An Annual Policy Review is essential for maintaining comprehensive protection against evolving risks. This process involves evaluating your current insurance portfolio to ensure limits align with your assets. By proactively conducting a Coverage Gap Identification, you can address hidden vulnerabilities before a loss occurs. Ensure your financial security remains intact year after year; below are some ready to use templates.

Image cover: The Comprehensive Guide to Annual Policy Reviews and Coverage Gap Templates

Letter Samples List

- Annual Comprehensive Policy Review and Coverage Gap Identification Letter

- Commercial Insurance Annual Risk Assessment and Coverage Gap Letter

- Personal Lines Annual Coverage Evaluation and Gap Identification Letter

- Homeowners Policy Annual Review and Asset Protection Gap Letter

- Auto Insurance Annual Renewal and Liability Coverage Gap Letter

- Umbrella Liability Coverage Gap Identification and Annual Review Letter

- Life Insurance Annual Benefit Review and Coverage Shortfall Letter

- Business Owner Policy Annual Review and Risk Gap Identification Letter

- Cyber Liability Annual Coverage Gap and Security Review Letter

- Workers Compensation Annual Policy Evaluation and Gap Letter

- Health Insurance Annual Benefit Review and Coverage Gap Letter

- General Liability Annual Policy Assessment and Coverage Gap Letter

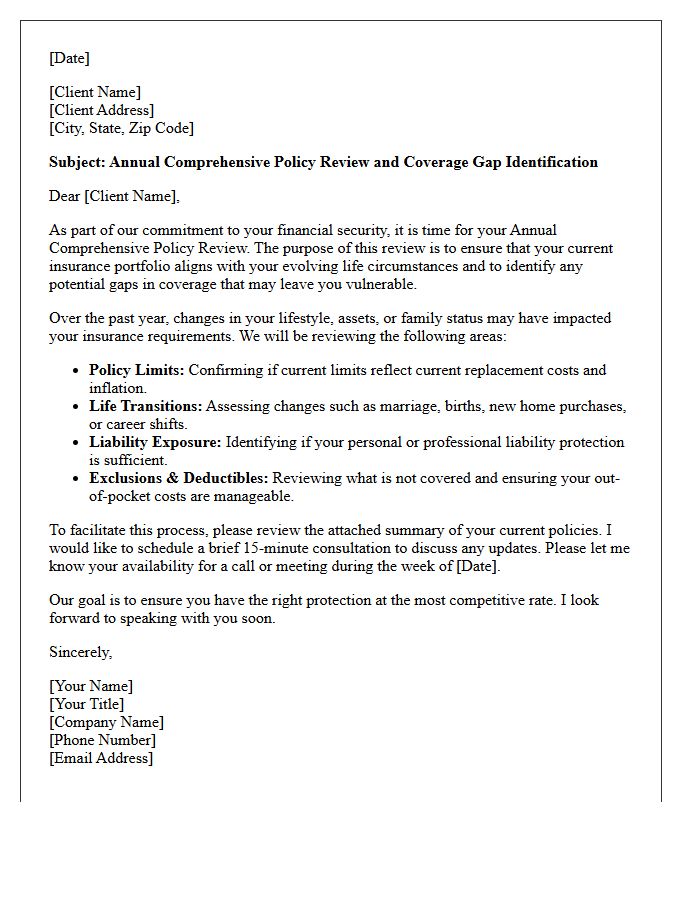

Annual Comprehensive Policy Review and Coverage Gap Identification Letter

An Annual Comprehensive Policy Review is a vital risk management process that evaluates your current insurance against evolving exposures. This systematic assessment ensures that policy limits and endorsements remain aligned with your financial goals. A critical outcome is the Coverage Gap Identification Letter, which formally documents specific vulnerabilities or uninsured risks discovered during the audit. Reviewing this letter helps policyholders make informed decisions to mitigate potential losses, ensuring continuity of protection and preventing unexpected out-of-pocket expenses when a claim occurs. Professional oversight during this review maintains optimal asset security.

