An insurance policy reaches a lapse of coverage due to cash value depletion when the internal account can no longer sustain monthly mortality charges and fees. This typically occurs in permanent life insurance when loans, withdrawals, or poor market performance exhaust the funds. To help you notify clients or understand your options, below are some ready to use templates.

Image cover: Policy Cancellation Due to Cash Value Depletion: Essential Templates and Notice Samples

Letter Samples List

- Warning Letter for Impending Policy Lapse Due to Cash Value Depletion

- Urgent Letter Regarding Cash Value Depletion and Policy Lapse

- Grace Period Notification Letter for Cash Value Depletion

- Final Grace Period Letter Before Coverage Lapse

- Formal Letter of Coverage Lapse Due to Cash Value Depletion

- Policy Termination Letter Due to Insufficient Cash Value

- Notice Letter of Policy Lapse From Cash Value Depletion

- Reinstatement Option Letter Following Cash Value Depletion Lapse

- Premium Funding Request Letter to Prevent Coverage Lapse

- Account Status Letter Detailing Cash Value Depletion and Lapse

- Policyholder Advisory Letter on Cash Value Depletion Lapse

- Insurance Agency Letter Confirming Lapse of Coverage

- Coverage Cancellation Letter Due to Depleted Cash Value

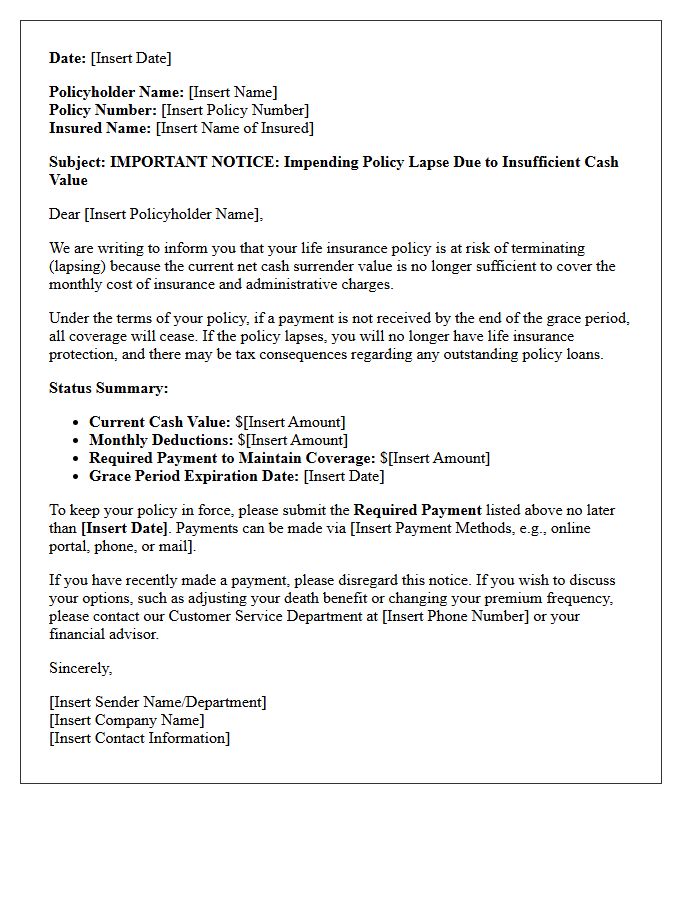

Warning Letter for Impending Policy Lapse Due to Cash Value Depletion

A warning letter for impending policy lapse is a critical notice sent when your life insurance policy's cash value is no longer sufficient to cover monthly mortality and administrative charges. This typically occurs in permanent plans like universal life if premiums are underpaid or loan interest accumulates. To maintain your death benefit and prevent the policy from terminating, you must make a catch-up payment before the grace period ends. Ignoring this notice results in a total loss of coverage and potential tax consequences on outstanding loans.

