Protect your company's future by securing Key Person Life Insurance for startup founders. This essential coverage provides financial stability and reassures investors if a visionary leader passes away unexpectedly. It mitigates risk, covers recruitment costs, and ensures business continuity during critical transitions. Learn how to safeguard your venture's valuation today. Below are some ready to use templates.

Image cover: Securing Your Startup's Future: Key Person Life Insurance Templates and Samples for Founders

Letter Samples List

- Key Person Life Insurance Prospecting Letter

- Startup Founder Valuation Risk Assessment Letter

- Venture Capital Required Key Person Insurance Letter

- Co-Founder Business Continuity Protection Letter

- Key Person Life Insurance Policy Proposal Letter

- Board of Directors Key Person Compliance Letter

- Startup Executive Policy Issuance Approval Letter

- Key Person Insurance Annual Needs Review Letter

- Seed Funding Stage Key Person Insurance Letter

- Startup Founder Policy Grace Period Warning Letter

- Key Person Life Insurance Beneficiary Update Letter

- Insurance Agency Founder Protection Introduction Letter

- Series A Funding Policy Expansion Letter

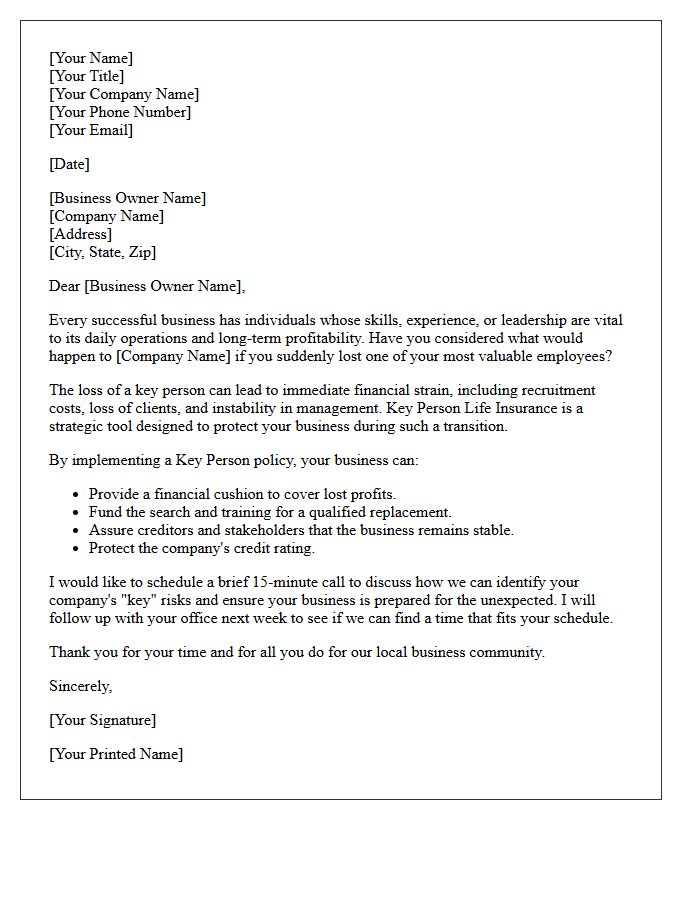

Key Person Life Insurance Prospecting Letter

A Key Person Life Insurance prospecting letter must focus on business continuity by highlighting the financial risks of losing a top executive. Clearly articulate how a sudden vacancy impacts profits, credit access, and stakeholder confidence. Use a professional tone to address the tax-advantaged benefits of the policy, such as funding executive search costs or stabilizing cash flow. Keep the message concise, emphasizing that protecting human capital is just as vital as insuring physical assets. End with a clear call to action to schedule a risk assessment consultation.

