When an insurance provider fails to accept a reasonable settlement offer within policy limits, they may be liable for Insurance Bad Faith. Our guide explores how a formal demand letter protects your rights and establishes a record of insurer negligence to maximize recovery. To help you draft your own legal notice, below are some ready to use template.

Image cover: Winning Your Bad Faith Claim: Essential Failure to Settle Demand Letter Templates and Strategic Samples

Letter Samples List

- Initial Policy Limit Demand Letter

- Notice of Insurance Bad Faith Failure to Settle Letter

- Third-Party Bad Faith Failure to Settle Demand Letter

- First-Party Bad Faith Failure to Settle Demand Letter

- Time-Sensitive Bad Faith Demand to Settle Letter

- Excess Judgment Bad Faith Liability Demand Letter

- Breach of Implied Covenant and Bad Faith Letter

- Unreasonable Delay and Failure to Settle Demand Letter

- Demand Letter for Extracontractual Damages and Bad Faith

- Final Warning of Bad Faith Failure to Settle Letter

- Statutory Bad Faith Failure to Settle Notice Letter

- Pre-Litigation Bad Faith Failure to Settle Demand Letter

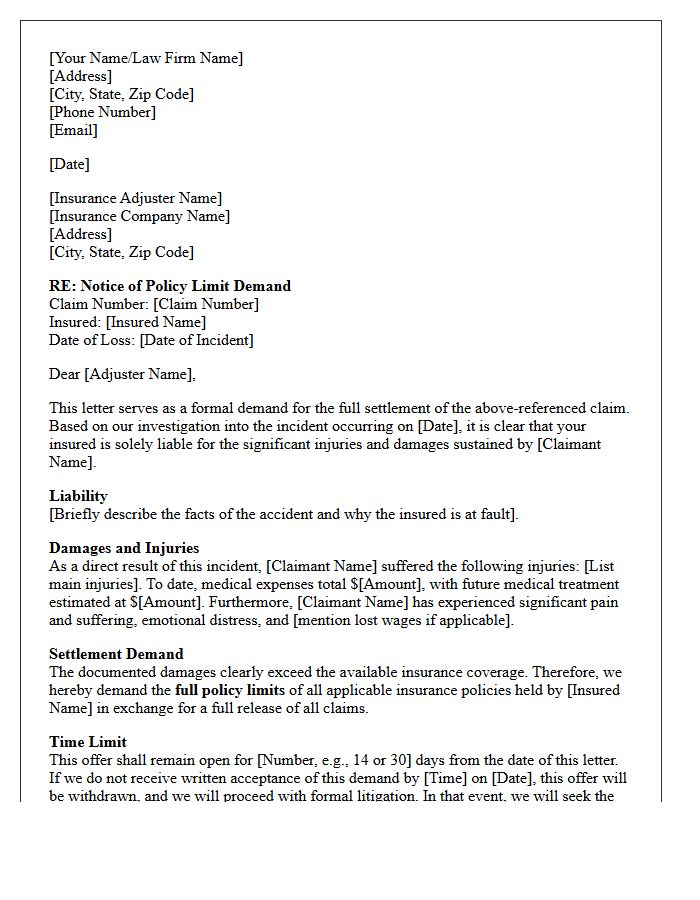

Initial Policy Limit Demand Letter

An Initial Policy Limit Demand Letter is a formal legal document sent to an insurance provider, requesting the full coverage amount to settle a claim. This letter is crucial for establishing bad faith potential if the insurer rejects a reasonable settlement. It must clearly outline liability, detail the extent of injuries, and provide a strict deadline for acceptance. By documenting that damages exceed the policy cap, the claimant creates legal leverage to hold the insurer accountable for the entire judgment, even if it eventually surpasses the original coverage limits.