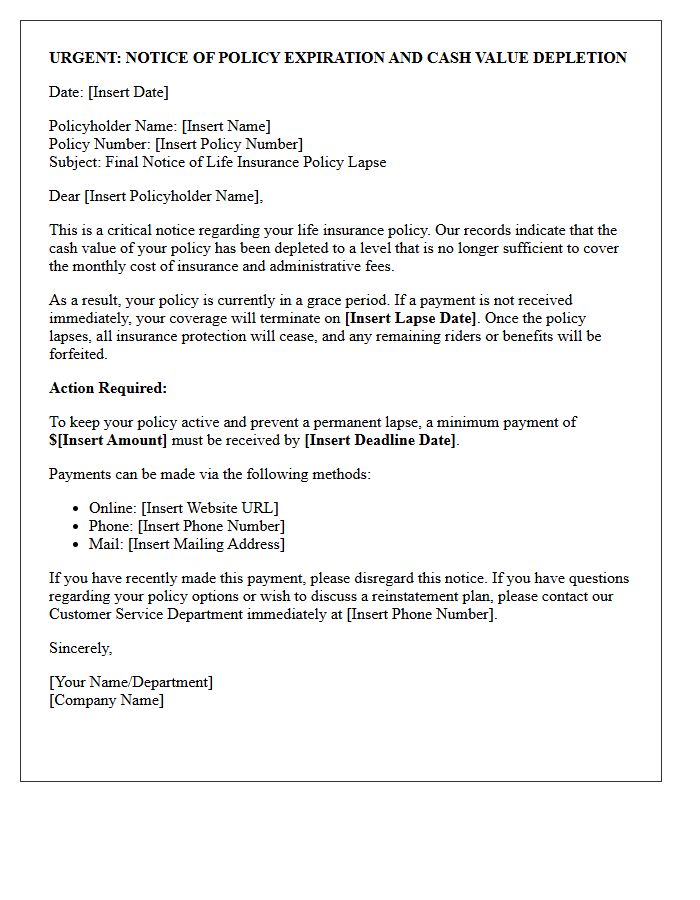

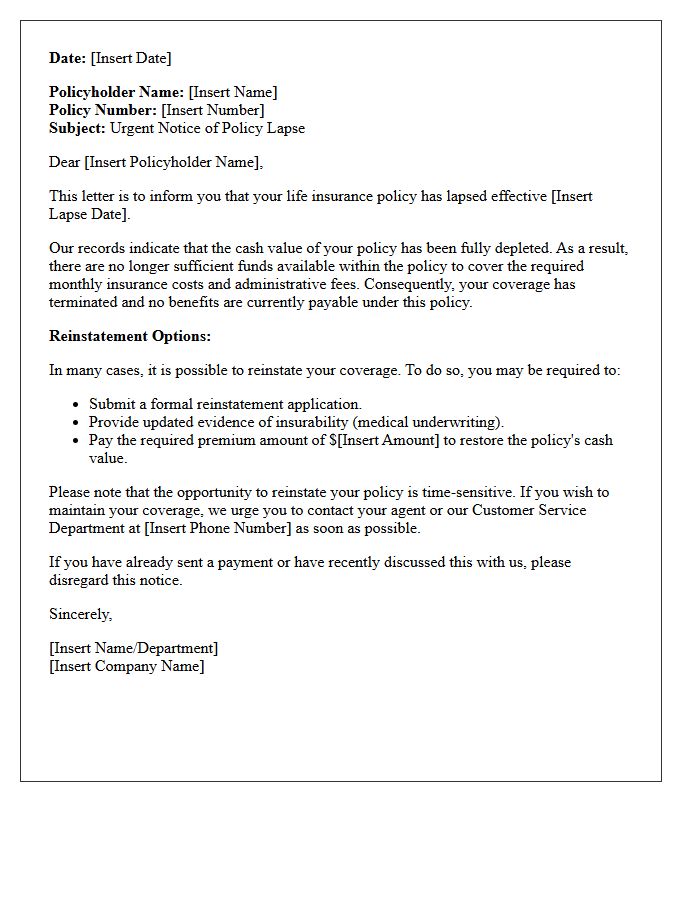

Urgent Letter Regarding Cash Value Depletion and Policy Lapse

A policy lapse notice is a critical warning that your life insurance coverage is at risk due to cash value depletion. This occurs when internal policy costs exceed the available account balance. To prevent a permanent loss of protection, you must take immediate action by paying the required premium or adjusting your death benefit. Ignoring this urgent letter can lead to the termination of your policy without value, leaving beneficiaries unprotected. Contact your provider instantly to explore reinstatement options or funding strategies to maintain your essential financial security.

