Protecting your business requires a clear General Liability Additional Insured Endorsement Confirmation. This critical document extends coverage to third parties, ensuring contractual compliance and mitigating financial risk during collaborative projects. Verifying these endorsements protects all stakeholders from unforeseen legal claims and liabilities. To simplify your documentation process, below are some ready to use template options to help you get started.

Image cover: Mastering the Additional Insured Endorsement: Practical Samples and Professional Templates

Letter Samples List

- General Liability Additional Insured Endorsement Confirmation Letter

- Contractor General Liability Additional Insured Confirmation Letter

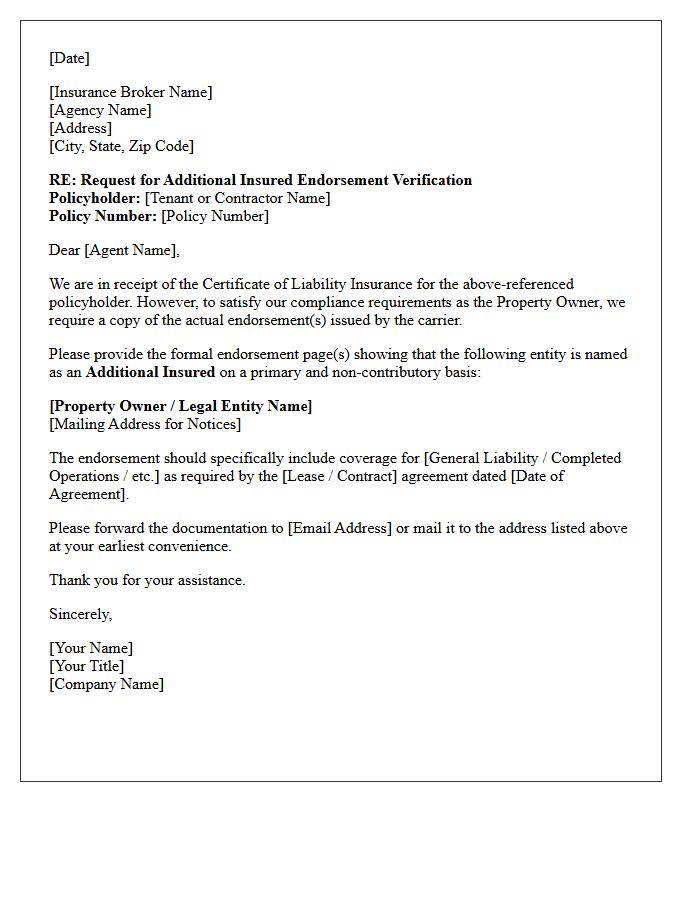

- Property Owner Additional Insured Endorsement Verification Letter

- Blanket Additional Insured Endorsement Confirmation Letter

- Vendor General Liability Additional Insured Approval Letter

- Certificate Of Insurance And Additional Insured Endorsement Letter

- Ongoing And Completed Operations Additional Insured Letter

- Special Event Additional Insured Liability Confirmation Letter

- Primary And Non-Contributory Additional Insured Endorsement Letter

- Additional Insured And Waiver Of Subrogation Confirmation Letter

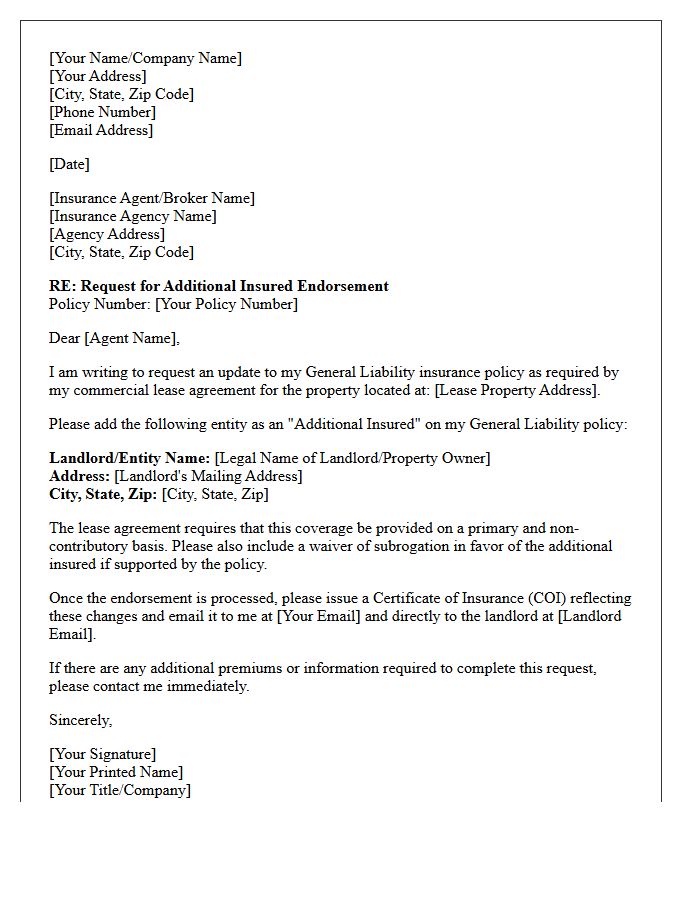

- Commercial Lease General Liability Additional Insured Letter

