As empty nesters transition to smaller homes, evaluating liability risks is essential. Relocating often changes your risk profile, making an Umbrella Policy Letter a vital tool for ensuring comprehensive protection against unforeseen legal claims. This guide explains how to secure your financial future during this lifestyle shift. To help you communicate with your insurance provider, below are some ready to use template.

Image cover: Maximize Your Protection: Downsizing Guide and Umbrella Policy Templates for Empty Nesters

Letter Samples List

- Empty Nester Downsizing Insurance Review Letter

- Asset Protection and Umbrella Policy Recommendation Letter

- Downsizing Your Home Coverage Adjustment Letter

- Comprehensive Umbrella Policy Introduction Letter

- Removing Dependents From Auto Insurance Update Letter

- Empty Nester Lifestyle Change and Umbrella Policy Letter

- Post-Retirement Liability and Umbrella Policy Letter

- Condominium Insurance Transition for Downsizers Letter

- Protecting Acquired Wealth With an Umbrella Policy Letter

- Downsized Property and Adjusted Premium Notification Letter

- High Net Worth Umbrella Policy Coverage Proposal Letter

- Relocation and Downsizing Insurance Policy Transfer Letter

- Empty Nester Premium Savings and Umbrella Upgrade Letter

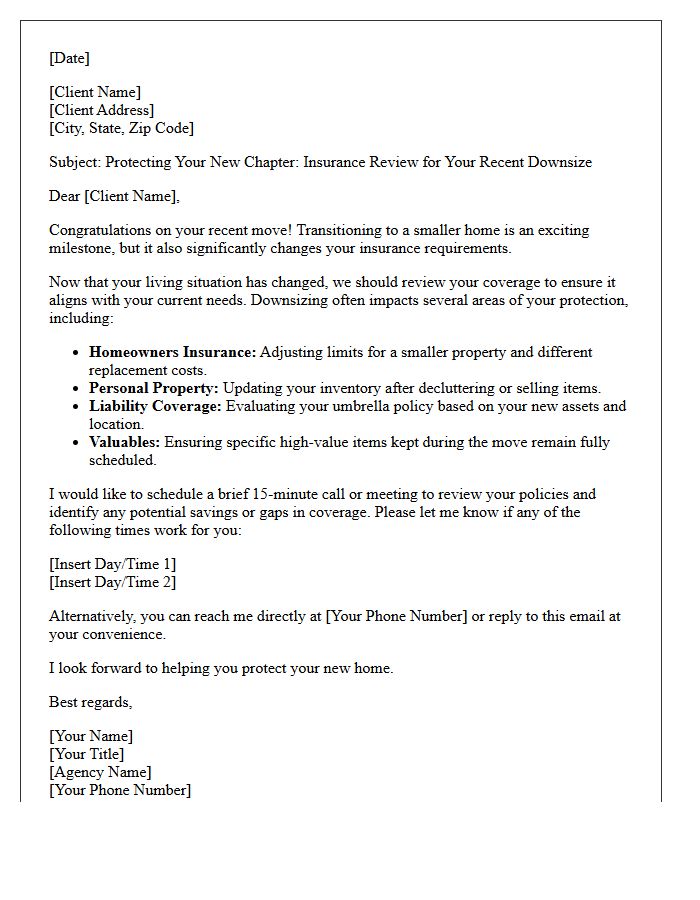

Empty Nester Downsizing Insurance Review Letter

An Empty Nester Downsizing Insurance Review Letter is a vital tool for adjusting coverage after children move out. It initiates a policy update to reflect your new lifestyle and potential move to a smaller home. This review identifies opportunities for premium savings as you reduce square footage and personal property limits. Highlighting changes in liability exposure and high-value assets ensures your protection remains accurate. Proactively sending this letter helps align your insurance costs with your current needs, preventing overpayment while securing your financial future during this significant life transition.