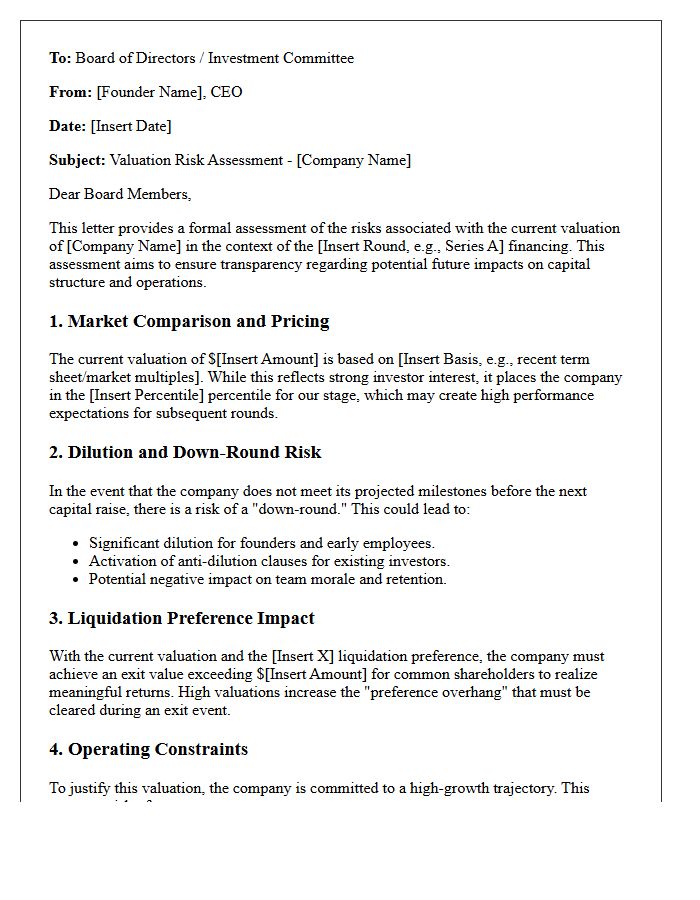

Startup Founder Valuation Risk Assessment Letter

A Startup Founder Valuation Risk Assessment Letter is a critical document used to justify equity pricing during early-stage funding. It identifies potential valuation volatility by analyzing market trends, burn rates, and intellectual property defensibility. This letter helps mitigate legal disputes and tax liabilities by providing a transparent framework for how a startup's worth was determined. For founders, it serves as a defensive tool to align investor expectations with realistic growth projections, ensuring that the financial risk associated with speculative assets is clearly disclosed and documented before finalizing investment rounds.

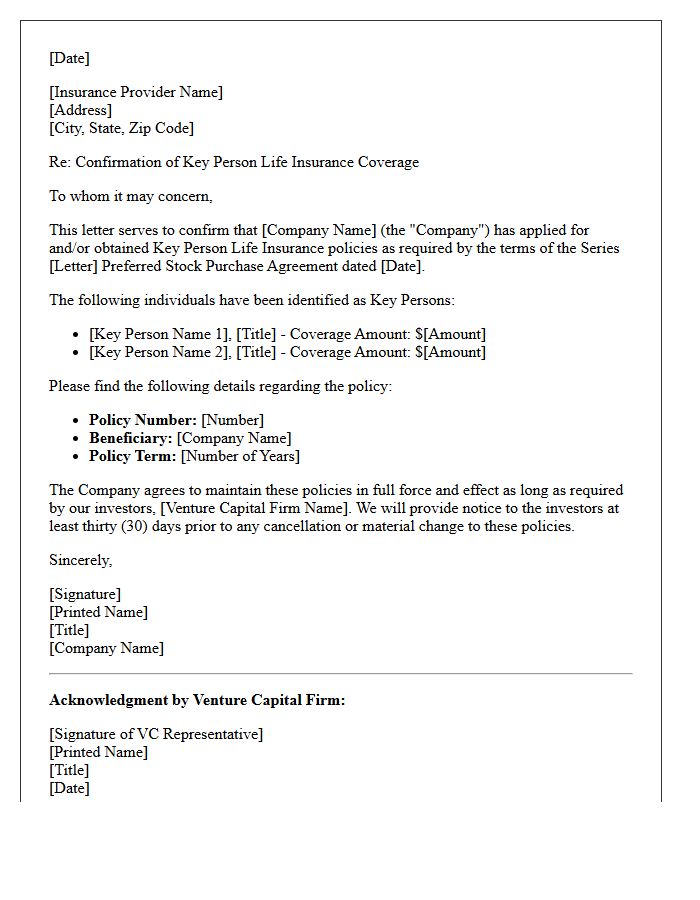

Venture Capital Required Key Person Insurance Letter

A Venture Capital Required Key Person Insurance Letter is a mandatory mandate often included in term sheets. It requires startups to secure life insurance for indispensable founders to protect the firm's investment. This policy ensures that if a critical leader passes away, the death benefit provides the company with vital liquidity to stabilize operations or find a replacement. Investors view this as a crucial risk mitigation strategy, ensuring the business survives the loss of its most valuable human capital during high-growth phases.

