Dealing with old collections requires caution, as a payment could restart the statute of limitations. A Time-Barred Debt Settlement Offer Letter allows you to resolve expired obligations for pennies on the dollar without unintentionally reviving your legal liability. Protect your rights while clearing your credit history effectively. To help you get started, below are some ready to use template.

Image cover: Proven Templates and Samples for Settling Expired Time-Barred Debts

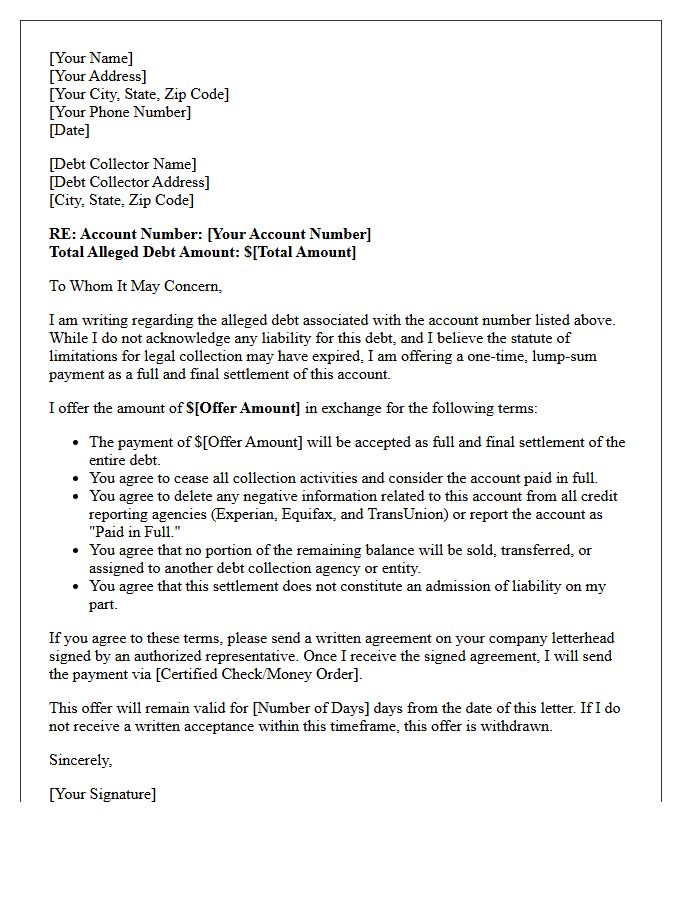

Letter Samples List

- Time-Barred Debt Settlement Offer Letter

- Expired Statute Of Limitations Debt Settlement Letter

