Missing a life insurance premium can lead to policy cancellation, leaving you without essential coverage. A Post-Lapse Reinstatement Offer Letter provides a formal way for insurers to invite policyholders to restore their protection by settling outstanding dues. This document outlines necessary steps, deadlines, and requirements to regain active status. To simplify your communication process, below are some ready to use template.

Image cover: Professional Life Insurance Reinstatement Offer Templates and Guide

Letter Samples List

- Standard Auto Policy Post-Lapse Reinstatement Offer Letter

- Term Life Insurance Post-Lapse Reinstatement Offer Letter

- Homeowners Coverage Post-Lapse Reinstatement Offer Letter

- Commercial Liability Post-Lapse Reinstatement Offer Letter

- Conditional Health Care Post-Lapse Reinstatement Offer Letter

- No Underwriting Requirement Post-Lapse Reinstatement Offer Letter

- Final Opportunity Post-Lapse Reinstatement Offer Letter

- Waived Penalty Fee Post-Lapse Reinstatement Offer Letter

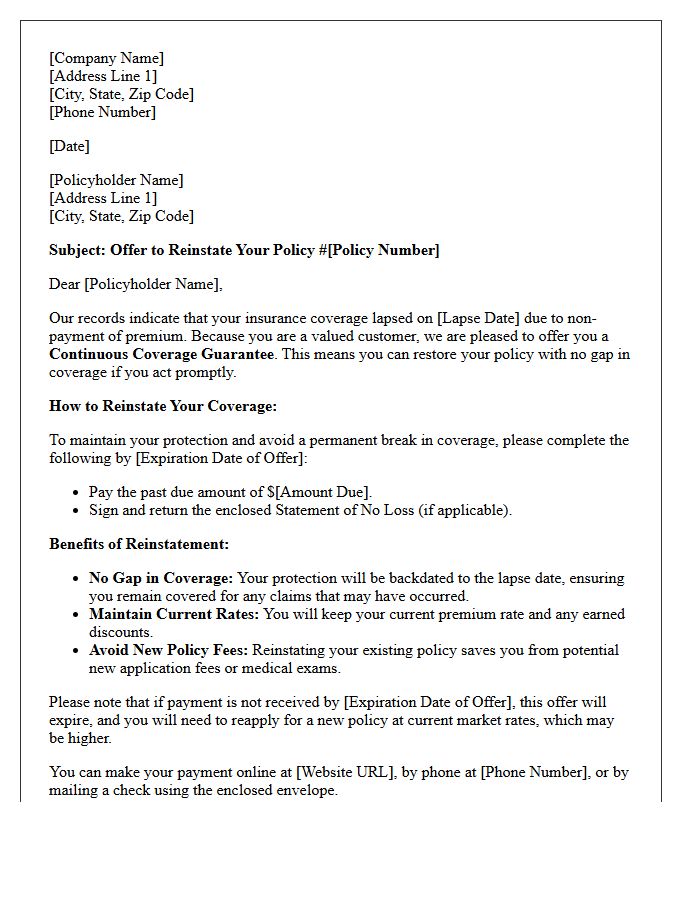

- Continuous Coverage Guarantee Post-Lapse Reinstatement Offer Letter

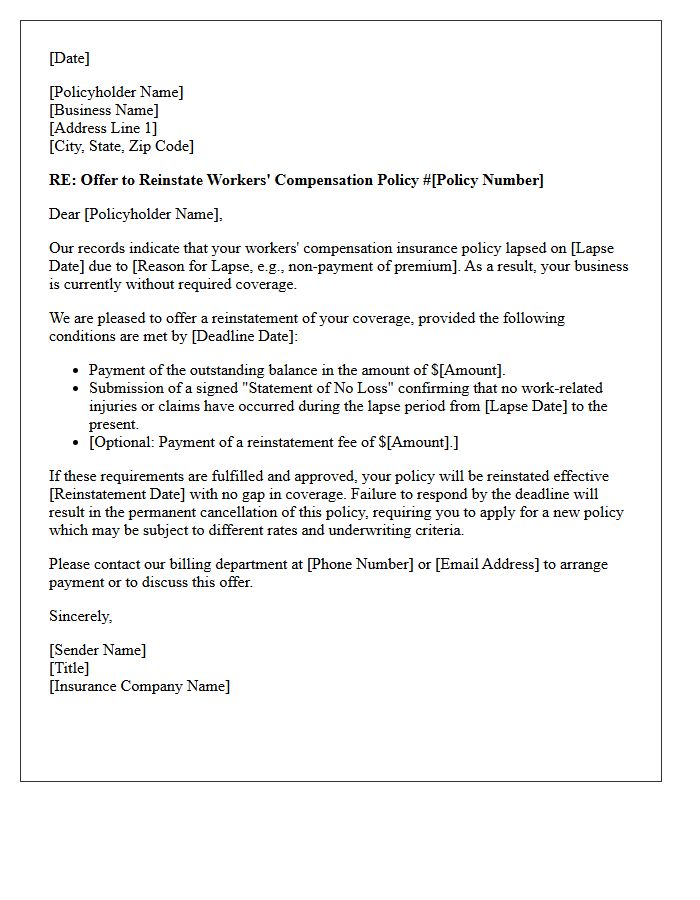

- Workers Compensation Post-Lapse Reinstatement Offer Letter

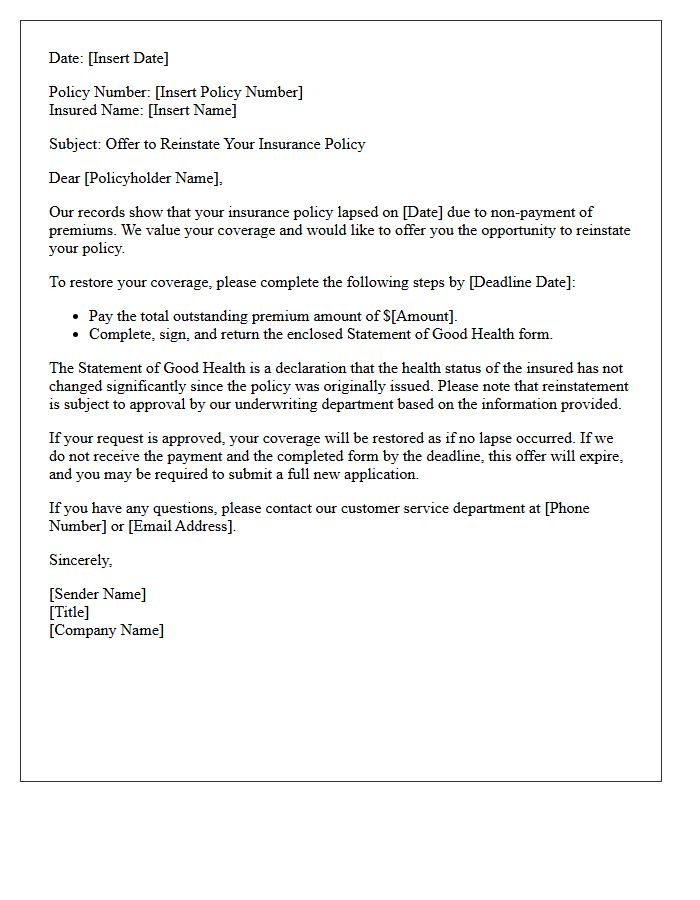

- Statement of Good Health Post-Lapse Reinstatement Offer Letter

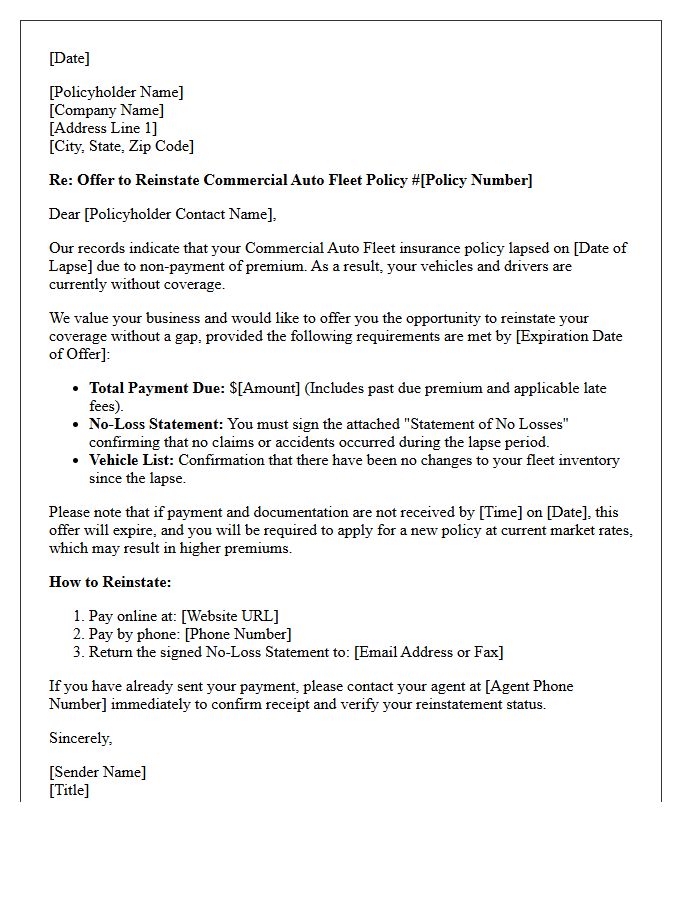

- Commercial Auto Fleet Post-Lapse Reinstatement Offer Letter

- Professional Indemnity Post-Lapse Reinstatement Offer Letter

Standard Auto Policy Post-Lapse Reinstatement Offer Letter

A Standard Auto Policy Post-Lapse Reinstatement Offer Letter is a time-sensitive document sent by insurers after a policy cancels due to non-payment. This reinstatement offer provides a vital grace period to restore coverage without a lapse in protection. To maintain continuous insurance, policyholders must pay the total past-due premium by the specified deadline. Failure to act results in a permanent lapse, potentially leading to higher future premiums and legal risks. Always verify if a Statement of No Loss is required to confirm no accidents occurred during the inactive period.

