Navigating financial hardship can be overwhelming, but a Home Equity Line of Credit Forgiveness Letter is a vital tool for negotiating debt reduction with your lender. This formal request outlines your financial situation to seek a partial or full discharge of your balance. Understanding how to structure your plea can significantly improve your chances of approval. Below are some ready to use template.

Image cover: HELOC Debt Forgiveness: Professional Hardship Letter Samples and Templates

Letter Samples List

- Home Equity Line of Credit Forgiveness Letter

- Real Estate Hardship and HELOC Forgiveness Letter

- Request for Home Equity Principal Forgiveness Letter

- HELOC Short Sale Deficiency Forgiveness Letter

- Lender Approved Home Equity Debt Forgiveness Letter

- Underwater Property HELOC Forgiveness Letter

- Negative Equity Settlement and Forgiveness Letter

- Loss of Income Home Equity Forgiveness Letter

- Medical Hardship HELOC Debt Forgiveness Letter

- Home Equity Deficiency Waiver and Forgiveness Letter

- Real Estate Foreclosure HELOC Forgiveness Letter

- Mutual Agreement HELOC Balance Forgiveness Letter

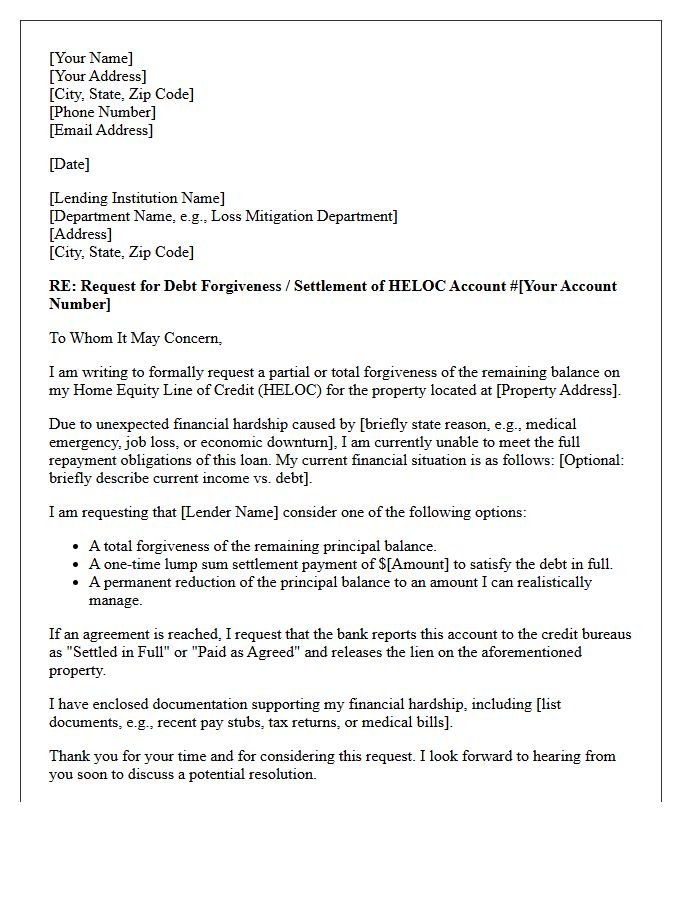

Home Equity Line of Credit Forgiveness Letter

A home equity line of credit forgiveness letter is a legal document from a lender confirming the cancellation of remaining HELOC debt. This usually occurs after a short sale, settlement, or loan modification. It is vital to verify that the letter includes a "release of lien" to clear your property title. Be aware that the IRS may treat forgiven amounts as taxable income, so always consult a professional. Keeping this official record is essential for protecting your credit score and ensuring no future collection actions can be taken against you.

Real Estate Hardship and HELOC Forgiveness Letter

A real estate hardship letter is a formal request for debt relief, explaining financial struggles like job loss or medical crises. When seeking HELOC forgiveness, you must demonstrate that your property value is lower than the balance owed. Lenders may consider a short payoff or settlement if they believe foreclosure will result in a greater loss. Clearly documenting your income reduction and offering a specific settlement amount are essential steps. Successfully negotiating lien release through this process can prevent foreclosure and provide a critical financial fresh start for distressed homeowners.