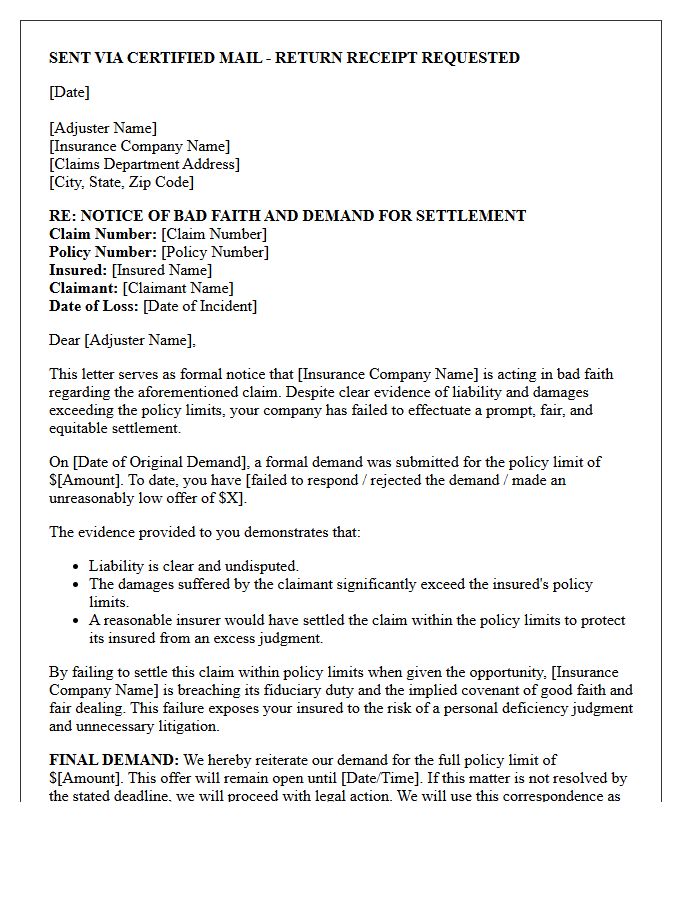

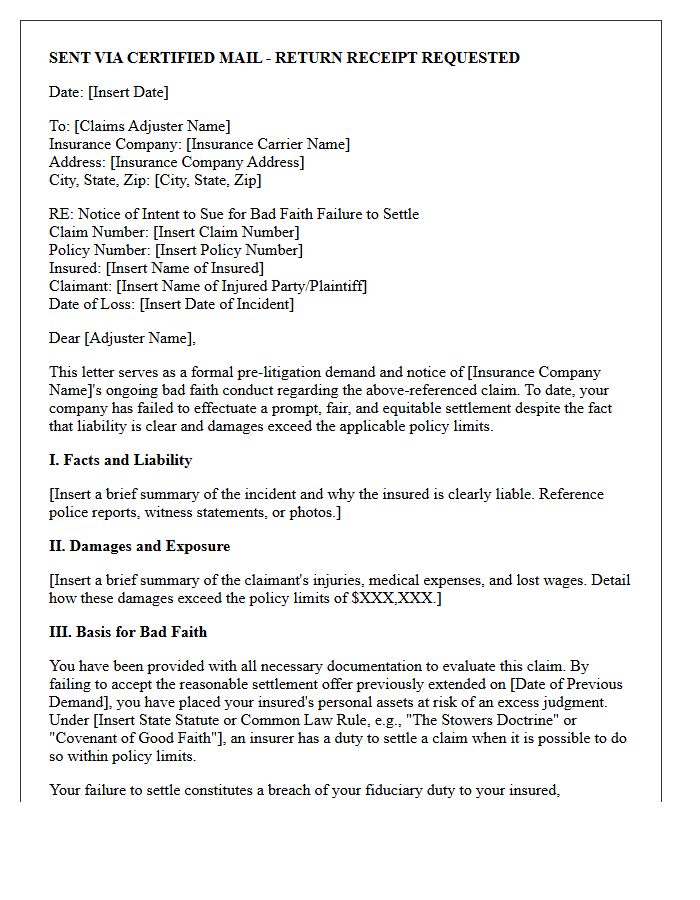

Notice of Insurance Bad Faith Failure to Settle Letter

A Notice of Insurance Bad Faith Failure to Settle Letter is a critical legal document sent to an insurer when they refuse a reasonable settlement offer within policy limits. This formal notice alerts the carrier that their delay or denial may constitute a breach of duty. By documenting the insurer's unreasonable conduct, you create a necessary foundation for a future bad faith lawsuit. It serves to hold the company accountable for exposing their insured to excess personal liability and ensures a record of their failure to act in good faith.