- Out Of Statute Account Discounted Settlement Letter

- Mutual Release And Time-Barred Debt Resolution Letter

- Pre-Litigation Time-Barred Obligation Settlement Letter

- Final Compromise On Time-Barred Debt Offer Letter

- Time-Barred Debt Nuisance Value Settlement Letter

- Expired Debt Amnesty And Settlement Offer Letter

- Legal Resolution For Time-Barred Account Letter

- Zombie Debt Full And Final Settlement Letter

- Time-Barred Collection Resolution Offer Letter

- Unenforceable Debt Voluntary Settlement Letter

- Statute-Barred Liability Settlement Agreement Letter

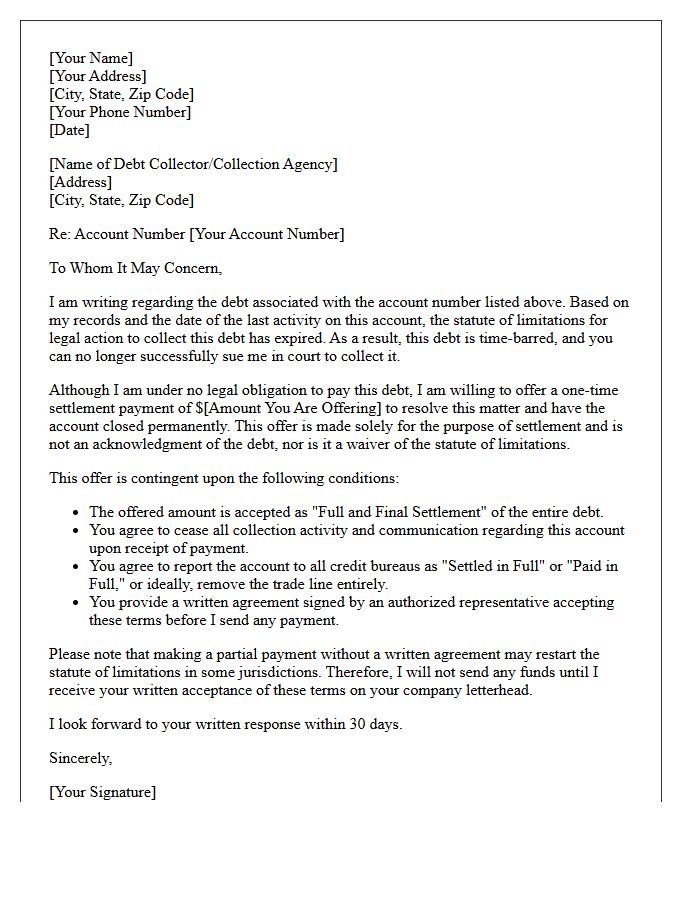

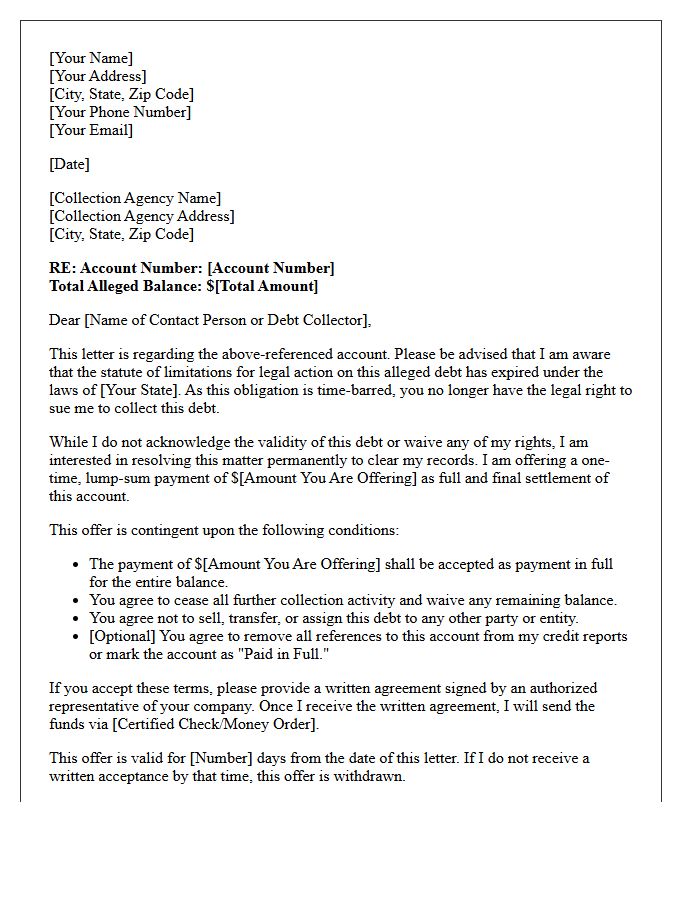

