Navigating financial hardship requires understanding your options. This guide provides a detailed Short Sale Versus Foreclosure Comparison to help homeowners evaluate credit impact, deficiency judgments, and future eligibility. Choosing the right path can protect your financial future and provide a fresh start. To simplify your communication with lenders, below are some ready to use template.

Image cover: Short Sale vs. Foreclosure: Comparison Letter Templates and Professional Samples

Letter Samples List

- Distressed Homeowner Short Sale Versus Foreclosure Comparison Letter

- Credit Impact Short Sale Versus Foreclosure Comparison Letter

- Financial Recovery Short Sale Versus Foreclosure Comparison Letter

- Notice Of Default Short Sale Versus Foreclosure Comparison Letter

- Future Homeownership Short Sale Versus Foreclosure Comparison Letter

- Urgent Pre-Foreclosure Short Sale Versus Foreclosure Comparison Letter

- Deficiency Judgment Short Sale Versus Foreclosure Comparison Letter

- Real Estate Agent Introductory Short Sale Versus Foreclosure Comparison Letter

- Investment Property Short Sale Versus Foreclosure Comparison Letter

- Timeline And Process Short Sale Versus Foreclosure Comparison Letter

- Relocation Assistance Short Sale Versus Foreclosure Comparison Letter

- Post-Modification Denial Short Sale Versus Foreclosure Comparison Letter

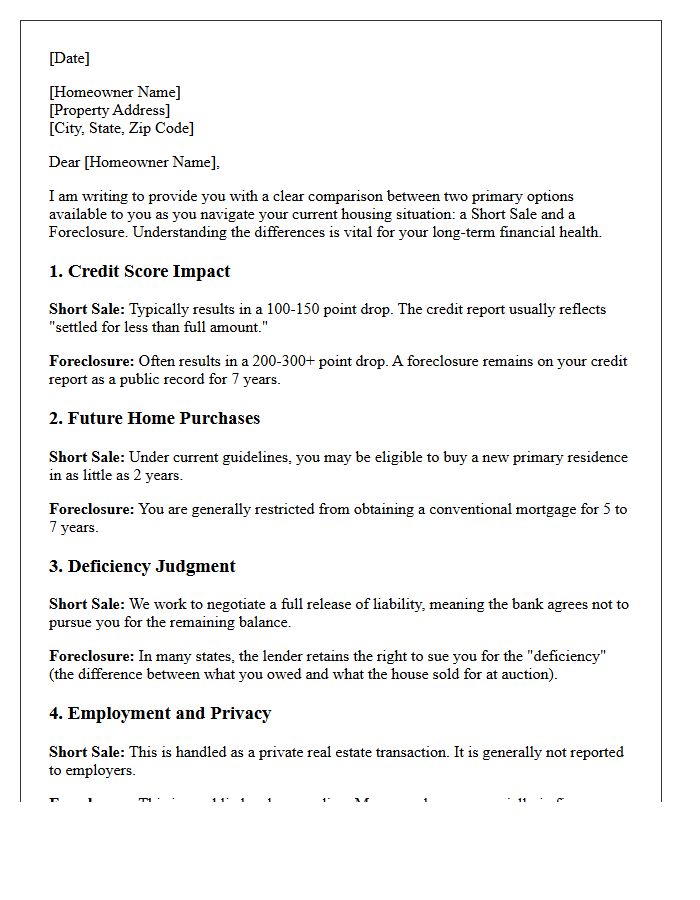

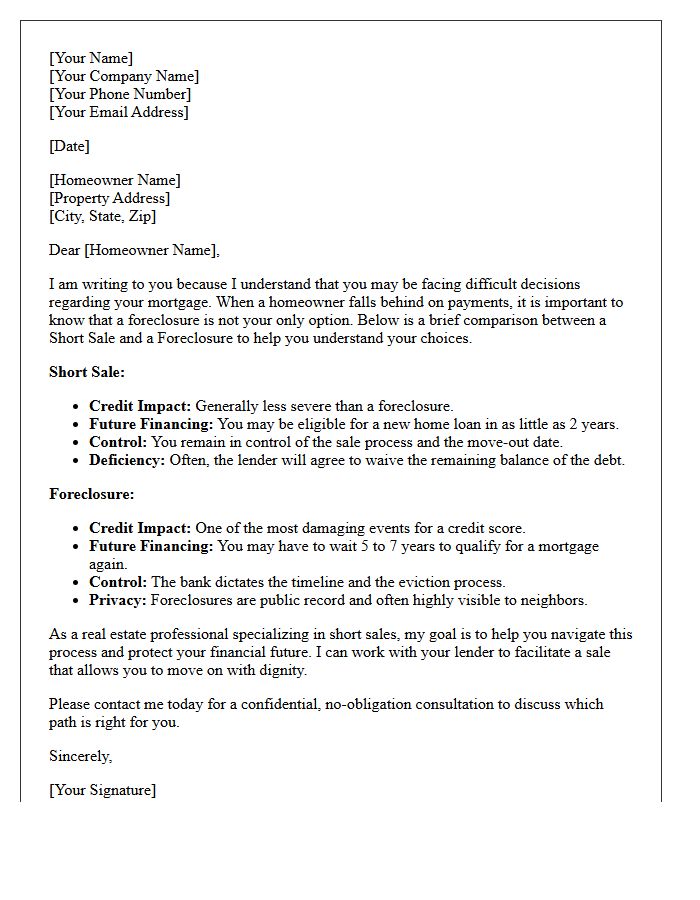

Distressed Homeowner Short Sale Versus Foreclosure Comparison Letter

A comparison letter helps a distressed homeowner evaluate the financial consequences of a short sale versus a foreclosure. It outlines how a short sale may result in a smaller credit score drop and a shorter waiting period for future home loans compared to the long-term damage of a foreclosure. This document is essential for negotiating with lenders to seek a deficiency waiver, potentially forgiving the remaining mortgage balance. Understanding these differences empowers homeowners to choose a path that preserves their financial recovery and future housing stability.

