A Mortgagee Clause Update Endorsement Letter is a formal notification sent to insurance providers to modify lienholder information on a policy. This essential document ensures that the correct financial institution is listed for coverage and claims processing. Keeping these details accurate protects your property investment and maintains loan compliance. Below are some ready to use templates.

Image cover: Official Guide: Mortgagee Clause Update Letter Templates and Samples

Letter Samples List

- Insured Request for Mortgagee Clause Update Endorsement Letter

- Carrier Submission for Mortgagee Clause Update Endorsement Letter

- Lender Confirmation of Mortgagee Clause Update Endorsement Letter

- Insured Confirmation of Mortgagee Clause Update Endorsement Letter

- Pending Information for Mortgagee Clause Update Endorsement Letter

- Urgent Mortgagee Clause Update Endorsement Request Letter

- Endorsement Document Cover Letter for Mortgagee Clause Update

- Refinance Mortgagee Clause Update Endorsement Letter

- Prior Lender Removal and Mortgagee Clause Update Letter

- Premium Adjustment for Mortgagee Clause Update Endorsement Letter

- Correction of Mortgagee Clause Update Endorsement Letter

- Final Policy Declaration and Mortgagee Clause Update Letter

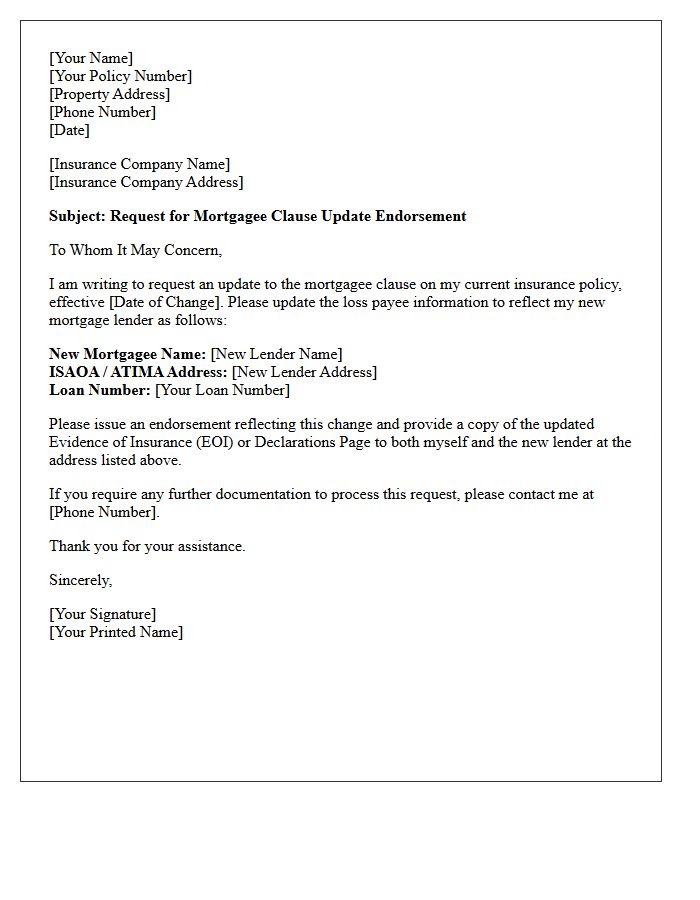

Insured Request for Mortgagee Clause Update Endorsement Letter

An Insured Request for Mortgagee Clause Update Endorsement Letter is a formal notification sent to an insurance provider to modify the lienholder information on a policy. This document ensures the mortgagee clause accurately reflects the current lender's name and address, which is vital for protecting their financial interest. Providing correct details prevents coverage lapses and ensures compliance with loan agreements. Always include your policy number, effective date, and the new lender's specific billing address to facilitate a seamless update and maintain proper evidence of insurance for your creditor.