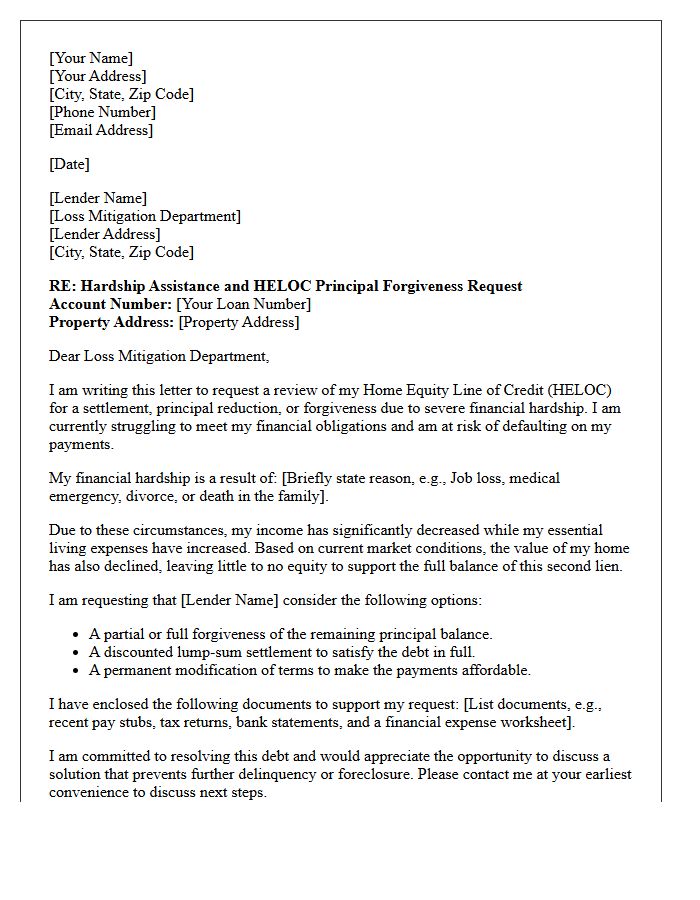

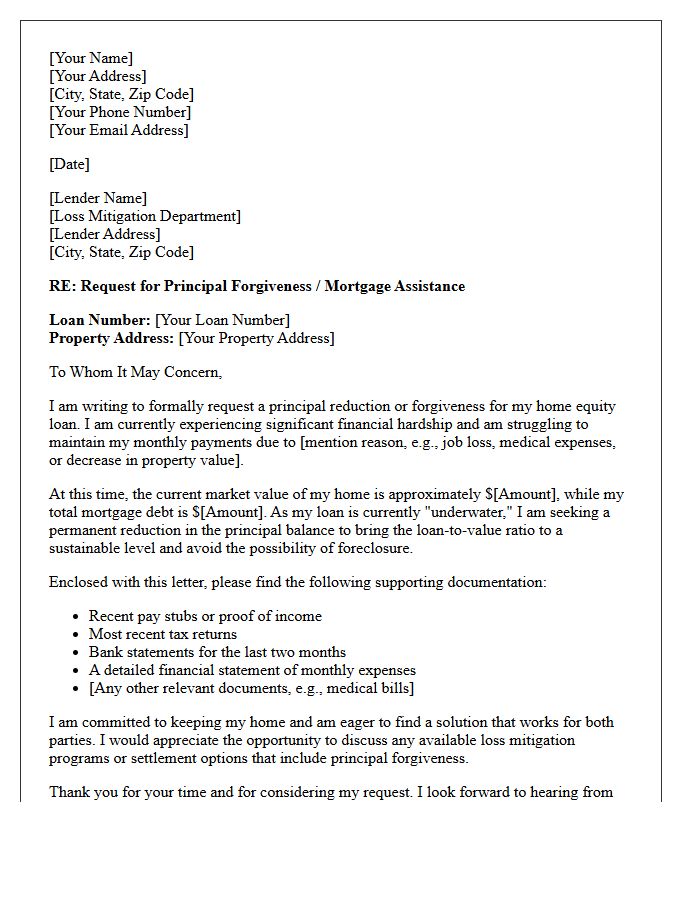

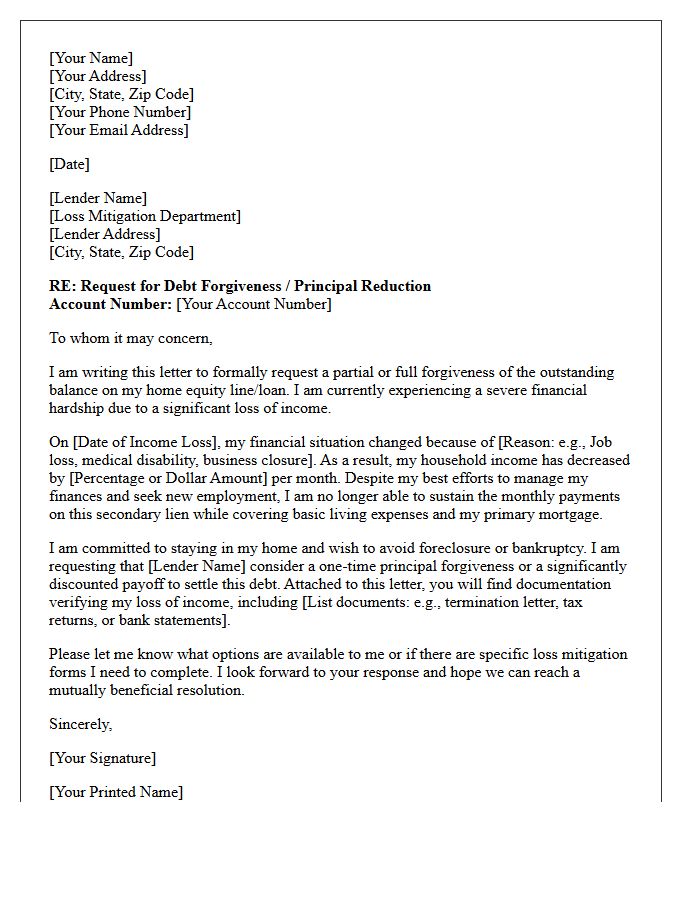

Request for Home Equity Principal Forgiveness Letter

A Home Equity Principal Forgiveness Letter is a formal request sent to a lender to reduce the outstanding balance of a secondary mortgage. This process is essential for homeowners facing severe financial hardship or negative equity. The document must clearly demonstrate an inability to maintain payments and provide evidence of the property's current market value. Successful approval allows borrowers to avoid foreclosure by making the debt more manageable. Always include a specific hardship statement and supporting financial documentation to improve the chances of a favorable lender decision and long-term housing stability.