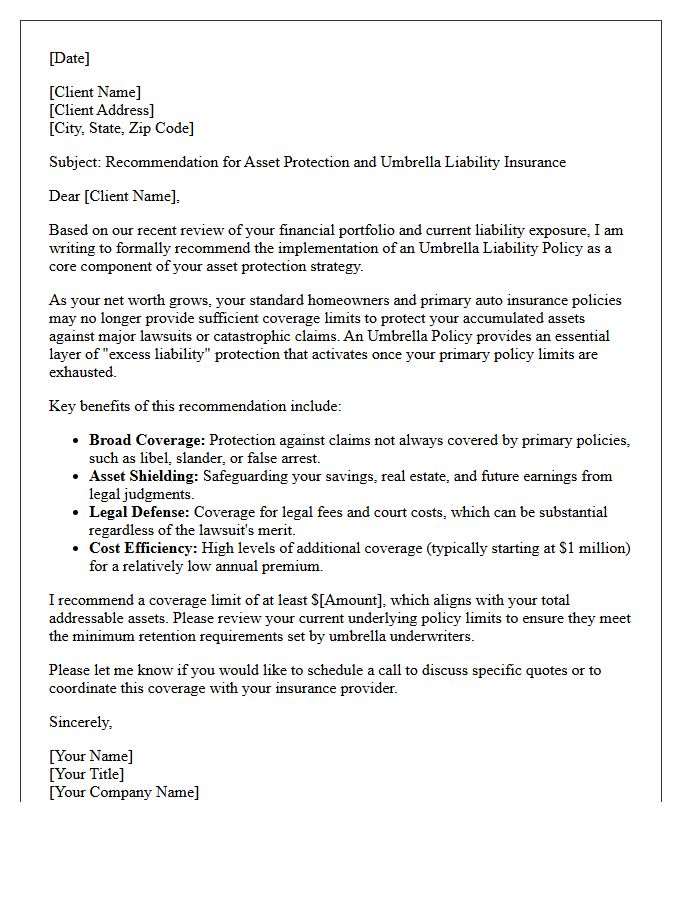

Asset Protection and Umbrella Policy Recommendation Letter

An asset protection strategy is essential for safeguarding your personal wealth against unforeseen litigation and liability claims. We strongly recommend an umbrella policy to provide an additional layer of coverage beyond your standard auto and homeowners insurance limits. This cost-effective solution protects your future earnings and physical assets from devastating legal judgements. By increasing your liability threshold, you ensure comprehensive financial security and peace of mind. Reviewing your current coverage ensures your net worth remains insulated from high-risk events and potential lawsuits that exceed primary policy boundaries.

