A Universal Life grace period provides a critical safety net if your policy lacks sufficient cash value to cover monthly deductions. If you fail to make required payments, your insurer must issue a formal lapse warning before coverage terminates. Understanding these timelines is essential to maintaining your financial protection. To help you communicate with your provider, below are some ready to use templates.

Image cover: Protecting Your Coverage: Universal Life Grace Period Notices and Reinstatement Templates

Letter Samples List

- Universal Life Grace Period Notification Letter

- Impending Lapse Warning Letter For Universal Life Policy

- Notice Of Grace Period Activation Letter

- Universal Life Policy Lapse Imminent Warning Letter

- Action Required Grace Period Alert Letter

- Universal Life Premium Past Due Grace Period Letter

- Final Warning Of Universal Life Policy Lapse Letter

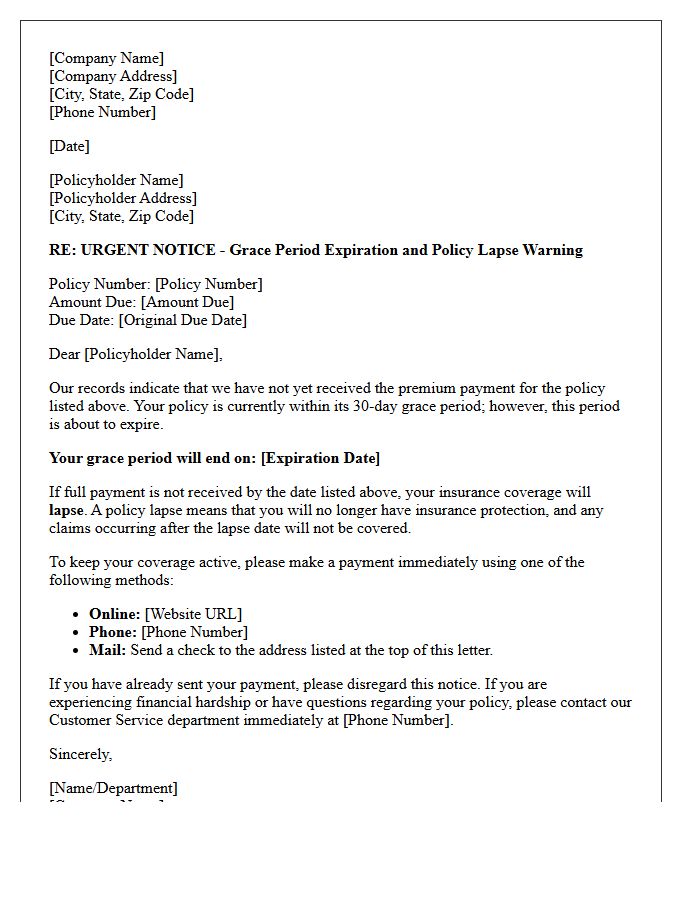

- Grace Period Expiration And Lapse Warning Letter

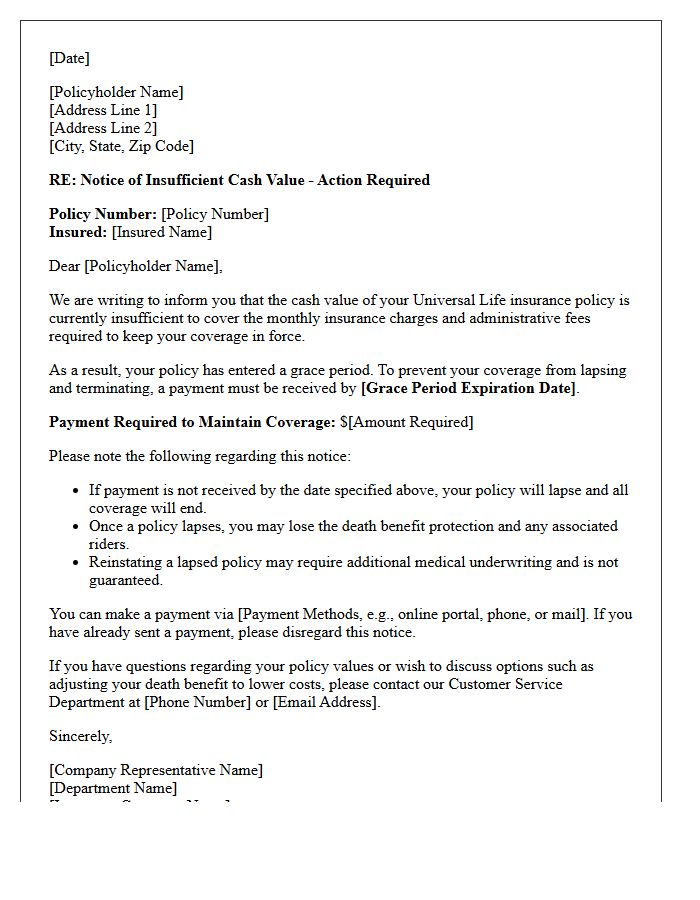

- Universal Life Insurance Insufficient Cash Value Letter

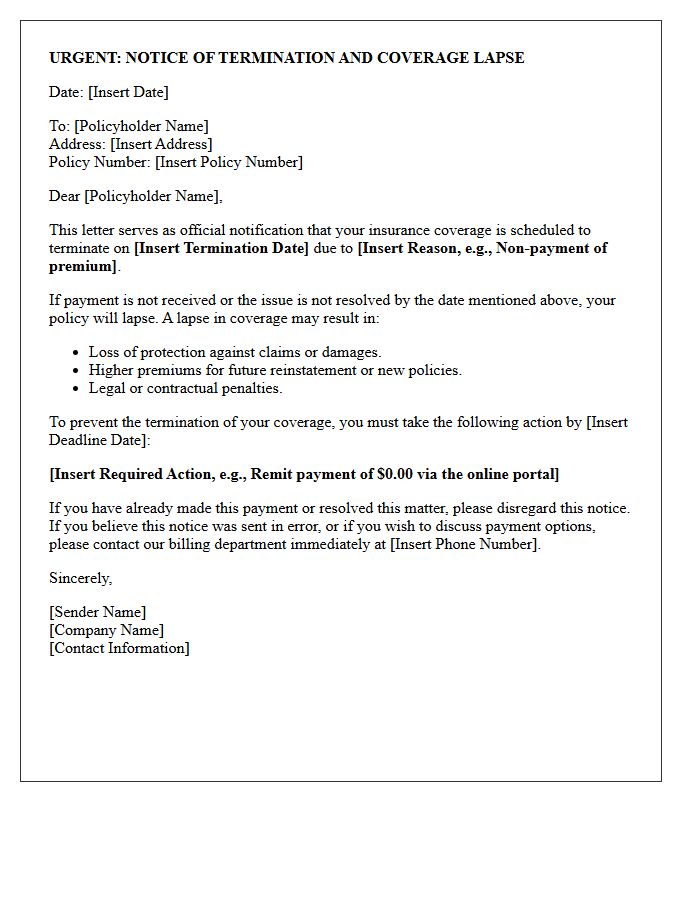

- Warning Of Coverage Termination And Lapse Letter

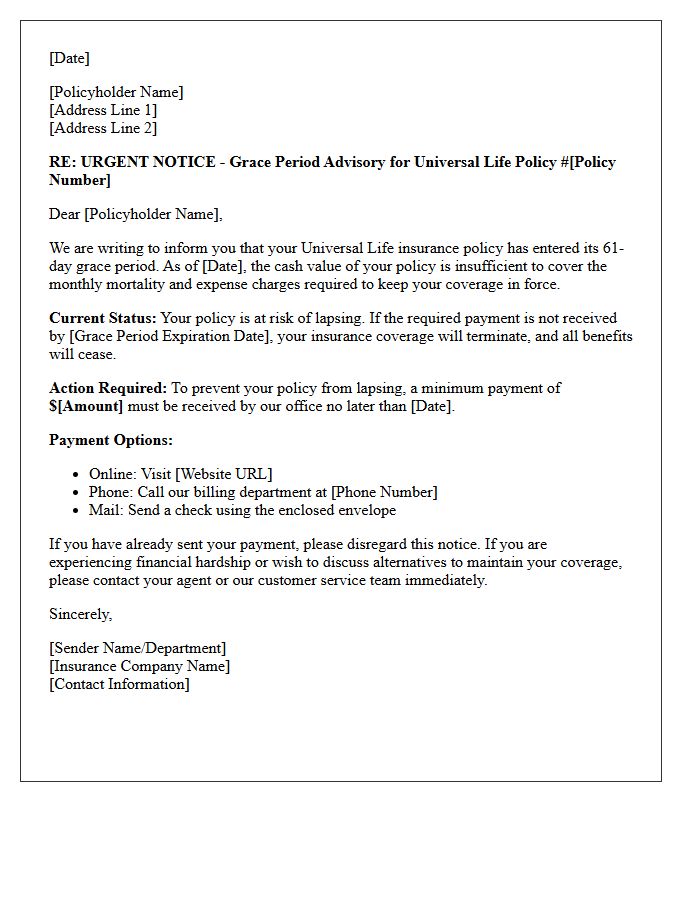

- Urgent Universal Life Grace Period Advisory Letter

- Notice Of Impending Lapse Pending Payment Letter