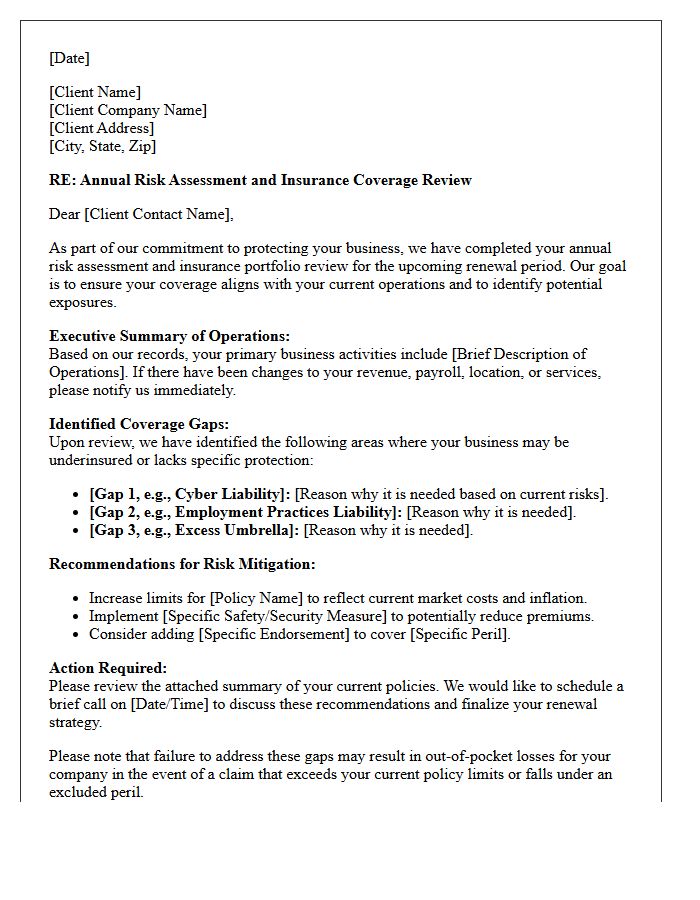

Commercial Insurance Annual Risk Assessment and Coverage Gap Letter

A Commercial Insurance Annual Risk Assessment is a critical evaluation of your business's evolving liabilities and asset values. Over time, operational shifts or inflation can create a coverage gap, leaving your company financially exposed during a claim. Upon completion, your broker issues a Coverage Gap Letter, which formally identifies underinsured areas or missing protections. Reviewing this document ensures your policy limits align with current market realities, helping you mitigate unforeseen financial losses and maintain comprehensive business continuity through proactive risk management.