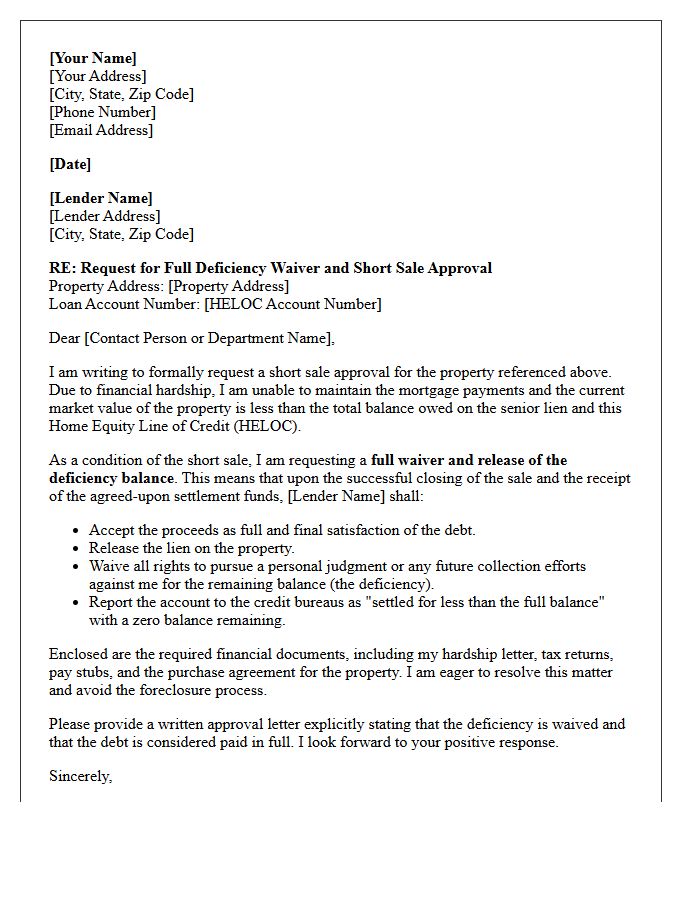

HELOC Short Sale Deficiency Forgiveness Letter

A HELOC Short Sale Deficiency Forgiveness Letter is a critical legal document issued by a lender during a real estate short sale. It explicitly states that the bank waives its right to pursue the borrower for the unpaid balance remaining on the home equity line of credit. Without this formal written release, lenders may seek a deficiency judgment or sell the debt to collectors. Homeowners must ensure the language confirms "full satisfaction of debt" to guarantee financial protection and prevent future legal liability or wage garnishments after the property is sold.

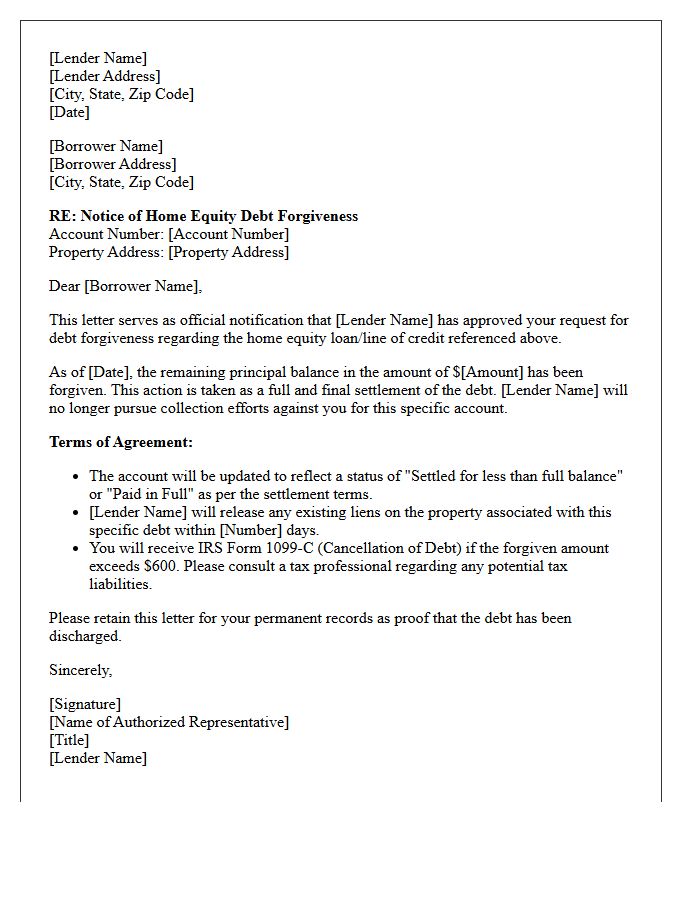

Lender Approved Home Equity Debt Forgiveness Letter

A Lender Approved Home Equity Debt Forgiveness Letter is a formal legal document confirming that a financial institution has agreed to cancel a specific portion of your secondary mortgage. This written release is essential during short sales or debt settlements to prove you are no longer liable for the remaining balance. Always verify if the agreement includes a deficiency waiver to prevent future collections. Be aware that forgiven amounts may be viewed as taxable income by the IRS, so keep this letter for your permanent financial records.