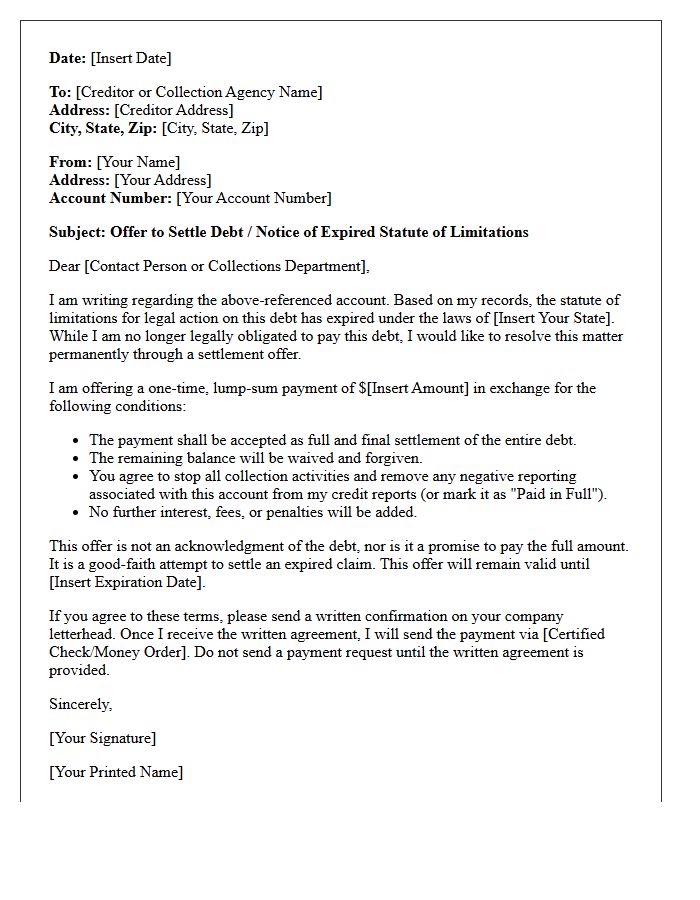

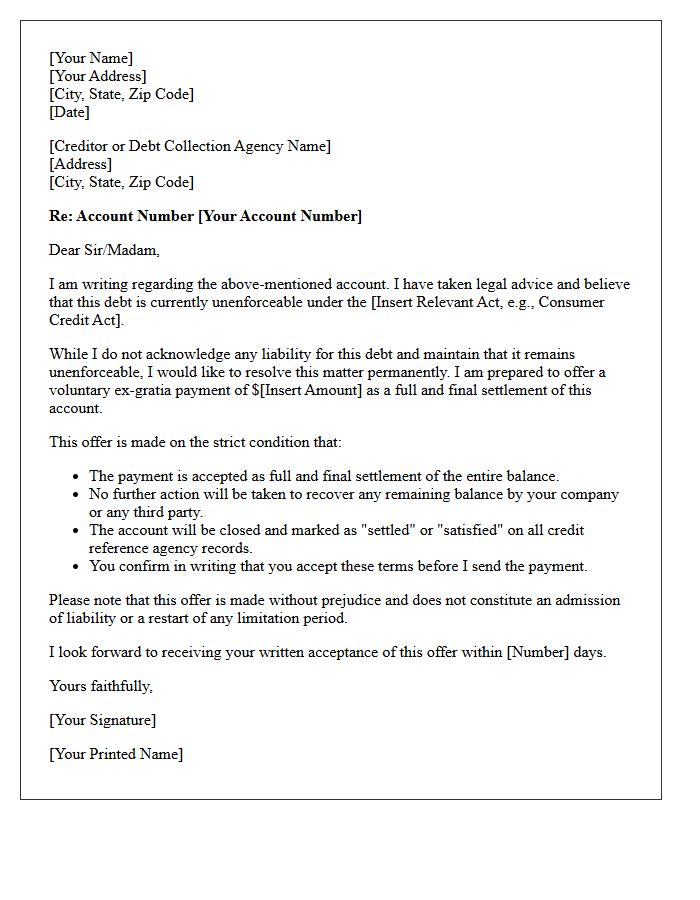

Time-Barred Debt Settlement Offer Letter

Receiving a Time-Barred Debt Settlement Offer Letter means a creditor is attempting to collect on an account past the statute of limitations. While you no longer have a legal obligation to pay, acknowledging the debt or making a partial payment can inadvertently restart the clock on your liability. Always verify the debt's age before responding. If you choose to settle, ensure the agreement is in writing and explicitly states that the payment extinguishes the debt entirely without reviving legal claims or damaging your credit further.

