Staying informed during a real estate transaction requires a clear Short Sale Bank Status Update Letter to communicate with lenders effectively. This essential document tracks the approval progress and ensures all parties remain aligned on the timeline. Monitoring your application status helps prevent delays and keeps the closing on schedule. To help you get started, below are some ready to use template.

Image cover: Professional Short Sale Status Update Templates and Bank Communication Guide

Letter Samples List

- Initial Submission Short Sale Bank Status Update Letter

- Missing Document Short Sale Bank Status Update Letter

- Negotiator Assignment Short Sale Bank Status Update Letter

- Broker Price Opinion Short Sale Bank Status Update Letter

- Property Appraisal Short Sale Bank Status Update Letter

- Investor Review Short Sale Bank Status Update Letter

- Mortgage Insurance Short Sale Bank Status Update Letter

- Counteroffer Review Short Sale Bank Status Update Letter

- Buyer Addendum Short Sale Bank Status Update Letter

- Management Escalation Short Sale Bank Status Update Letter

- Final Approval Short Sale Bank Status Update Letter

- Closing Extension Short Sale Bank Status Update Letter

- File Denial Short Sale Bank Status Update Letter

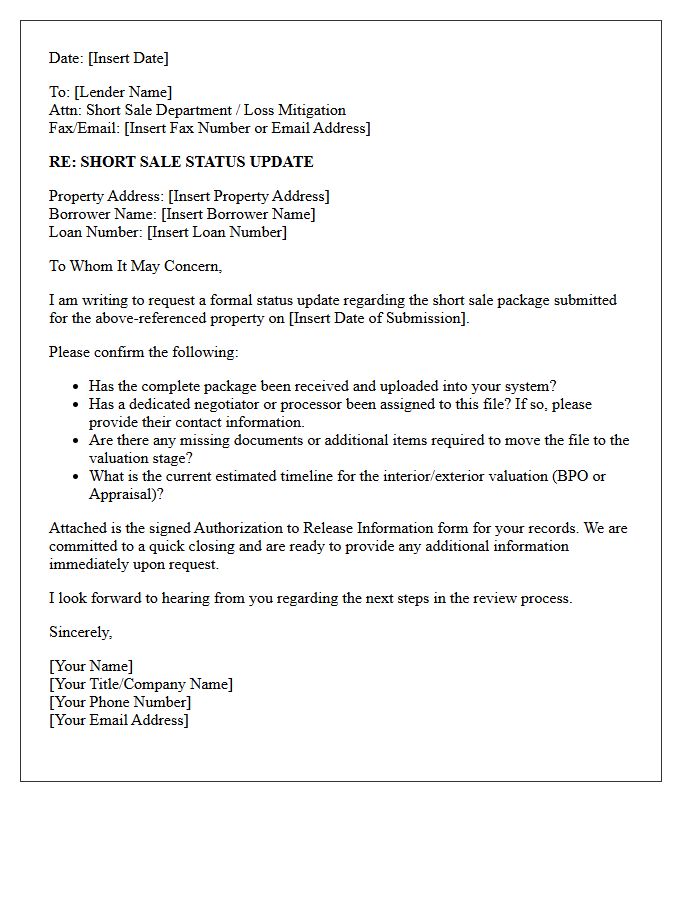

Initial Submission Short Sale Bank Status Update Letter

The Initial Submission Short Sale Bank Status Update Letter is a formal document verifying that a lender has received a complete loss mitigation package. It confirms that the short sale review has officially commenced. This letter provides an estimated timeline for the valuation process and identifies any missing documentation required to prevent delays. For homeowners and agents, receiving this update is critical as it signals the transition from application to active underwriting, ensuring the foreclosure process is temporarily paused while the bank evaluates the potential sale agreement.