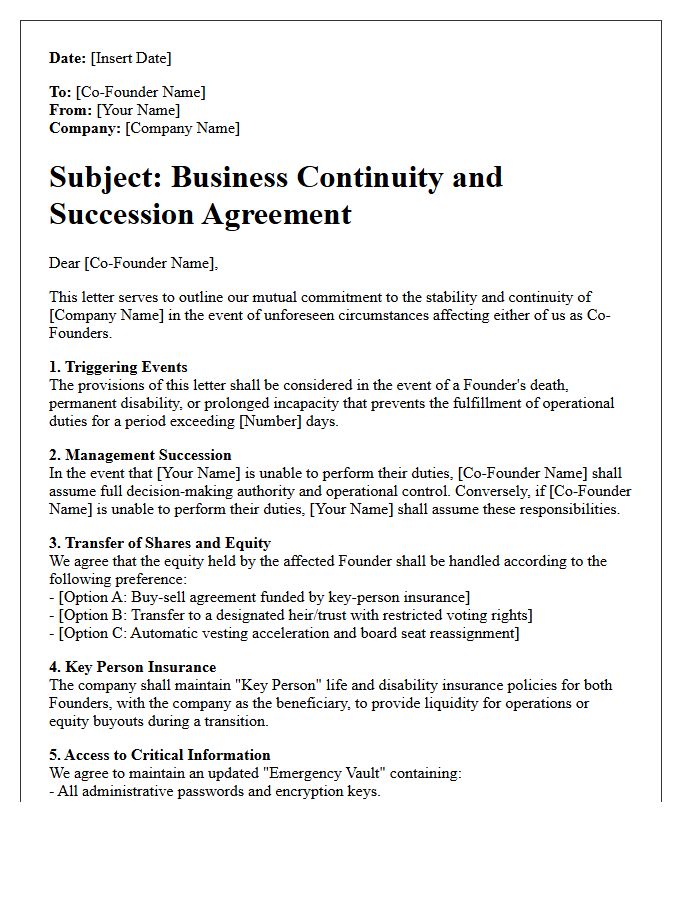

Co-Founder Business Continuity Protection Letter

A Co-Founder Business Continuity Protection Letter is a legal safeguard designed to ensure operational stability during unexpected departures. It outlines clear protocols for equity redistribution, decision-making authority, and intellectual property transfers if a partner leaves. By establishing these predefined terms, startups can mitigate internal disputes and provide investor confidence during leadership transitions. This document acts as a critical insurance policy, protecting the company's long-term viability and ensuring that the remaining founders maintain the necessary control to continue scaling the business without legal or administrative paralysis.

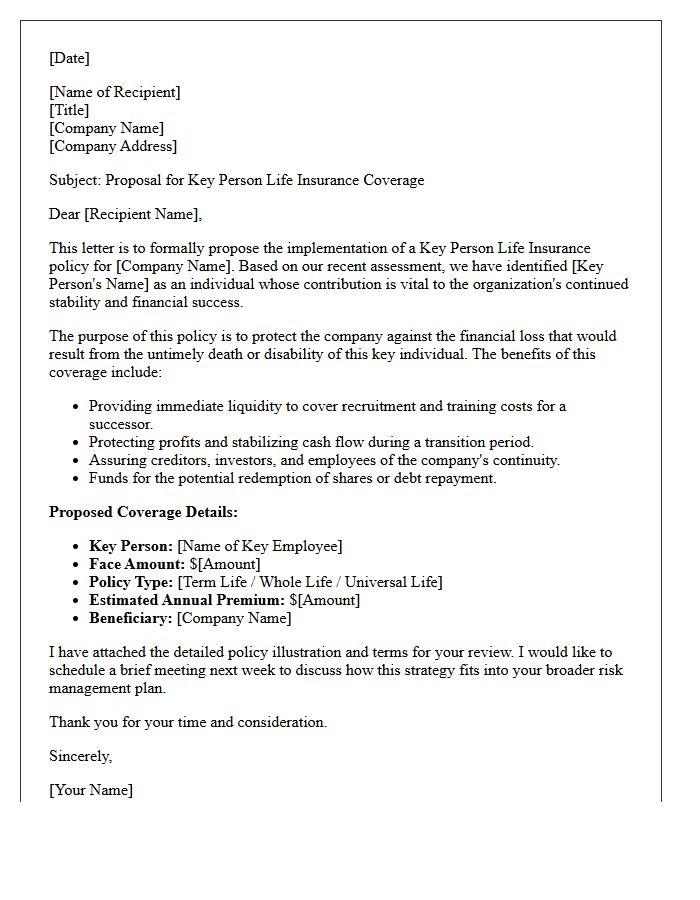

Key Person Life Insurance Policy Proposal Letter

A Key Person Life Insurance proposal letter is a formal document designed to protect a business against the financial loss of a vital employee. It outlines how the policy provides a contingency fund to cover recruitment costs, debt obligations, or revenue gaps during a transition. The proposal must clearly define the valuation of the individual's contribution and specify the premium structure. This strategic insurance ensures business continuity and maintains stakeholder confidence by safeguarding the company's financial stability against the unexpected loss of its most valuable human assets.