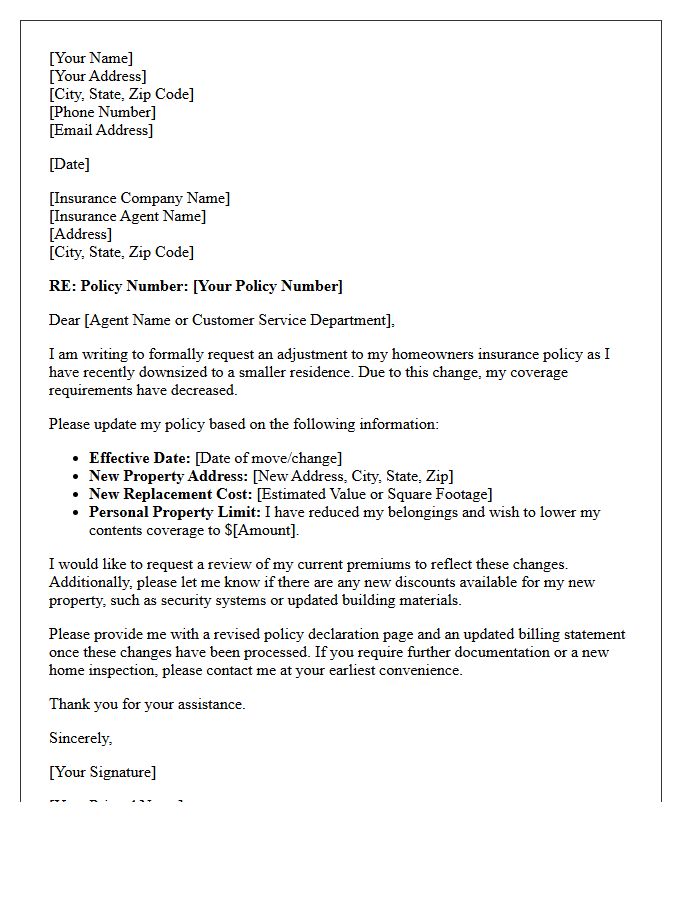

Downsizing Your Home Coverage Adjustment Letter

A Downsizing Your Home Coverage Adjustment Letter notifies your insurer that you are moving to a smaller property. This document is essential to recalibrate replacement costs and lower your premiums based on reduced square footage. It ensures your policy accurately reflects your new asset value while preventing overpayment. Promptly sending this written notice protects your financial interests and maintains valid liability protection. Always confirm that your coverage limits align with your new residence to avoid gaps during the transition between homes.

Comprehensive Umbrella Policy Introduction Letter

A Comprehensive Umbrella Policy Introduction Letter serves as a vital notification to clients about enhancing their risk management. It explains how an umbrella policy provides an essential layer of excess liability coverage beyond standard auto and homeowners insurance limits. The letter highlights the importance of protecting personal assets against catastrophic legal claims and unforeseen lawsuits. By emphasizing gaps in primary coverage, this document encourages policyholders to secure extended financial protection, ensuring comprehensive security for their future and peace of mind in an increasingly litigious environment.

Removing Dependents From Auto Insurance Update Letter

A formal Removing Dependents From Auto Insurance Update Letter serves as written notification to your provider to adjust your policy. It is crucial to provide the driver's full name and the effective date of removal to ensure accurate billing. This process typically reduces your premium once the individual is no longer a resident or has obtained their own coverage. Always request a written confirmation from your insurer to verify that the liability updates have been processed correctly, protecting you from paying unnecessary costs for inactive drivers on your plan.

Empty Nester Lifestyle Change and Umbrella Policy Letter

Transitioning into an empty nester lifestyle often involves downsizing or travel, which shifts your risk profile. During this change, you may receive an Umbrella Policy Letter from your insurer. This document suggests an extra layer of liability protection beyond standard auto or home coverage. As children move out, your assets and net worth might grow, making you a target for lawsuits. Securing an umbrella policy is a vital step in protecting your financial future and ensuring asset preservation during your retirement years.

Post-Retirement Liability and Umbrella Policy Letter

A post-retirement liability letter confirms that your Umbrella Policy remains in effect after leaving professional practice. This document is essential for maintaining continuous coverage against claims arising from prior acts. Even after retiring, you face potential lawsuits from past professional services. Ensuring your personal assets are protected through an extended reporting period or a tail policy prevents financial ruin. Always verify with your insurer that your excess liability limits adequately cover residual risks to guarantee long-term peace of mind during retirement.

Condominium Insurance Transition for Downsizers Letter

When moving from a house to a condo, a Condominium Insurance Transition for Downsizers Letter is essential to avoid coverage gaps. This document informs your provider about your new master policy details, ensuring you only pay for personal property and liability. It highlights the shift from standard homeowners insurance to a HO-6 policy, which covers "walls-in" assets and assessments. Providing this letter promptly ensures your asset protection remains continuous while potentially lowering your premiums during this significant lifestyle change.

Protecting Acquired Wealth With an Umbrella Policy Letter

An umbrella policy is a critical layer of liability coverage designed for protecting acquired wealth. Once your primary auto or home insurance limits are exhausted by a lawsuit, this policy provides supplemental protection against catastrophic financial claims. It serves as a safety net for your assets, savings, and future earnings, shielding them from legal judgments or settlements. For high-net-worth individuals, this cost-effective strategy ensures that a single accident does not lead to total financial ruin, preserving your long-term legacy and security.