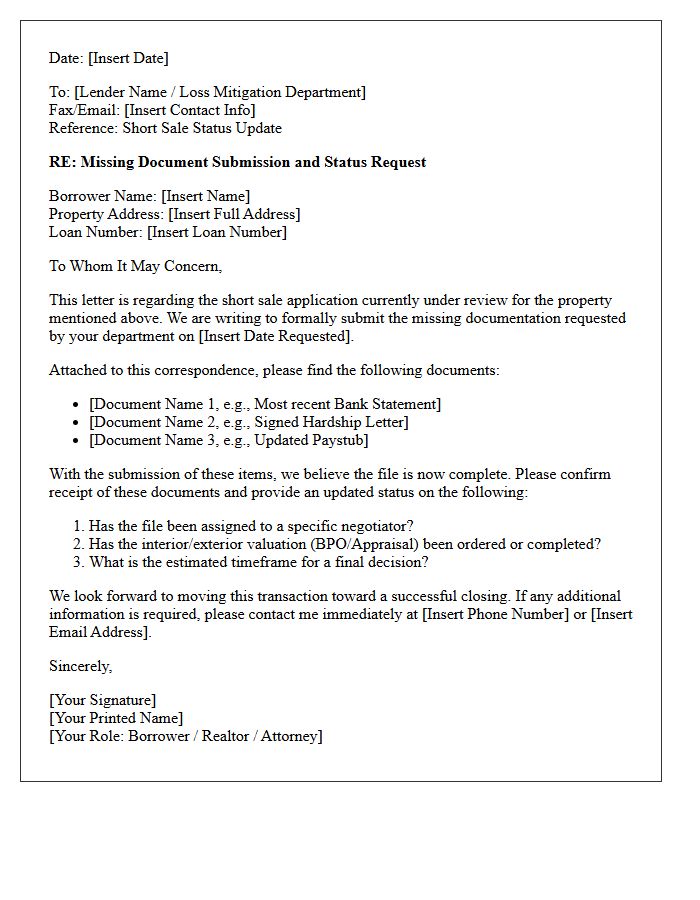

Missing Document Short Sale Bank Status Update Letter

A Missing Document Short Sale Bank Status Update Letter is a critical communication used to identify incomplete financial packages during the foreclosure avoidance process. This formal notice specifies which required items, such as tax returns or hardship letters, are still outstanding. Promptly addressing these deficiencies is essential to maintain processing timelines and prevent a file from being closed or denied. Timely responses ensure the lender can continue evaluating the short sale offer, ultimately helping homeowners avoid foreclosure through successful debt settlement.

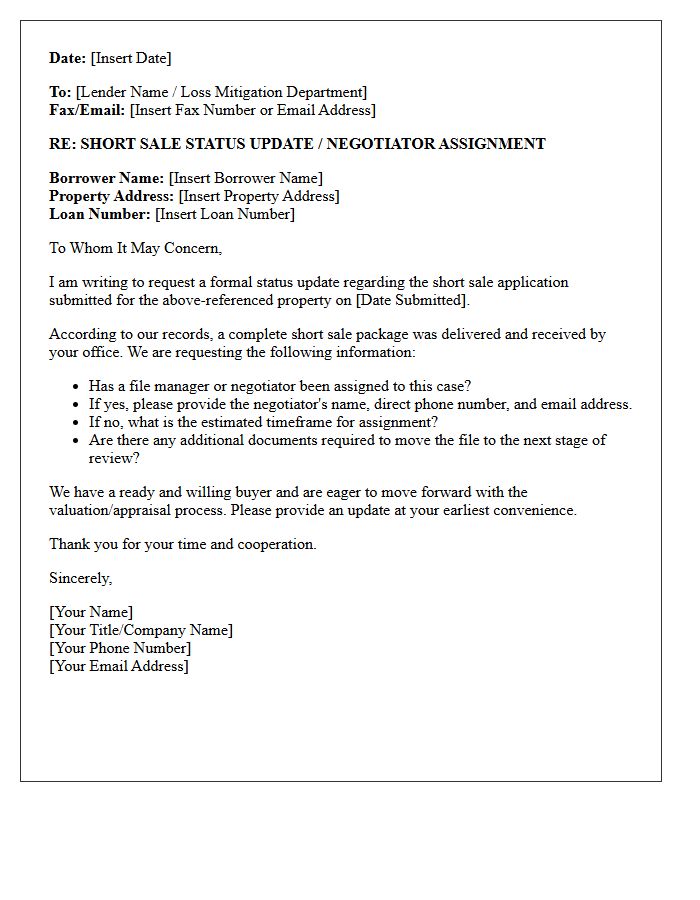

Negotiator Assignment Short Sale Bank Status Update Letter

A Negotiator Assignment status update confirms that the lender has designated a specific representative to review your short sale application. This is a critical milestone, signaling the transition from document collection to active evaluation. This letter provides the negotiator's contact details, facilitating direct communication for offer valuation and lien holder approvals. Timely responses to their requests are essential to maintain momentum, as this stage directly precedes the final approval letter and the successful closing of the real estate transaction.

Broker Price Opinion Short Sale Bank Status Update Letter

A Broker Price Opinion (BPO) is a critical valuation tool used by lenders to determine a property's current market value during a short sale. This status update letter informs stakeholders of the valuation results, which directly influence the bank's decision to approve or counter an offer. Timely updates ensure transparency between the seller and the lender. Accurate reporting is essential because the BPO serves as the primary benchmark for deficiency waivers and final transaction approval in distressed real estate proceedings.