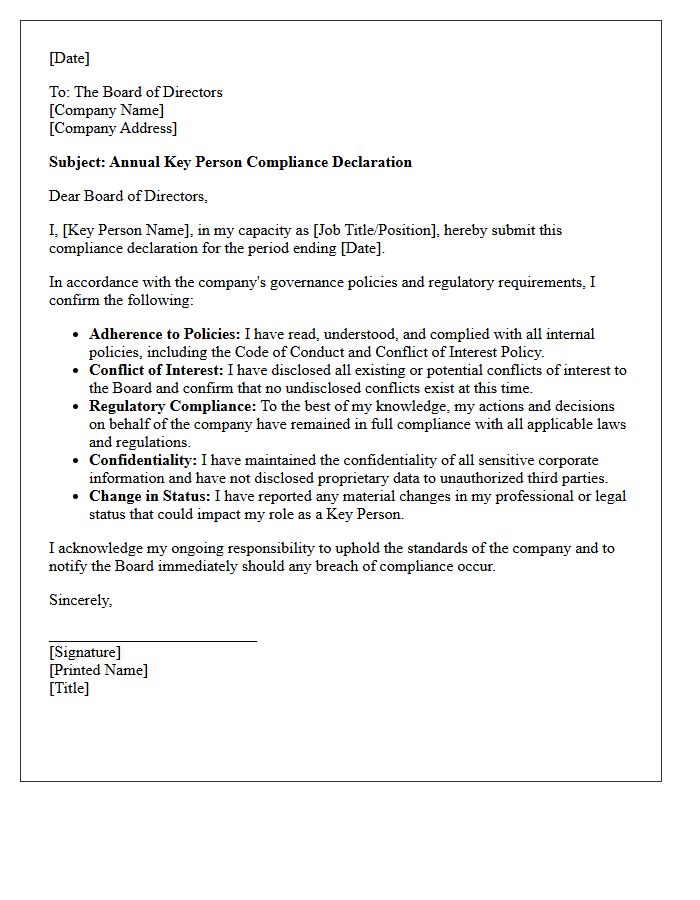

Board of Directors Key Person Compliance Letter

A Board of Directors Key Person Compliance Letter is a critical document used to verify that leadership members adhere to specific regulatory standards. It confirms that "Key Persons" undergo rigorous background checks and financial vetting to maintain institutional integrity. This certification is essential for corporate governance and licensing, ensuring that those in control meet mandatory legal and ethical requirements. By signing, directors acknowledge their fiduciary duties and disclose potential conflicts of interest, protecting the organization from legal liability and ensuring operational transparency within highly regulated industries.