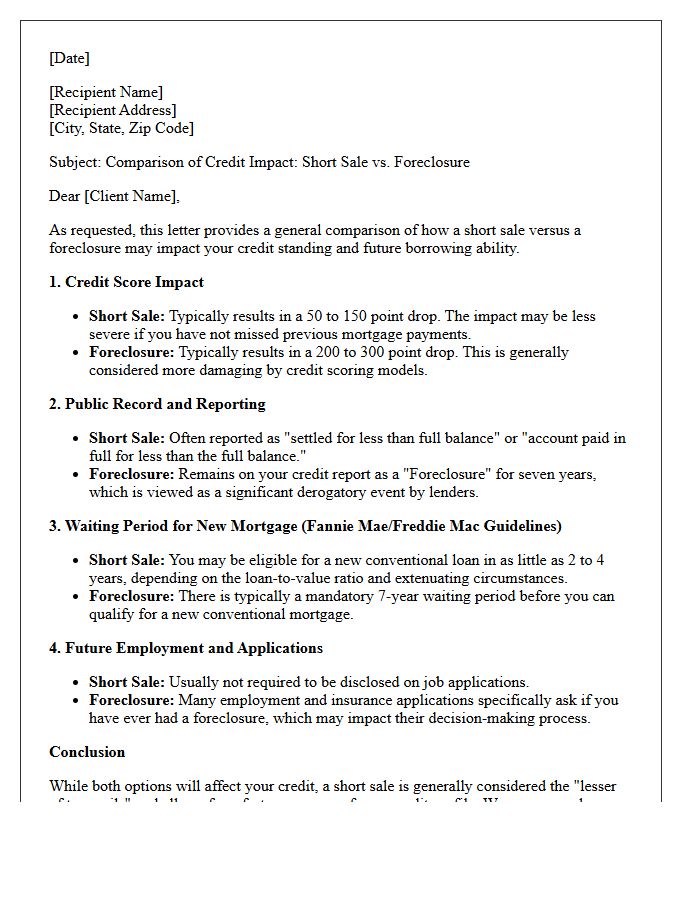

Credit Impact Short Sale Versus Foreclosure Comparison Letter

A credit impact comparison letter evaluates how a short sale versus a foreclosure affects your financial future. While both actions result in a derogatory mark, a short sale typically allows for faster credit recovery, often within two years. Conversely, a foreclosure can lower scores by over 100 points and remains on reports for seven years, severely limiting loan eligibility. This letter provides essential deficiency judgment information and helps homeowners understand which liquidation option minimizes long-term damage to their creditworthiness and future borrowing potential.

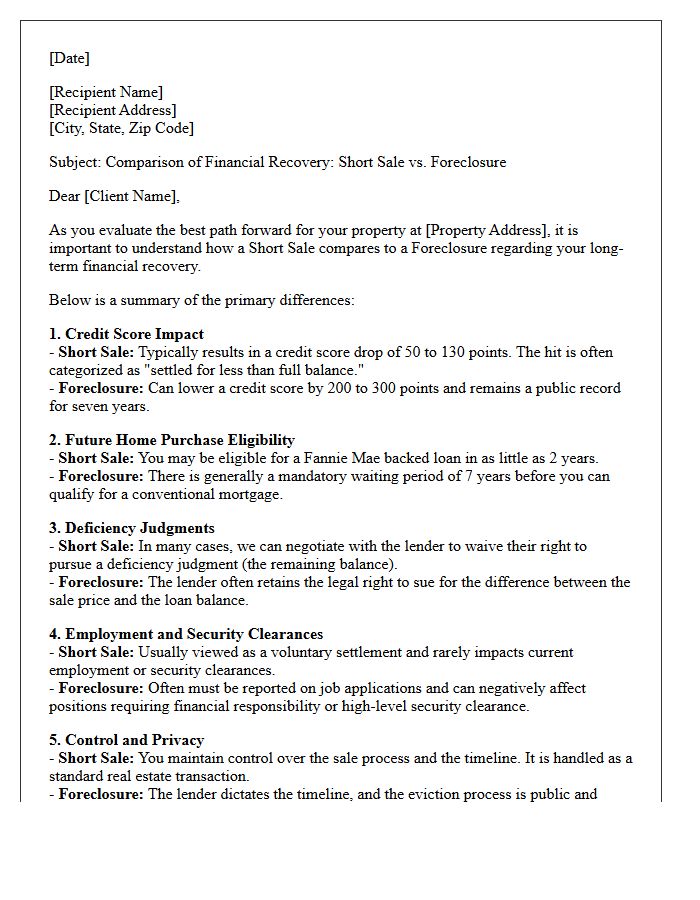

Financial Recovery Short Sale Versus Foreclosure Comparison Letter

A comparison letter clarifies the impact of a short sale versus a foreclosure on your future. While both options resolve delinquent debt, a short sale typically results in less severe credit score damage and a shorter waiting period for new home loans. Foreclosures may lead to deficiency judgments and long-term financial instability. This document provides the essential data needed to make an informed decision, helping homeowners choose the most effective path toward financial recovery and preserving their long-term borrowing power after a property hardship.

Notice Of Default Short Sale Versus Foreclosure Comparison Letter

A Notice of Default marks the formal start of foreclosure, but homeowners can still pursue a short sale to mitigate damage. While a foreclosure stays on credit reports for seven years and often involves an involuntary eviction, a short sale allows for a deficiency waiver and a faster financial recovery. This comparison letter outlines how selling the property for less than the loan balance provides more control and dignity than a public auction. Understanding these options is essential for protecting future borrowing power and avoiding the long-term consequences of a completed foreclosure.

