An Escrow Account Reconciliation Notice is a formal communication sent to borrowers detailing the adjustment of their monthly mortgage payments. It ensures that funds collected for property taxes and insurance align with actual costs, preventing shortages or surpluses. Maintaining transparency in these calculations is essential for regulatory compliance and borrower trust. To simplify your communication, below are some ready to use templates.

Image cover: Mastering Escrow Account Reconciliation: Essential Notice Samples and Professional Templates

Letter Samples List

- Annual Escrow Account Reconciliation Notice Letter

- Escrow Account Shortage Adjustment Notice Letter

- Escrow Account Surplus Refund Notice Letter

- Monthly Real Estate Escrow Reconciliation Letter

- Final Escrow Account Disbursement and Reconciliation Letter

- Escrow Account Deficiency Demand Notice Letter

- Post-Closing Escrow Reconciliation Status Letter

- Escrow Account Audit and Reconciliation Notice Letter

- Property Tax Escrow Account Reconciliation Letter

- Hazard Insurance Escrow Reconciliation Notice Letter

- Escrow Account Payment Change Notice Letter

- Buyer Earnest Money Escrow Reconciliation Letter

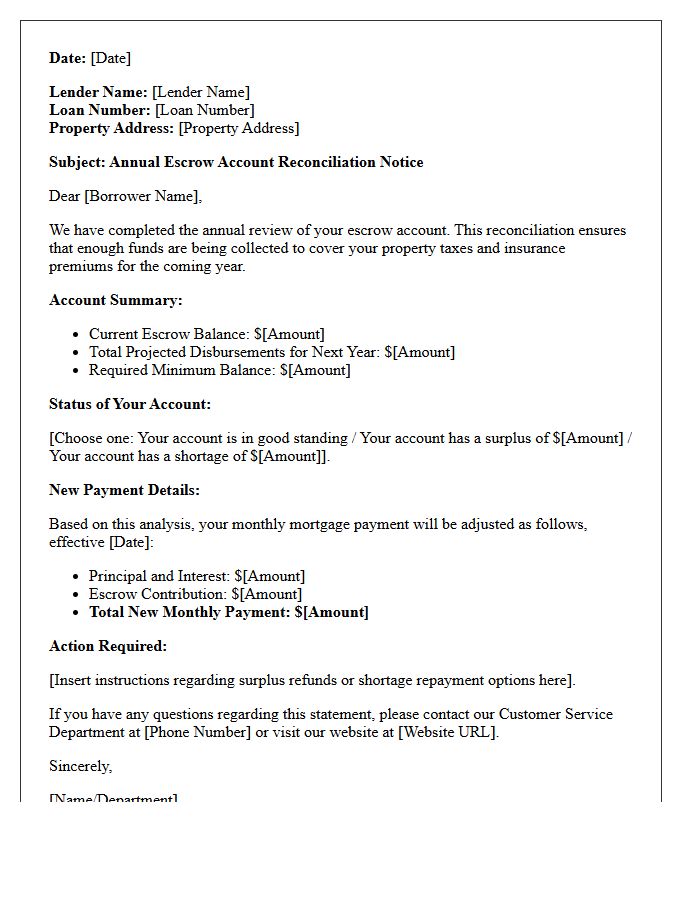

Annual Escrow Account Reconciliation Notice Letter

The Annual Escrow Account Reconciliation Notice is a mandatory statement from your mortgage lender. It details the escrow analysis performed to ensure your monthly payments cover property taxes and insurance. This letter identifies any escrow shortage or surplus based on actual billing changes. If your tax assessments or premiums increased, your future mortgage payment will likely rise to compensate. Reviewing this document is essential to understanding payment adjustments and maintaining a balanced account throughout the year.