Downsized Property and Adjusted Premium Notification Letter

A Downsized Property and Adjusted Premium Notification Letter informs policyholders that their insurance coverage has been modified due to a reduction in property size or value. This formal notice confirms that the premium amount has been recalculated to reflect the lower risk level. It is essential to review the document to ensure the new policy limits accurately match your current assets. Retaining this letter is crucial for maintaining precise financial records and verifying that you are no longer paying for unnecessary coverage after downsizing your primary residence or commercial space.

High Net Worth Umbrella Policy Coverage Proposal Letter

A High Net Worth Umbrella Policy Coverage Proposal Letter outlines essential excess liability protection for affluent clients. It details how the policy provides an additional layer of security above standard homeowners and auto insurance limits, specifically targeting risks like personal injury or costly lawsuits. This document highlights critical asset protection strategies, explaining how it safeguards wealth from catastrophic claims. It often includes customized limits and specialized endorsements, ensuring comprehensive coverage tailored to high-value lifestyles and complex legal exposures not addressed by basic insurance policies.

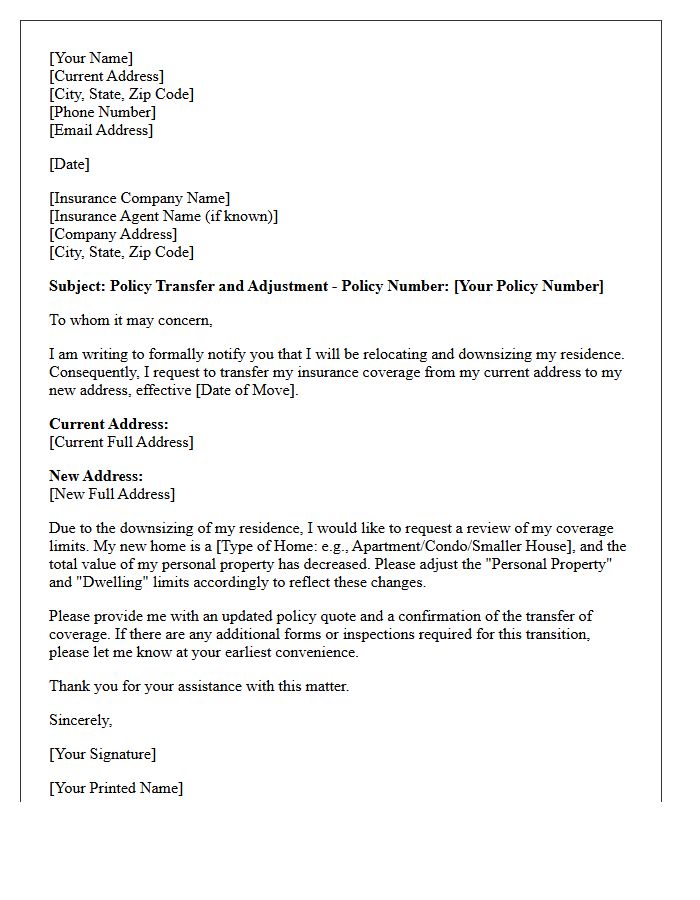

Relocation and Downsizing Insurance Policy Transfer Letter

A Relocation and Downsizing Insurance Policy Transfer Letter is a formal request to move existing coverage to a new residence. It ensures continuous protection for your belongings during a transition. You must notify your insurer of the change in address, property size, and security features to adjust premiums accurately. Providing detailed documentation of high-value items is essential for maintaining liability limits. Timely submission prevents coverage gaps, ensuring your personal property remains insured against loss or damage throughout the downsizing process and within your new smaller living space.

