A Hired and Non-Owned Auto Endorsement Confirmation Letter validates that your business insurance covers vehicles you lease or employee-owned cars used for work tasks. This document is essential for proving liability protection and meeting contractual requirements with clients. It ensures your company is shielded from unforeseen vehicular risks. To simplify your documentation process, below are some ready to use template.

Image cover: Hired and Non-Owned Auto (HNOA) Endorsement: Confirmation Letter Templates and Professional Samples

Letter Samples List

- Standard Hired and Non-Owned Auto Endorsement Confirmation Letter

- Commercial Auto Policy Hired and Non-Owned Auto Endorsement Confirmation Letter

- General Liability Hired and Non-Owned Auto Endorsement Confirmation Letter

- Business Owner Policy Hired and Non-Owned Auto Endorsement Confirmation Letter

- Mid-Term Addition Hired and Non-Owned Auto Endorsement Confirmation Letter

- Contractor Liability Hired and Non-Owned Auto Endorsement Confirmation Letter

- Delivery Operations Hired and Non-Owned Auto Endorsement Confirmation Letter

- Corporate Fleet Hired and Non-Owned Auto Endorsement Confirmation Letter

- Small Business Hired and Non-Owned Auto Endorsement Confirmation Letter

- Policy Renewal Hired and Non-Owned Auto Endorsement Confirmation Letter

- Non-Profit Organization Hired and Non-Owned Auto Endorsement Confirmation Letter