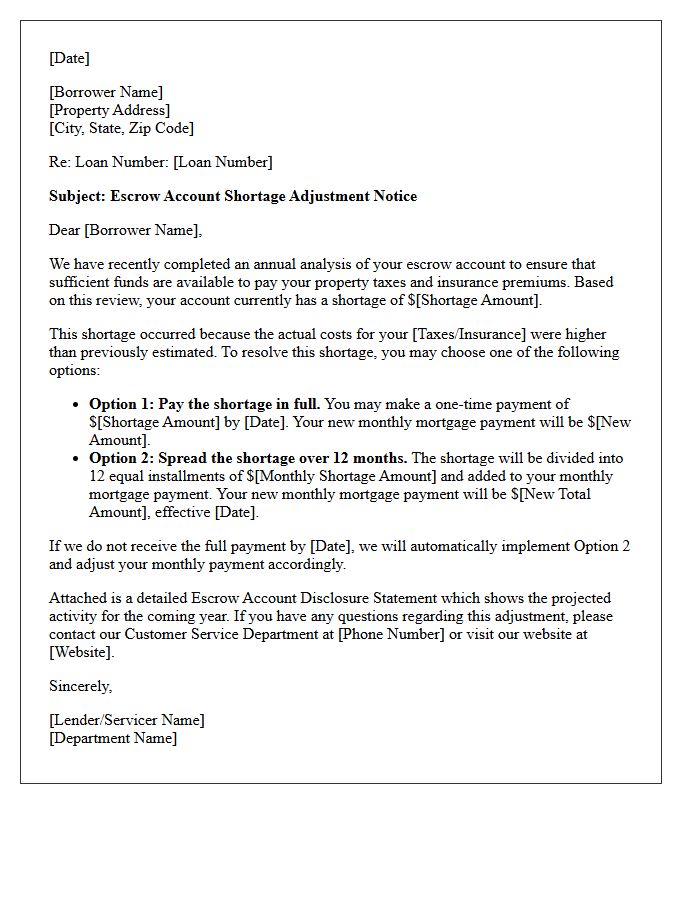

Escrow Account Shortage Adjustment Notice Letter

An Escrow Account Shortage Adjustment Notice Letter informs homeowners that their property taxes or insurance premiums increased beyond current funds. To rectify this deficit, lenders provide two repayment options: a one-time lump-sum payment or a monthly increase in your mortgage installments. It is essential to review the included annual escrow analysis to verify tax assessments and premium hikes. Addressing a shortage promptly prevents long-term financial strain and ensures your loan compliance while maintaining adequate coverage for your home's essential liabilities.

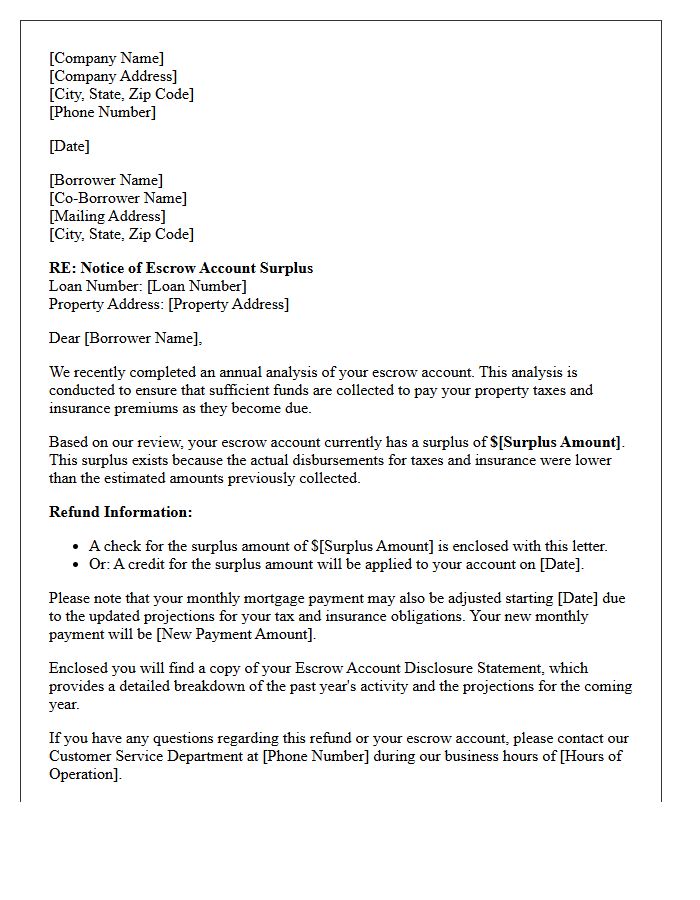

Escrow Account Surplus Refund Notice Letter

An Escrow Account Surplus Refund Notice Letter is an official document sent by mortgage lenders when your annual analysis reveals a positive balance. This occurs because actual property taxes or insurance premiums were lower than estimated. The letter confirms a surplus refund is being issued, typically via a check or a credit toward future payments. It is crucial to review this notice alongside your escrow statement to ensure accurate disbursements and to understand how these adjustments might impact your monthly mortgage payment going forward.