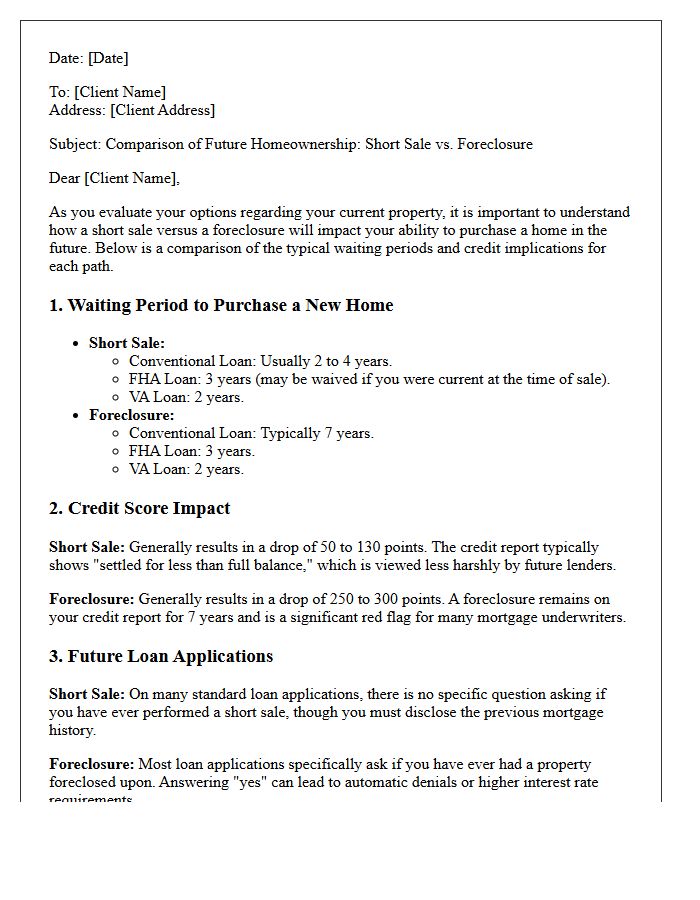

Future Homeownership Short Sale Versus Foreclosure Comparison Letter

A short sale and foreclosure comparison letter is a vital disclosure document for homeowners facing financial distress. It highlights that a short sale typically causes less damage to credit scores compared to a foreclosure. Most importantly, it outlines the waiting period required before qualifying for a future mortgage, often being much shorter for those who settle via short sale. Understanding these timelines helps homeowners strategically plan for future homeownership while minimizing long-term financial consequences and deficiency judgments. Consulting this comparison ensures informed decision-making during the loss mitigation process.