- Specific Project Additional Insured Endorsement Notification Letter

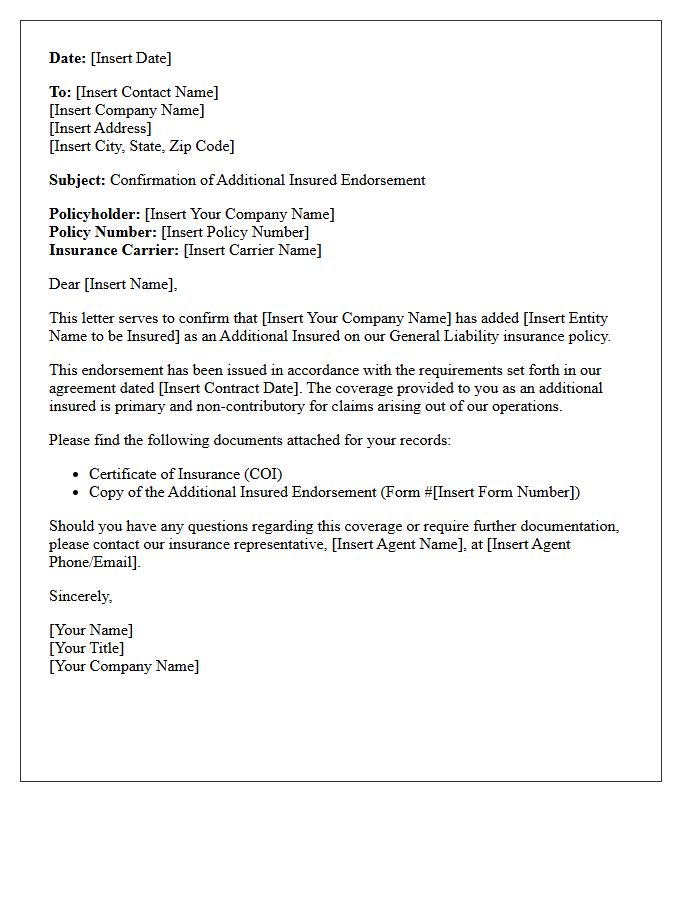

General Liability Additional Insured Endorsement Confirmation Letter

A General Liability Additional Insured Endorsement Confirmation Letter serves as official verification that a third party is protected under a policyholder's coverage. This document validates that an endorsement has been formally added, extending liability protection to entities like landlords or contractors. It is more definitive than a standard Certificate of Insurance because it confirms the policy has been legally modified. Businesses use this to manage risk transfer and ensure compliance with contractual insurance requirements, providing proof that the insurer will defend the additional party during a claim.

Contractor General Liability Additional Insured Confirmation Letter

A Contractor General Liability Additional Insured Confirmation Letter provides official proof that a specific entity is added to a policyholder's coverage. This document is essential for risk management, ensuring that the Additional Insured is protected against third-party claims arising from the contractor's operations. It verifies that coverage extends to legal defense costs and potential damages. Always confirm the letter includes the correct policy numbers and effective dates to guarantee indemnification and maintain project compliance under contractual agreements.