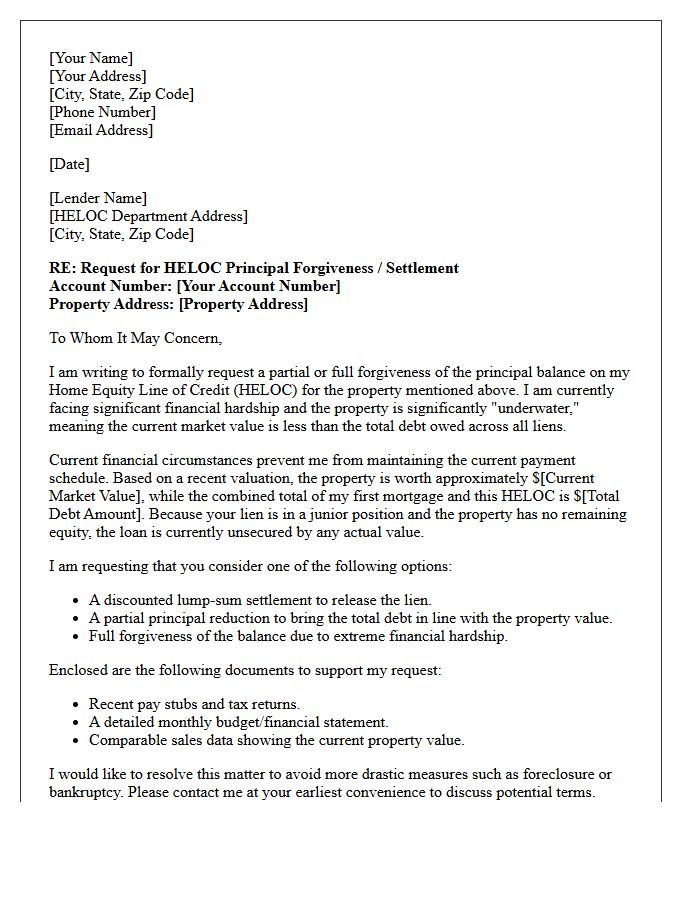

Underwater Property HELOC Forgiveness Letter

An Underwater Property HELOC Forgiveness Letter is a formal request sent to a lender asking to cancel secondary mortgage debt when the home's market value is lower than the balance owed. To improve approval odds, homeowners must demonstrate severe financial hardship and prove that the lender would recover less through foreclosure. Successful debt settlement or partial discharge results in a release of the lien, though it may trigger tax implications. Providing clear documentation of income loss and current property valuations is essential for negotiating a successful deficiency waiver.

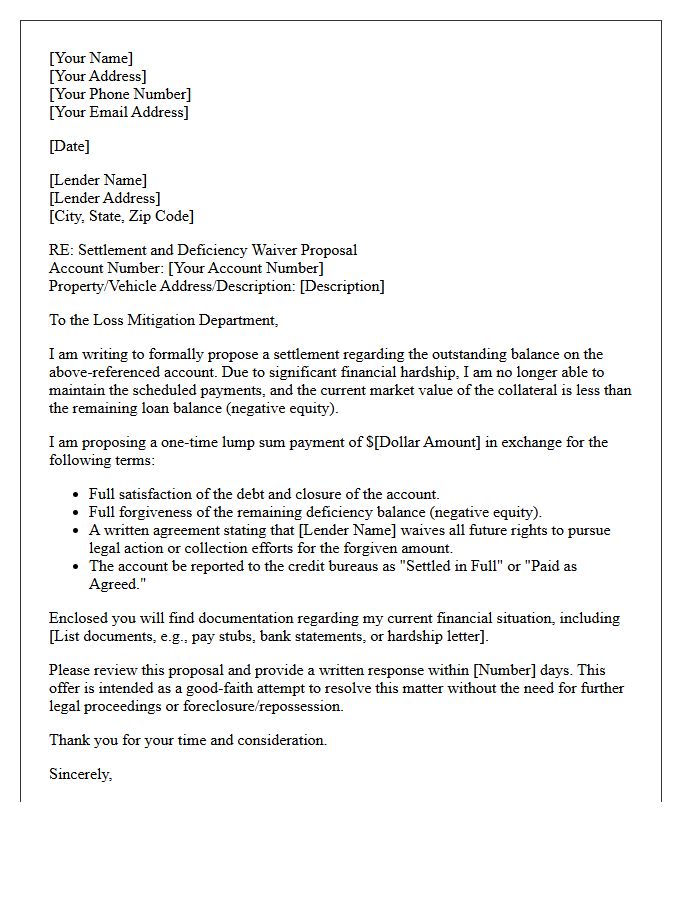

Negative Equity Settlement and Forgiveness Letter

A Negative Equity Settlement occurs when a lender agrees to accept less than the total balance owed on a loan, typically after a vehicle total loss or property sale. Obtaining a Forgiveness Letter is critical, as it serves as legal proof that the remaining deficiency balance is waived. Without this official document, creditors may still pursue the debtor for the difference or report it as a default. It is essential to confirm if the forgiven amount is taxable income and ensure the agreement permanently releases you from further financial liability.