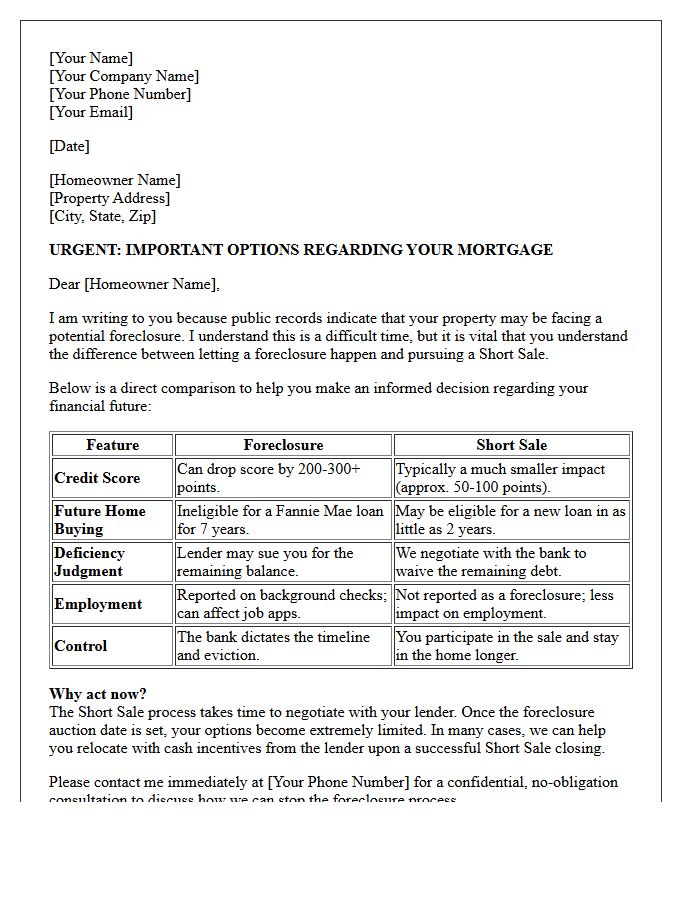

Urgent Pre-Foreclosure Short Sale Versus Foreclosure Comparison Letter

An Urgent Pre-Foreclosure Short Sale Versus Foreclosure Comparison Letter is a critical document used to educate distressed homeowners. It highlights the benefits of a short sale, such as credit score preservation and debt forgiveness, against the long-term damage of a foreclosure. This professional comparison outlines how a proactive sale can prevent deficiency judgments and provide a faster path to future homeownership. By clearly presenting these options, real estate professionals help owners make informed decisions to avoid legal consequences and financial ruin during a housing crisis or mortgage default.

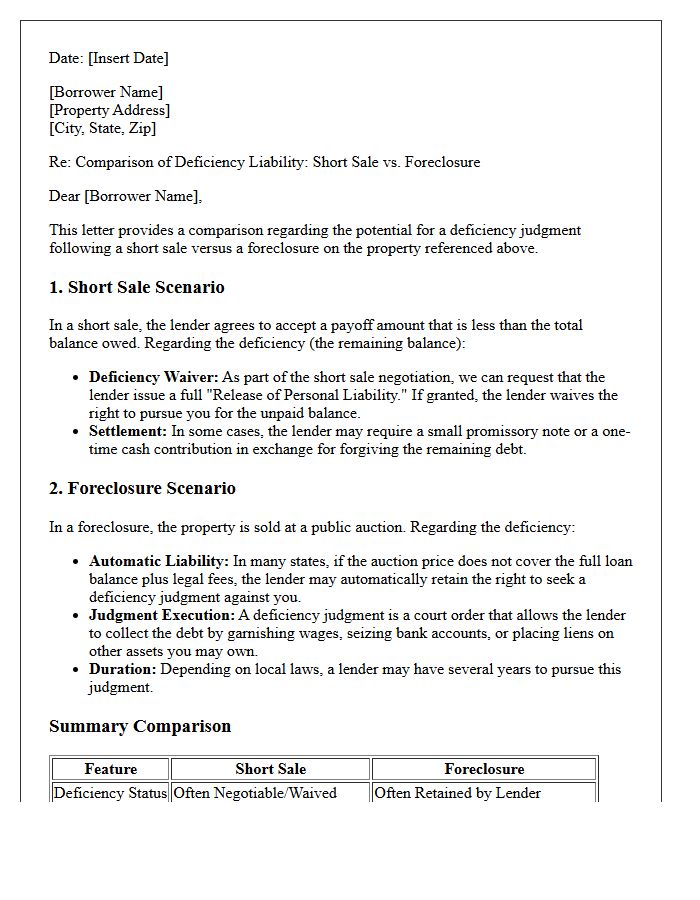

Deficiency Judgment Short Sale Versus Foreclosure Comparison Letter

A comparison letter analyzes the deficiency judgment risks between a short sale and foreclosure. In a short sale, lenders may waive the right to pursue the remaining loan balance, whereas foreclosure often results in an automatic judgment for the shortfall. This document highlights how settlement negotiations can protect personal assets and future earnings. Understanding these legal differences is essential for homeowners to avoid long-term financial liability. Always ensure the final agreement explicitly states that the debt is considered paid in full to prevent future collection efforts by the mortgage lender.

Real Estate Agent Introductory Short Sale Versus Foreclosure Comparison Letter

A short sale versus foreclosure comparison letter is a vital educational tool for real estate agents targeting distressed homeowners. It clearly outlines the financial consequences of each path, highlighting how a short sale can better preserve credit scores compared to the long-term damage of a foreclosure. By providing a side-by-side analysis of deficiency judgments and future loan eligibility, agents establish themselves as knowledgeable experts. This proactive communication builds trust and empathy, encouraging homeowners to seek professional guidance to avoid legal pitfalls while exploring viable alternatives to losing their property to the bank.