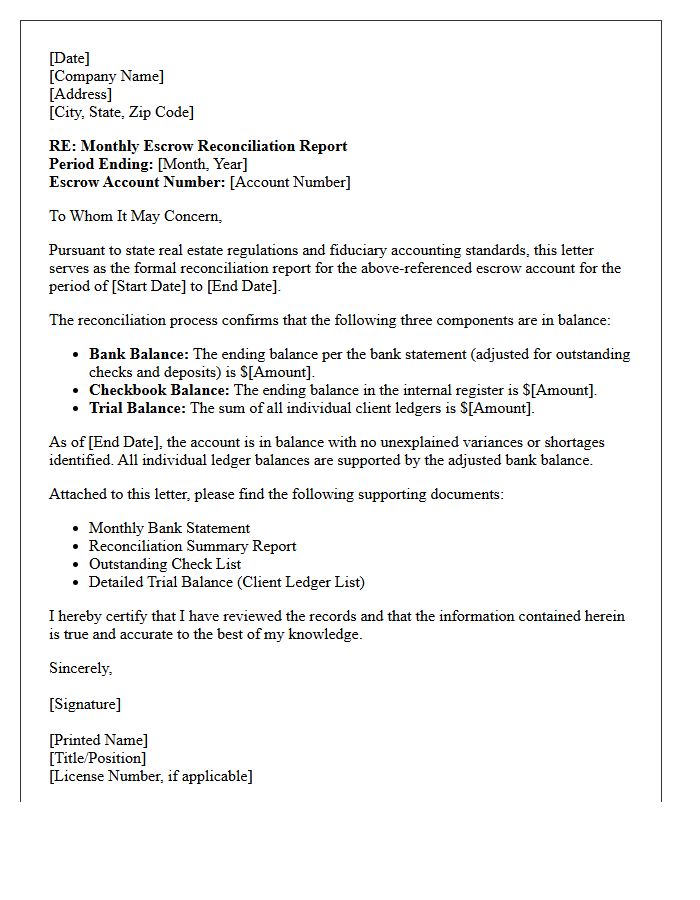

Monthly Real Estate Escrow Reconciliation Letter

A Monthly Real Estate Escrow Reconciliation Letter is a critical compliance document used to verify that a brokerage's trust account records align perfectly with bank statements. This process ensures that fiduciary duties are met and client funds are protected from errors or fraud. Brokerages must compare the bank balance, the cash ledger, and the sum of individual client liabilities to achieve a "three-way reconciliation." Maintaining these accurate, monthly records is mandatory for most regulatory audits and helps prevent the commingling of funds, ensuring financial transparency in every real estate transaction.