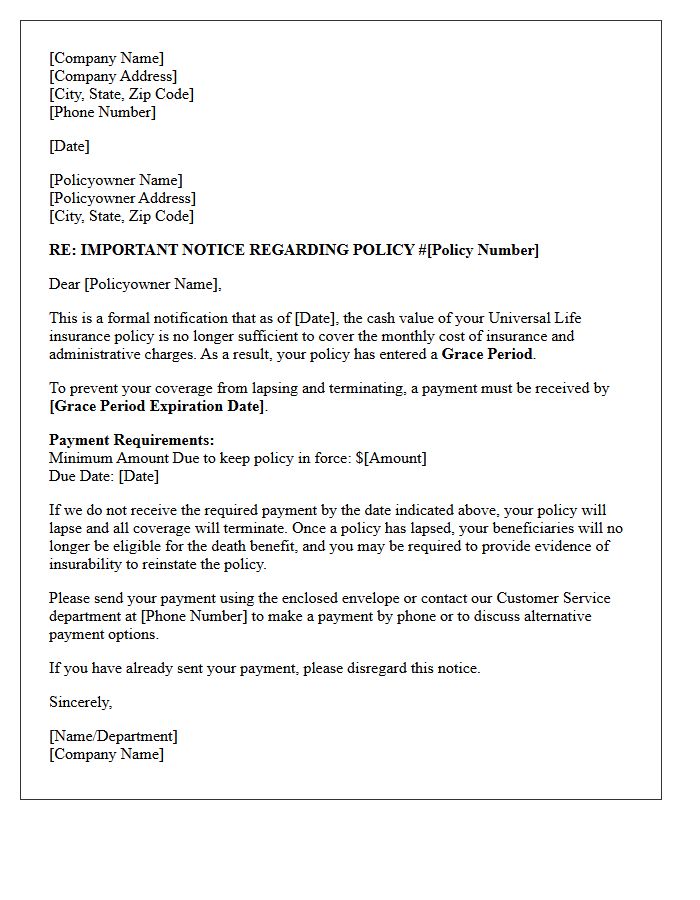

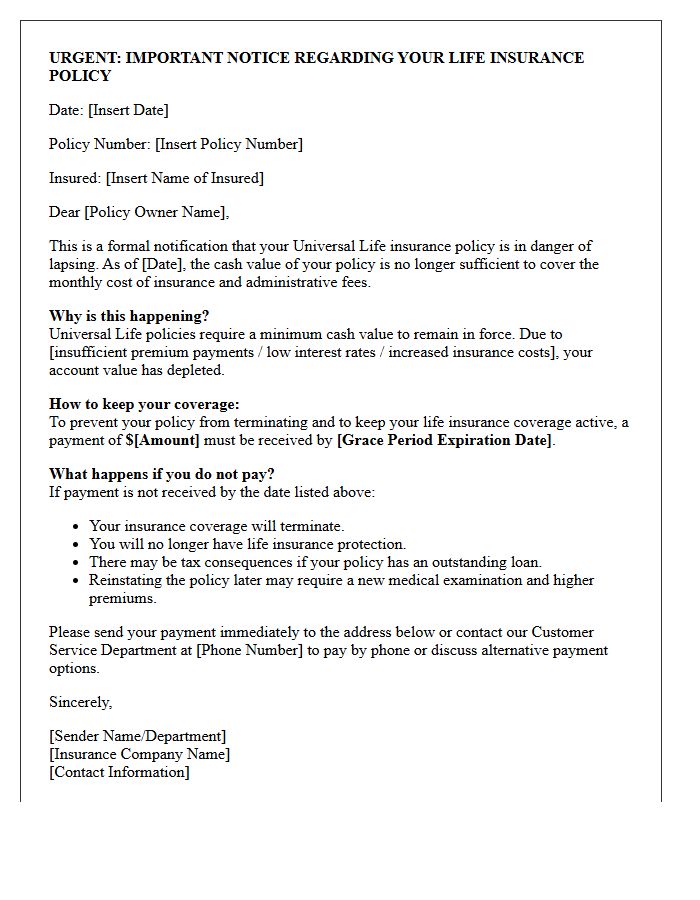

Universal Life Grace Period Notification Letter

A Universal Life Grace Period Notification Letter is a critical legal notice sent when a policy's cash value is insufficient to cover monthly insurance costs. It informs the policyholder that their coverage is at risk of lapsing due to underfunding. The document outlines the minimum premium payment required and the specific deadline to keep the policy active. Receiving this letter serves as a final warning to take immediate action, ensuring that the death benefit remains in force and permanent protection is maintained for beneficiaries.