- Employee Transit Hired and Non-Owned Auto Endorsement Confirmation Letter

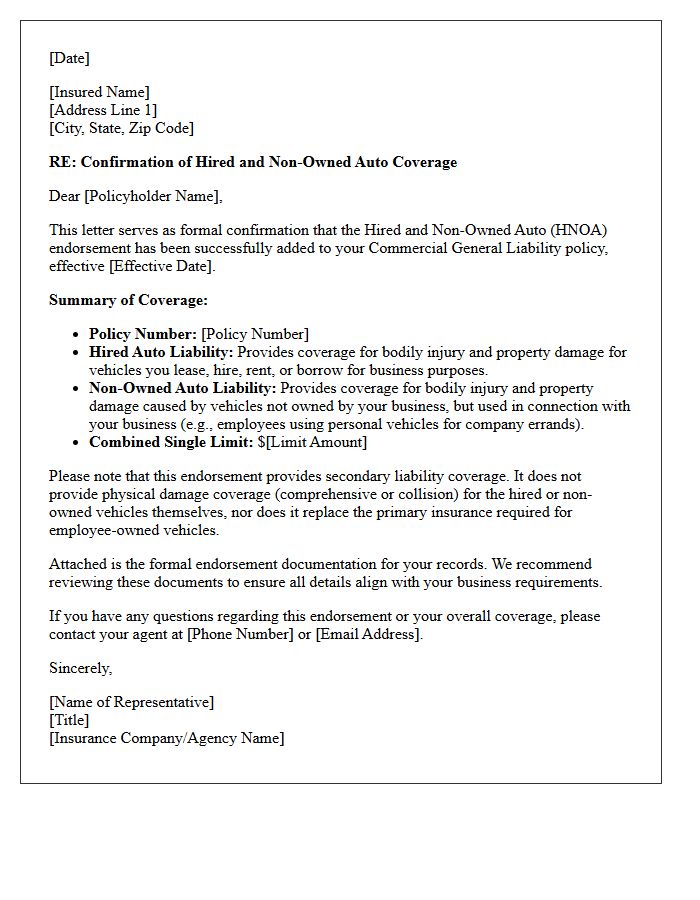

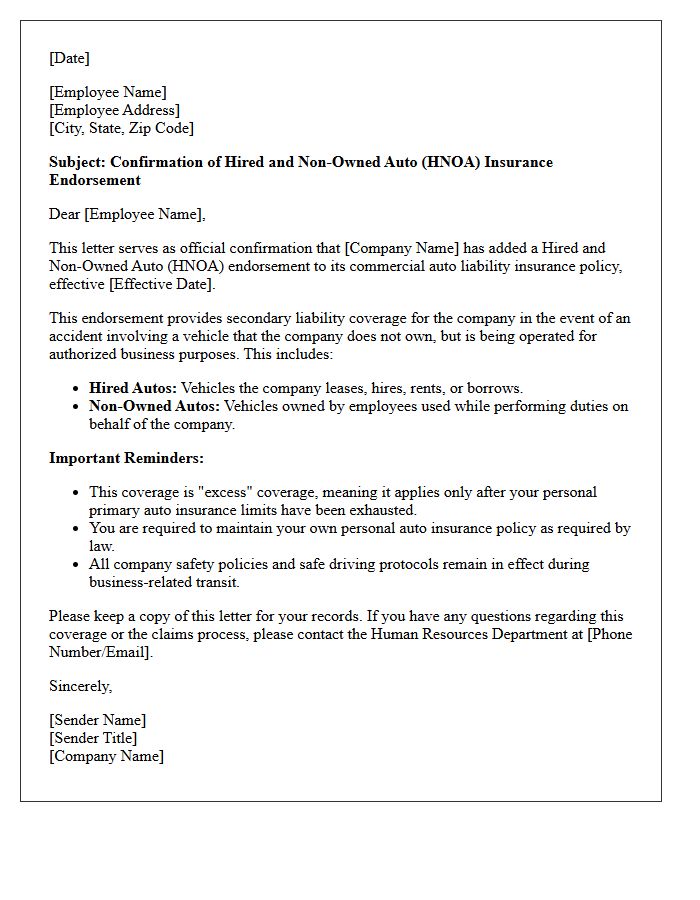

Standard Hired and Non-Owned Auto Endorsement Confirmation Letter

A Standard Hired and Non-Owned Auto Endorsement Confirmation Letter serves as official proof that your commercial auto policy covers vehicles used for business purposes that the company does not own. This essential document verifies liability protection for rented vehicles or employee-owned cars driven on behalf of the organization. It ensures that the business is shielded from financial loss during accidents, filling critical gaps in standard coverage. Providing this letter to clients or partners confirms that your vicarious liability is properly managed and that the enterprise maintains comprehensive professional standards.

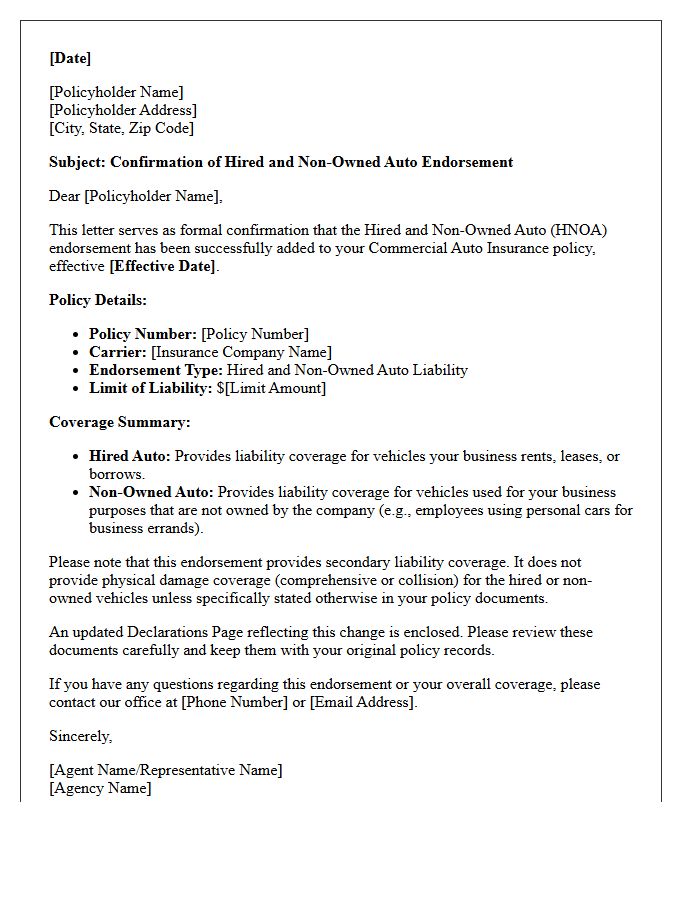

Commercial Auto Policy Hired and Non-Owned Auto Endorsement Confirmation Letter

A Hired and Non-Owned Auto (HNOA) endorsement confirmation letter serves as formal proof that your commercial policy covers vehicles not owned by the business. This includes cars rented for professional use or personal vehicles driven by employees for work tasks. This document is essential for liability protection, ensuring the company is shielded against third-party claims during business-related travel. Clients and contractors often require this letter to verify that the business maintains adequate insurance coverage for off-lease transportation risks, filling critical gaps in standard commercial auto policies.