Loss of Income Home Equity Forgiveness Letter

A loss of income home equity forgiveness letter is a formal request to lenders seeking debt cancellation or payment relief due to financial hardship. This document must clearly explain your involuntary unemployment or reduced earnings while providing verifiable proof of your situation. Successfully negotiating these terms can prevent foreclosure and protect your remaining home equity. It is essential to propose a specific settlement or modification plan to show a proactive commitment to resolving the balance. Professional legal or financial advice is recommended when drafting this hardship affidavit to ensure legal compliance.

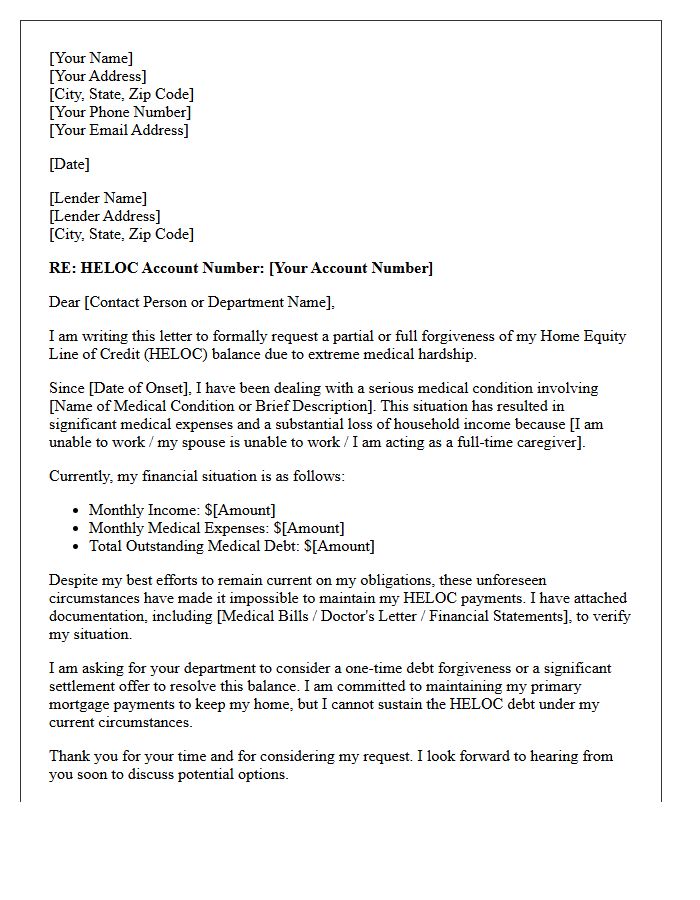

Medical Hardship HELOC Debt Forgiveness Letter

A Medical Hardship HELOC Debt Forgiveness Letter is a formal request to your lender to reduce or cancel home equity debt due to extreme healthcare costs. To improve your chances, you must provide documented proof of your financial crisis, such as medical bills and loss of income. Clearly explain why your situation is involuntary and permanent. While banks are not legally required to grant forgiveness, they may offer a short sale, settlement, or loan modification to avoid the costly foreclosure process. Always send the letter via certified mail for tracking.