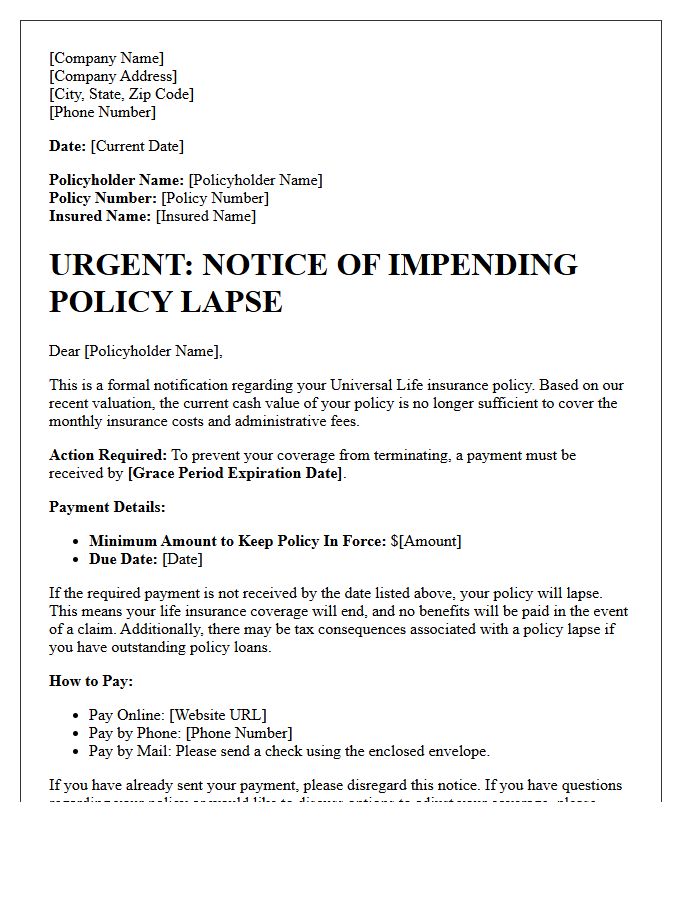

Impending Lapse Warning Letter For Universal Life Policy

An impending lapse warning letter is a critical notice indicating your universal life insurance policy is at risk of terminating due to insufficient cash value. This happens when monthly mortality charges and administrative fees exceed your current account balance and premium payments. To keep coverage active, you must pay the specified minimum amount before the grace period expires. Failure to act results in a total loss of protection without a death benefit payout. Review your policy's performance regularly to avoid unexpected coverage termination.