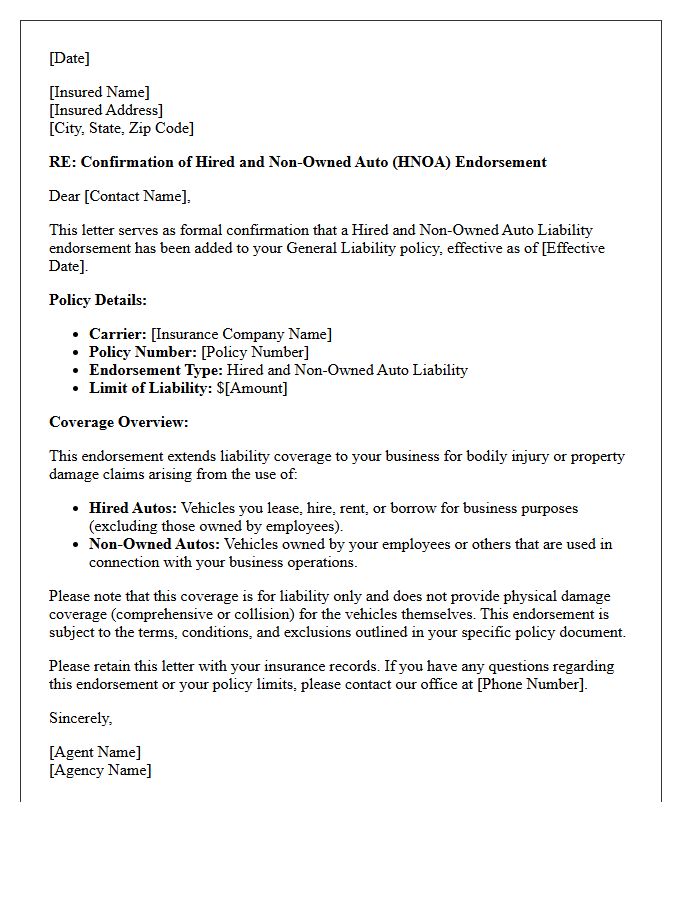

General Liability Hired and Non-Owned Auto Endorsement Confirmation Letter

A General Liability Hired and Non-Owned Auto Endorsement Confirmation Letter serves as official proof that your business insurance policy extends liability coverage to vehicles not owned by the company. This includes rented cars or personal vehicles driven by employees for work purposes. It confirms that the insurer will cover bodily injury or property damage claims resulting from accidents during business operations. This document is essential for contractual compliance, providing peace of mind to clients and partners that secondary liability risks are properly managed and insured.