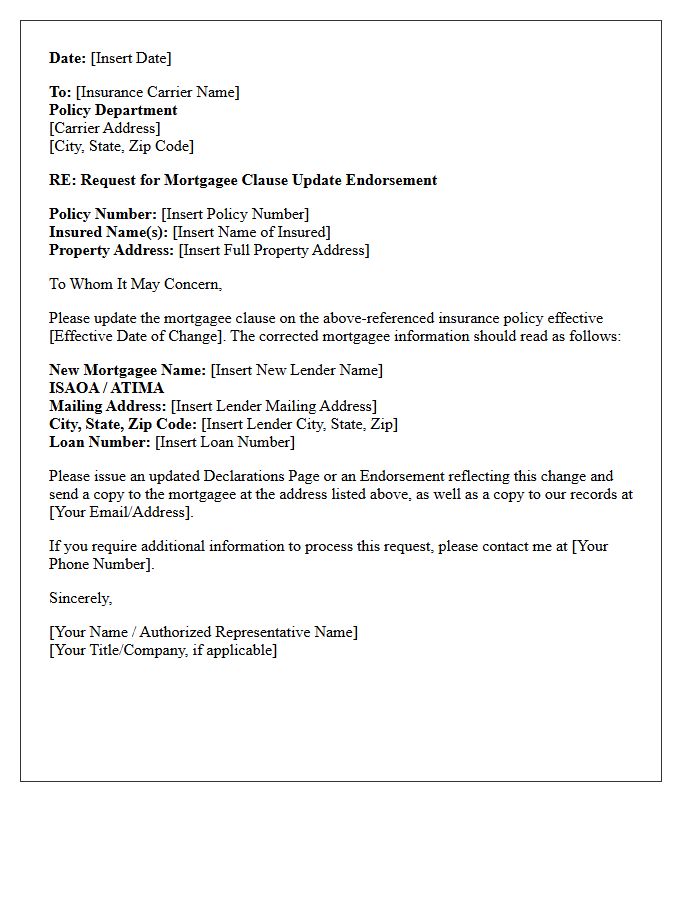

Carrier Submission for Mortgagee Clause Update Endorsement Letter

A carrier submission for a mortgagee clause update ensures your property insurance policy reflects the correct lender details. This endorsement letter is vital because it protects the lienholder's financial interest in the asset. When refinancing or switching lenders, you must provide the carrier with the new mortgagee name, address, and loan number. Failure to update this information can result in payment delays, escrow complications, or a technical breach of your loan agreement. Always confirm that the declaration page matches your current mortgage documentation to maintain seamless coverage compliance.

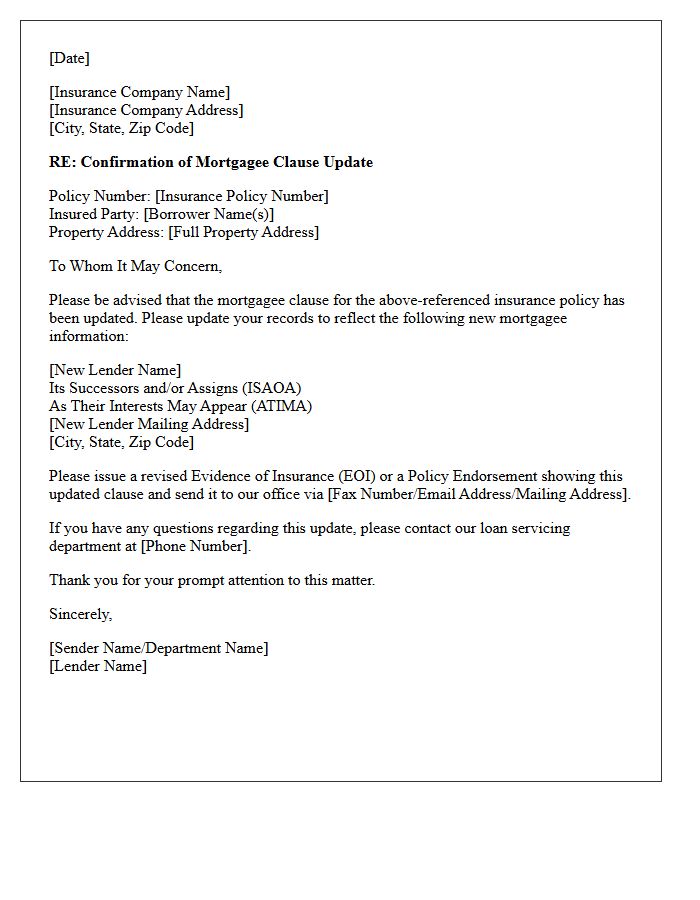

Lender Confirmation of Mortgagee Clause Update Endorsement Letter

A Lender Confirmation of Mortgagee Clause Update Endorsement Letter is a formal document verifying that an insurance policy's loss payee information has been accurately revised. This letter serves as legal evidence that the lender's specific interest in the property is protected under the correct corporate name and address. Ensuring this update is processed correctly is vital for maintaining loan compliance and preventing disruptions during the mortgage closing or escrow process. It guarantees that insurance claim payouts are properly directed to the lienholder to satisfy financial obligations.