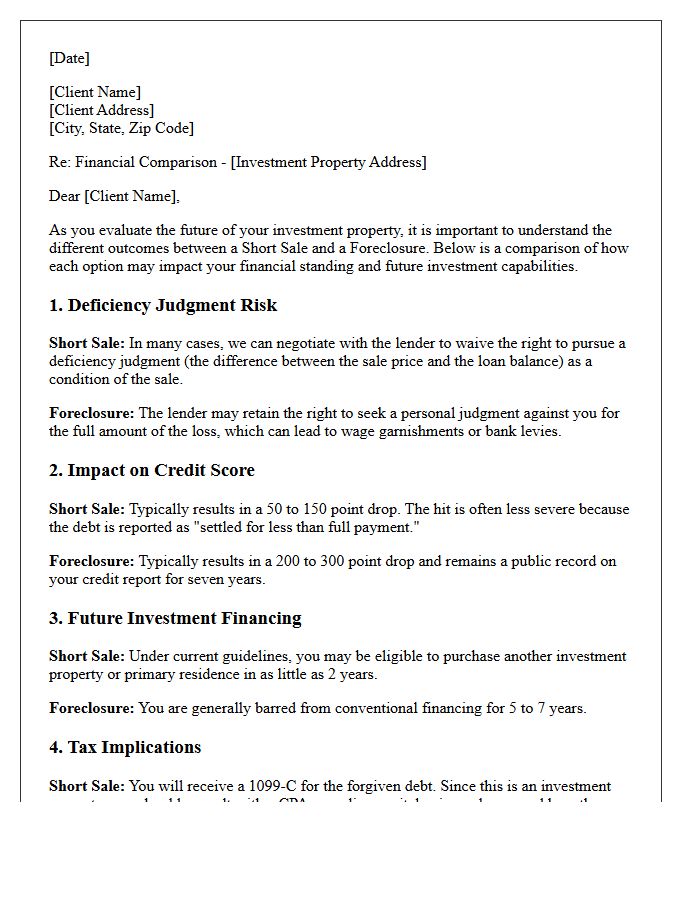

Investment Property Short Sale Versus Foreclosure Comparison Letter

An Investment Property Short Sale Versus Foreclosure Comparison Letter helps owners evaluate liquidation options. A short sale involves selling the property for less than the mortgage balance with lender approval, often preserving credit scores better than a foreclosure. Conversely, foreclosure is a forced legal process leading to property repossession. This letter compares deficiency judgments, tax implications, and future borrowing eligibility. Understanding these differences is essential for minimizing financial liability and protecting long-term investment portfolios when facing distressed real estate scenarios.