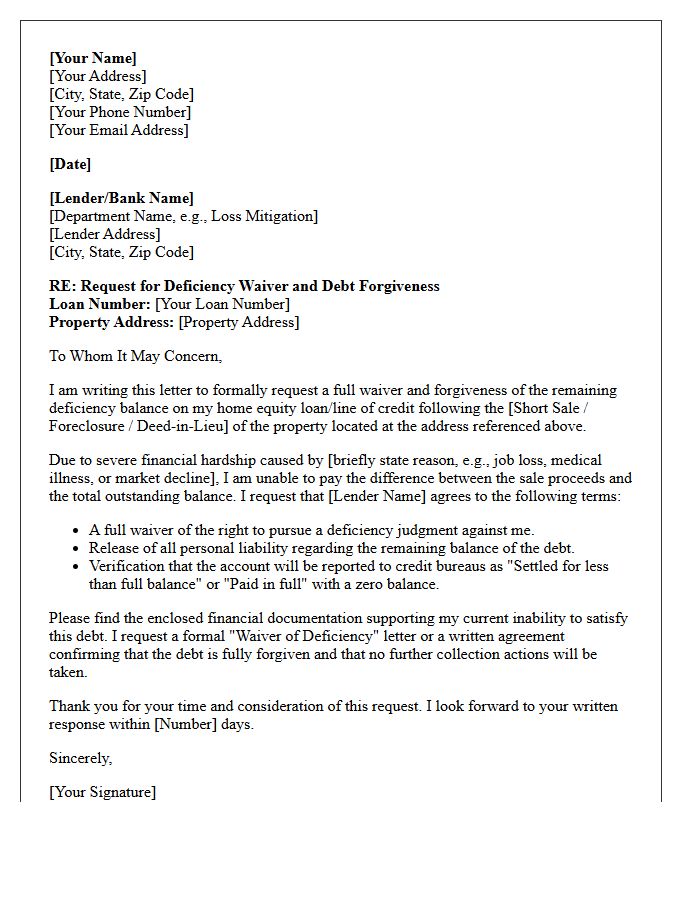

Home Equity Deficiency Waiver and Forgiveness Letter

A Home Equity Deficiency Waiver is a critical legal agreement where a lender forfeits the right to pursue a borrower for the remaining balance after a short sale or foreclosure. Obtaining a formal Forgiveness Letter is essential because it serves as official proof that the debt is canceled, preventing future collection actions or judgments. Without this specific language, homeowners may remain personally liable for the financial gap. Always consult a professional to ensure the document explicitly waives deficiency rights to protect your future financial stability and credit health.

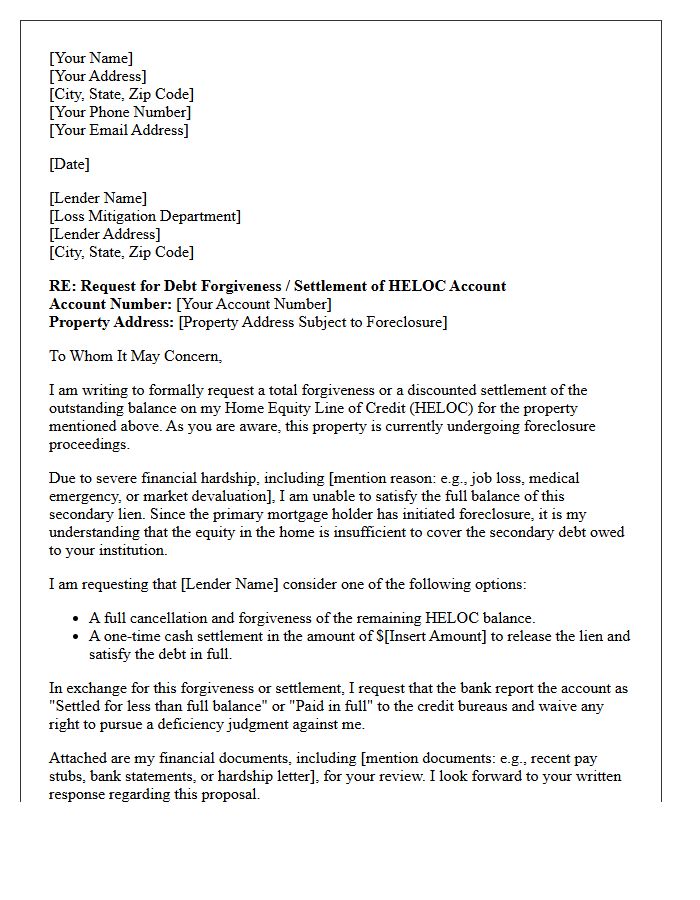

Real Estate Foreclosure HELOC Forgiveness Letter

A Real Estate Foreclosure HELOC Forgiveness Letter is a formal request sent to a lender asking to waive the remaining debt on a Home Equity Line of Credit after a foreclosure. Since a HELOC is a secondary lien, the sale proceeds often fail to cover the balance, leaving the borrower liable for a deficiency judgment. Obtaining a written release is crucial to prevent future collection efforts and lawsuits. It is a vital step in debt settlement to ensure the homeowner is fully legally discharged from further financial obligations following the loss of the property.