Term Life Insurance Post-Lapse Reinstatement Offer Letter

A Term Life Insurance Post-Lapse Reinstatement Offer Letter is a critical notice sent after coverage expires due to unpaid premiums. This document outlines the specific reinstatement requirements, such as paying overdue balances and submitting a Statement of Health. Act quickly, as these offers are time-sensitive. Successfully completing the process allows you to restore your original policy without undergoing a full new medical exam, maintaining your initial coverage rates and protecting your beneficiaries' financial security. Always review the deadline to ensure your policy protection remains intact.

Homeowners Coverage Post-Lapse Reinstatement Offer Letter

A homeowners coverage post-lapse reinstatement offer letter is a formal notice from your insurer providing a temporary opportunity to restore expired protection. This document typically outlines specific conditions, such as paying outstanding premiums and signing a no-loss statement to confirm no claims occurred during the gap. Acting quickly is essential to avoid permanent coverage termination and potential financial risk. Always verify the reinstatement deadline and any additional fees required to maintain your property's continuous security and comply with mortgage lender requirements.

Commercial Liability Post-Lapse Reinstatement Offer Letter

A Commercial Liability Post-Lapse Reinstatement Offer Letter is a formal notification from an insurer providing an opportunity to restore coverage after a policy has cancelled due to non-payment. The most critical element is the reinstatement deadline, as missing this date results in a permanent lapse. Business owners must typically submit a signed "no loss" statement and pay all outstanding premiums to reactivate protection. Timely action is essential to avoid unprotected exposures and ensure continuous liability protection for business operations, assets, and legal defense costs.