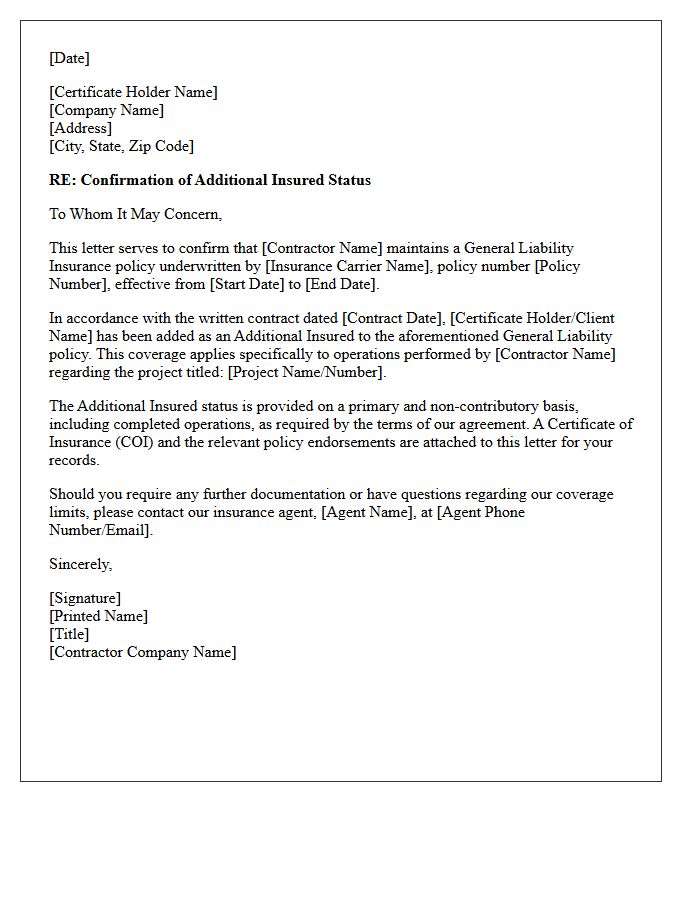

Property Owner Additional Insured Endorsement Verification Letter

A Property Owner Additional Insured Endorsement Verification Letter is a critical document confirming that a landlord or owner is officially protected under a tenant's liability insurance policy. It serves as formal proof of coverage, ensuring the owner is defended against third-party claims arising from the tenant's operations. Verifying this endorsement is essential for risk mitigation, as it guarantees the policy has been correctly amended. Without this specific verification, owners may face significant financial exposure, making it a vital requirement in modern commercial real estate lease compliance.