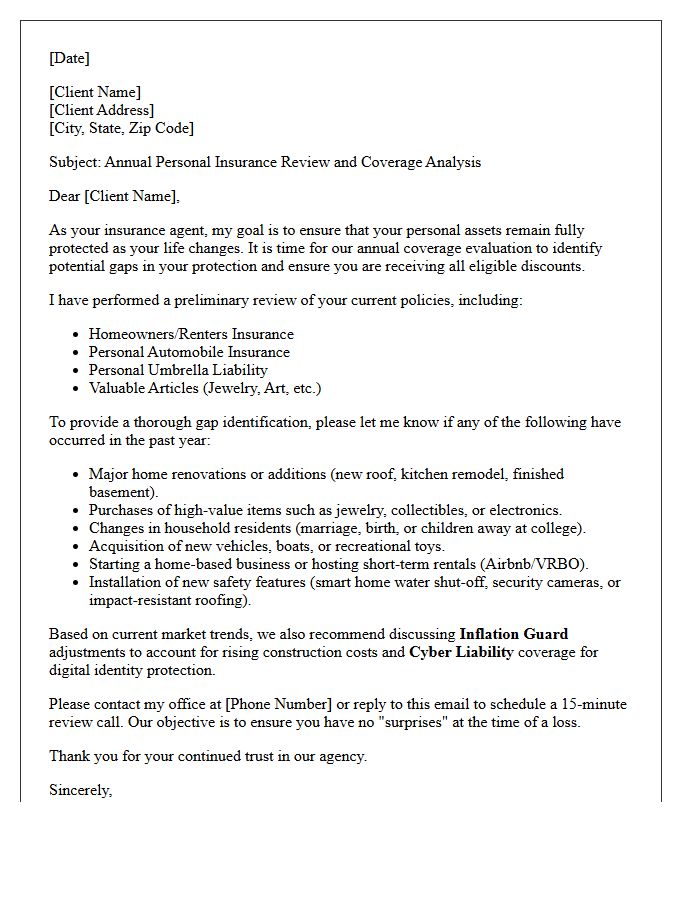

Personal Lines Annual Coverage Evaluation and Gap Identification Letter

A Personal Lines Annual Coverage Evaluation and Gap Identification Letter is a critical document used to assess insurance adequacy. It highlights potential coverage gaps between your current policy limits and your actual exposure to risks like inflation, property upgrades, or new liabilities. Reviewing this letter ensures your assets remain fully protected and prevents financial shortfalls during a claim. Regular evaluations are essential to mitigate underinsurance and adapt your protection to life changes, ensuring your personal insurance portfolio remains robust, comprehensive, and tailored to your evolving needs.

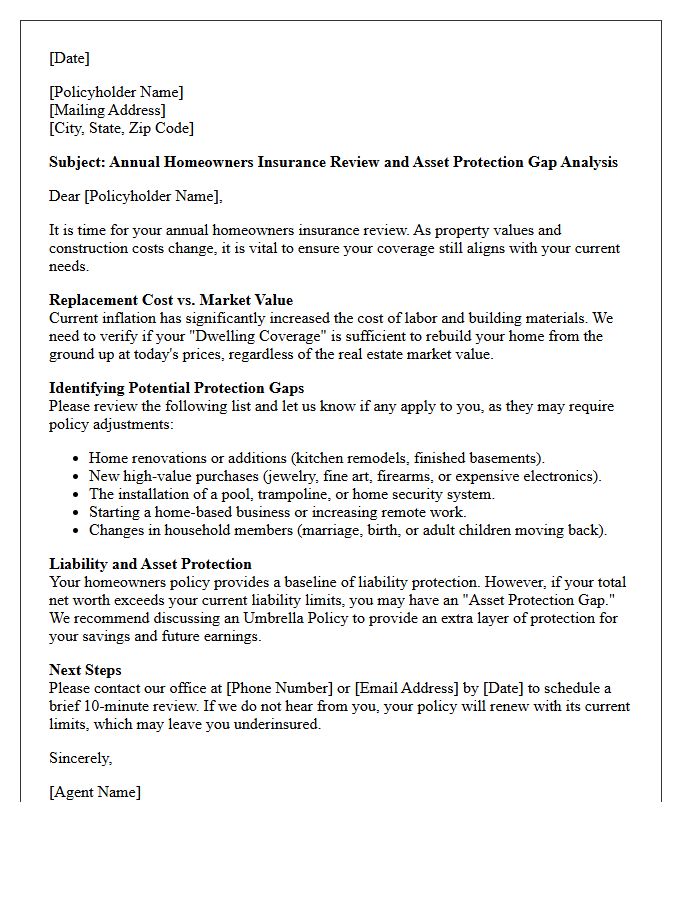

Homeowners Policy Annual Review and Asset Protection Gap Letter

A Homeowners Policy Annual Review ensures your coverage keeps pace with rising construction costs and home improvements. Without regular updates, you risk a significant Asset Protection Gap, leaving your personal wealth vulnerable to lawsuits or total loss. An annual review identifies undervalued limits and missing endorsements. Receiving an Asset Protection Gap Letter serves as a formal warning that your current policy may not fully shield your net worth against catastrophic liability. Bridging this gap is essential to maintaining financial security and ensuring your most valuable investments remain fully insured.