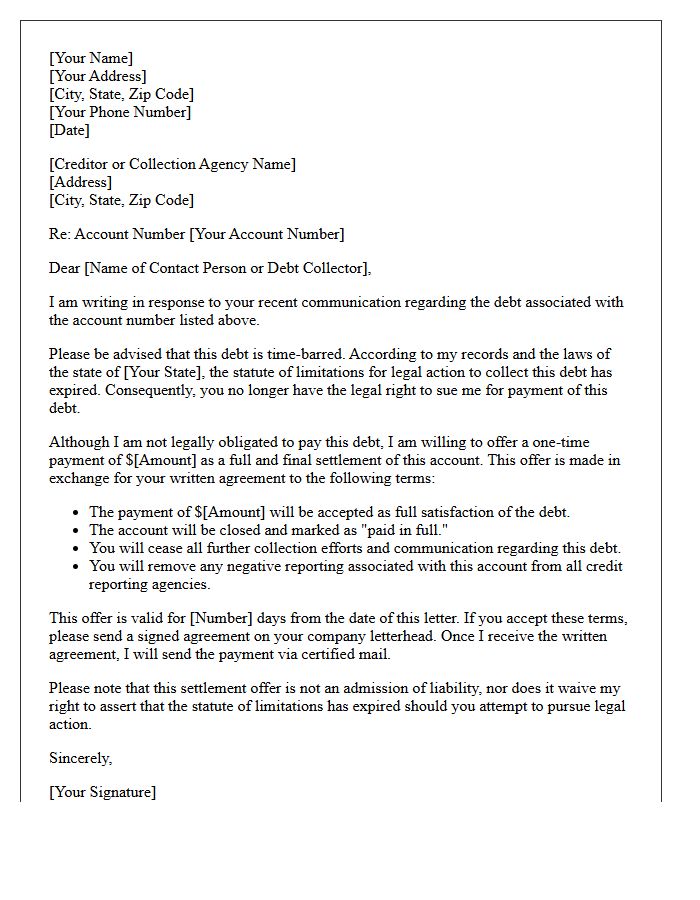

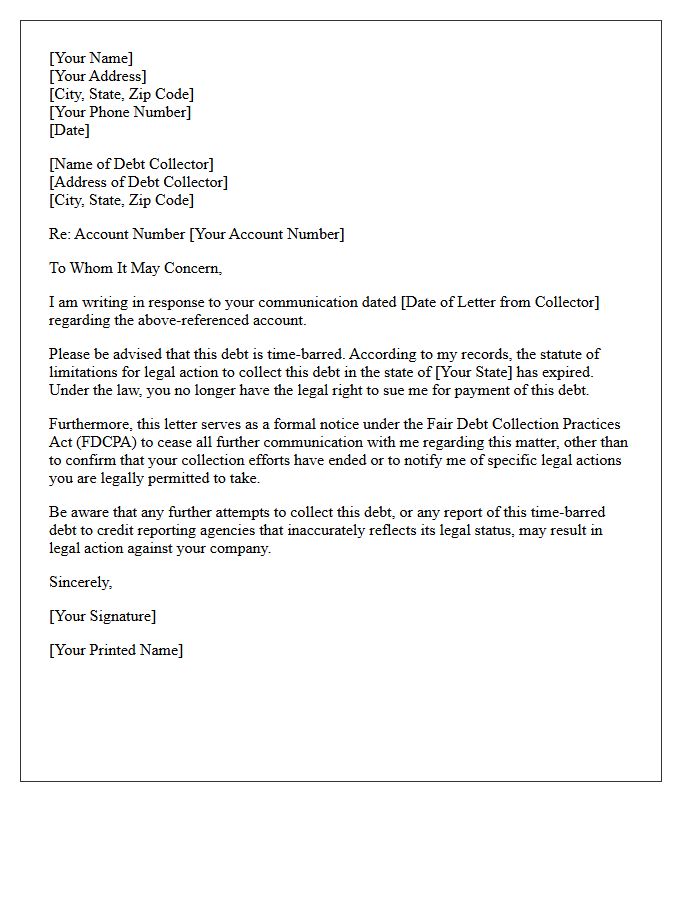

Expired Statute Of Limitations Debt Settlement Letter

An Expired Statute of Limitations Debt Settlement Letter is a formal notice sent to collectors stating that a debt is legally time-barred. Once this legal limit passes, creditors lose the right to sue for payment. Before sending, verify your state's specific timeline to ensure the debt is truly expired. Avoid making partial payments or acknowledging ownership, as this can restart the clock. Use this letter to demand that the agency cease all communication and stop further collection attempts on the unenforceable debt.