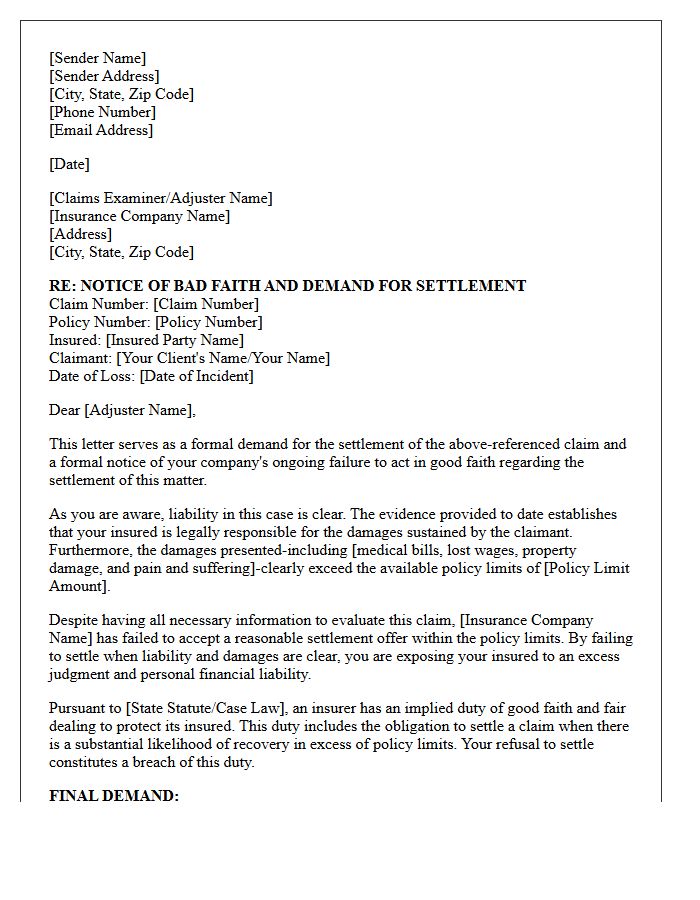

Third-Party Bad Faith Failure to Settle Demand Letter

A third-party bad faith claim arises when an insurance provider fails to accept a reasonable settlement offer within policy limits. The demand letter serves as a formal notice, establishing a clear deadline for the insurer to resolve the liability claim. By documented refusal to settle, the insurer may be held liable for the entire court judgment, even if it exceeds the original coverage. Proving wrongful denial or gross negligence is essential to hold companies accountable for prioritizing profits over their duty to protect the insured from financial ruin.

First-Party Bad Faith Failure to Settle Demand Letter

A First-Party Bad Faith Failure to Settle Demand Letter is a formal legal notice sent to an insurer when they unreasonably refuse to pay a valid claim. It establishes a paper trail of the company's breach of the implied covenant of good faith and fair dealing. This document provides clear evidence of the insurer's valuation errors or investigative failures. By detailing specific policy violations and demanding prompt resolution, the letter creates necessary leverage for potential litigation or statutory penalties if the insurer continues to act in bad faith against their own policyholder.

Time-Sensitive Bad Faith Demand to Settle Letter

A Time-Sensitive Bad Faith Demand to Settle is a strategic legal tool used by plaintiffs to pressure insurance companies into resolving a claim within a specific deadline. If the insurer fails to accept a reasonable settlement offer within the timeframe, they risk being held liable for the full court judgment, even if it exceeds the policy limits. This maneuver creates a foundation for a bad faith lawsuit by demonstrating that the insurer prioritized their financial interests over their duty to protect the policyholder from excessive personal financial exposure.

Excess Judgment Bad Faith Liability Demand Letter

An Excess Judgment Bad Faith Liability Demand Letter is a critical legal notice sent to an insurance company when they fail to settle a claim within policy limits. This document asserts that the insurer breached its duty to protect the insured, potentially exposing them to personal financial ruin. By formally documenting a reasonable settlement opportunity, the letter lays the groundwork for a bad faith lawsuit. If the insurer refuses and a court awards an amount exceeding the coverage, the company may be held liable for the full excess judgment regardless of policy caps.

Breach of Implied Covenant and Bad Faith Letter

A Breach of Implied Covenant and Bad Faith Letter is a formal legal notice asserting that an insurance company or contracting party failed to act with honesty and fairness. This document alleges that the insurer's conduct, such as unreasonably denying a valid claim or delaying payments, violated the inherent duty of good faith. Sending this letter serves as a critical prerequisite for litigation, demanding that the breaching party rectify their actions to avoid potential consequential damages and legal penalties resulting from their deceptive or unfair practices.