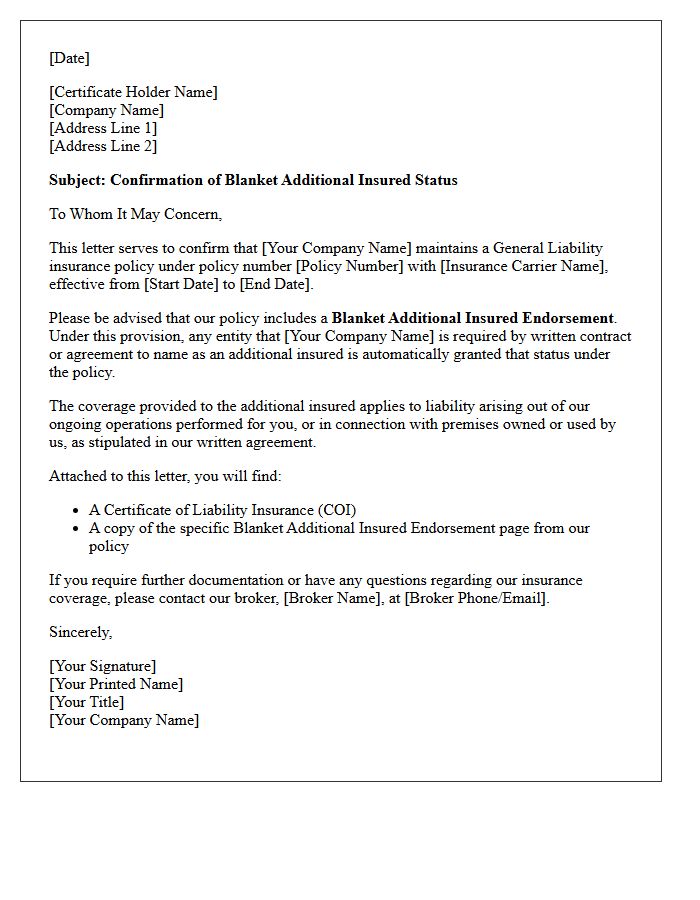

Blanket Additional Insured Endorsement Confirmation Letter

A Blanket Additional Insured Endorsement Confirmation Letter serves as formal proof that a policyholder's coverage automatically extends to third parties required by written contract. Unlike specific endorsements, this blanket provision streamlines compliance by eliminating the need to name each entity individually on the policy. It is crucial for verifying that vicarious liability protection is active, ensuring that partners or clients are defended under the insured's primary program. Always confirm the letter references the specific endorsement form number to guarantee the scope of coverage meets contractual obligations.

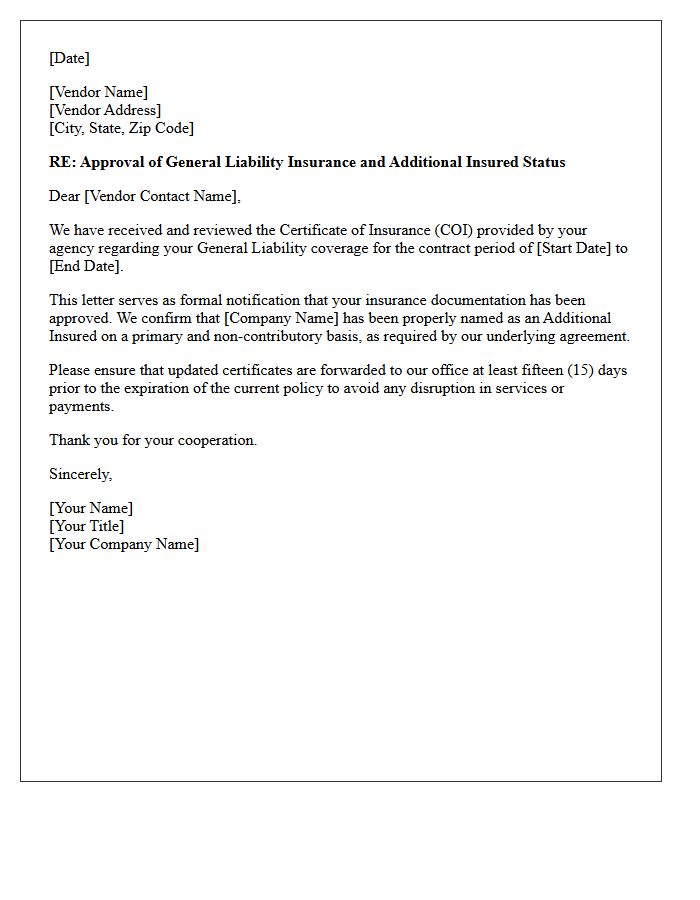

Vendor General Liability Additional Insured Approval Letter

A Vendor General Liability Additional Insured Approval Letter is a formal document confirming that a third-party vendor has successfully added your business to their insurance policy. This letter validates that vicarious liability coverage is active, protecting your company from claims arising out of the vendor's operations. It serves as essential compliance verification, ensuring that the specific endorsement meets your contractual requirements before work begins. Always verify the policy limits and expiration dates listed within the letter to maintain continuous risk mitigation and legal protection.