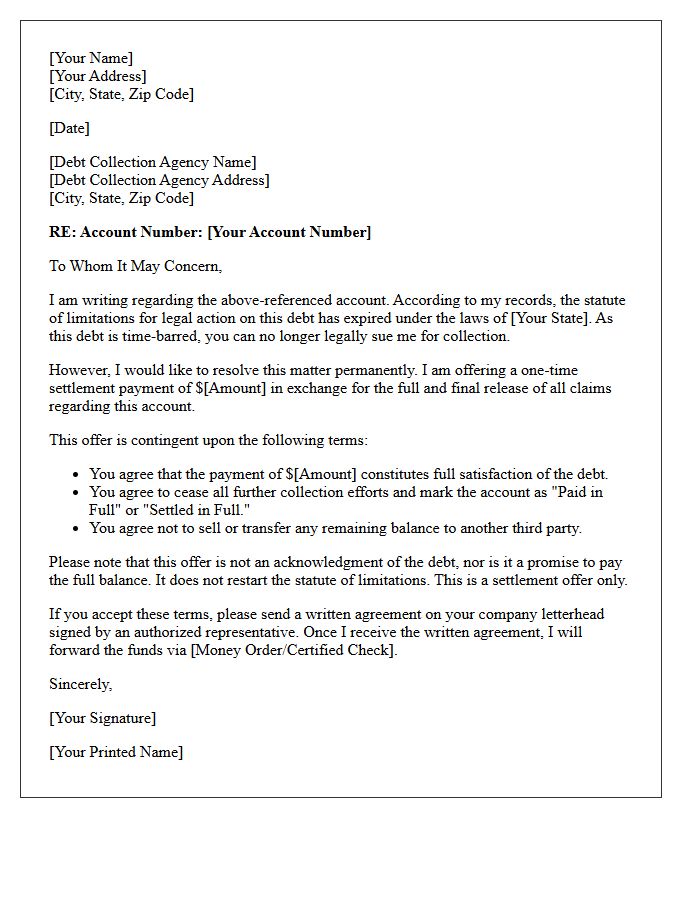

Out Of Statute Account Discounted Settlement Letter

An Out of Statute Account Discounted Settlement Letter is a formal offer to resolve a debt that has passed the legal collection timeframe. Since the creditor can no longer successfully sue for payment, they often accept significantly lower amounts. It is crucial to remember that making a partial payment or acknowledging the debt in writing can sometimes restart the clock on the statute of limitations. Always verify the debt's age and your local laws before responding to ensure you do not inadvertently waive your legal protections against expired claims.

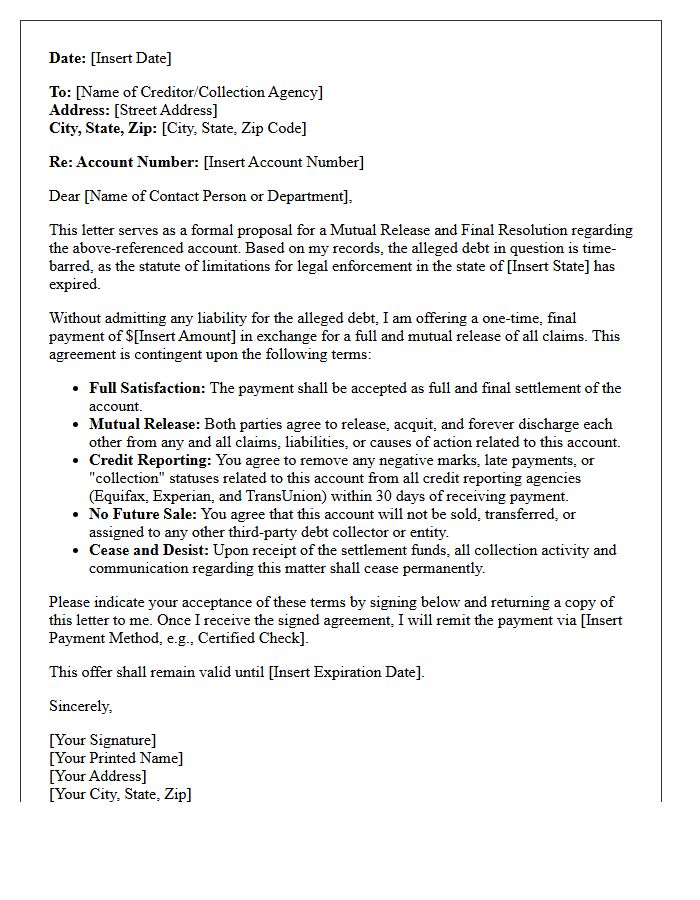

Mutual Release And Time-Barred Debt Resolution Letter

A Mutual Release and Time-Barred Debt Resolution Letter is a legal document used to settle expired debts that are past the statute of limitations. This agreement ensures that both the creditor and debtor waive future claims, effectively closing the account permanently. By signing, the creditor agrees not to pursue further legal action, while the debtor avoids zombie debt harassment. It is essential for protecting your credit score and financial peace of mind by securing a written confirmation that the obligation is legally satisfied and no longer enforceable in court.