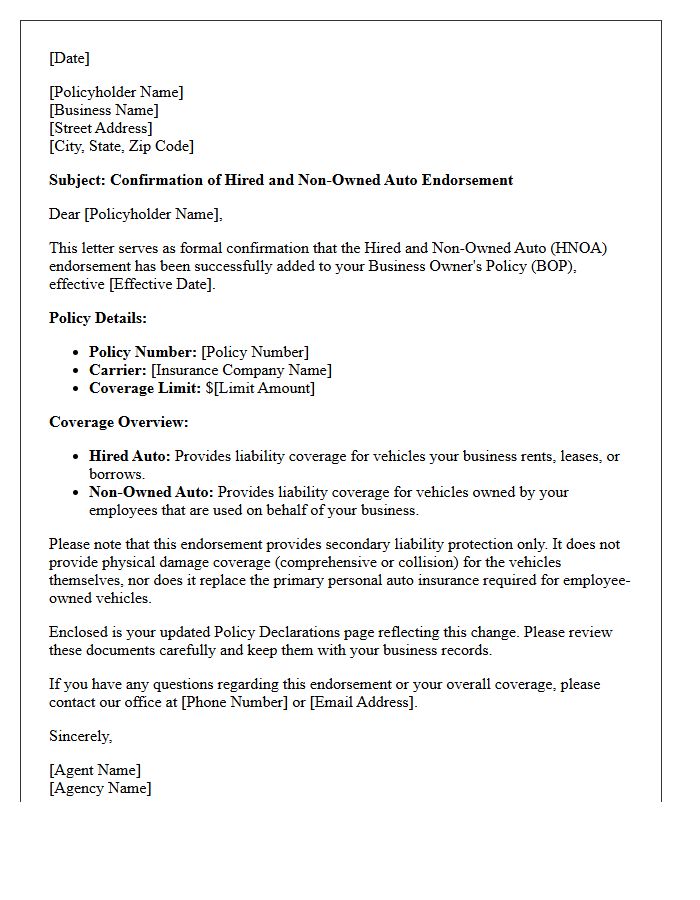

Business Owner Policy Hired and Non-Owned Auto Endorsement Confirmation Letter

A Business Owner Policy (BOP) Hired and Non-Owned Auto Endorsement Confirmation Letter serves as official proof that your commercial insurance extends liability protection to vehicles not owned by the company. This endorsement is essential when employees use personal cars for work or when the business rents vehicles. It confirms that the insurer provides secondary coverage for third-party bodily injury and property damage claims. Having this confirmation letter helps satisfy contractual requirements and ensures the business is protected against vicarious liability during professional operations.

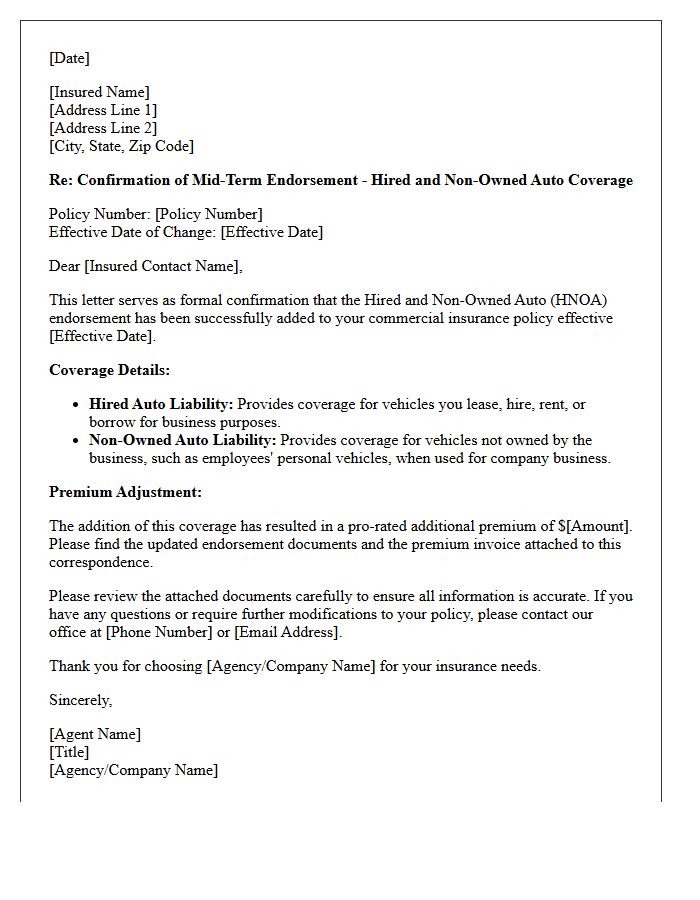

Mid-Term Addition Hired and Non-Owned Auto Endorsement Confirmation Letter

A Mid-Term Addition Hired and Non-Owned Auto Endorsement Confirmation Letter officially validates that your commercial policy now includes liability protection for vehicles used for business but not owned by the company. This endorsement is essential for covering employees driving personal cars or rented vehicles for work-related tasks. Receiving this letter confirms that the liability coverage is active mid-policy, ensuring immediate protection against third-party claims and maintaining your business's compliance with contractual insurance requirements and risk management standards.