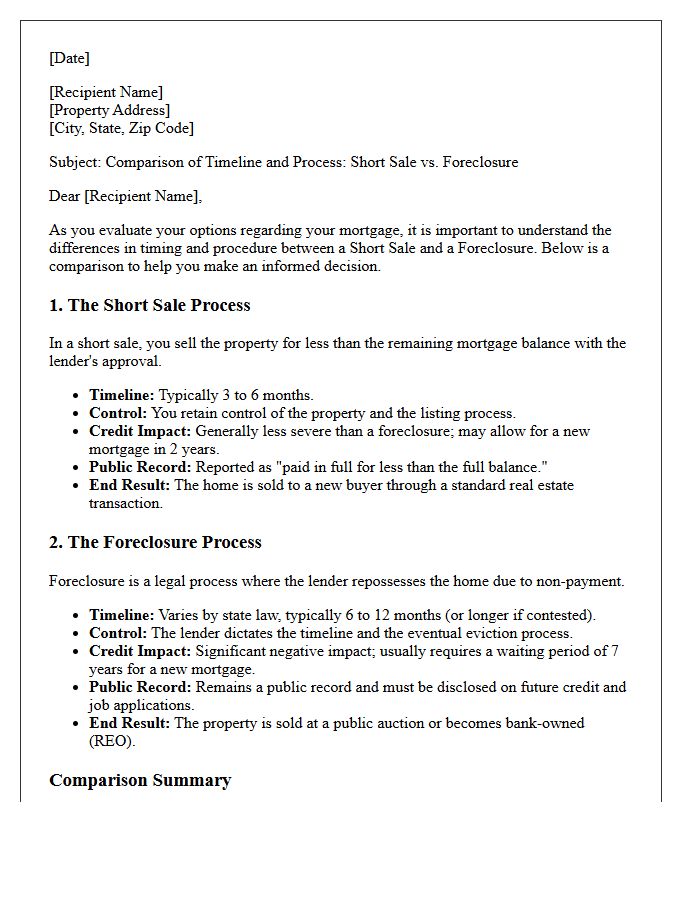

Timeline And Process Short Sale Versus Foreclosure Comparison Letter

A short sale and foreclosure significantly impact your financial future differently. A short sale requires lender approval to sell for less than the mortgage balance, offering a collaborative resolution that often preserves credit scores better. Conversely, foreclosure is a forced legal action where the bank seizes the property, typically resulting in a more severe, long-term credit decline. While short sales involve extensive paperwork and longer negotiation periods, they often allow for faster re-entry into homeownership compared to the mandatory waiting periods following a foreclosure proceedings completion.

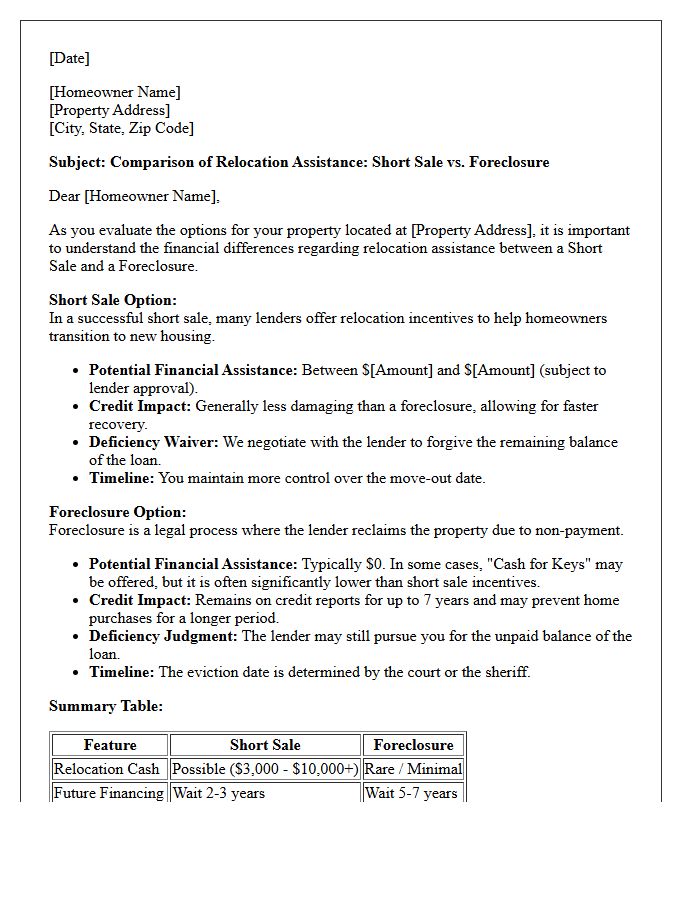

Relocation Assistance Short Sale Versus Foreclosure Comparison Letter

A Relocation Assistance Short Sale Versus Foreclosure Comparison Letter is a critical document for homeowners facing financial distress. It outlines the monetary incentives, often called "cash for keys," available through a short sale compared to the total loss of equity in a foreclosure. This letter helps sellers understand how relocation benefits can facilitate a smoother transition to new housing. By comparing both paths, owners can see the long-term advantages of avoiding foreclosure, protecting their credit score, and securing essential moving funds to stabilize their future financial situation effectively.