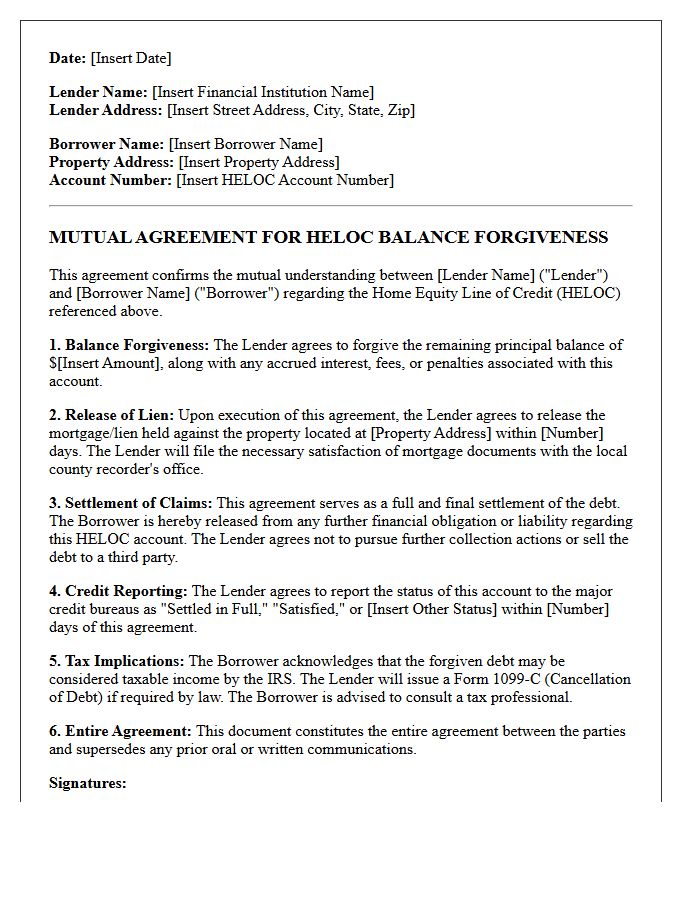

Mutual Agreement HELOC Balance Forgiveness Letter

A Mutual Agreement HELOC Balance Forgiveness Letter is a legal contract between a borrower and a lender to settle a Home Equity Line of Credit for less than the total amount owed. This document serves as written proof that the lender agrees to waive the remaining debt, preventing future collection actions. It is crucial to ensure the letter explicitly states the account is settled in full and specifies any tax implications or credit reporting impacts resulting from the forgiven debt amount.

What is a HELOC forgiveness letter?

A HELOC forgiveness letter is an official document from a mortgage lender stating that a borrower's Home Equity Line of Credit balance has been partially or fully cancelled, typically as part of a debt settlement or short sale agreement.

Can you negotiate a Home Equity Line of Credit forgiveness?

Yes, lenders may agree to forgive a portion of a HELOC through a "settlement for less than full balance" if the borrower is in financial hardship, the home's value has significantly dropped, or the lender wants to avoid the costs of foreclosure.

Are there tax implications for HELOC debt forgiveness?

Yes, the IRS generally treats forgiven debt as taxable income. If your lender issues a 1099-C form following a HELOC forgiveness letter, you may be required to report the cancelled amount on your federal tax return unless you qualify for an insolvency exception.

How does a HELOC forgiveness letter affect your credit score?

Receiving a forgiveness letter often results in a negative impact on your credit score, as the account is typically reported to bureaus as "settled for less than the full amount" rather than "paid in full."

What should be included in a formal HELOC settlement agreement?

A formal agreement should clearly state the total amount forgiven, the final payment required to close the account, a confirmation that the lien on the property will be released, and the specific terms regarding how the account will be reported to credit bureaus.

Comments