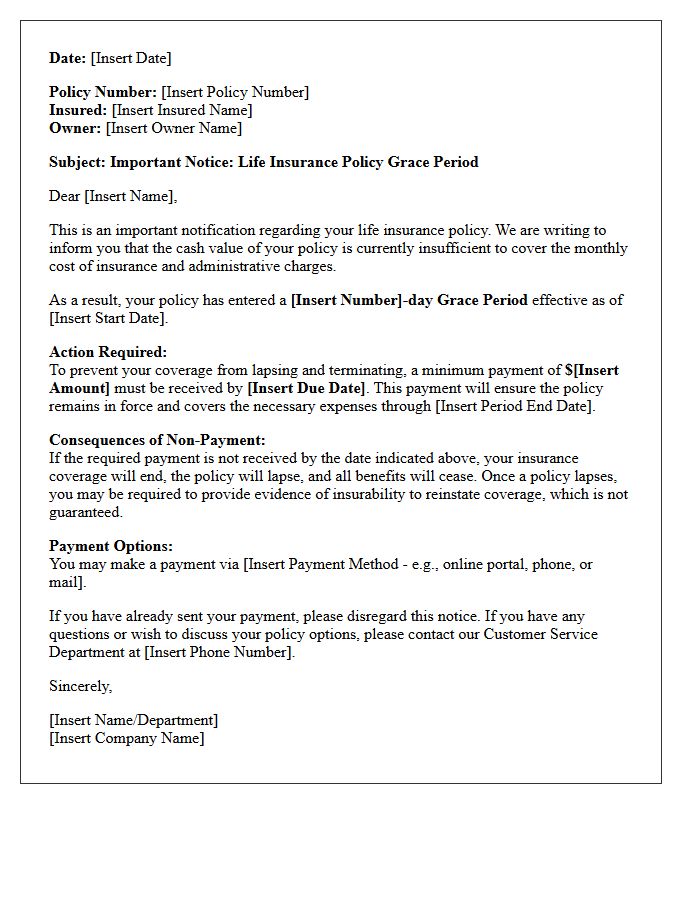

Grace Period Notification Letter for Cash Value Depletion

A Grace Period Notification Letter is a critical warning issued when your life insurance policy's cash value is insufficient to cover monthly charges. This formal notice alerts policyholders that their coverage is at risk of lapse unless a required premium payment is made by a specific deadline. Receiving this letter indicates that your policy has entered a grace period, typically lasting 30 to 31 days. To maintain financial protection and prevent the permanent loss of death benefits, you must remit the specified payment to restore the policy's net equity immediately.