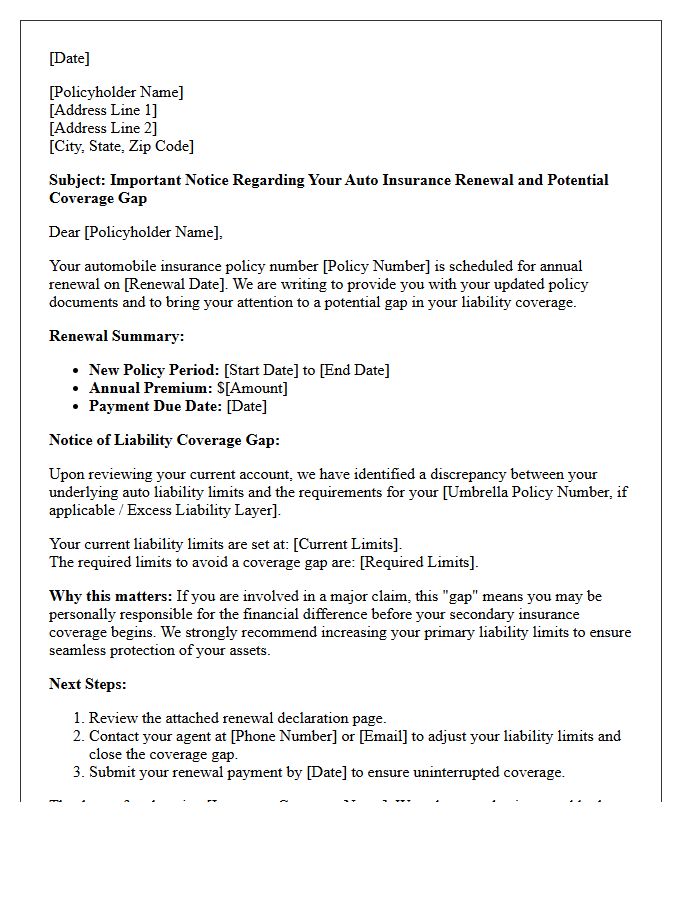

Auto Insurance Annual Renewal and Liability Coverage Gap Letter

An auto insurance annual renewal ensures continuous protection, but a Liability Coverage Gap Letter signifies a dangerous lapse in your policy. If your coverage expires before renewing, you face legal penalties and financial vulnerability. This formal notice warns that you lack financial responsibility, which can lead to license suspension or vehicle registration blocks. Maintaining uninterrupted liability coverage is essential to avoid being flagged by state databases. Always review renewal terms promptly to prevent gaps, ensuring your legal compliance and protecting your assets from potential third-party claims during unforeseen accidents.

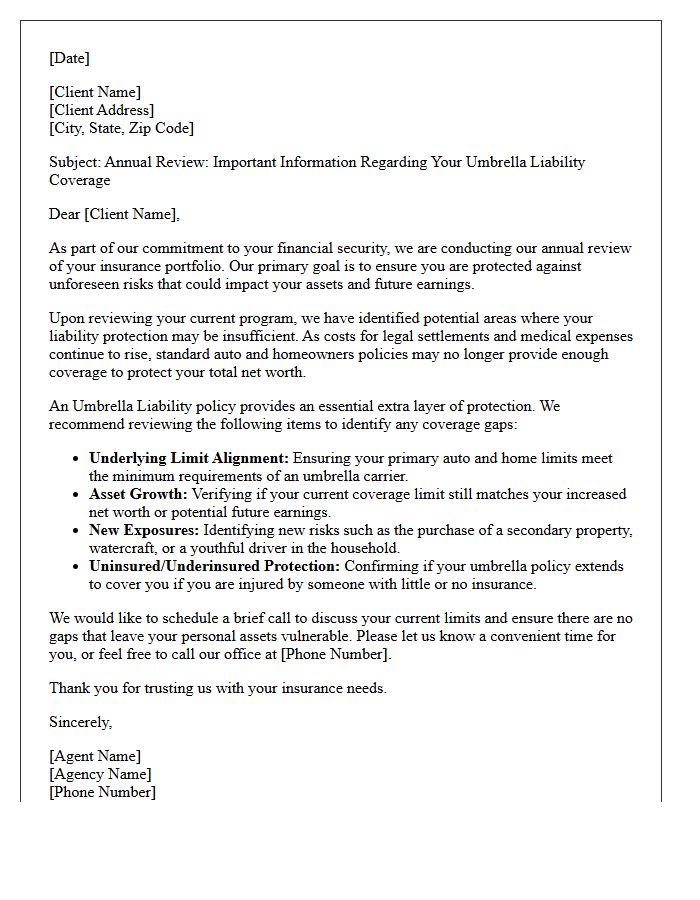

Umbrella Liability Coverage Gap Identification and Annual Review Letter

Conducting an annual insurance review is essential to identify potential coverage gaps between primary policies and your umbrella liability layer. As underlying limits change or assets increase, a rigorous gap identification process ensures continuous protection against catastrophic loss. This formal review letter documents necessary adjustments to your auto, home, or watercraft policies, maintaining the specific retention levels required by your excess carrier. Failure to align these limits can lead to significant out-of-pocket expenses, making proactive evaluation the most effective strategy for comprehensive risk management and personal financial security.