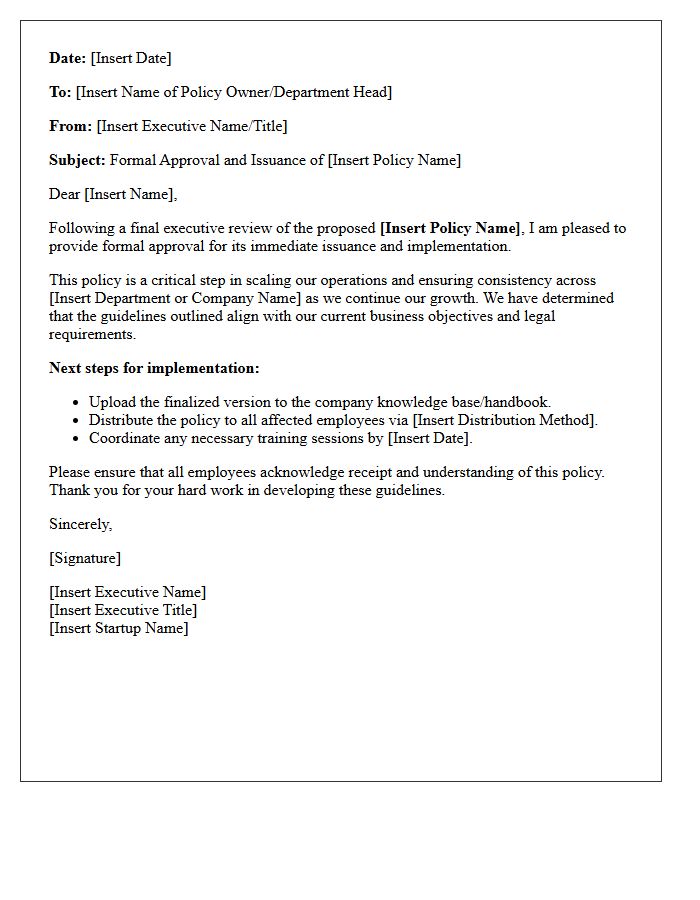

Startup Executive Policy Issuance Approval Letter

A Startup Executive Policy Issuance Approval Letter is a formal document authorizing the activation of insurance coverage for key leadership. It confirms that the underwriting process is complete and the premium has been accepted. For high-growth companies, this letter is essential to validate Key Person Insurance or D&O policies required by investors during funding rounds. It serves as official proof of protection, outlining the effective date and policy scope to ensure the executive and the startup are legally shielded against operational risks and unforeseen liabilities.

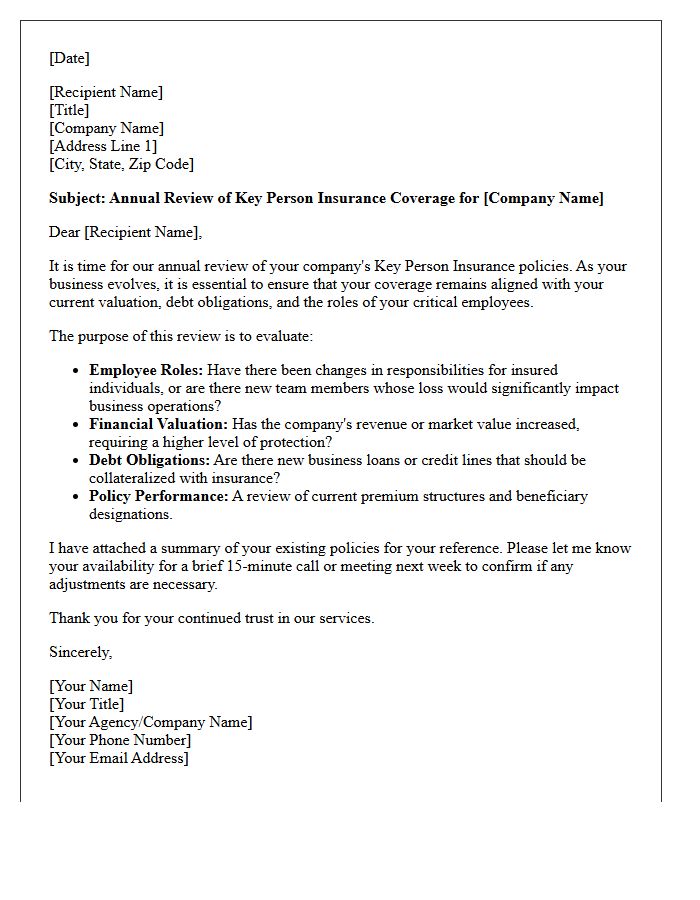

Key Person Insurance Annual Needs Review Letter

A Key Person Insurance Annual Needs Review Letter is a vital document used to assess if current coverage aligns with a company's evolving financial stability. Businesses must regularly evaluate the policy value to account for salary changes, new strategic roles, or increased debt obligations. This review ensures that the loss of a crucial executive does not result in operational failure or liquidity crises. Updating these terms annually protects business continuity and maintains stakeholder confidence by reflecting the actual market value of the individual's contributions to the organization.