Insured Confirmation of Mortgagee Clause Update Endorsement Letter

An Insured Confirmation of Mortgagee Clause Update Endorsement Letter is a vital document that formally notifies an insurance company to change the lienholder details on a policy. It ensures that the mortgagee clause accurately reflects the current lender's name and address. This update is crucial for maintaining proper coverage, ensuring loss payee rights are protected, and confirming that the lender receives official notifications regarding policy status or renewals. Failing to provide this confirmation can lead to administrative errors during escrow payments or claims processing.

Pending Information for Mortgagee Clause Update Endorsement Letter

A Mortgagee Clause Update Endorsement is essential for maintaining accurate legal records on your insurance policy. This document ensures the lender's correct name and billing address are listed, protecting their financial interest in the property. Failure to provide pending information promptly can lead to escrow payment delays or lapses in coverage. Always verify the Loan Number and specific mortgagee language required by your financial institution to ensure seamless communication between your insurance provider and the bank.

Urgent Mortgagee Clause Update Endorsement Request Letter

An Urgent Mortgagee Clause Update Endorsement Request is a critical formal notice sent to insurance providers to rectify lender information on a policy. This document ensures the mortgagee clause accurately reflects the financial institution's legal name, address, and loan number. Prompt processing is vital to maintain compliance with loan agreements, prevent escrow payment delays, and ensure the lender is properly protected in the event of a claim. Failure to update this information can lead to coverage lapses or administrative issues during property transfers or refinancing.

Endorsement Document Cover Letter for Mortgagee Clause Update

An endorsement document cover letter is essential for requesting a mortgagee clause update on your insurance policy. This formal notice ensures the lender's financial interest is correctly recorded, typically after a loan transfer or refinancing. Providing the new mortgagee name, address, and loan number prevents lapses in compliance. Accurate documentation guarantees that the insurance carrier directs claim payments and renewal notifications to the appropriate financial institution. Using a professional cover letter streamlines the endorsement process, maintaining the legal alignment between your property coverage and your current mortgage provider.

Refinance Mortgagee Clause Update Endorsement Letter

A Refinance Mortgagee Clause Update is a critical document used to amend your homeowners insurance policy during a loan restructuring. It ensures the new lender is properly listed as the primary loss payee and lienholder. This endorsement protects the financial interests of the financial institution and maintains compliance with closing requirements. Failing to update this clause can delay your funding or cause issues with escrow disbursements. Always verify that the ISAOA/ATIMA verbiage is accurate to guarantee seamless coverage transition and legal protection for all parties involved.

Prior Lender Removal and Mortgagee Clause Update Letter

A Prior Lender Removal and Mortgagee Clause Update Letter is a vital document sent to insurance companies during a property refinance or transfer. It ensures the replacement of an old financial institution with the new lienholder on a homeowners policy. Correctly updating this clause is essential to guarantee that insurance claim payouts are directed to the proper entity. Failure to submit this update can result in coverage lapses, improper loss payee designations, or delays in closing your loan. Always verify the new lender's specific address and loan number for accuracy.

Premium Adjustment for Mortgagee Clause Update Endorsement Letter

A Premium Adjustment for Mortgagee Clause Update Endorsement Letter formalizes changes to your insurance policy's loss payee information. When a lender's name or address changes, this legal document ensures the mortgagee clause remains accurate. Crucially, updating these details can trigger a premium recalculation based on administrative costs or modified risk assessments. Homeowners must verify these updates to maintain continuous coverage and ensure that claim payments are correctly directed to the valid lienholder, preventing potential lending compliance issues or lapses in financial protection.