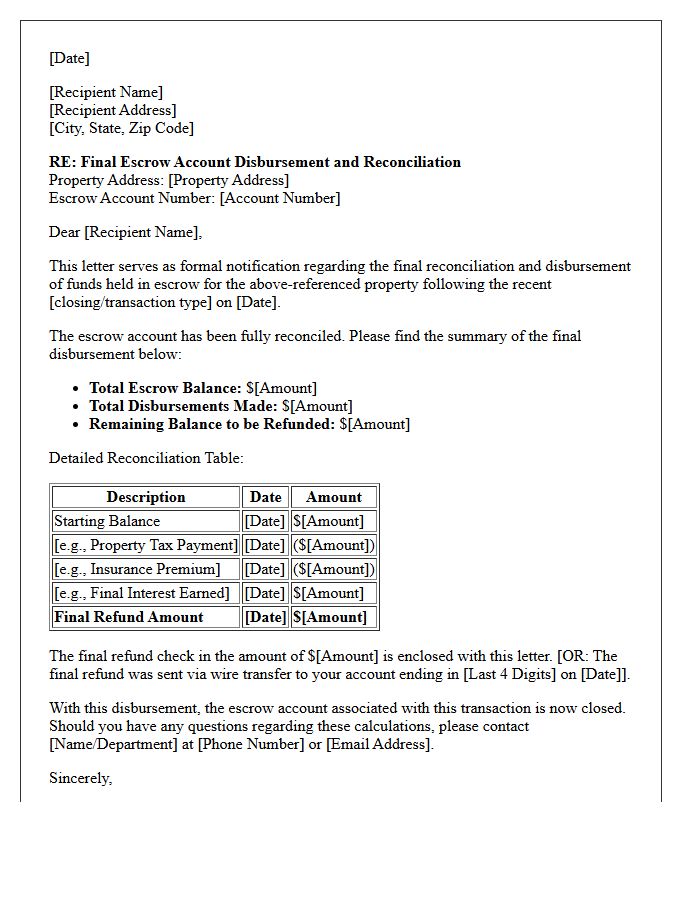

Final Escrow Account Disbursement and Reconciliation Letter

A Final Escrow Account Disbursement and Reconciliation Letter is the official closing statement used to liquidate remaining funds after a real estate transaction or mortgage payoff. It provides a detailed breakdown of all tax payments, insurance premiums, and service fees processed through the account. Recipients must verify this document to ensure the remaining balance is accurately refunded or applied to the principal balance. This record is essential for personal financial auditing and ensures that all fiduciary obligations have been legally settled between the lender, title agent, and homeowner.

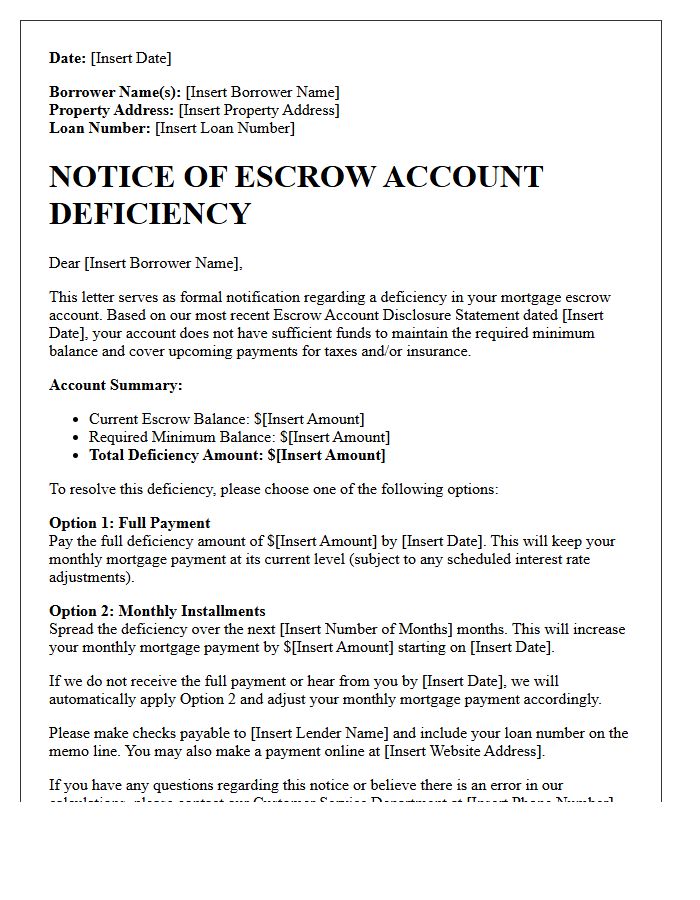

Escrow Account Deficiency Demand Notice Letter

An Escrow Account Deficiency Demand Notice Letter informs a homeowner that their escrow balance has fallen below the required minimum. This shortfall usually occurs due to an increase in property taxes or insurance premiums. The notice requires the borrower to pay the shortage amount to ensure future obligations are met. Failure to address this demand can lead to significantly higher monthly mortgage payments as the lender adjusts the escrow analysis to recover the funds. It is critical to review the statement for accuracy and respond promptly to maintain financial stability.