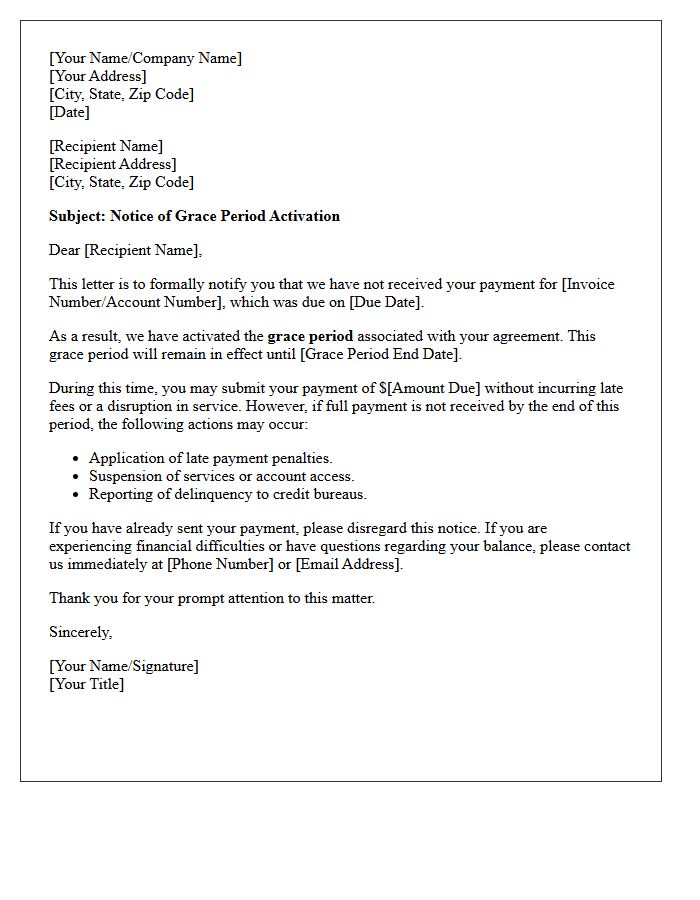

Notice Of Grace Period Activation Letter

A Notice of Grace Period Activation Letter is a formal document sent by a service provider or lender to inform you that a payment is overdue. It confirms that a specified extension has been granted, allowing you to settle the balance without immediate penalties or service disconnection. During this period, you must take urgent action to pay the outstanding amount. Failure to comply before the grace period expires typically results in late fees, interest charges, or a permanent suspension of your account and services.

Universal Life Policy Lapse Imminent Warning Letter

Receiving a Universal Life Policy Lapse Imminent Warning Letter signifies your coverage is at risk due to insufficient cash value to cover monthly insurance costs. This usually happens when interest rates drop or premium payments are too low. To prevent a total loss of benefits, you must act quickly by paying the requested amount or adjusting your death benefit. Ignoring this notice leads to a grace period expiration, after which the policy terminates without value, potentially creating a taxable event on outstanding policy loans.