Correction of Mortgagee Clause Update Endorsement Letter

A Mortgagee Clause Update Endorsement Letter is a critical document used to rectify errors in a lienholder's information on an insurance policy. Ensuring the correct legal name, address, and loan number is vital for protecting the lender's financial interest. If these details are inaccurate, it can lead to payment delays, escrow discrepancies, or issues during claim settlements. Promptly issuing this correction ensures continuous compliance with mortgage agreements and maintains the seamless disbursement of insurance funds to the appropriate financial institution.

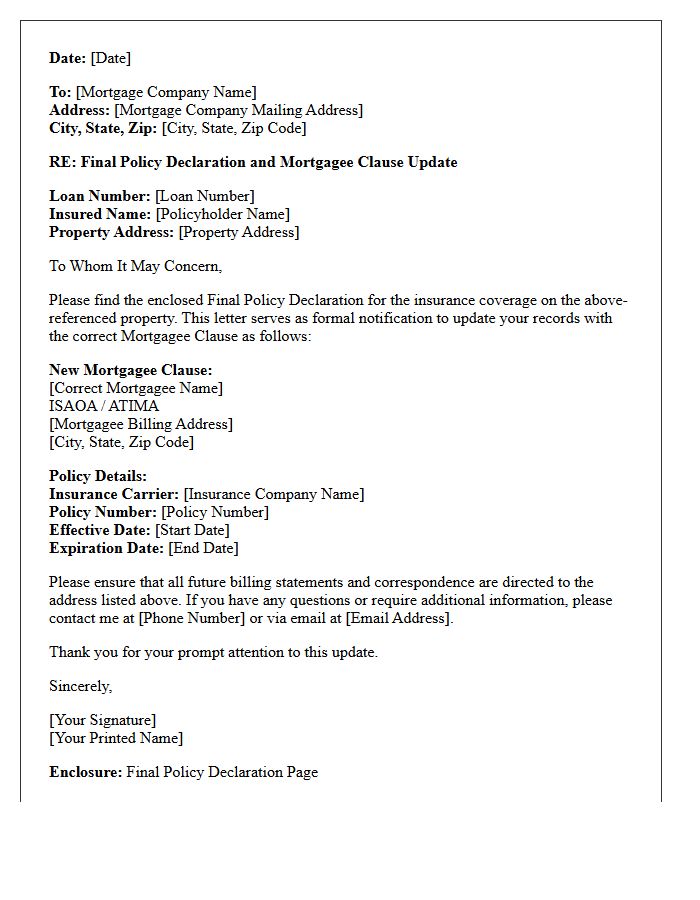

Final Policy Declaration and Mortgagee Clause Update Letter

A Final Policy Declaration confirms your active insurance coverage details, including limits and premiums. When changing lenders or updating loan information, a Mortgagee Clause Update Letter is essential to ensure your financial institution is correctly listed as the loss payee. This document protects the lender's interest in the property and guarantees they receive necessary notifications regarding policy status. Promptly providing these updates prevents escrow payment delays and ensures continuous compliance with your mortgage agreement requirements, maintaining your property's protection against potential claims.

What is a Mortgagee Clause Update Endorsement Letter?

A Mortgagee Clause Update Endorsement Letter is an official document sent to an insurance provider to amend the lienholder information on a property insurance policy. It ensures that the correct financial institution is listed as the loss payee and receives relevant policy notifications.

When should I request a Mortgagee Clause update?

You should request an update whenever your mortgage is sold to a new servicer, if your current lender changes its legal name or billing address, or when refinancing your home loan. Keeping this information current prevents lapses in escrow payments and ensures claims are processed correctly.

What information is required for a Mortgagee Clause endorsement?

The letter must include the policyholder's name, the policy number, the property address, and the new lender's full legal name, department (such as ISAOA/ATIMA), and their specific mailing address for insurance documentation.

Does updating the Mortgagee Clause affect my insurance premium?

Updating the mortgagee clause is an administrative change and typically does not impact your insurance premium or coverage limits. However, it is vital for ensuring that your lender continues to pay the premium through your escrow account on time.

What does ISAOA/ATIMA mean in a Mortgagee Clause?

ISAOA stands for "Its Successors and/or Assigns," and ATIMA stands for "As Their Interests May Appear." These legal terms are included in the endorsement to ensure that the lender's rights are protected even if the loan is transferred or sold to another entity.

Comments