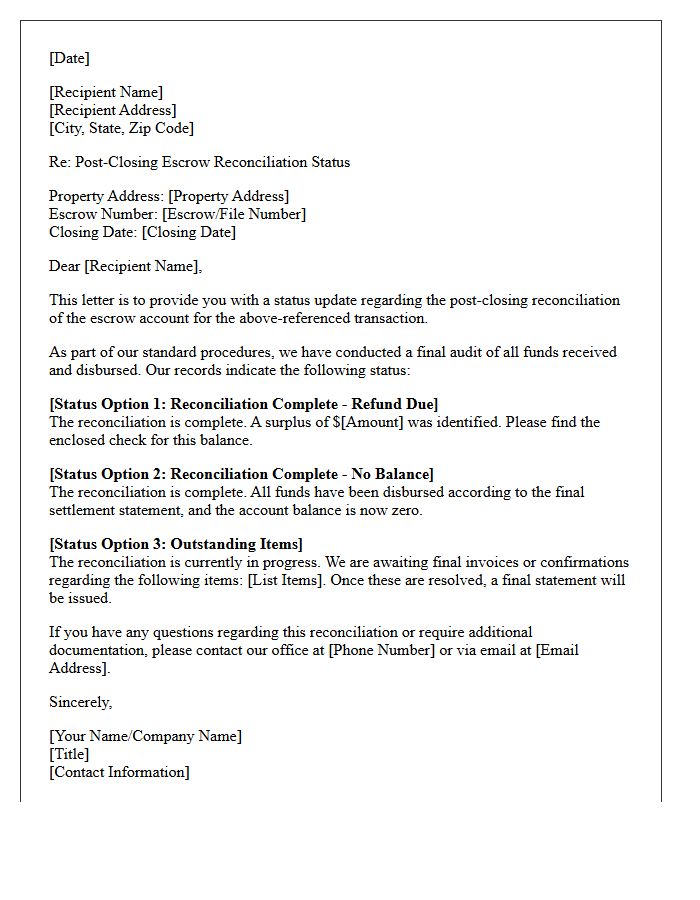

Post-Closing Escrow Reconciliation Status Letter

A Post-Closing Escrow Reconciliation Status Letter is a critical document confirming that a real estate transaction has been financially finalized. It verifies that all funds held in escrow were properly balanced and disbursed according to the settlement statement. This letter ensures that no outstanding checks remain and that the title agency has completed its fiduciary duties. For homeowners and lenders, receiving this status update provides legal assurance that the account reconciliation process is accurate, protecting all parties from future financial discrepancies or accounting errors after the closing date.