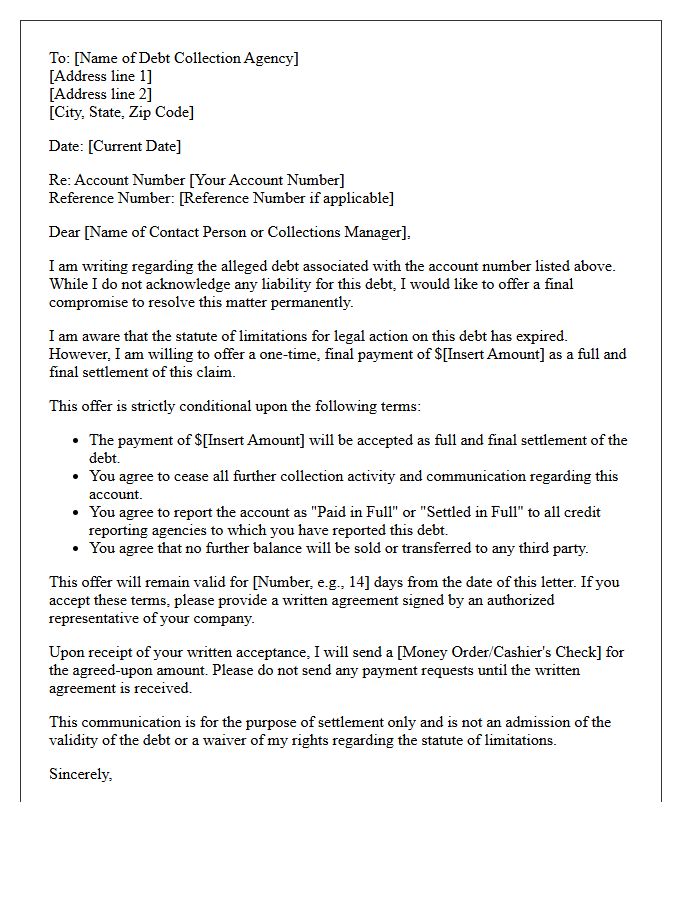

Pre-Litigation Time-Barred Obligation Settlement Letter

A Pre-Litigation Time-Barred Obligation Settlement Letter addresses a debt that has exceeded the legal statute of limitations for judicial enforcement. While creditors may still request payment, they cannot successfully sue you to recover the funds. This document often proposes a voluntary settlement to resolve the account and stop collection efforts. It is crucial to avoid making a partial payment or acknowledging the debt in writing before signing, as doing so may restart the limitations clock, effectively reviving the creditor's right to pursue legal action against you.

Final Compromise On Time-Barred Debt Offer Letter

The final compromise on a time-barred debt offer letter represents a formal agreement to settle an outstanding balance that has surpassed the statute of limitations. While creditors can no longer legally sue for payment, making a partial payment or acknowledging the debt in writing can inadvertently restart the clock on the legal timeframe. Consumers must ensure the letter clearly states that the payment serves as a full and final settlement. Reviewing these offers carefully is essential to resolve old obligations without unintentionally reviving expired legal liabilities or damaging credit scores further.

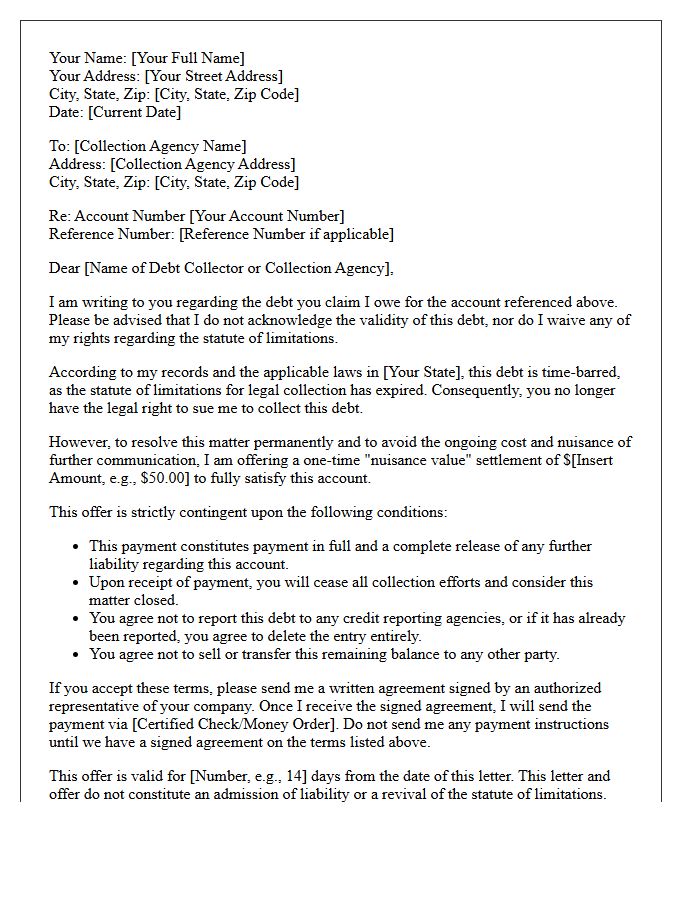

Time-Barred Debt Nuisance Value Settlement Letter

A Time-Barred Debt Nuisance Value Settlement Letter is a strategic legal tool used when a debt exceeds the statute of limitations. Since creditors can no longer legally sue for payment, the debt carries low financial weight. This letter offers a small, one-time "nuisance" payment to permanently close the account and stop collection harassment. It must explicitly state that the payment does not revive the expired limitation period. Sending this document helps clear your credit history and prevents junk debt buyers from repeatedly selling your expired obligations to other agencies.