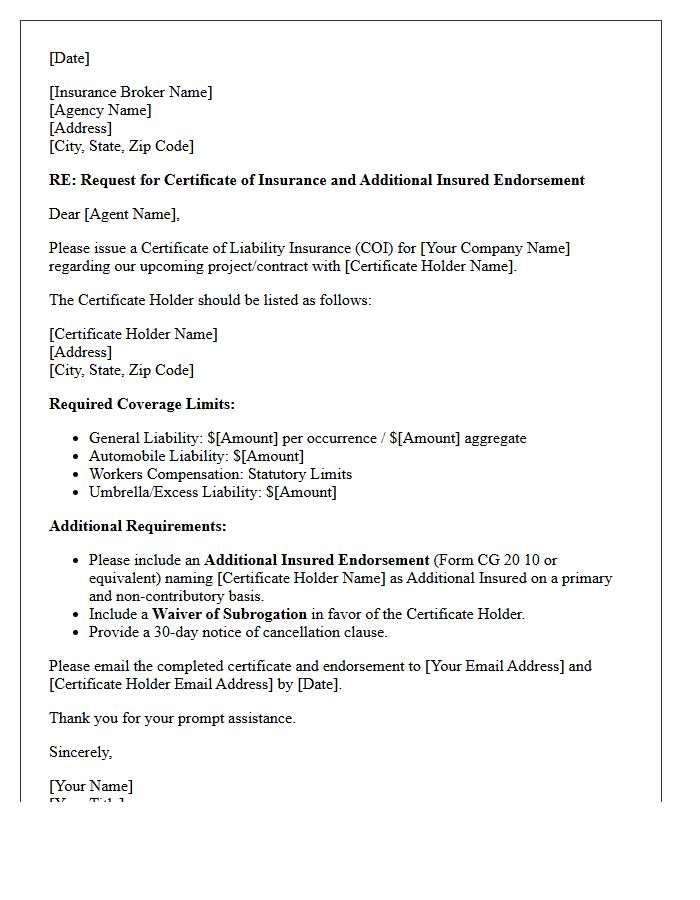

Certificate Of Insurance And Additional Insured Endorsement Letter

A Certificate of Insurance (COI) acts as a snapshot of active coverage, but it does not grant legal rights to third parties. To gain actual protection under another entity's policy, you must obtain an Additional Insured Endorsement. This formal amendment updates the insurance contract, ensuring your business is covered for vicarious liability arising from the policyholder's operations. Always verify that the endorsement specifically names your organization or includes a blanket provision to ensure the transfer of risk is legally enforceable and valid during a claim.

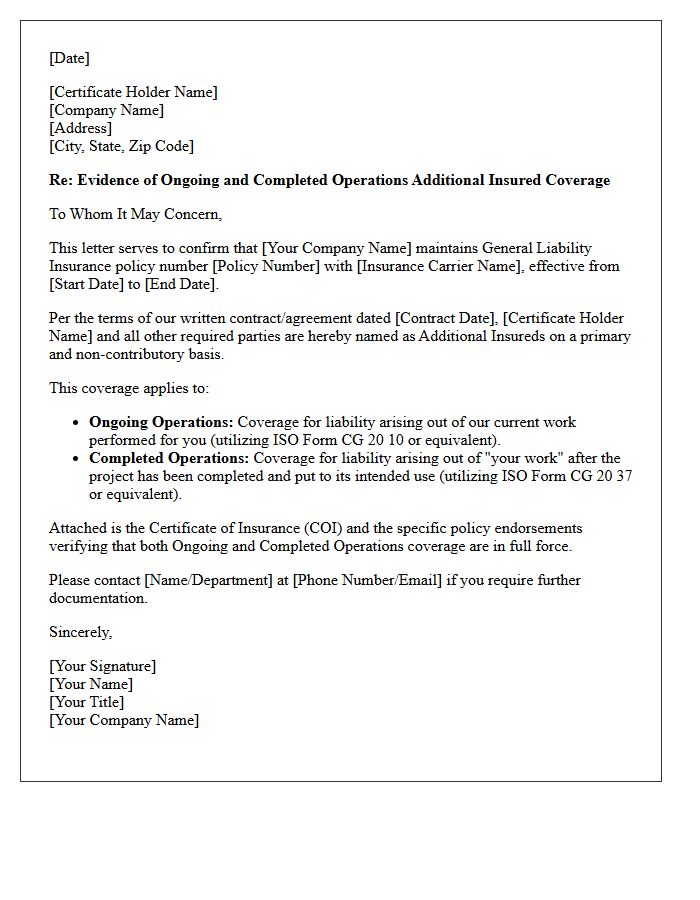

Ongoing And Completed Operations Additional Insured Letter

An Ongoing and Completed Operations Additional Insured endorsement is vital for contractors to manage liability. While standard certificates often only cover active work, this specific coverage extends protection to the additional insured for claims arising after a project is finished. It protects third parties from property damage or bodily injury resulting from past workmanship. Without the completed operations provision, coverage typically expires once the job is finalized, leaving parties exposed to long-term legal risks. Always verify that both CG 20 10 and CG 20 37 forms (or equivalents) are present for comprehensive protection.