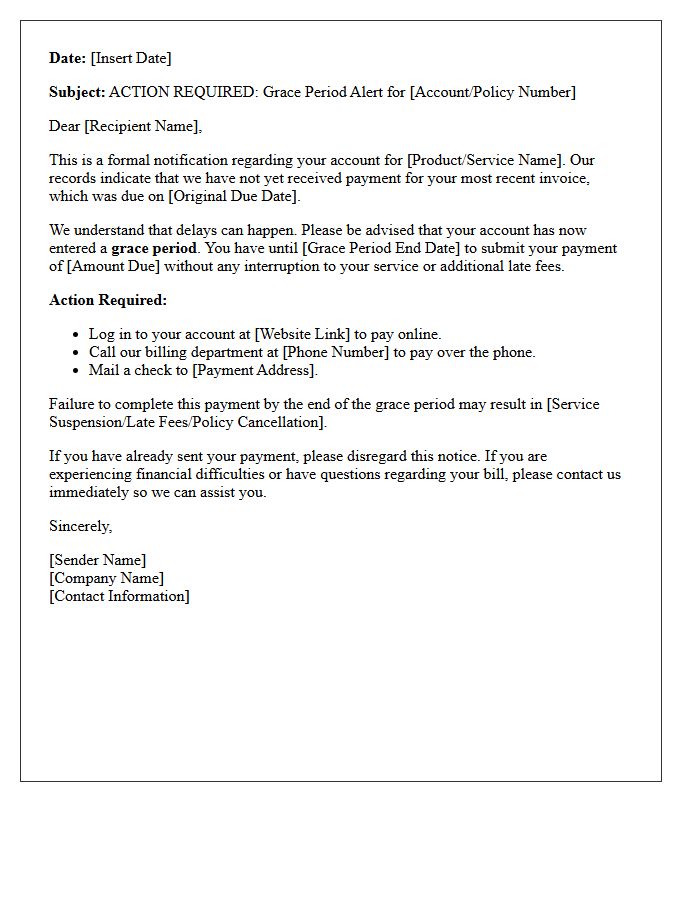

Action Required Grace Period Alert Letter

An Action Required Grace Period Alert Letter is a formal notification informing policyholders that their premium payment is overdue. This document serves as a critical warning before coverage cancellation occurs. It specifies the outstanding balance, the final deadline for payment, and the consequences of non-payment. Receiving this letter indicates you are within a temporary extension period, allowing you to maintain active insurance protection. To avoid a lapse in coverage, immediate action is necessary to settle the account within the timeframe specified in the notice.

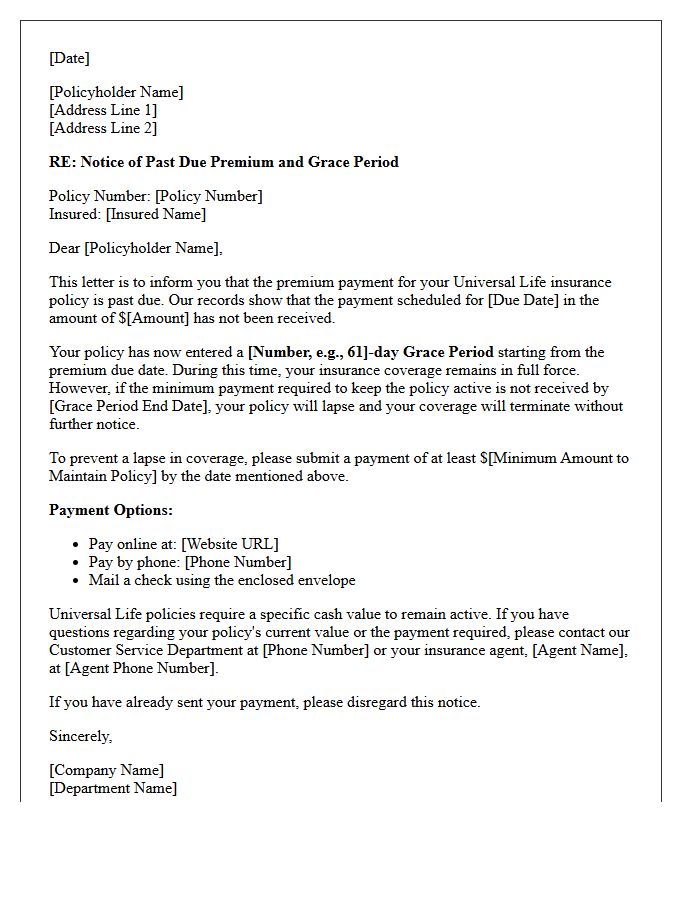

Universal Life Premium Past Due Grace Period Letter

A Universal Life Premium Past Due Grace Period Letter is a formal notice sent when your policy lacks sufficient cash value to cover monthly charges. This critical document initiates a grace period, typically lasting 61 days, providing a final window to pay the required premium and prevent a total lapse in coverage. If payment is not received by the specified deadline, the insurance policy will terminate, resulting in a loss of death benefits. It is essential to act immediately to ensure your life insurance protection remains active and enforceable.