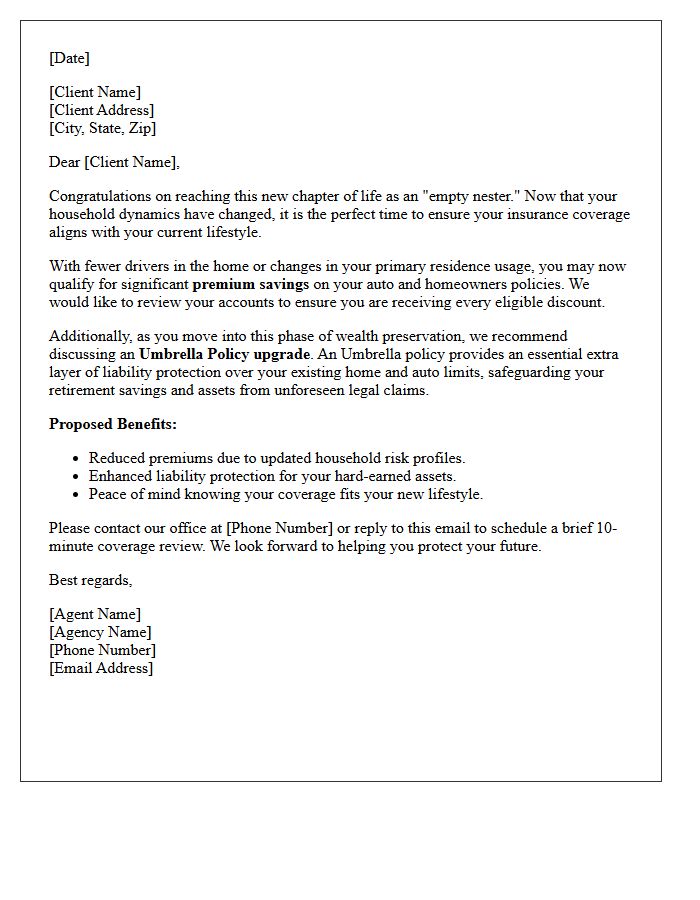

Empty Nester Premium Savings and Umbrella Upgrade Letter

An Empty Nester Premium Savings and Umbrella Upgrade Letter informs homeowners that lifestyle changes may qualify them for lower insurance rates. As children move out, reduced household activity often decreases liability risks, triggering potential discounts on primary policies. The letter encourages adding an Umbrella Policy, which provides essential excess liability coverage to protect your accumulated assets and retirement savings against unforeseen lawsuits. Reviewing these updates ensures your comprehensive financial protection aligns with your current life stage while maximizing cost efficiency through bundled savings and refined risk assessments.

1. Why should empty nesters consider an umbrella policy when downsizing?

Downsizing often involves significant changes in assets and lifestyle risks. An umbrella policy provides an essential layer of liability protection beyond standard homeowner and auto limits, safeguarding your retirement savings and remaining assets from unpredictable lawsuits or major accidents.

2. Does downsizing to a smaller home reduce the need for an umbrella policy?

Not necessarily. While a smaller home may mean less physical property to maintain, your personal net worth and retirement accounts remain vulnerable to legal claims. An umbrella policy ensures that even if your primary insurance is exhausted, your financial independence during your empty-nest years is not compromised.

3. How does an umbrella policy letter assist in the downsizing process?

An umbrella policy letter serves as formal documentation of your extended liability coverage. It provides peace of mind to financial planners and family members, confirming that your transition to a smaller residence includes a comprehensive risk management strategy to protect your legacy.

4. Are liability risks different for empty nesters living in condos or townhomes?

Yes. Many empty nesters downsize to properties with shared amenities or Homeowners Associations (HOAs). An umbrella policy can offer protection in complex liability situations, such as incidents occurring in common areas or guest injuries that exceed the limited liability coverage provided by a standard condo insurance policy.

5. Should I update my umbrella policy letter after selling my family home?

Absolutely. You should update your umbrella policy letter whenever you undergo a major life change like downsizing. This ensures your coverage limits reflect your current asset portfolio and that your new primary residence is correctly listed, maintaining seamless liability protection during your retirement years.

Comments