Property Appraisal Short Sale Bank Status Update Letter

A short sale bank status update letter serves as a formal communication tool to track progress during distressed property negotiations. This document provides a valuation timeline, confirming when the lender's appraisal or Broker Price Opinion (BPO) was completed. It is essential for ensuring transparency between the seller, buyer, and financial institution. This letter helps stakeholders understand the bank's current position regarding the property appraisal, potential price adjustments, and the overall approval stage, preventing unnecessary delays in the closing process while maintaining alignment on the home's fair market value.

Investor Review Short Sale Bank Status Update Letter

An Investor Review status letter is a critical update notifying parties that the mortgage servicer has submitted the short sale offer to the underlying owner of the loan for final approval. This stage confirms that the bank's internal valuation is complete and the file meets basic eligibility. It represents the final transition before a formal Short Sale Approval Letter is issued. Timely responses to additional documentation requests during this period are essential to prevent delays or file closures while the investor evaluates the net recovery on the property.

Mortgage Insurance Short Sale Bank Status Update Letter

A Mortgage Insurance Short Sale Bank Status Update Letter is a formal notification regarding the current progress of a short sale application. This document confirms if the mortgage insurer has approved the reduced payoff amount. It serves as a vital communication link between the lender, the homeowner, and the insurance provider to verify eligibility. Understanding the approval status is essential for timelines, as it dictates whether the bank can proceed with the property transfer while mitigating financial losses for the lien holder through indemnity coverage.

Counteroffer Review Short Sale Bank Status Update Letter

A short sale counteroffer represents a critical stage where the lender proposes new terms, such as a higher purchase price or specific closing conditions. Receiving a bank status update letter is essential for tracking progress and ensuring the lien holder is actively reviewing the file. To avoid foreclosure, parties must respond quickly to these updates, as delays can lead to file closure. Understanding these official communications ensures transparency between the buyer, seller, and bank during complex negotiations to reach a final short sale approval.

Buyer Addendum Short Sale Bank Status Update Letter

The Buyer Addendum Short Sale Bank Status Update Letter is a critical legal document used to maintain transparency during distressed property negotiations. It requires the seller to provide regular, written progress reports regarding lender approval status. This addendum ensures the buyer remains informed about processing timelines and potential delays from the financial institution. By setting defined deadlines for status disclosures, it protects the buyer's interests and allows for informed decision-making regarding the continuation of the contract while waiting for final short sale authorization.

Management Escalation Short Sale Bank Status Update Letter

A management escalation letter is a critical tool to resolve delays in the short sale process. When standard communication fails, this formal request targets high-level bank supervisors to expedite a status update. It must include the loan number, property address, and a clear timeline of previous attempts to reach the servicer. By bypasssing entry-level representatives, you ensure that decision-makers address processing bottlenecks, helping to secure a final approval before potential foreclosure deadlines. Clear documentation of the bank's inaction is essential for a successful escalation outcome.

Final Approval Short Sale Bank Status Update Letter

A Final Approval Short Sale Bank Status Update Letter is the official authorization from a mortgage lender confirming the settlement terms. This document highlights the deficiency waiver, specifying if the bank forgives the remaining loan balance. It outlines the required closing date, approved net proceeds, and specific payouts to lienholders. Receiving this letter is the final milestone in the short sale process, signaling that the bank has legally accepted a payoff for less than the total debt owed to facilitate the property transfer.