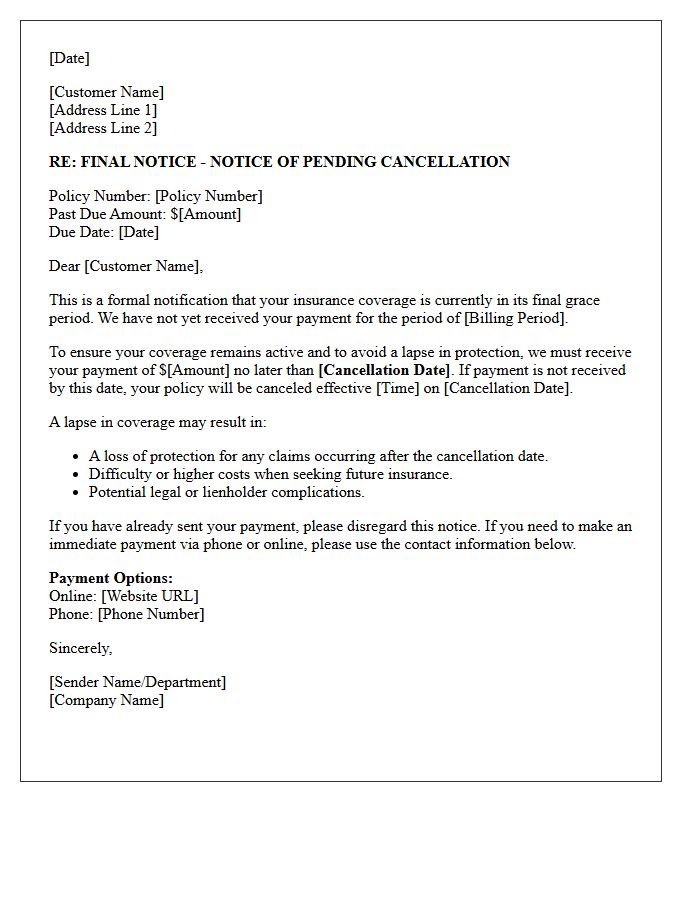

Final Grace Period Letter Before Coverage Lapse

A final grace period letter is a critical termination notice issued by insurance companies before a policy cancels. This document serves as your last opportunity to pay outstanding premiums and maintain protection. Once this window expires, your coverage lapse becomes official, leaving you without financial security and potentially causing higher future rates. It is essential to act immediately upon receipt to prevent a gap in coverage. Always verify the payment deadline and specific reinstatement terms to ensure your policy remains active and your claims stay protected.

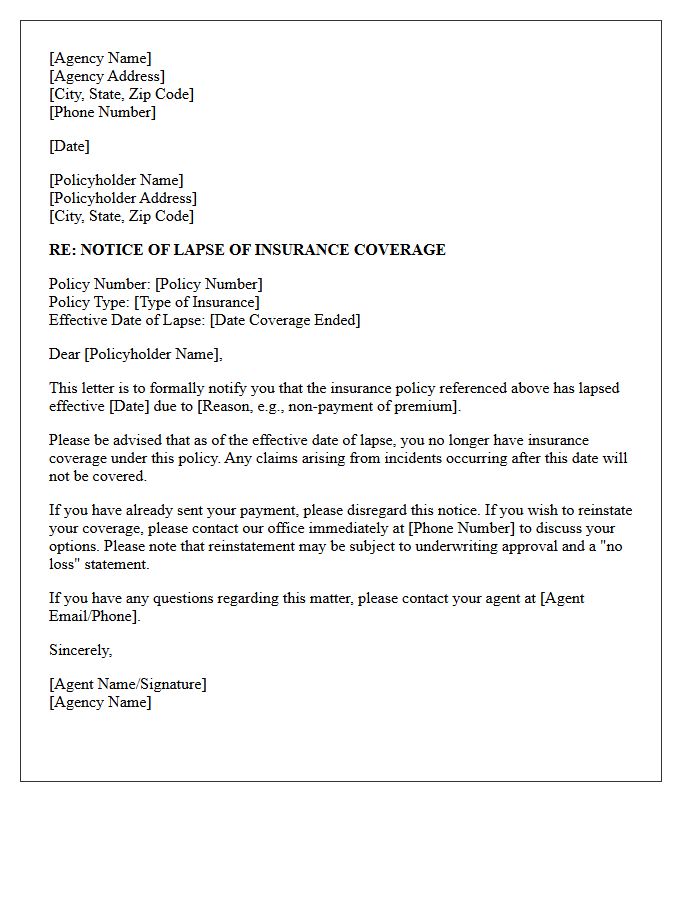

Formal Letter of Coverage Lapse Due to Cash Value Depletion

A formal notice of coverage lapse due to cash value depletion warns policyholders that their permanent life insurance is at risk. This occurs when the policy's internal account no longer holds sufficient funds to cover monthly insurance costs and administrative fees. To prevent a permanent termination of benefits, the owner must make a catch-up payment within the specified grace period. Failure to act results in the loss of protection and potential tax consequences, making it critical to monitor funding levels regularly to maintain long-term financial security.