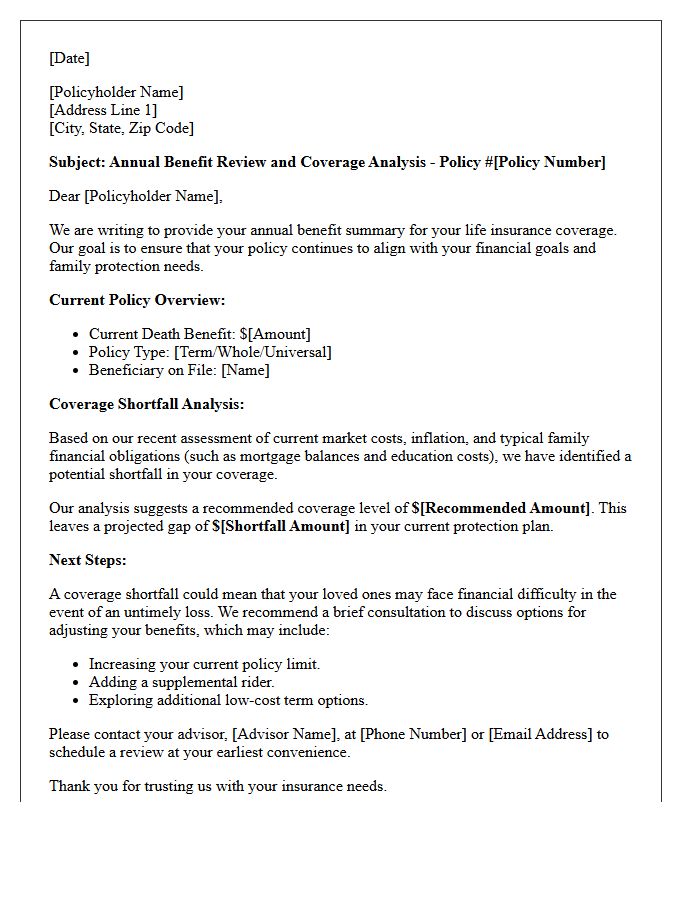

Life Insurance Annual Benefit Review and Coverage Shortfall Letter

A Life Insurance Annual Benefit Review identifies gaps between your current policy and evolving financial needs. If your death benefit no longer covers debts or family expenses, you may receive a Coverage Shortfall Letter. This document acts as a formal alert that your existing protection is insufficient. Regularly reviewing these statements ensures your beneficiaries remain fully protected against inflation or lifestyle changes. Addressing a shortfall promptly prevents financial hardship, allowing you to adjust premiums or increase coverage to maintain long-term security for your loved ones.