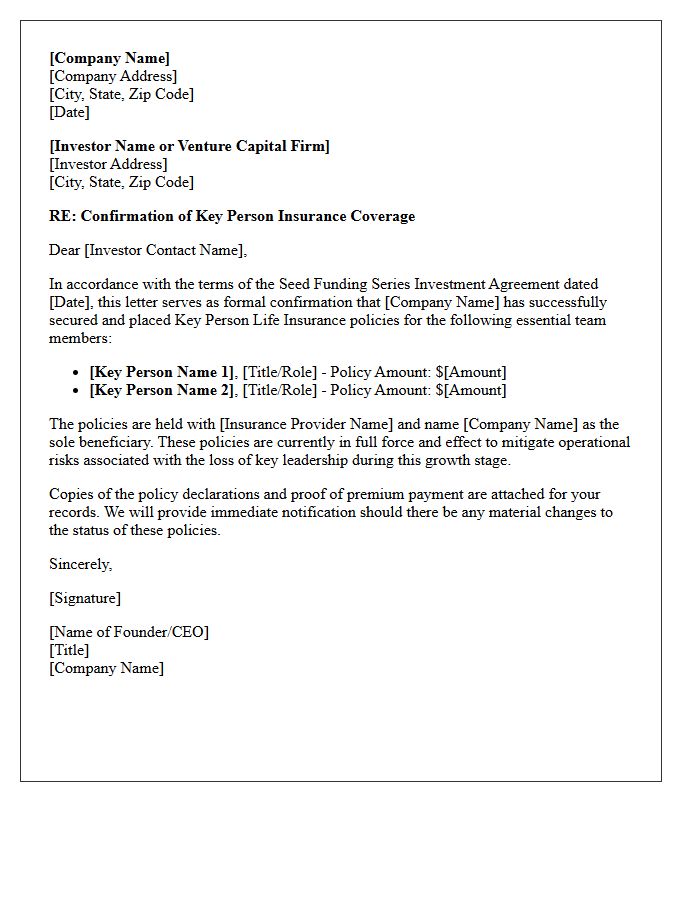

Seed Funding Stage Key Person Insurance Letter

A Seed Funding Stage Key Person Insurance Letter is a critical document often required by venture capitalists during early investment rounds. It confirms the startup has secured life or disability coverage for foundational founders whose expertise is essential to the company's survival. This letter mitigates risk for investors by ensuring financial liquidity and business continuity should a visionary leader become incapacitated. Providing this assurance demonstrates professional maturity, protects the startup's valuation, and fulfills a common pre-closing condition necessary to finalize seed-stage capital injections and safeguard future growth operations.

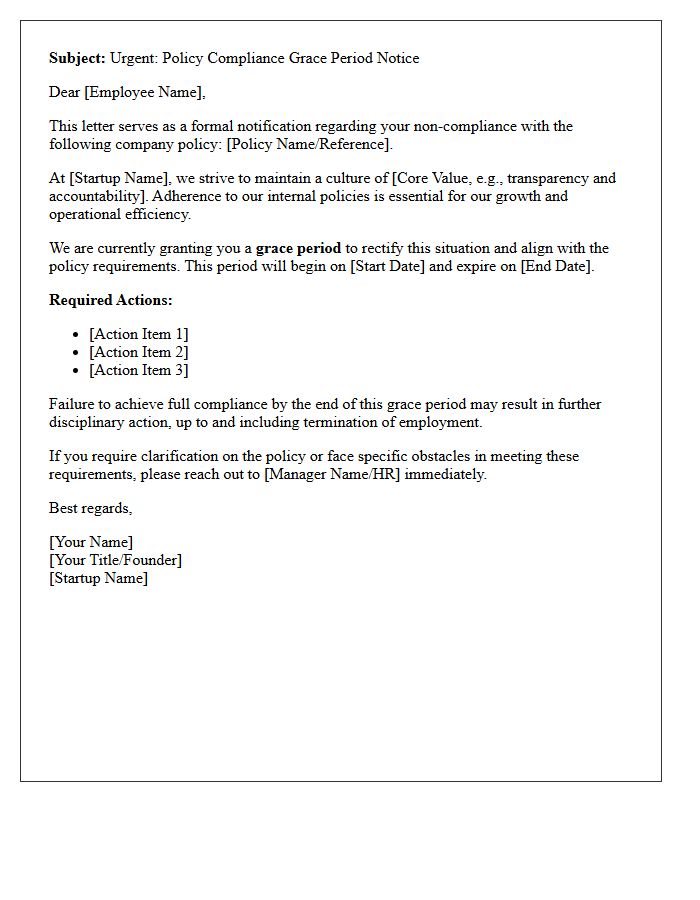

Startup Founder Policy Grace Period Warning Letter

A Startup Founder Policy Grace Period Warning Letter serves as a formal notification that a founder has breached internal governance or compliance protocols. This document outlines the specific violation and provides a defined timeframe to rectify the issue before facing penalties. It is a critical tool for maintaining accountability and protecting the company's legal standing. Founders must treat this period as a final opportunity to align with shareholder agreements or operational standards, as failure to comply may result in loss of equity vesting or removal from leadership positions.