Expired Debt Amnesty And Settlement Offer Letter

An Expired Debt Amnesty offer occurs when a creditor proposes settling a time-barred debt for a fraction of the total balance. It is crucial to understand that Statute of Limitations laws vary by state; once a debt expires, you are no longer legally obligated to pay. However, making a partial payment or acknowledging the debt in writing can reset the clock, reviving the creditor's right to sue. Always verify the debt's age and consult local consumer protection laws before responding to ensure you do not inadvertently reactivate an unenforceable financial obligation.

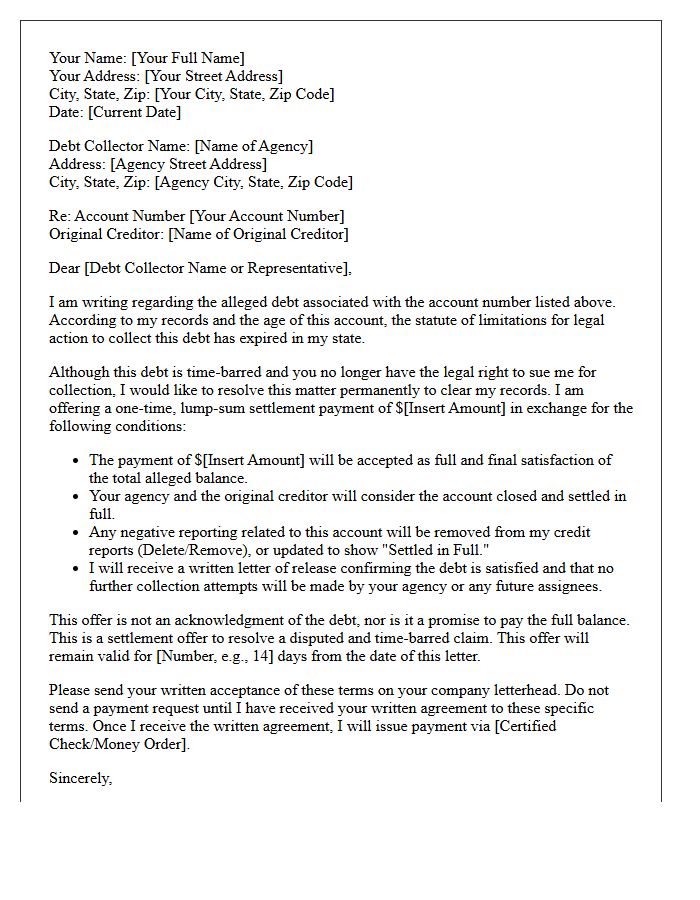

Legal Resolution For Time-Barred Account Letter

A legal resolution for a time-barred account letter serves as formal notice that a debt is legally uncollectible due to the expired statute of limitations. This written response informs collectors they can no longer sue for payment. It is vital to avoid making a partial payment or acknowledging ownership of the debt within the letter, as doing so can inadvertently restart the clock on the legal timeframe. Use this document to demand a cessation of all collection activities and to protect your consumer rights under federal law.

Zombie Debt Full And Final Settlement Letter

A Zombie Debt Full and Final Settlement Letter is a critical legal tool used to resolve old, expired, or unverified debts often resurrected by collection agencies. Before sending this written offer, ensure the debt is legitimate and verify the Statute of Limitations in your jurisdiction. A successful settlement must explicitly state that the payment serves as full satisfaction of the account, preventing future collections. Always send via certified mail and demand a written acceptance before transferring funds to protect your credit report and legal rights permanently.

Time-Barred Collection Resolution Offer Letter

A Time-Barred Collection Resolution Offer Letter informs you that a debt is legally unenforceable due to the expired statute of limitations. While creditors can no longer sue you for payment, they may still attempt to settle for a lower amount. It is critical to understand that making a partial payment or acknowledging the debt in writing can restart the limitations clock, reviving the collector's right to sue. Always verify your state's legal timeframes and review your consumer rights under the FDCPA before responding to such settlement offers.

Unenforceable Debt Voluntary Settlement Letter

An Unenforceable Debt Voluntary Settlement Letter is a strategic formal notice used when a creditor cannot legally compel repayment, often due to statute-barred limitations or lack of original credit agreements. Even if a debt is legally unenforceable, it still exists and may affect credit scores. This letter offers a reduced, one-time payment to close the account permanently. It is crucial to state that the payment is made without admitting liability, ensuring the creditor accepts the full and final settlement in writing to prevent future collection attempts or legal harassment.