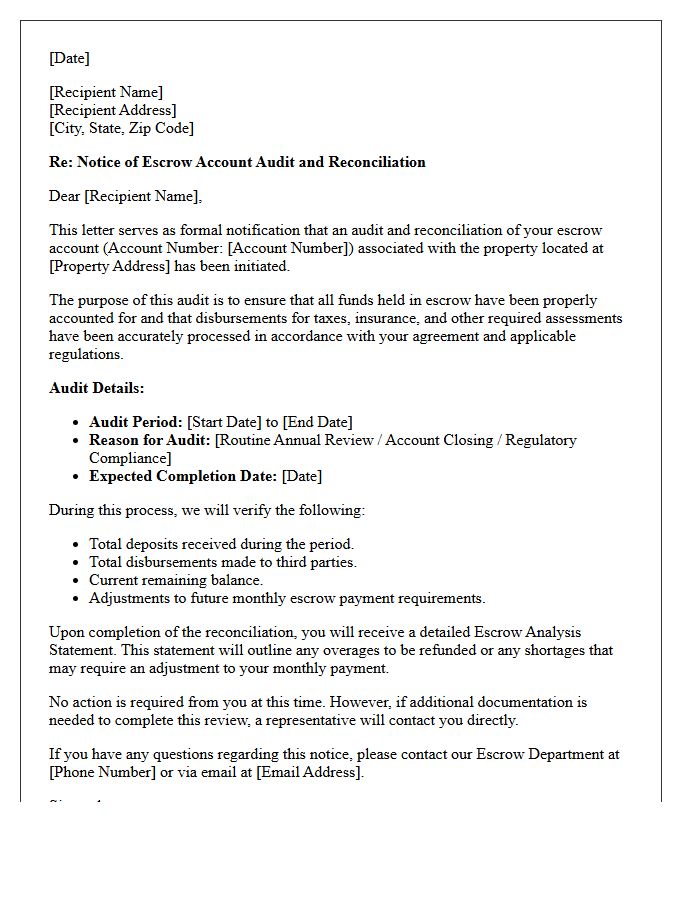

Escrow Account Audit and Reconciliation Notice Letter

An Escrow Account Audit and Reconciliation Notice Letter informs parties about a formal review of funds held in trust. This document ensures financial accuracy by identifying discrepancies between recorded balances and actual bank holdings. It serves as a legal record of compliance, verifying that disbursements and deposits align with contractual obligations. For property managers or legal firms, regular reconciliation prevents mismanagement and maintains transparency. Receiving this notice indicates a proactive step to rectify errors, satisfy regulatory requirements, and protect the integrity of the fiduciary relationship between all involved stakeholders.

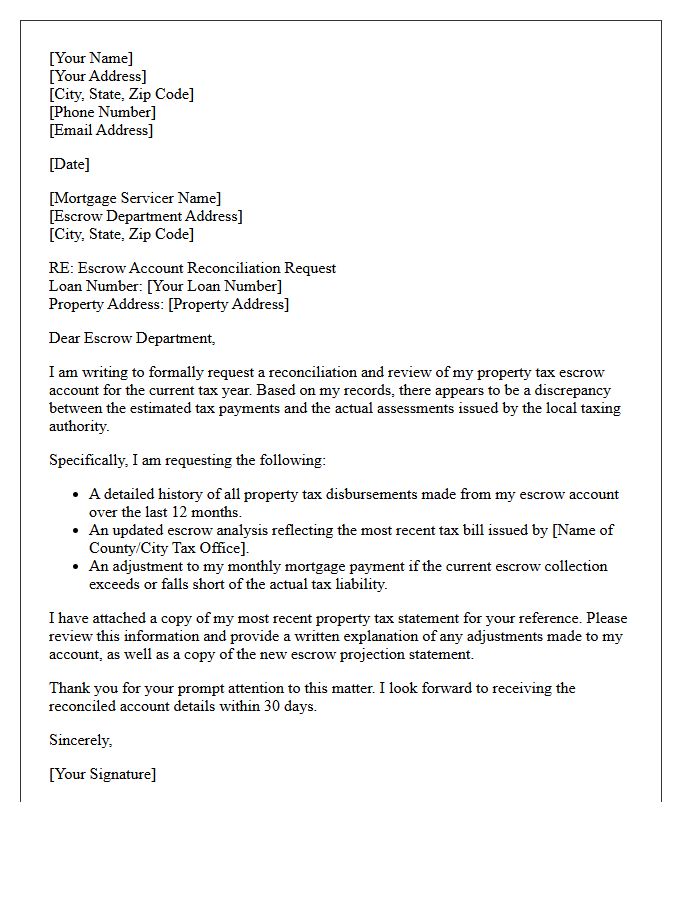

Property Tax Escrow Account Reconciliation Letter

A property tax escrow account reconciliation letter is an official notice from your mortgage lender detailing the annual review of your escrow account. This document compares estimated tax and insurance payments against actual disbursements to ensure a sufficient balance. It identifies an overage, resulting in a refund check, or a shortage, which may increase your monthly mortgage payment. Reviewing this statement is essential for managing your housing budget and verifying that your property taxes are paid correctly and on time by the financial institution.