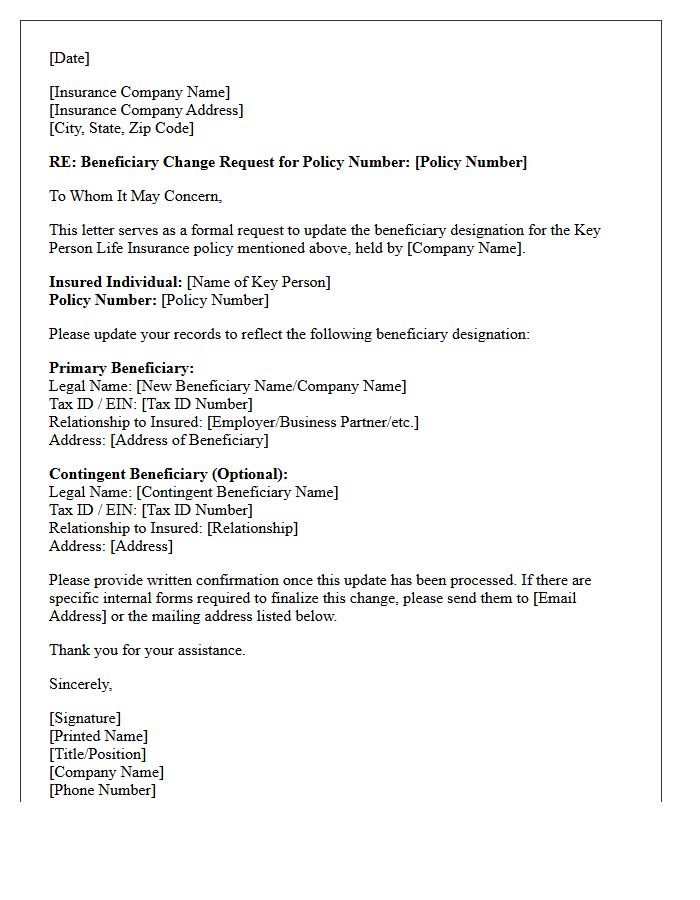

Key Person Life Insurance Beneficiary Update Letter

A Key Person Life Insurance Beneficiary Update Letter is a formal document used to notify an insurer of changes to the designated recipient of policy proceeds. This update is critical when a company experiences structural shifts, such as mergers, acquisitions, or leadership transitions. Ensuring the beneficiary information remains current prevents legal disputes and financial delays during a claim. The letter must include the policy number, the new beneficiary's legal name, and tax identification details to maintain business continuity and ensure the organization receives the intended financial protection after the loss of a vital employee.

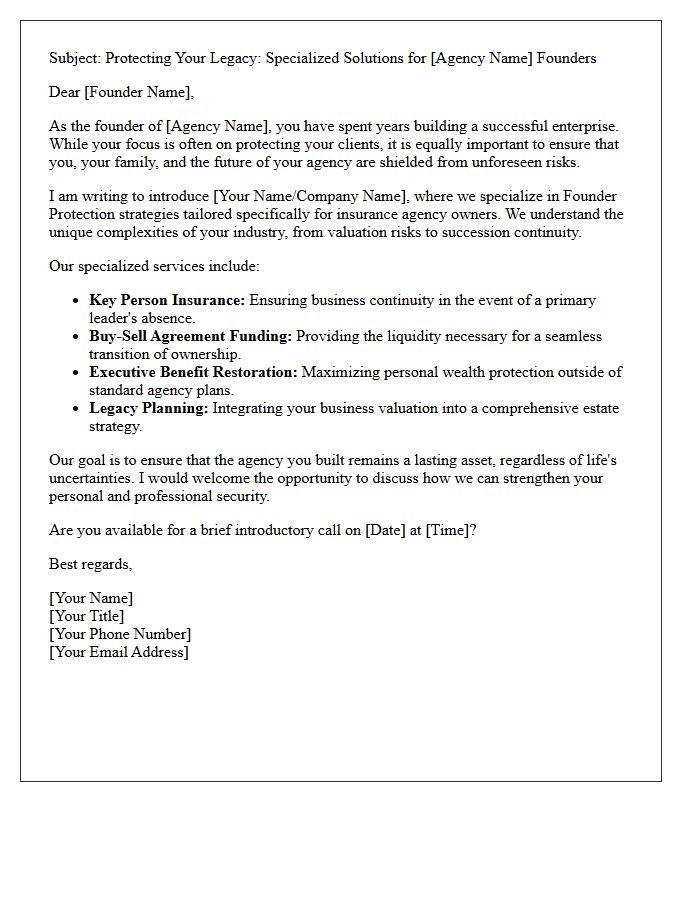

Insurance Agency Founder Protection Introduction Letter

An Insurance Agency Founder Protection Introduction Letter is a strategic document designed to secure a founder's legacy and business continuity during ownership transitions. This professional outreach informs carriers and clients of leadership changes while emphasizing risk mitigation and operational stability. By outlining succession plans and protective clauses, the letter builds immediate trust with stakeholders. It serves as a vital tool for maintaining contractual integrity, preventing client attrition, and ensuring that the agency's core values remain intact during sensitive periods of structural evolution or potential acquisition.