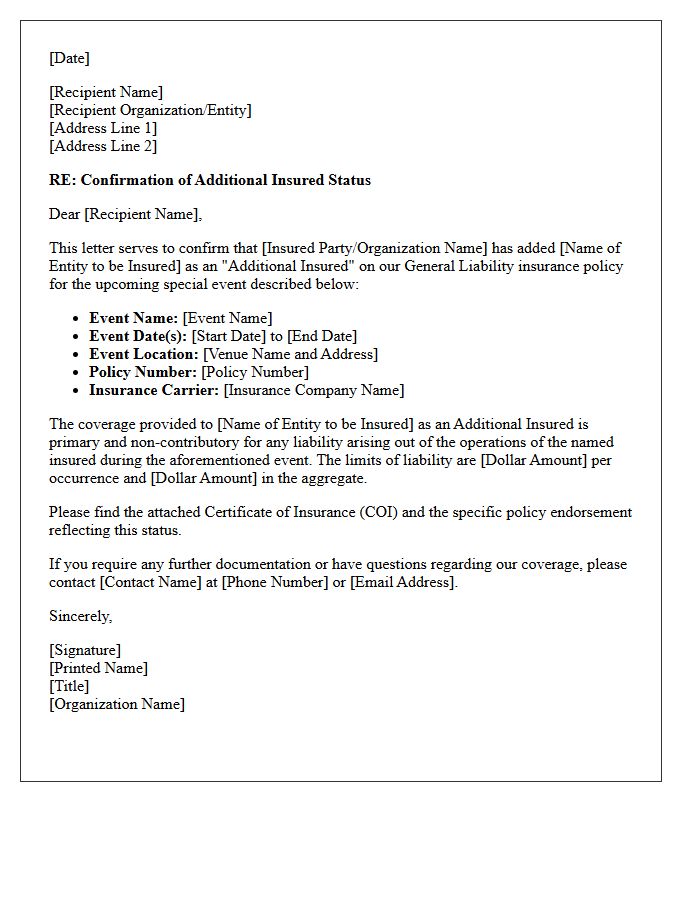

Special Event Additional Insured Liability Confirmation Letter

A Special Event Additional Insured Liability Confirmation Letter is a legal certificate verifying that a specific entity is protected under your insurance policy for a one-time occasion. This document is essential because it ensures the additional insured party is covered against claims arising from your event activities. It serves as official proof of vicarious liability protection, confirming that coverage limits meet contractual requirements. Always verify that the event dates, coverage amounts, and entity names are accurately listed to prevent financial risk or venue access issues.

