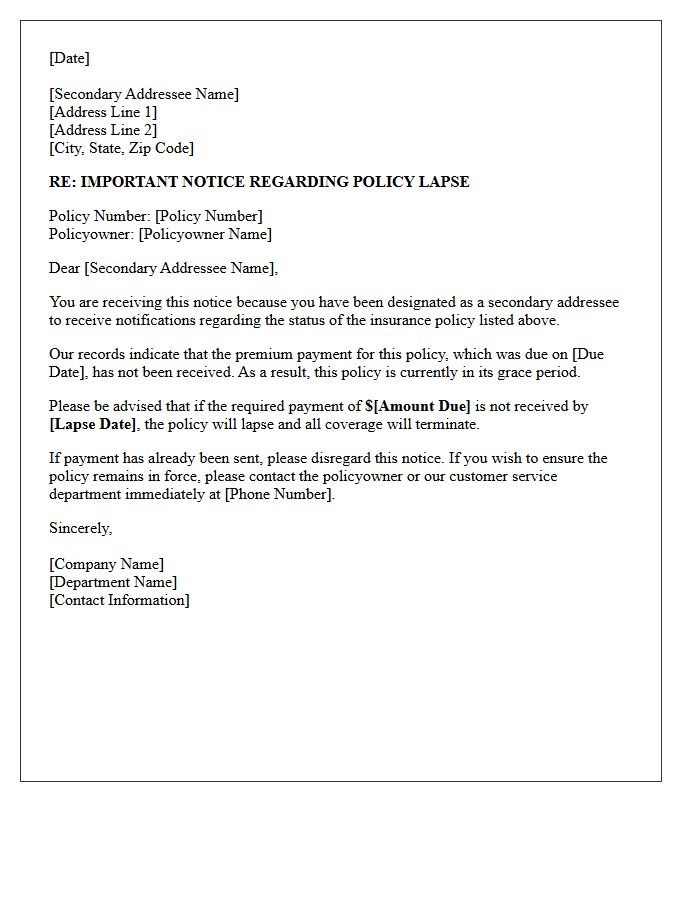

Secondary Addressee Lapse Warning Letter

A Secondary Addressee Lapse Warning Letter is a critical safeguard for long-term care insurance policies. It notifies a designated third party if a premium is unpaid and the policy is at risk of terminating. This ensures that vulnerable policyholders, particularly those facing cognitive decline or health challenges, do not lose vital coverage due to simple oversight. Designating a secondary contact provides an essential safety net, allowing a trusted person to intervene and prevent a coverage lapse before the grace period expires.