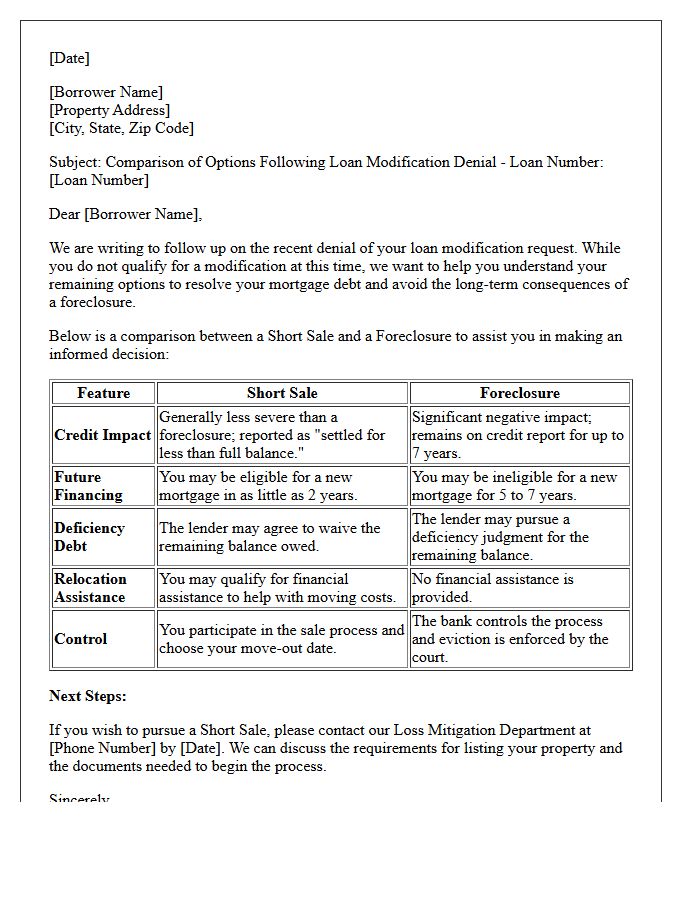

Post-Modification Denial Short Sale Versus Foreclosure Comparison Letter

A Post-Modification Denial Short Sale Versus Foreclosure Comparison Letter is a critical disclosure document sent to homeowners after a loan modification request is rejected. It provides a side-by-side analysis of deficiency judgment risks, credit score impacts, and future borrowing eligibility. This comparison helps borrowers understand why a short sale is often a more favorable liquidation alternative than a standard foreclosure. By outlining specific financial consequences, the letter empowers homeowners to make informed decisions to mitigate long-term economic damage during financial distress.

What is the primary difference between a short sale and a foreclosure?

In a short sale, the homeowner sells the property for less than the remaining mortgage balance with the lender's approval, whereas a foreclosure is a legal process where the lender seizes the property after the homeowner fails to make payments.

How does a short sale affect my credit score compared to a foreclosure?

While both events negatively impact credit, a short sale typically results in a smaller point drop (approximately 50 to 130 points) and recovers faster, whereas a foreclosure can lower a score by 200 points or more and remains a major derogatory mark for seven years.

Which option allows me to buy a new home sooner?

A short sale generally allows you to apply for a conventional mortgage in as little as 2 to 4 years, while a foreclosure typically requires a waiting period of 7 years before you are eligible for a new conventional loan.

Will I still owe money to the bank after a short sale or foreclosure?

In a short sale, you can often negotiate a "deficiency waiver" to forgive the remaining debt; however, in a foreclosure, the lender may pursue a deficiency judgment to collect the balance unless prohibited by state law or specific agreements.

How do the tax implications differ between a short sale and a foreclosure?

Both options may result in taxable income from debt cancellation; however, homeowners may qualify for exclusions under the Mortgage Forgiveness Debt Relief Act or insolvency rules, making it essential to consult a tax professional for both scenarios.

Comments