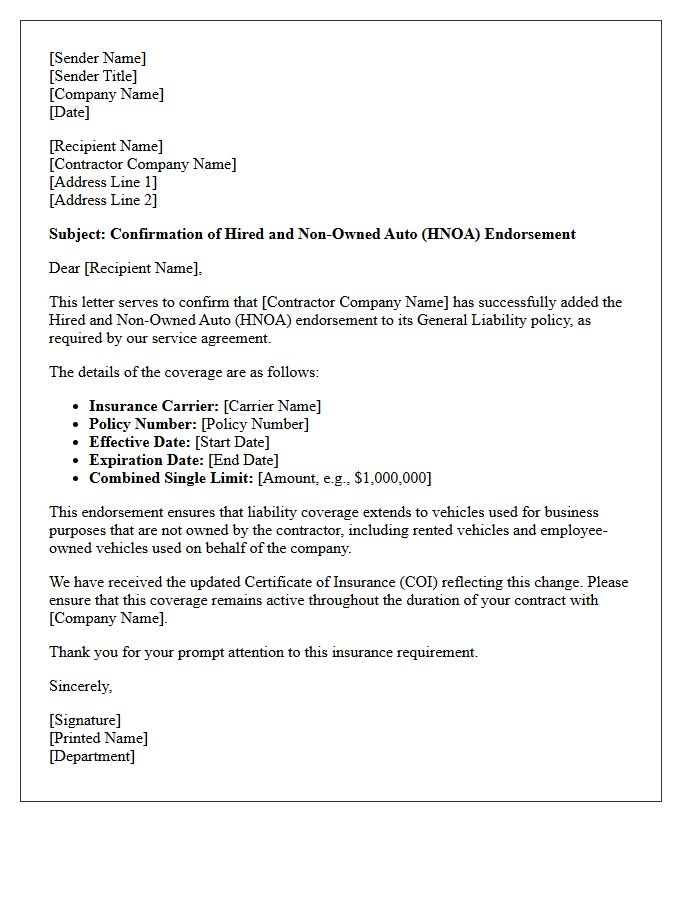

Contractor Liability Hired and Non-Owned Auto Endorsement Confirmation Letter

A Contractor Liability Hired and Non-Owned Auto (HNOA) Endorsement Confirmation Letter provides formal proof that vicarious liability coverage is active. This document verifies that the contractor's policy protects against lawsuits arising from accidents involving rented vehicles or personal cars used for business purposes. It ensures the hiring party is shielded from financial risks if a contractor or employee causes an accident while performing work-related tasks. Verifying this certificate of insurance is essential for risk management and contract compliance, ensuring secondary coverage is in place for non-company owned vehicles.

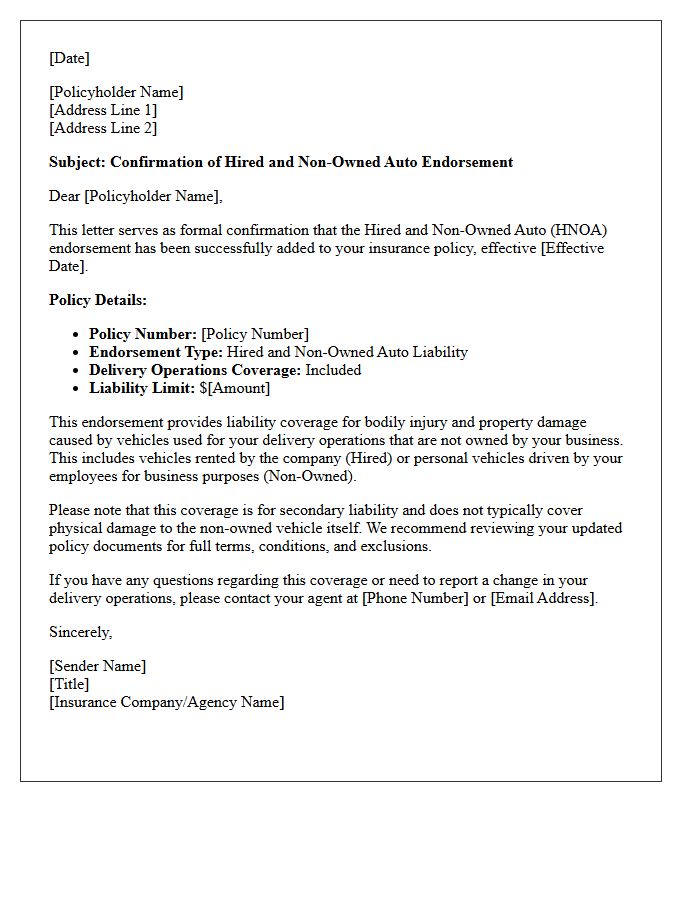

Delivery Operations Hired and Non-Owned Auto Endorsement Confirmation Letter

A Delivery Operations Hired and Non-Owned Auto Endorsement Confirmation Letter validates that a business carries essential liability protection for vehicles used for work but not owned by the company. This document is critical for independent contractors and delivery platforms to verify that hired and non-owned auto (HNOA) coverage is active. It ensures financial protection against third-party bodily injury or property damage claims arising during professional delivery tasks, filling the gap where personal auto policies typically exclude commercial use. Maintaining this formal confirmation is vital for legal compliance and operational risk management.