Unreasonable Delay and Failure to Settle Demand Letter

An unreasonable delay in responding to a demand letter can be legally interpreted as bad faith. Insurance companies have a fiduciary duty to evaluate claims promptly and settle within policy limits when liability is clear. Failure to settle often exposes the insurer to bad faith litigation and excess judgments beyond the original coverage. Documenting all timelines is essential, as stalling tactics may justify additional damages for the claimant. Timely communication is a legal necessity to avoid severe financial penalties and judicial sanctions during the claims process.

Demand Letter for Extracontractual Damages and Bad Faith

A demand letter for extracontractual damages is a formal legal notice alleging an insurer breached its duty of good faith and fair dealing. This document outlines how the company failed to settle a claim reasonably, potentially exposing the insured to liability beyond policy limits. By documenting specific bad faith practices, such as unreasonable delays or inadequate investigation, the claimant seeks compensation for emotional distress or punitive damages. It serves as a critical prerequisite for litigation, pressuring insurers to resolve disputes fairly to avoid costly court judgments and statutory penalties.

Final Warning of Bad Faith Failure to Settle Letter

A Final Warning of Bad Faith Failure to Settle Letter is a critical legal document sent to an insurance company when they refuse a reasonable settlement offer within policy limits. It serves as a formal notice that their denial or delay may constitute a breach of fiduciary duty. By establishing a clear record of the insurer's unreasonable conduct, this letter lays the essential groundwork for a future bad faith lawsuit, potentially holding the insurer liable for the full extent of damages beyond the original policy coverage.

Statutory Bad Faith Failure to Settle Notice Letter

A Statutory Bad Faith Failure to Settle Notice Letter is a formal legal document required in many jurisdictions before filing a lawsuit against an insurance company. It serves as a mandatory civil remedy notice, alerting the insurer that they failed to settle a claim within policy limits despite clear liability. This letter provides the carrier a final opportunity to cure the violation. Accurately documenting the insurer's refusal to settle is essential for recovering damages beyond policy limits, ensuring the insurer is held accountable for acting in bad faith toward the insured.

Pre-Litigation Bad Faith Failure to Settle Demand Letter

A Pre-Litigation Bad Faith Failure to Settle Demand Letter is a critical legal tool sent to an insurance carrier before filing a lawsuit. It establishes a formal time-limited opportunity for the insurer to settle a claim within policy limits. By documenting clear evidence of liability and damages, the letter creates a record of the insurer's fiduciary duty to protect its insured. If the company unreasonably refuses to settle, this document serves as the foundation for future bad faith litigation, potentially holding the insurer liable for judgments exceeding the original policy coverage.

What is an insurance bad faith failure to settle claim?

An insurance bad faith failure to settle claim arises when an insurance company refuses to accept a reasonable settlement offer within policy limits despite clear liability and damages. This breach of fiduciary duty exposes the insured policyholder to an excess judgment, making the insurer potentially liable for the entire verdict regardless of policy caps.

What are the essential elements of a failure to settle demand letter?

A comprehensive demand letter must establish that the claim value exceeds policy limits, liability is clear, and a specific time-limited settlement offer was made. It should explicitly warn the insurer that rejecting the offer constitutes bad faith and that they will be held responsible for any "excess judgment" rendered at trial.

How does a time-limited demand trigger bad faith liability?

A time-limited demand creates a legal window for the insurer to protect its policyholder. If the insurer ignores or rejects a "reasonable" offer within this timeframe, they may be found to have acted in bad faith by prioritizing their own financial interests over the financial safety of the insured party.

What damages can be recovered in a bad faith failure to settle lawsuit?

If bad faith is proven, the insurer may be required to pay the full amount of the jury's verdict, even if it exceeds the original policy limits. Additionally, the plaintiff may seek recovery for emotional distress, attorney fees, interest on the judgment, and in cases of egregious conduct, punitive damages.

What evidence is needed to prove an insurer failed to settle in good faith?

Evidence typically includes the original demand letter, the insurer's written rejection or internal claims file notes, expert testimony regarding industry standards, and proof that the insurer failed to conduct a proper investigation or communicate settlement opportunities to their insured.

Comments