Conditional Health Care Post-Lapse Reinstatement Offer Letter

A Conditional Health Care Post-Lapse Reinstatement Offer Letter is a formal notice sent by insurers after a policy cancels due to non-payment. This document outlines specific eligibility requirements, such as paying outstanding premiums and providing a statement of good health. It is critical to understand that coverage is not active until the insurer formally approves the request. Acting within the specified deadline is essential to avoid a permanent loss of benefits and to ensure continuous medical protection without needing to undergo a full new underwriting process.

No Underwriting Requirement Post-Lapse Reinstatement Offer Letter

A No Underwriting Requirement Post-Lapse Reinstatement Offer is a critical time-bound opportunity to restore your insurance coverage without a new medical exam. If your policy lapses due to missed premiums, this letter allows you to bypass complex health assessments, provided you pay the outstanding balance by the specified deadline. Accepting this offer ensures your original policy terms and benefits remain intact regardless of changes in your health status. Act quickly, as these guaranteed reinstatement windows are typically brief and expire permanently once the grace period ends.

Final Opportunity Post-Lapse Reinstatement Offer Letter

A Final Opportunity Post-Lapse Reinstatement Offer Letter is a critical formal notice allowing policyholders to restore expired insurance coverage. This time-sensitive document outlines specific reinstatement requirements, such as paying outstanding premiums and providing evidence of insurability. Acting promptly is essential to avoid a permanent loss of protection and the need for a new application at higher rates. Review the deadline carefully to ensure your policy benefits remain active and your financial security is preserved without interruption.