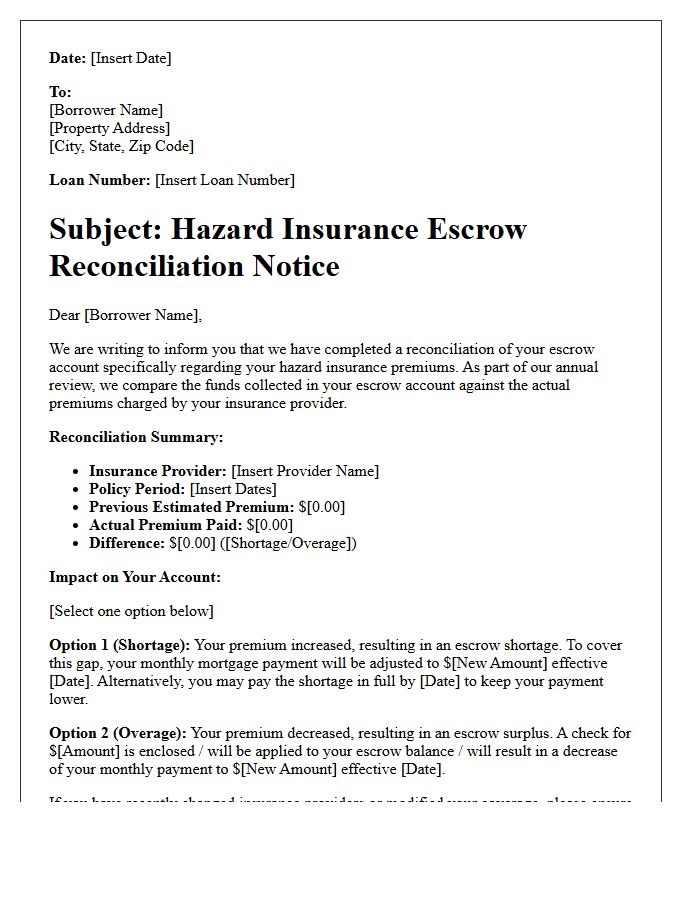

Hazard Insurance Escrow Reconciliation Notice Letter

A Hazard Insurance Escrow Reconciliation Notice Letter is a formal document sent by mortgage lenders to adjust your escrow account. It informs homeowners of changes in homeowners insurance premiums that impact monthly mortgage payments. If your premium increases, the lender may identify an escrow shortage, requiring a higher monthly contribution or a one-time payment. Conversely, a surplus may result in a refund check. Reviewing this notice is essential to ensure your property remains protected and to understand updates to your total monthly housing costs.

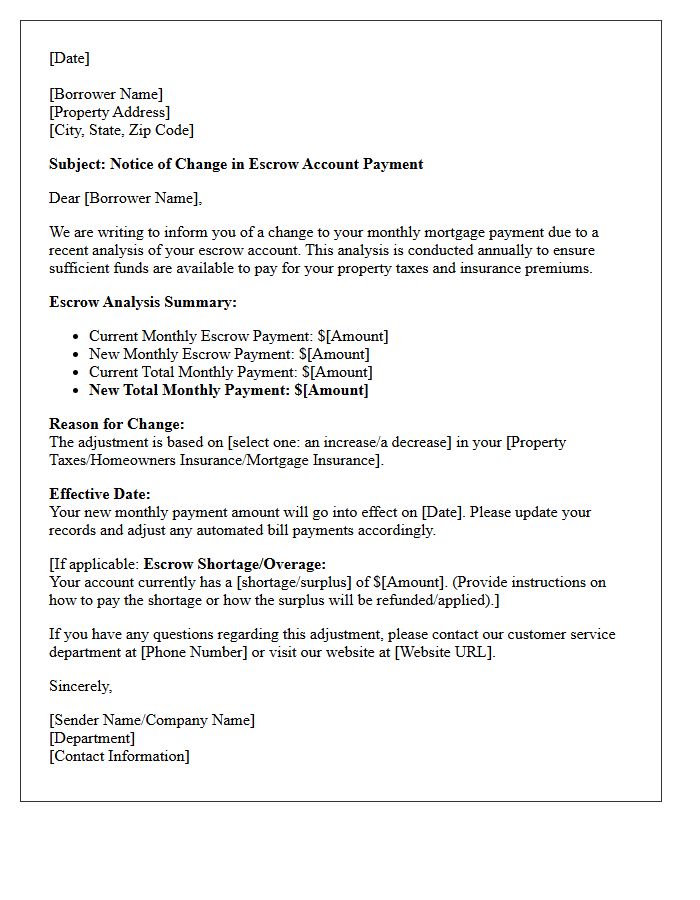

Escrow Account Payment Change Notice Letter

An Escrow Account Payment Change Notice Letter is a mandatory update from your mortgage servicer detailing adjustments to your monthly bill. This typically occurs after an annual escrow analysis, where the lender re-evaluates costs for property taxes and homeowners insurance. If these expenses increase, your payment will likely rise to cover the shortage. Conversely, a surplus may result in a lower payment or a refund check. Reviewing this notice is essential to understand changes in your mortgage obligations and ensure your household budget remains accurate.