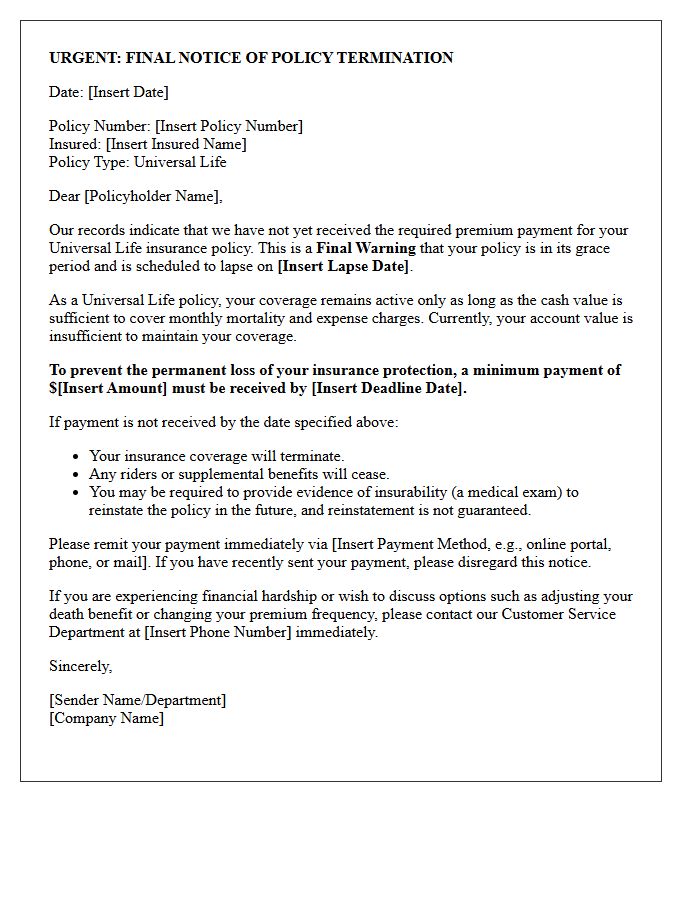

Final Warning Of Universal Life Policy Lapse Letter

Receiving a Final Warning Of Universal Life Policy Lapse letter indicates your insurance coverage is at critical risk due to insufficient cash value. This notice is a legal requirement providing a final grace period to pay the minimum premium necessary to keep the policy active. Failure to act immediately results in a total termination of benefits and loss of protection. To prevent a lapse, policyholders should contact their provider to discuss reinstatement options, catch-up payments, or adjusting the death benefit to lower ongoing costs before the specified deadline.

Grace Period Expiration And Lapse Warning Letter

Receiving a lapse warning letter indicates your insurance policy is nearing termination due to unpaid premiums. Once the grace period expires, your coverage officially ends, leaving you without financial protection. This formal notice serves as a final opportunity to settle outstanding balances before the contract is canceled. To maintain active coverage and avoid the complexities of policy reinstatement, you must submit payment immediately. Ignoring this document results in a loss of benefits and may lead to higher future rates or a total denial of coverage based on your updated risk profile.

Universal Life Insurance Insufficient Cash Value Letter

Receiving a Universal Life Insurance Insufficient Cash Value Letter is a critical warning that your policy is at risk of lapsing. This occurs when the internal cash account can no longer cover rising insurance costs, often due to low interest rates or skipped payments. To keep coverage active, you must pay the requested catch-up premium immediately. Ignoring this notice means losing your death benefit and potential tax advantages. Review your policy illustration with an advisor to determine if increasing premiums or adjusting the face amount is necessary for long-term sustainability.

Warning Of Coverage Termination And Lapse Letter

Receiving a Warning of Coverage Termination means your insurance policy is at risk of a lapse due to unpaid premiums or missing documentation. This formal notice serves as a final alert before your benefits officially expire. It is crucial to take immediate action by submitting the required payment or information before the specified deadline to maintain protection. A coverage gap can lead to higher future rates, legal penalties, or financial loss if an incident occurs while uninsured. Always contact your provider directly to confirm your current policy status and ensure continuous security.

Urgent Universal Life Grace Period Advisory Letter

An Urgent Universal Life Grace Period Advisory Letter is a critical notice indicating your policy is at risk of lapsing due to insufficient cash value. This formal warning signifies that your premium payments have not covered insurance costs, triggering a grace period typically lasting 30 to 61 days. To maintain coverage and prevent permanent loss of benefits, you must remit the specified minimum payment immediately. Ignoring this document can result in the termination of your life insurance policy without further notice, leaving beneficiaries unprotected.