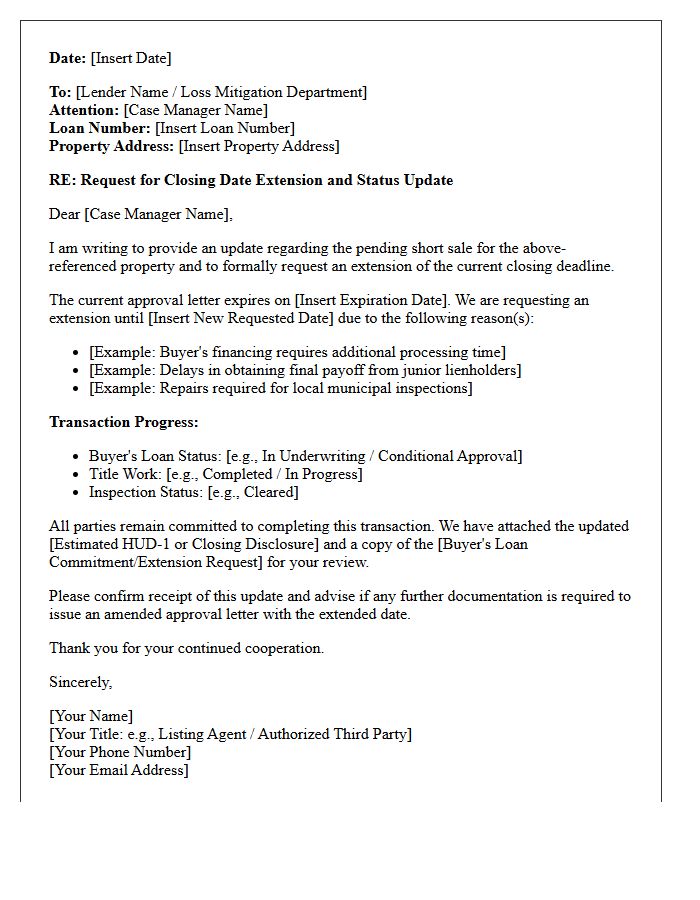

Closing Extension Short Sale Bank Status Update Letter

A Closing Extension Short Sale Bank Status Update Letter is a critical document used to request additional time from a lender to finalize a real estate transaction. It ensures the lien holder remains informed about delays in processing or closing. Timely communication prevents the foreclosure process from resuming prematurely. This letter must clearly state the reasons for the extension, the new projected closing date, and any progress made with the buyer's financing. Maintaining active status with the bank is essential for securing final approval and completing the sale successfully.

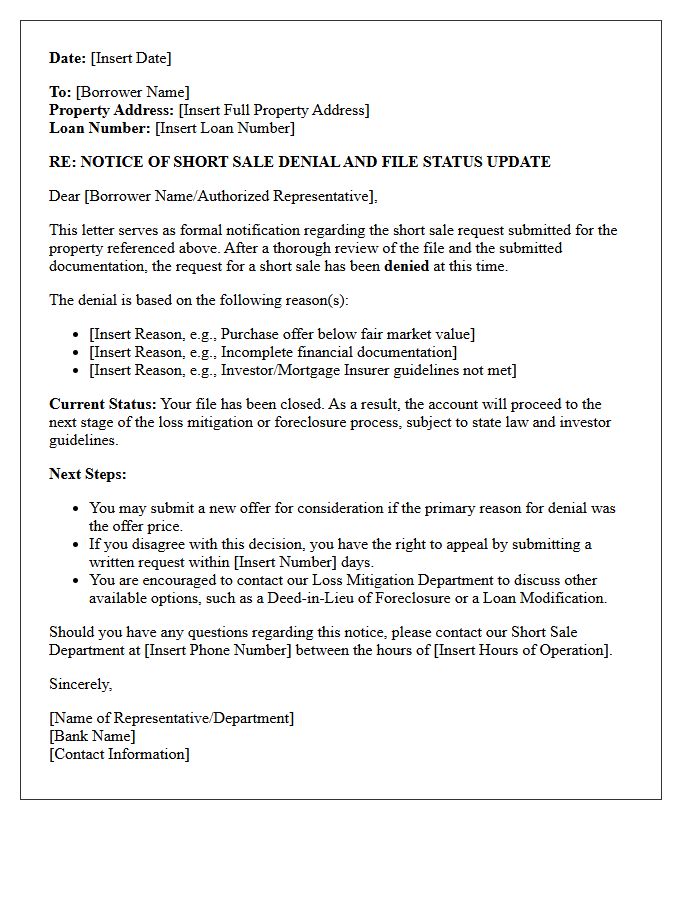

File Denial Short Sale Bank Status Update Letter

A File Denial Short Sale Bank Status Update Letter is a formal notification from a lender rejecting a short sale application. This document is critical because it highlights specific deficiencies, such as missing documentation, an insufficient offer price, or investor disapproval. Receiving this letter indicates that the current proposal failed to meet the bank's mitigation guidelines. Homeowners must act quickly to address the cited issues or file an appeal to prevent the property from moving closer to a foreclosure sale. Constant communication with the servicer is essential to resolve these status updates.

What is a Short Sale Bank Status Update Letter?

A Short Sale Bank Status Update Letter is a formal document sent by a mortgage lender to the homeowner or their agent providing a progress report on the short sale application, including pending documents and current review stages.

How often should I receive a status update from the bank during a short sale?

Most lenders issue a status update letter every 15 to 30 days, or whenever a major milestone is reached, such as the completion of a Broker Price Opinion (BPO) or a file transfer to the mortgage-backed securities investor.

What are the common statuses listed in a short sale update letter?

Common statuses include "Incomplete" (awaiting documents), "Under Review" (the negotiator is evaluating the file), "Valuation Stage" (the bank is determining property value), and "Investor Review" (the final stage before approval).

Why does my short sale status letter say "Incomplete Package"?

An "Incomplete Package" status typically means the bank requires updated financial documents, such as recent pay stubs or bank statements, or that specific signatures are missing from the hardship letter or tax authorization forms.

Can a bank status update letter guarantee short sale approval?

No, a status update letter is not an approval. It is a procedural notification used to track the timeline; final approval is only granted once the lender issues a formal "Short Sale Approval Letter" outlining the terms and deficiency waiver.

Comments