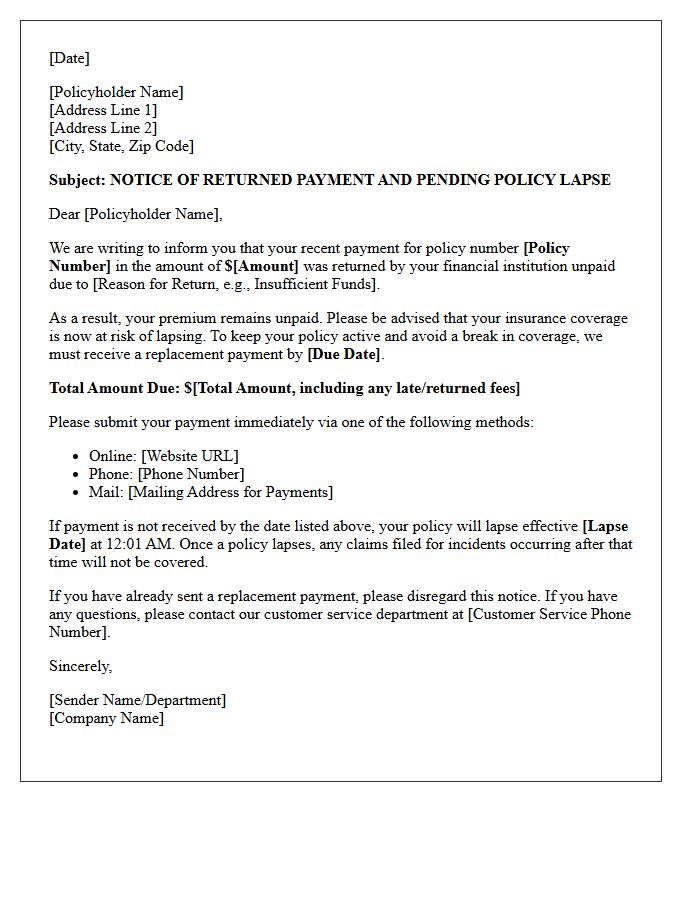

Returned Payment And Pending Lapse Letter

Receiving a Returned Payment and Pending Lapse Letter indicates your insurance premium payment failed, often due to insufficient funds or incorrect banking details. This notification serves as a critical grace period warning, informing you that your coverage is at risk of cancellation. To avoid a total loss of protection, you must provide a valid payment method immediately. Failure to resolve the balance before the specified deadline will result in a policy lapse, potentially leading to higher future rates or a denial of claims during the uninsured period.

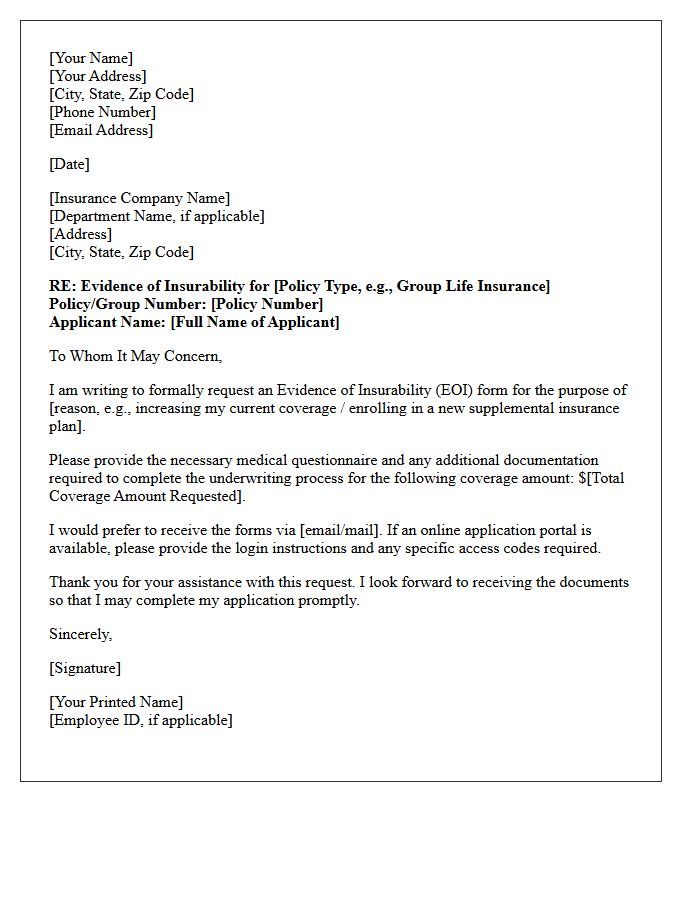

Evidence Of Insurability Request Letter

An Evidence of Insurability (EOI) request letter is a formal document from an insurer requiring medical proof of good health before approving additional coverage. This process typically occurs when applying for life or disability insurance exceeding guaranteed issue limits or during late enrollment. Applicants must usually complete a health questionnaire or undergo a medical exam to assess risk. Providing accurate information is vital, as any discrepancies can lead to claim denials. Always submit the requested documentation promptly to ensure your supplemental benefits become effective without unnecessary delays.