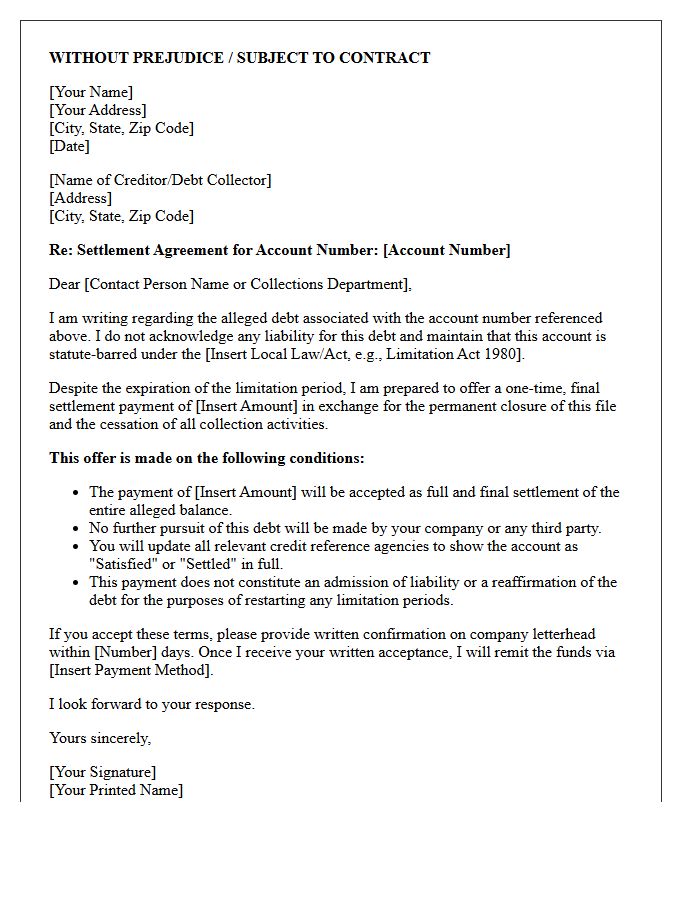

Statute-Barred Liability Settlement Agreement Letter

A Statute-Barred Liability Settlement Agreement Letter is a formal document used to resolve debts that have passed the legal limitation period. Since creditors can no longer sue for payment, this letter proposes a final, often reduced, sum to close the account permanently. It is crucial to use specific language to ensure the payment is accepted as full satisfaction without unintentionally acknowledging the debt in a way that restarts the clock. Once signed, it provides legal protection against further collection efforts and formalizes the debt's unenforceable status.

What is a time-barred debt settlement offer letter?

A time-barred debt settlement offer letter is a formal written proposal sent by a debtor to a creditor or collection agency to resolve a debt that has passed the legal statute of limitations for lawsuits. This letter typically offers a lump-sum payment or structured plan to clear the record without acknowledging the debt in a way that restarts the clock.

Does offering a settlement on time-barred debt restart the statute of limitations?

In many jurisdictions, making a partial payment or a written promise to pay can "toll" or restart the statute of limitations, making the debt legally enforceable again. When sending a settlement offer for time-barred debt, it is crucial to include a disclaimer stating that the offer is not an admission of the debt's validity or a waiver of your rights regarding the statute of limitations.

Should I pay a collection agency for debt that is past the statute of limitations?

Deciding to pay time-barred debt depends on your financial goals. While you cannot be sued for the debt, it may still appear on your credit report or result in persistent collection calls. A settlement offer letter can help stop collections and potentially improve your credit score, provided you receive a "paid in full" or "settled in full" agreement in writing.

What should be included in a time-barred debt settlement proposal?

A legally sound settlement letter should include the account number, the proposed settlement amount, a request for a "letter of release" upon payment, and a specific statement that the debt is time-barred. It should also stipulate that the payment is contingent upon the creditor reporting the account as "settled" to credit bureaus and ceasing all future collection efforts.

Can a creditor sue me after I send a settlement offer for old debt?

If the debt is truly time-barred, a creditor generally cannot win a lawsuit against you. However, some collectors may still attempt to file a suit. Sending a settlement offer does not give them the right to sue unless the language in your letter inadvertently reaffirms the debt or you make a payment that resets the legal clock. Always consult local state laws before sending a formal offer.

Comments