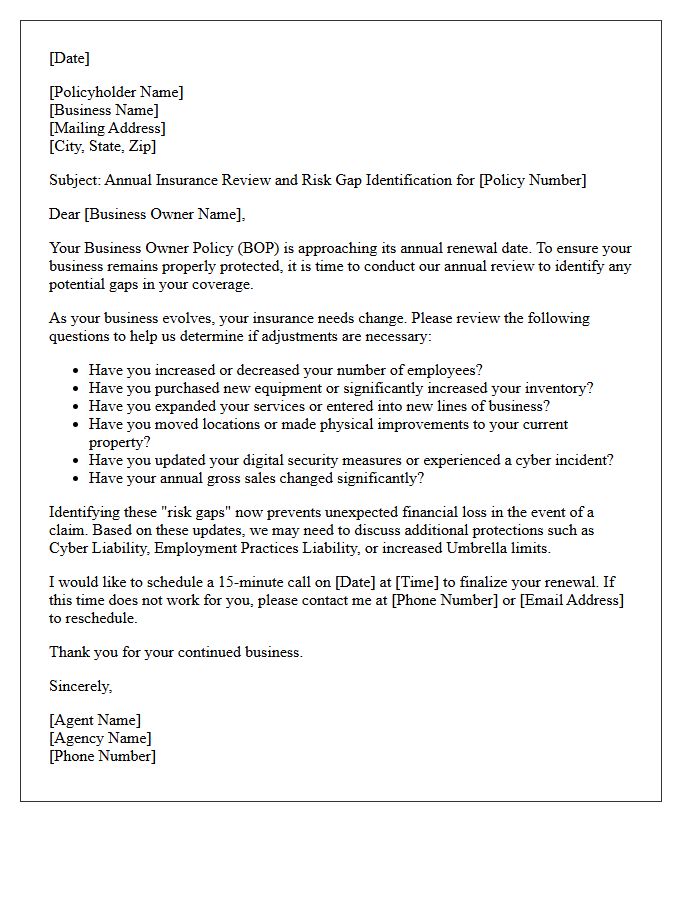

Business Owner Policy Annual Review and Risk Gap Identification Letter

An annual review of your Business Owner Policy (BOP) is critical for identifying risk gaps that emerge as your company evolves. This proactive assessment ensures your coverage limits align with current asset values and operational changes. By formalizing this process through a Risk Gap Identification Letter, you document potential vulnerabilities and necessary adjustments. Regular evaluations prevent underinsurance, protect against new liabilities, and ensure your business continuity remains secure. Staying updated on policy terms mitigates financial exposure and maintains robust protection in a shifting market landscape.

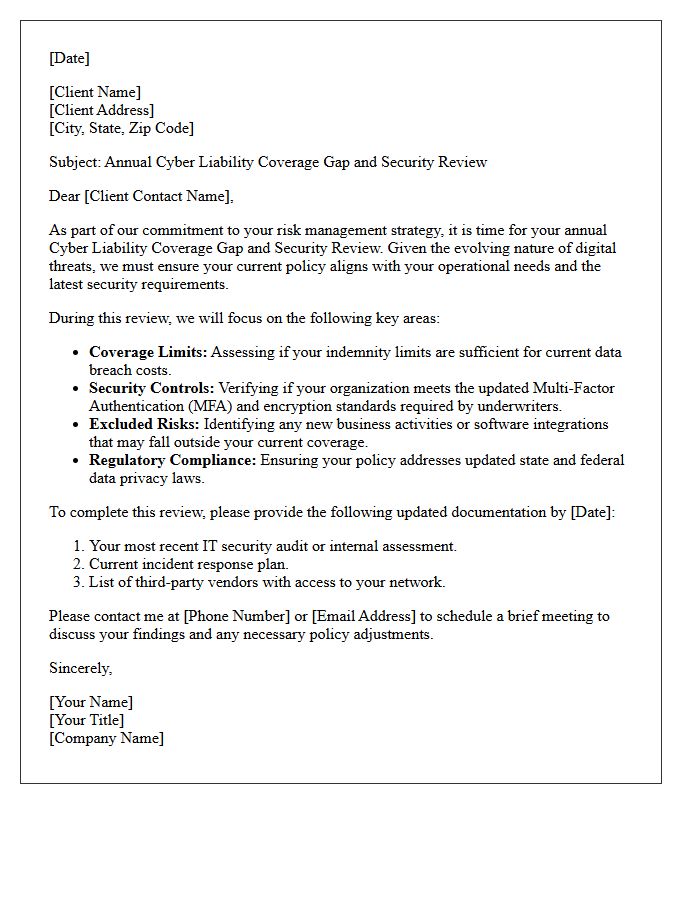

Cyber Liability Annual Coverage Gap and Security Review Letter

A Cyber Liability Annual Coverage Gap and Security Review Letter is a critical document used to identify insurance deficiencies and technical vulnerabilities. This formal assessment ensures your current policy aligns with evolving digital threats and regulatory requirements. By performing this review, organizations can address unprotected risks, verify security controls, and prevent costly financial losses during a data breach. Regularly updating this letter is essential for maintaining comprehensive risk management and ensuring that your business remains resilient against sophisticated cyberattacks and unforeseen liability exposures.