Corporate Fleet Hired and Non-Owned Auto Endorsement Confirmation Letter

A Corporate Fleet Hired and Non-Owned Auto Endorsement Confirmation Letter validates that a company's insurance policy extends liability coverage to vehicles not owned by the entity. This essential document confirms protection for employee-owned cars or rented vehicles used during official business operations. It ensures that the corporation is shielded from third-party claims if an accident occurs while staff members are driving for work purposes. Obtaining this formal verification is a critical step in risk management, providing legal assurance to partners and stakeholders that comprehensive vicarious liability gaps are effectively closed.

Small Business Hired and Non-Owned Auto Endorsement Confirmation Letter

A Small Business Hired and Non-Owned Auto Endorsement Confirmation Letter serves as official proof that your commercial liability policy extends coverage to vehicles not owned by the company. This document is essential for verifying that rented vehicles and employees using personal cars for business errands are protected against third-party liability claims. It confirms that the HNOA endorsement is active, helping small businesses manage risks, satisfy contractual requirements with clients, and fill critical gaps where personal auto insurance typically excludes professional use.

Policy Renewal Hired and Non-Owned Auto Endorsement Confirmation Letter

A Policy Renewal Confirmation Letter serves as official proof that your Hired and Non-Owned Auto (HNOA) endorsement remains active. This essential document validates that your business has continuous liability coverage for vehicles used for work purposes that the company does not own, such as employee-owned cars or rentals. Ensuring this endorsement is updated during renewal protects your organization from potential third-party bodily injury or property damage claims. Always verify that the limits and effective dates on the confirmation letter align with your current commercial auto insurance requirements.

Non-Profit Organization Hired and Non-Owned Auto Endorsement Confirmation Letter

A Non-Profit Organization Hired and Non-Owned Auto Endorsement Confirmation Letter proves that the entity has liability coverage for vehicles used for business purposes that it does not own. This essential document confirms protection against third-party claims resulting from accidents involving rented cars or employee-owned vehicles driven on behalf of the non-profit. It ensures that both the organization and its volunteers are shielded from financial loss, bridging critical gaps in standard commercial auto policies and satisfying requirements for contractual compliance and risk management protocols.

Employee Transit Hired and Non-Owned Auto Endorsement Confirmation Letter

An Employee Transit Hired and Non-Owned Auto Endorsement Confirmation Letter verifies that your commercial auto insurance extends liability coverage to vehicles not owned by the business. This essential document confirms that the policy protects the company when staff members use personal vehicles or rentals for official business errands. It serves as formal proof for clients or partners that potential vicarious liability gaps are closed, ensuring the organization is shielded from financial loss during employee transit activities not covered by standard personal insurance policies.

What is a Hired and Non-Owned Auto (HNOA) Endorsement Confirmation Letter?

A Hired and Non-Owned Auto Endorsement Confirmation Letter is an official document issued by an insurance provider verifying that a business policy has been extended to cover liability for vehicles rented by the company or personal vehicles driven by employees for business purposes.

Why do clients or vendors require an HNOA confirmation letter?

Clients and vendors require this letter to ensure that the business has adequate liability protection in place should an accident occur while an employee is operating a vehicle not owned by the company, thereby protecting the hiring party from vicarious liability claims.

What specific information is included in an HNOA endorsement letter?

The letter typically includes the insurance carrier's details, policy number, effective dates, the specific limits of liability for hired and non-owned segments, and a statement confirming that these coverages are active endorsements on the primary commercial general liability or auto policy.

Does a Hired and Non-Owned Auto Endorsement cover physical damage to the vehicle?

Generally, a standard HNOA endorsement confirmation letter verifies liability coverage for third-party bodily injury and property damage; it does not typically cover physical damage (comprehensive or collision) to the hired or non-owned vehicle itself unless specifically noted as "Hired Auto Physical Damage" coverage.

How can a business obtain a formal HNOA Endorsement Confirmation Letter?

A business can obtain this letter by contacting their insurance broker or carrier to request a Certificate of Insurance (COI) or a formal letter of experience that explicitly lists the Hired and Non-Owned Auto endorsement and its respective coverage limits.

Comments