Waived Penalty Fee Post-Lapse Reinstatement Offer Letter

A Waived Penalty Fee Post-Lapse Reinstatement Offer Letter is a formal notice from an insurer allowing you to restore a terminated policy without extra costs. This time-sensitive document provides a grace period extension, enabling policyholders to maintain continuous coverage by paying only the outstanding premiums. It is crucial to act before the expiration date listed in the letter to avoid permanent loss of benefits or the requirement of a new medical exam. Reviewing these terms ensures your financial protection remains intact after an accidental payment lapse.

Continuous Coverage Guarantee Post-Lapse Reinstatement Offer Letter

A Continuous Coverage Guarantee offer allows policyholders to restore protection after a missed payment. This Post-Lapse Reinstatement letter is a time-sensitive opportunity to maintain benefits without a gap in history. By paying the outstanding premium by the specified deadline, you ensure uninterrupted security and avoid the need for new medical underwriting or higher rates. Reviewing these terms promptly is essential to protect your policy status and guarantee that your coverage remains active despite a temporary lapse in payment.

Workers Compensation Post-Lapse Reinstatement Offer Letter

A Workers Compensation Post-Lapse Reinstatement Offer Letter is a critical notice sent by an insurer after a policy cancels due to non-payment. This document outlines the specific requirements to reinstate coverage and avoid a permanent gap. Business owners must quickly pay the outstanding premium and provide a "no loss statement" certifying no injuries occurred during the lapse. Acting immediately is essential to maintain legal compliance, protect employees, and prevent costly penalties or uninsured claims. Always verify the reinstatement deadline mentioned in the letter to ensure continuous protection for your business.

Statement of Good Health Post-Lapse Reinstatement Offer Letter

A Statement of Good Health is a mandatory legal document required when applying for life insurance reinstatement after a policy lapses. This offer letter allows you to restore coverage without a full medical exam, provided you confirm your health status has not declined since the original issue date. You must truthfully disclose any new medical conditions or treatments. Timely submission, along with overdue premiums, is critical to maintaining your financial protection. Failure to provide accurate information can lead to future claim denials or permanent policy cancellation.

Commercial Auto Fleet Post-Lapse Reinstatement Offer Letter

A Commercial Auto Fleet Post-Lapse Reinstatement Offer Letter is a critical formal notice allowing policyholders to restore expired coverage. This document outlines specific reinstatement conditions, such as outstanding premium payments and potential "no loss" declarations. Act promptly, as these offers are time-sensitive and prevent permanent gaps in protection. Timely acceptance ensures your business vehicles remain legally compliant and avoids the high costs associated with high-risk re-rating. Review all terms carefully to maintain continuous liability defense and operational continuity for your fleet.

Professional Indemnity Post-Lapse Reinstatement Offer Letter

A Professional Indemnity Post-Lapse Reinstatement Offer Letter is a formal document sent by insurers to policyholders whose coverage has expired. Its primary purpose is to provide a reinstatement opportunity, allowing the professional to restore protection without a permanent break in cover. It is vital to review the retroactive date, as maintaining continuous coverage is essential for protection against claims arising from past work. This offer usually requires a signed declaration confirming no known claims occurred during the gap to ensure the policy remains valid and legally compliant.

What is a Post-Lapse Reinstatement Offer Letter?

A Post-Lapse Reinstatement Offer Letter is a formal notification sent by an insurance company to a policyholder whose coverage has expired due to non-payment, offering a specific window of time to restore the policy without requiring a full new application.

How long do I have to respond to a reinstatement offer?

The deadline is typically specified within the letter as a "Limited Time Offer," often ranging from 15 to 30 days from the date of the notice. Failure to submit payment and required documentation by this date may result in the permanent termination of the policy.

Do I need to undergo a new medical exam to reinstate my policy?

In many cases, a Post-Lapse Reinstatement Offer allows you to bypass a new medical exam provided you sign a "Statement of Good Health" confirming that your physical condition hasn't changed since the original policy was issued.

Will my insurance premiums increase after a reinstatement?

Generally, if you accept the offer within the specified timeframe, your original premium rate and policy terms remain the same. However, you will be required to pay all past-due premiums, and potentially interest, to bring the policy current.

What happens if my reinstatement request is denied?

If the insurer denies your reinstatement-usually due to changes in health status or missed deadlines-your coverage remains inactive. You would then need to apply for a brand-new policy at your current age and health status, which may result in higher premiums.

Comments