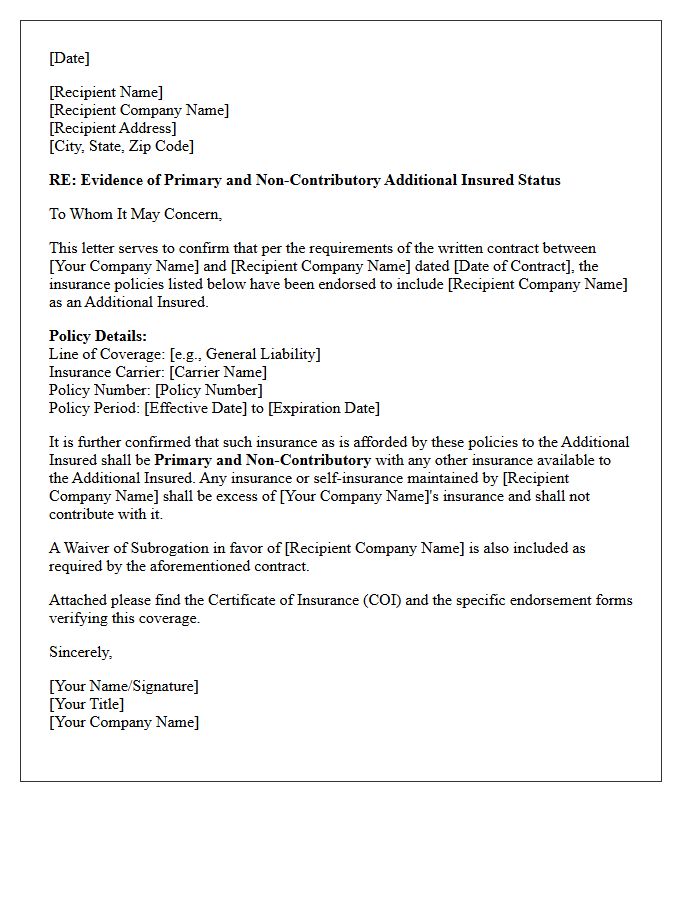

Primary And Non-Contributory Additional Insured Endorsement Letter

A Primary and Non-Contributory endorsement is a critical insurance provision that determines the order of payment during a claim. It ensures the additional insured's policy remains protected, forcing the policyholder's insurance to pay first without seeking contribution from other available coverage. This legal protection is essential in commercial contracts to shift liability risks away from the hiring entity. By securing this letter, businesses verify that their own insurance limits stay intact while the primary policy handles indemnification and defense costs for covered losses arising from the contracted work.

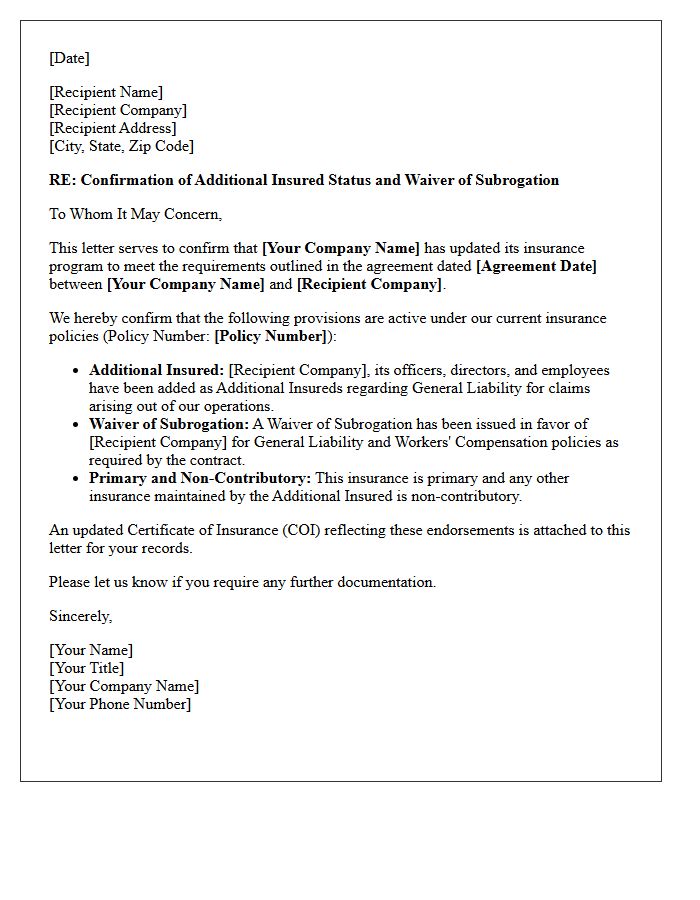

Additional Insured And Waiver Of Subrogation Confirmation Letter

An Additional Insured and Waiver of Subrogation Confirmation Letter serves as formal proof that a policyholder's insurance coverage extends to a third party. The Additional Insured status grants the beneficiary direct protection under the policy, while the Waiver of Subrogation prevents the insurer from seeking recovery costs from that party after paying a claim. This document is essential for contractual compliance, ensuring risk is properly transferred and legal liabilities are minimized during business partnerships or construction projects. It confirms that specific endorsements are active and legally binding.