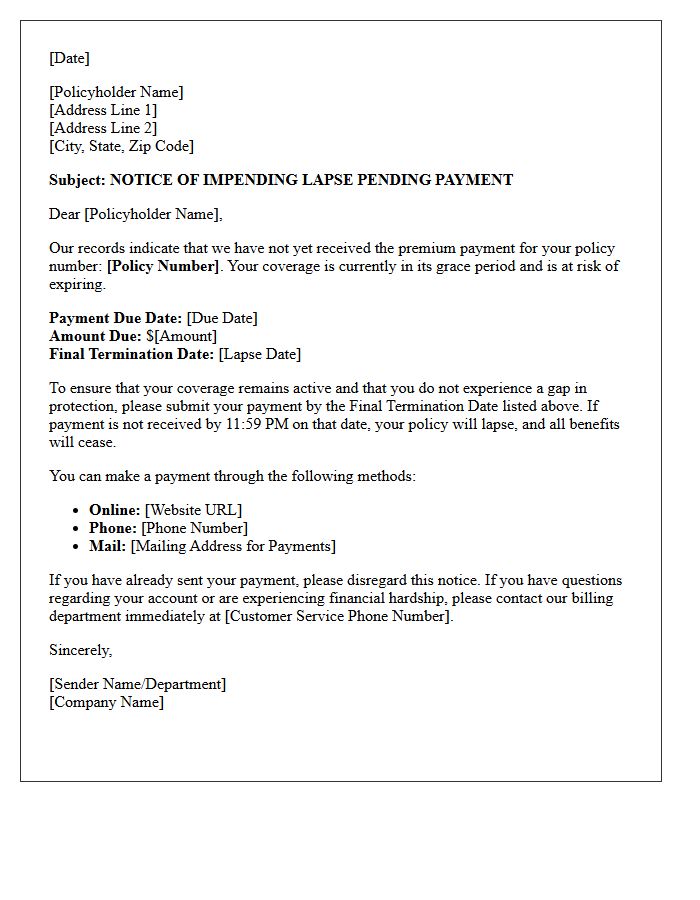

Notice Of Impending Lapse Pending Payment Letter

A Notice Of Impending Lapse Pending Payment Letter is a critical warning from your insurance provider. It indicates your coverage is at risk of cancellation due to unpaid premiums. To maintain active protection, you must submit the outstanding balance by the specified deadline. Failure to act will result in a lapse, leaving you without legal or financial coverage and potentially leading to higher future rates. Always verify the grace period mentioned in the letter to ensure your policy remains active and avoid costly reinstatement fees.

What is the standard grace period for a Universal Life insurance policy?

Most Universal Life insurance policies include a 31-day grace period that begins the day your policy's cash surrender value is insufficient to cover the monthly mortality and expense charges. During this window, your coverage remains active while you arrange the necessary premium payment.

How will I be notified if my Universal Life policy is at risk of lapsing?

Insurance carriers are legally required to send a written lapse warning notice to your last known address at least 30 days before coverage terminates. This notice will specify the exact premium amount required to keep the policy in force and the deadline by which the payment must be received.

Can a Universal Life policy lapse if I have been making regular payments?

Yes, if the internal cost of insurance (COI) rises or if interest credited to the cash value decreases, your scheduled payments may no longer be sufficient to cover monthly deductions. If the cash value hits zero, the policy enters the grace period regardless of your payment history.

What happens to the death benefit during the grace period?

The full death benefit remains in effect throughout the duration of the grace period. However, if the insured passes away during this time, the insurance company will typically deduct the overdue premium amount from the final payout sent to the beneficiaries.

Is it possible to reinstate a Universal Life policy after the grace period ends?

If a policy lapses after the grace period, most companies allow reinstatement within 3 to 5 years. This process generally requires "evidence of insurability" (a new medical exam), payment of all back premiums, and interest on the overdue amount to restore the original terms of the contract.

Comments