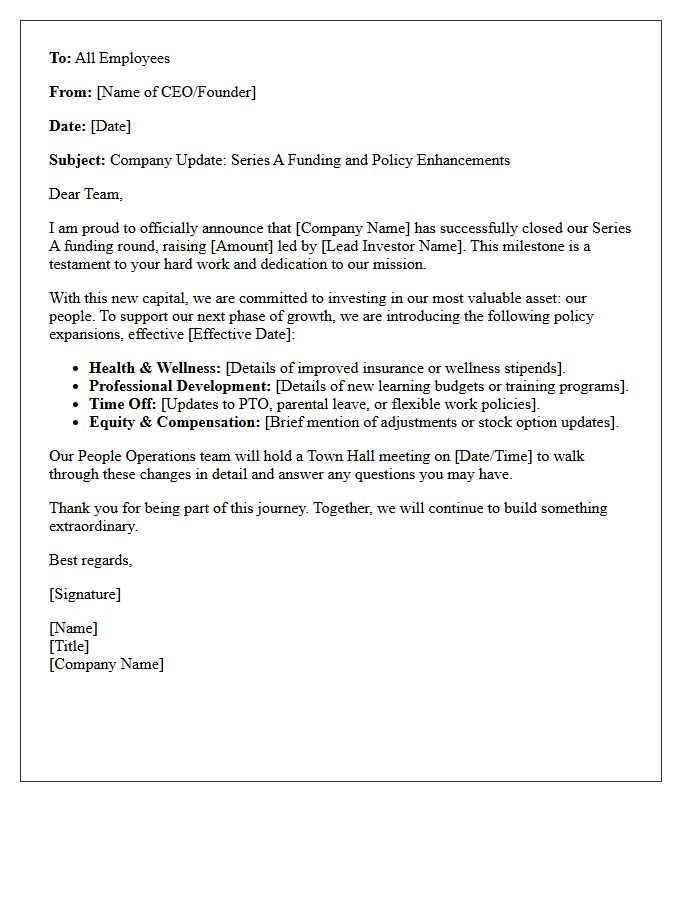

Series A Funding Policy Expansion Letter

A Series A Funding Policy Expansion Letter is a formal document used to notify stakeholders about updated operational guidelines following a primary institutional investment round. It outlines how new capital influences governance, spending limits, and hiring protocols. This letter ensures transparency between founders and investors, aligning the company's growth strategy with its fiduciary duties. Understanding these policy shifts is essential for maintaining compliance and scaling effectively while protecting the interests of newly onboarded venture capitalists and the original founding team during the transition to a high-growth phase.

What is Key Person Life Insurance for startup founders?

Key Person Life Insurance is a life insurance policy taken out by a startup on the life of a critical founder or executive. The company pays the premiums and is the designated beneficiary, providing a financial safety net to stabilize operations, reassure investors, and cover recruitment costs if the founder passes away.

Why do venture capitalists require Key Person Life Insurance?

VCs often mandate Key Person Life Insurance as a condition for funding to mitigate "key person risk." It ensures that the startup has the immediate liquidity necessary to pivot, hire a replacement, or manage an orderly liquidation, thereby protecting the investors' capital in the event of a founder's death.

How much coverage is typically required for a startup founder?

The coverage amount is usually determined by the startup's valuation, the size of the investment round, or the founder's replacement cost. Common policy values range from $1 million to $5 million, or an amount equal to the total investment of the lead VC in the current round.

Is Key Person Life Insurance tax-deductible for the startup?

Generally, premiums paid by a startup for Key Person Life Insurance are not tax-deductible as a business expense. However, the death benefit payout is typically received by the company tax-free, providing the full face value of the policy to support business continuity.

What happens to the policy if the founder leaves the startup?

If a founder leaves the company, the startup has several options: they can let the policy lapse, surrender it for its cash value (if applicable), or transfer ownership to the founder as part of a severance package. In some cases, the policy may be converted to personal coverage by the departing individual.

Comments