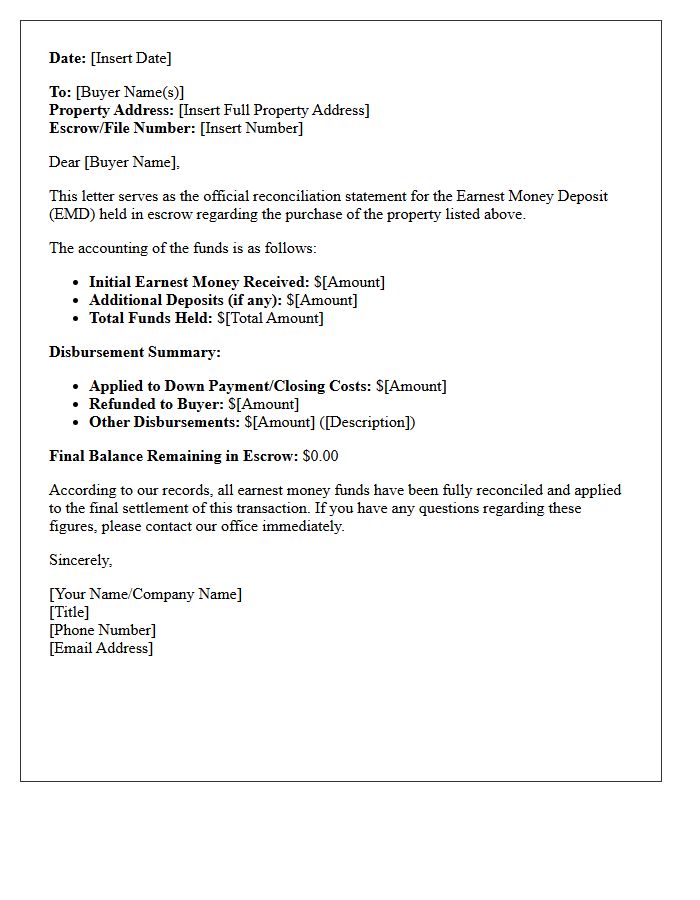

Buyer Earnest Money Escrow Reconciliation Letter

A Buyer Earnest Money Escrow Reconciliation Letter is a vital document used to verify the release of held funds. This letter confirms that the earnest money deposit matches the final settlement figures. It ensures transparency between the buyer, seller, and escrow agent, preventing financial discrepancies during the closing process. Signed by all parties, it serves as a formal authorization to allocate or refund the deposit correctly. Maintaining this record is essential for legal compliance and clear accounting, protecting your financial interests before the property title officially transfers.

What is an Escrow Account Reconciliation Notice?

An Escrow Account Reconciliation Notice is an official statement sent by a mortgage servicer to notify a borrower of the findings from an annual escrow analysis. It details whether the account has a surplus, a shortage, or a deficiency based on the actual costs of property taxes and insurance premiums compared to previous estimates.

Why did my monthly mortgage payment change after receiving this notice?

Your monthly payment typically changes because the costs for your homeowners insurance or property taxes have fluctuated. If these expenses increase, your servicer must raise your monthly escrow contribution to ensure sufficient funds are available; conversely, if costs decrease, your monthly payment may go down.

How do I resolve an escrow shortage or deficiency mentioned in the notice?

Borrowers generally have two options: you can pay the total shortage amount in a single lump-sum payment to keep your monthly principal and interest payment stable, or you can choose to spread the shortage amount across 12 monthly installments, which will be added to your regular mortgage payment.

What happens if my reconciliation notice shows an escrow surplus?

If your account has a surplus of $50 or more, and your mortgage is current, the servicer is generally required to issue a refund check for the overage. If the surplus is less than $50, the servicer may choose to issue a refund or apply the credit toward your future monthly escrow payments.

How often is an Escrow Account Reconciliation performed?

Under the Real Estate Settlement Procedures Act (RESPA), mortgage lenders and servicers are required to perform an escrow account reconciliation at least once every 12-month period to ensure the account remains balanced and compliant with federal regulations.

Comments