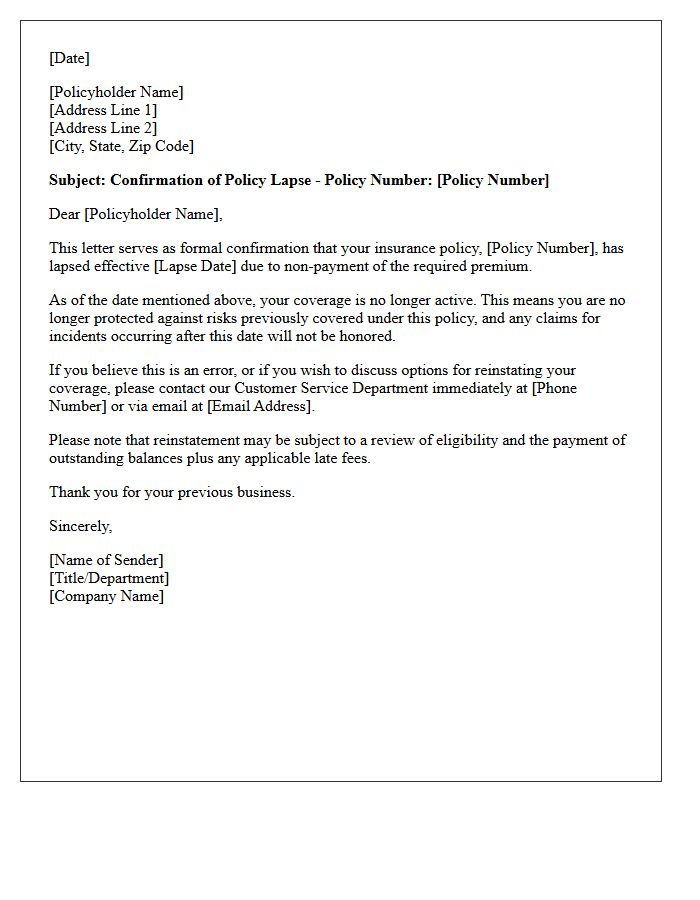

Lapsed Policy Status Confirmation Letter

A Lapsed Policy Status Confirmation Letter is an official document from an insurer verifying that coverage has ended due to non-payment of premiums. This formal notice confirms the exact date the policy became inactive and outlines the loss of financial protection. It is essential for policyholders to understand their current insurance standing and serves as necessary documentation when attempting to reinstate coverage or proving a gap in history to future providers. Receiving this letter indicates that the beneficiary is no longer entitled to policy benefits or claims payouts.

Post-Lapse Insurance Options Letter

A Post-Lapse Insurance Options Letter is a crucial notice sent when a policy terminates due to non-payment. This document outlines reinstatement rights, allowing policyholders to restore coverage by paying overdue premiums and meeting health requirements. It may also detail options like non-forfeiture benefits or converting to a different plan. Promptly reviewing this letter is essential to avoid a permanent loss of protection and to understand specific deadlines for recovering your insurance benefits before the grace period and reinstatement window fully expire.

What is a term life insurance policy lapse notification?

A term life insurance policy lapse notification is a formal notice sent by an insurance provider informing the policyholder that their coverage has ended due to non-payment of premiums. This document signifies that the death benefit is no longer active and the grace period has expired.

How long is the grace period before a life insurance policy lapses?

Most term life insurance policies include a standard grace period of 30 or 31 days following a missed premium payment. During this window, the policy remains in force, and coverage is maintained if the outstanding balance is paid before the period ends.

Will I receive a warning before my term life insurance policy cancels?

Yes, insurance regulations typically require carriers to send a "pending lapse" or "late payment" notice to the policyholder's last known address or email. This notification provides a specific deadline to pay the overdue premium to prevent a total loss of coverage.

Can a lapsed term life insurance policy be reinstated?

Many insurers allow policy reinstatement within a specific timeframe (often 1 to 5 years) after a lapse. However, the policyholder may be required to pay all back premiums with interest and provide new evidence of insurability, such as a medical exam, to prove they still meet underwriting requirements.

Does a life insurance lapse notification affect my credit score?

No, a term life insurance policy lapse does not typically affect your credit score. Life insurance is not a debt-based product; therefore, non-payment simply results in the termination of the contract and the cessation of coverage rather than a report to credit bureaus.

Comments