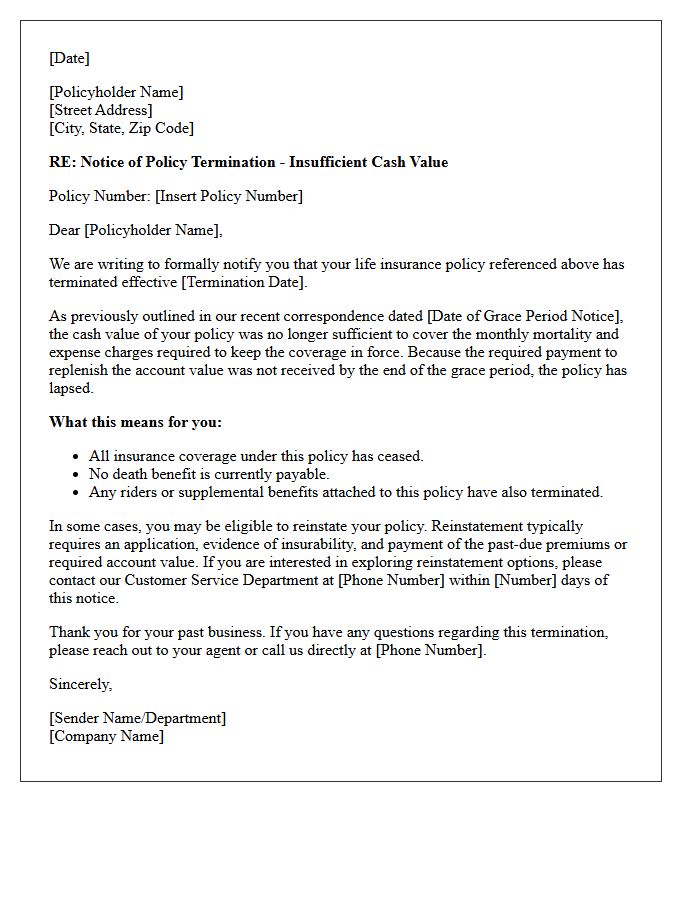

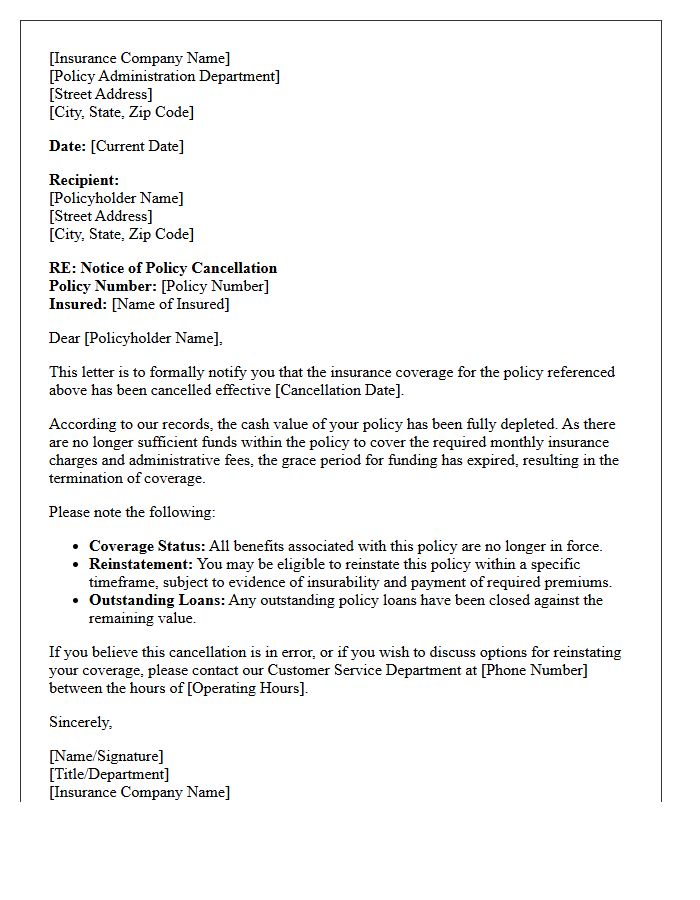

Policy Termination Letter Due to Insufficient Cash Value

A policy termination letter serves as formal notice that your life insurance coverage will end because the insufficient cash value is no longer enough to cover monthly mortality charges and administrative fees. To prevent a permanent lapse in protection, policyholders typically enter a 31-day grace period. During this time, you must make a required premium payment to keep the policy active. Failure to act results in the loss of death benefits and potential tax consequences on any outstanding loans, making immediate reinstatement efforts critical for maintaining your financial security.

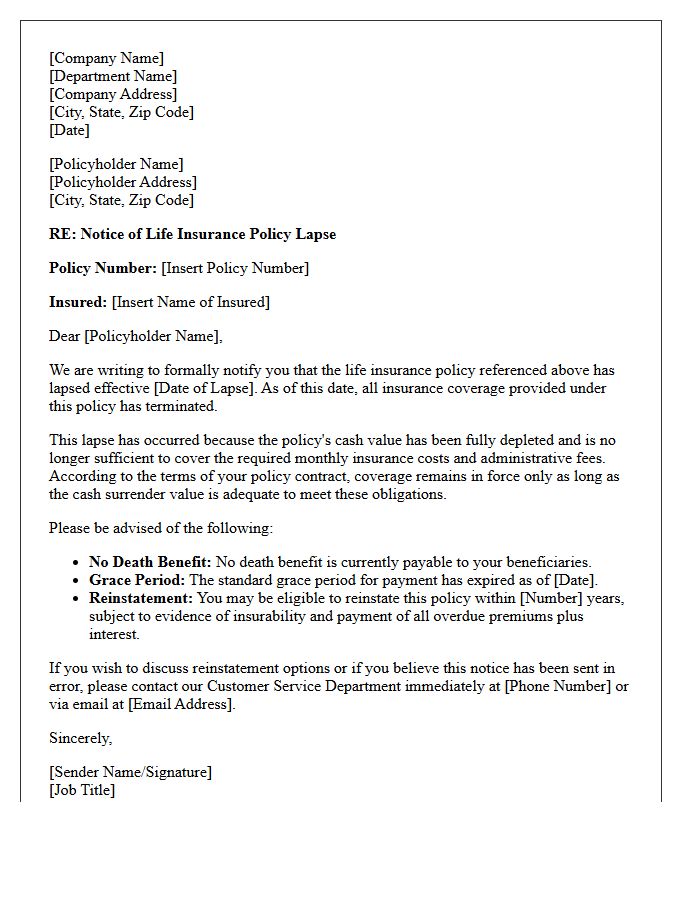

Notice Letter of Policy Lapse From Cash Value Depletion

A notice letter regarding policy lapse due to cash value depletion is a critical warning that your life insurance coverage is at risk. This occurs when the accumulated account value is no longer sufficient to cover monthly mortality charges and administrative fees. To prevent a permanent loss of coverage, policyholders must typically pay a catch-up premium within a specified grace period. Ignoring this notice results in the termination of death benefits and potential tax liabilities. Reviewing your statement immediately is essential to maintain your financial security and policy standing.

Reinstatement Option Letter Following Cash Value Depletion Lapse

A Reinstatement Option Letter is a formal notification sent after a life insurance policy terminates due to cash value depletion. This document outlines specific reinstatement requirements, such as paying overdue premiums and providing evidence of insurability. Acting quickly is essential, as there is a limited timeframe to restore coverage without starting a new application. Reviewing this letter helps policyholders understand the reinstatement period and the necessary steps to recover lost benefits, ensuring the protection of their financial beneficiaries remains intact after an unexpected policy lapse.