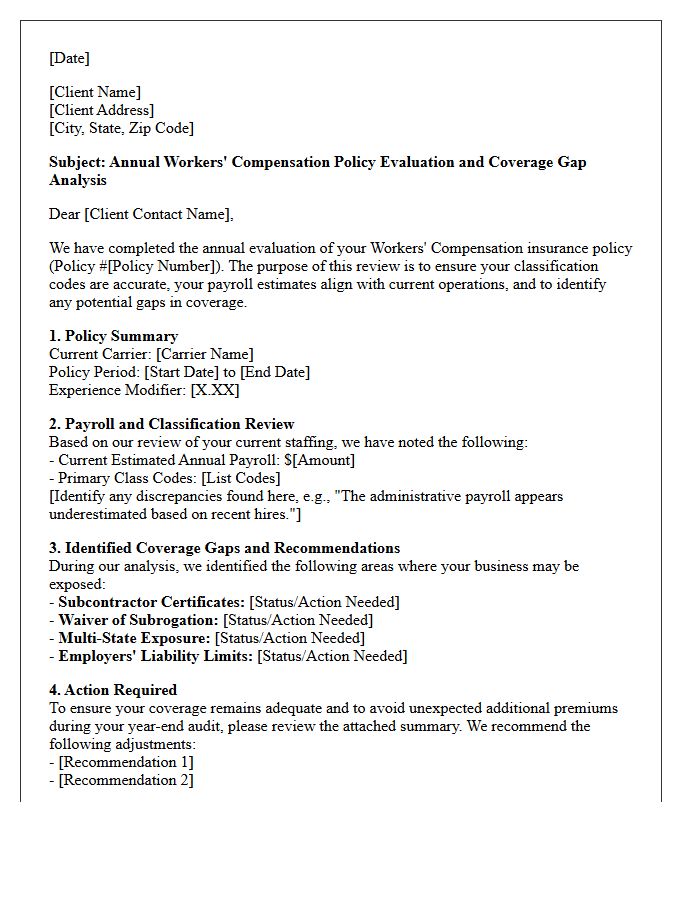

Workers Compensation Annual Policy Evaluation and Gap Letter

A Workers Compensation Annual Policy Evaluation ensures your business maintains accurate payroll classifications and stays compliant with state laws. This systematic review identifies potential overpayments or coverage deficiencies before they become liabilities. Following the evaluation, a Gap Letter serves as a critical document highlighting specific insurance vulnerabilities and recommended corrections. Understanding these reports helps employers mitigate financial risks, prepare for audits, and ensure employees are properly protected. Regular assessments are essential to align your policy with current operational realities and avoid unexpected penalties or premium hikes.

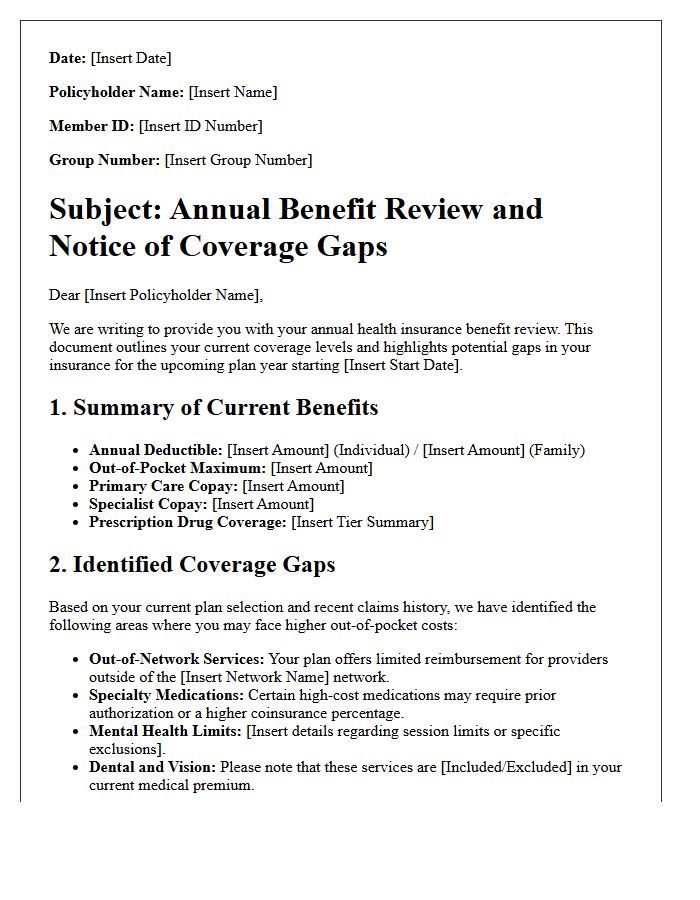

Health Insurance Annual Benefit Review and Coverage Gap Letter

An Annual Benefit Review is a critical evaluation of your health insurance coverage, ensuring it aligns with your current medical needs. It identifies a coverage gap, which occurs when there is a temporary limit in policy protection, potentially increasing out-of-pocket costs for prescriptions or treatments. Receiving a Coverage Gap Letter is a formal notification that you have reached these limits. Understanding these documents is essential for financial planning and making informed adjustments during open enrollment to maintain continuous, comprehensive healthcare protection without unexpected expenses.