Commercial Lease General Liability Additional Insured Letter

A Commercial Lease General Liability Additional Insured Letter verifies that a tenant has extended their insurance coverage to protect the landlord. It confirms the Additional Insured endorsement, ensuring the property owner is shielded from third-party claims arising from the tenant's operations. This document is a critical compliance requirement that validates specific policy limits and coverage dates. Without this formal confirmation, landlords face increased financial risk. Always ensure the letter accurately reflects the indemnification clauses specified within your lease agreement to maintain full legal and financial protection.

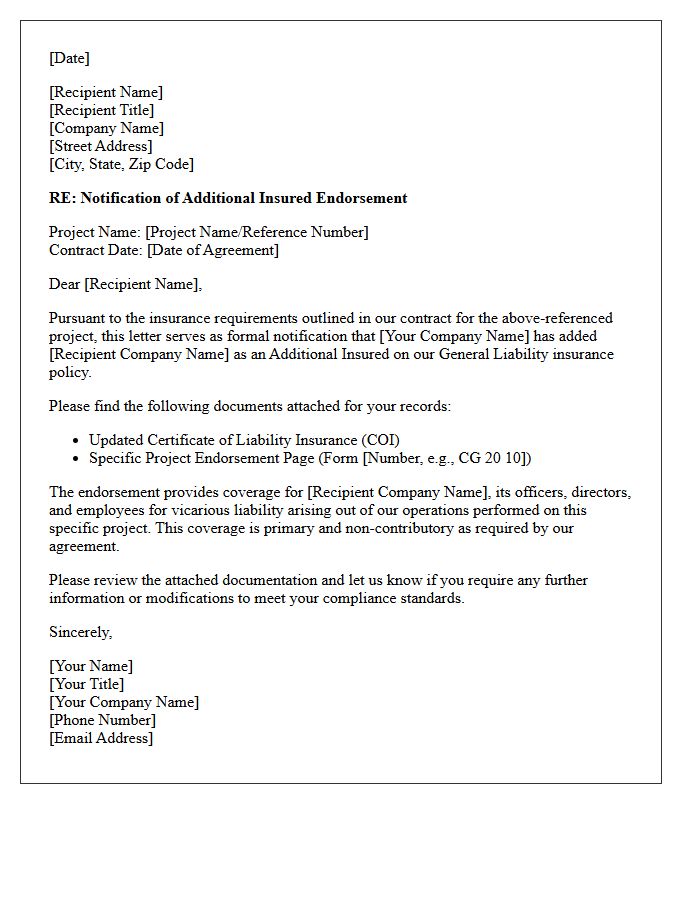

Specific Project Additional Insured Endorsement Notification Letter

A Specific Project Additional Insured Endorsement Notification Letter serves as formal proof that a third party is granted liability protection under a lead policy for a defined job site. Unlike blanket coverage, this document confirms that the additional insured status applies exclusively to the designated contract. It is crucial for verifying compliance with insurance requirements, ensuring that specific project risks are properly mitigated. Always verify that the endorsement language matches the contractual obligations to prevent coverage gaps during potential litigation or claims arising from project operations.

What is a General Liability Additional Insured Endorsement?

A General Liability Additional Insured Endorsement is a policy amendment that extends liability coverage to a third party, such as a landlord or client, protecting them under the policyholder's insurance for specific claims arising out of the policyholder's operations.

How do I obtain confirmation of an Additional Insured Endorsement?

Confirmation is typically obtained by requesting a Certificate of Insurance (COI) from the insurance provider that specifically lists the third party as an "Additional Insured" and includes the corresponding endorsement form number, such as CG 20 10 or CG 20 37.

What is the difference between a Certificate of Insurance and an Endorsement?

A Certificate of Insurance is a high-level summary of coverage used for informational purposes, whereas an endorsement is a legal change to the insurance contract that officially adds the third party to the policy's coverage protections.

Does an Additional Insured Endorsement provide primary and non-contributory coverage?

Not automatically; for an endorsement to be primary and non-contributory, specific language must be included in the endorsement or via a separate "Primary and Non-Contributory" rider to ensure the policyholder's insurance pays first before the additional insured's own policy.

Why is a "Blanket" Additional Insured Endorsement used for confirmation?

A Blanket Additional Insured Endorsement is used to automatically provide coverage to any entity the policyholder is contractually required to insure, simplifying the confirmation process by removing the need to issue individual endorsements for every new contract or project.

Comments