Premium Funding Request Letter to Prevent Coverage Lapse

A premium funding request letter is a critical formal notice sent to a financier or client to secure capital for insurance costs. Its primary goal is to ensure the continuation of protection by preventing a policy cancellation due to non-payment. This document must clearly state the outstanding balance, the specific due date, and the consequences of missing the deadline. Providing timely financial intervention protects your business from liability exposures and ensures that essential coverage remains active during critical periods, maintaining your organization's overall financial stability and risk management strategy.

Account Status Letter Detailing Cash Value Depletion and Lapse

An Account Status Letter is a critical legal notice warning policyholders about Cash Value Depletion. This document signifies that your life insurance policy lacks sufficient funds to cover monthly mortality charges and administrative fees. If the net cash surrender value reaches zero, the policy enters a grace period before a total Lapse occurs. Once lapsed, all death benefits and coverage cease immediately. To prevent termination, you must make a catch-up payment or adjust the face value to maintain the contract's active status and preserve your financial protection.

Policyholder Advisory Letter on Cash Value Depletion Lapse

A Policyholder Advisory Letter warns owners when a life insurance policy faces a Cash Value Depletion Lapse. This critical notification arrives when the account's internal balance becomes insufficient to cover monthly mortality charges and administrative fees. To prevent a permanent loss of coverage, policyholders must take immediate action, such as paying additional premiums or adjusting the death benefit. Ignoring this alert leads to the policy terminating without value. Understanding these notices is essential for maintaining financial protection and ensuring the policy remains in force during market volatility or rising costs.

Insurance Agency Letter Confirming Lapse of Coverage

An insurance agency letter confirming a lapse of coverage serves as formal notice that your policy is no longer active. This document typically highlights the effective date of termination, meaning you currently have no financial protection against risks. Common causes include non-payment or failure to meet underwriting requirements. It is critical to address this immediately to avoid legal penalties, higher future premiums, or a permanent gap in insurance. If you receive this notice, contact your agent instantly to discuss potential reinstatement options and restore your essential coverage.

Coverage Cancellation Letter Due to Depleted Cash Value

A coverage cancellation letter for a policy with depleted cash value serves as a formal notice that your life insurance is at risk of lapsing. This occurs when the policy loans or internal costs exceed the available equity, leaving insufficient funds to cover premiums. To prevent a total loss of benefits, policyholders must typically make a catch-up payment within a specified grace period. Reviewing your annual statements regularly is essential to monitor performance and avoid unexpected termination of your financial protection.

What is a lapse of coverage due to cash value depletion?

A lapse occurs when the cash value within a permanent life insurance policy falls to zero or becomes insufficient to cover the monthly cost of insurance and administrative fees, resulting in the termination of the policy's death benefit.

What causes the cash value in a life insurance policy to deplete?

Cash value depletion is typically caused by insufficient premium payments, high outstanding policy loans and accrued interest, or increased internal insurance costs as the policyholder ages, which eventually exceed the policy's interest earnings.

Will I receive a notification before my policy lapses due to low cash value?

Yes, insurance companies are legally required to provide a grace period-typically 30 to 61 days-and must send a formal notice stating the premium amount required to keep the policy active before the coverage officially terminates.

Can I reinstate a life insurance policy after it has lapsed?

Most insurers allow reinstatement within a specific timeframe (usually 3 to 5 years), provided the policyholder pays all back premiums plus interest and, in many cases, undergoes a new medical exam to prove insurability.

How can I prevent my life insurance policy from lapsing?

To prevent a lapse, you should regularly monitor your policy's annual statements, pay back outstanding policy loans, increase your premium contributions if the cost of insurance rises, or consider a policy 1035 exchange to a product better suited for your current financial situation.

Comments