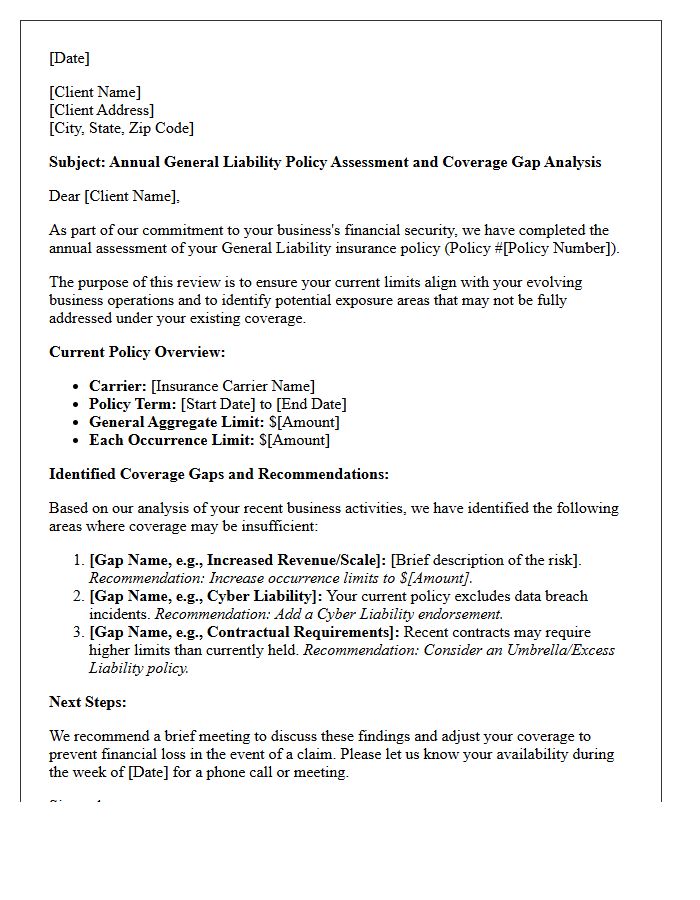

General Liability Annual Policy Assessment and Coverage Gap Letter

A General Liability Annual Policy Assessment is a critical review ensuring your business protection aligns with current operations. This process identifies exposures that emerged during the year, preventing costly underinsurance. Following the assessment, a Coverage Gap Letter highlights specific vulnerabilities where existing policies fail to provide security. Understanding these documents is essential for risk mitigation, as they document professional advice and pinpoint necessary endorsements. Addressing these findings promptly ensures continuous financial protection and prevents legal liabilities from unforeseen incidents that fall outside your standard policy terms.

What is the purpose of the Annual Policy Review and Coverage Gap Identification Letter?

The primary purpose of this letter is to provide a comprehensive evaluation of your current insurance portfolio to ensure your protection aligns with your evolving lifestyle and to identify any potential risks where your current coverage may be insufficient.

Why is it necessary to conduct an annual review if my policy hasn't changed?

While your policy terms may remain the same, external factors such as inflation, increased property values, changes in local building codes, or personal life events (like home renovations or new asset acquisitions) can create significant gaps in your coverage over time.

What specific "coverage gaps" are typically identified during this process?

Common gaps include inadequate liability limits, outdated property valuations, lack of specialized riders for high-value items, and missing endorsements for specific perils like sewer backup, cyber liability, or updated ordinance and law requirements.

How does identifying coverage gaps benefit my long-term financial security?

By proactively addressing underinsured areas, you mitigate the risk of substantial out-of-pocket expenses following a loss. This ensures that your insurance serves as a reliable safety net, preventing personal financial depletion during a major claim event.

What information do I need to provide for a thorough policy assessment?

To ensure an accurate review, you should provide updates on any major purchases, structural improvements to your property, changes in household occupancy, and details of any new business activities conducted from your primary residence.

Comments