Receiving a Notice of Non-Renewal because of an uninsurable driver can jeopardize your auto policy. Insurance companies often terminate coverage when a high-risk individual is added to the household. Understanding how to address these eligibility issues is essential for maintaining protection. To help you respond formally to your insurer, below are some ready to use templates.

Image cover: Insurance Non-Renewal Notice: Including an Uninsurable Driver (Templates & Samples)

Letter Samples List

- Notice of Non-Renewal Due to Uninsurable Driver Letter

- Official Letter of Policy Non-Renewal for Unacceptable Driving Record

- Uninsurable Household Member Non-Renewal Notification Letter

- Letter of Non-Renewal Regarding Addition of Excluded Driver

- Insurance Agency Letter Informing Policyholder of Non-Renewal Due to High-Risk Driver

- High-Risk Driver Addition Policy Non-Renewal Letter

- Commercial Auto Non-Renewal Letter for Uninsurable Employee Addition

- Personal Auto Insurance Non-Renewal Letter Due to License Suspension of Added Driver

- Letter of Intent Not to Renew Following Uninsurable Driver Endorsement Request

- Final Notice Letter of Coverage Non-Renewal for Uninsurable Operator

- Standard Letter of Non-Renewal Based on Underwriting Guidelines for Added Drivers

- Unacceptable Risk Driver Addition Policy Non-Renewal Letter

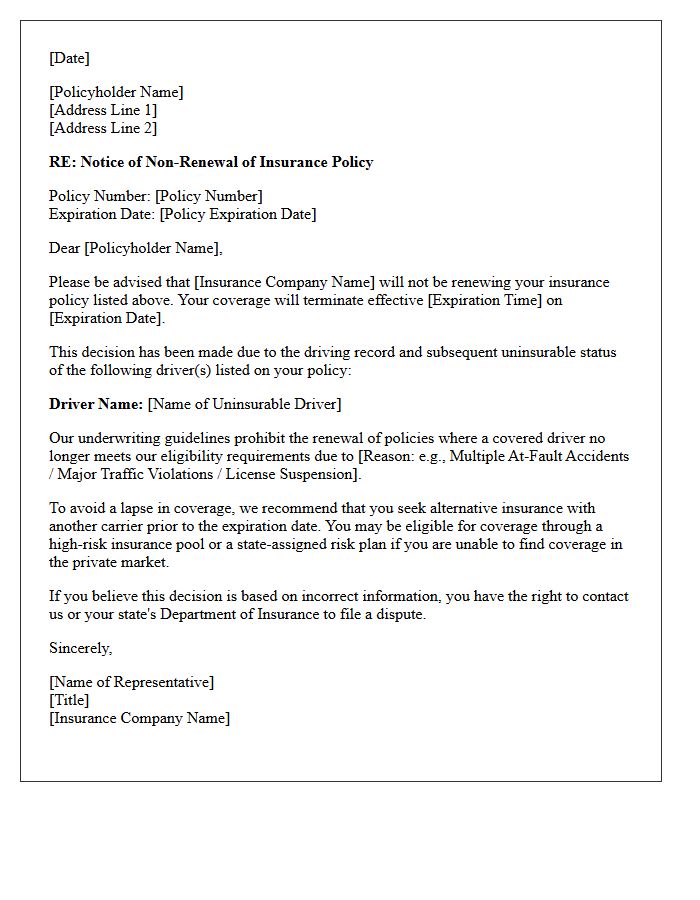

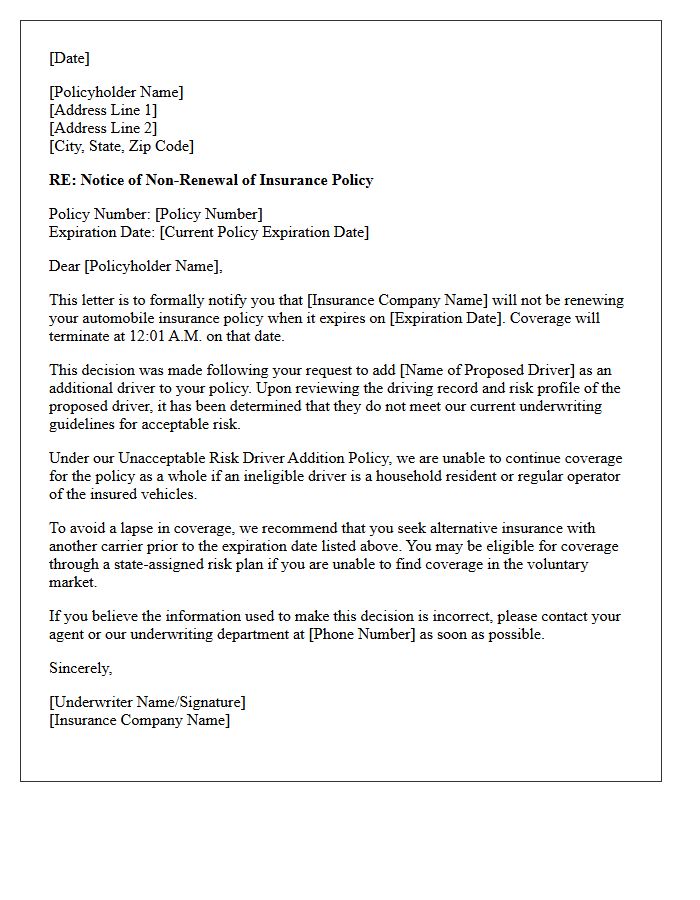

Notice of Non-Renewal Due to Uninsurable Driver Letter

A Notice of Non-Renewal due to an uninsurable driver is a formal legal document stating your insurance carrier will not extend coverage past the current policy expiration. This usually occurs when a household member's driving record includes severe violations, multiple accidents, or license suspensions that exceed the company's risk tolerance. Receiving this notice means you must secure alternative coverage immediately to avoid a lapse. To maintain your policy, you may be required to formally exclude the high-risk individual through a named driver exclusion, legally preventing them from operating your vehicles.

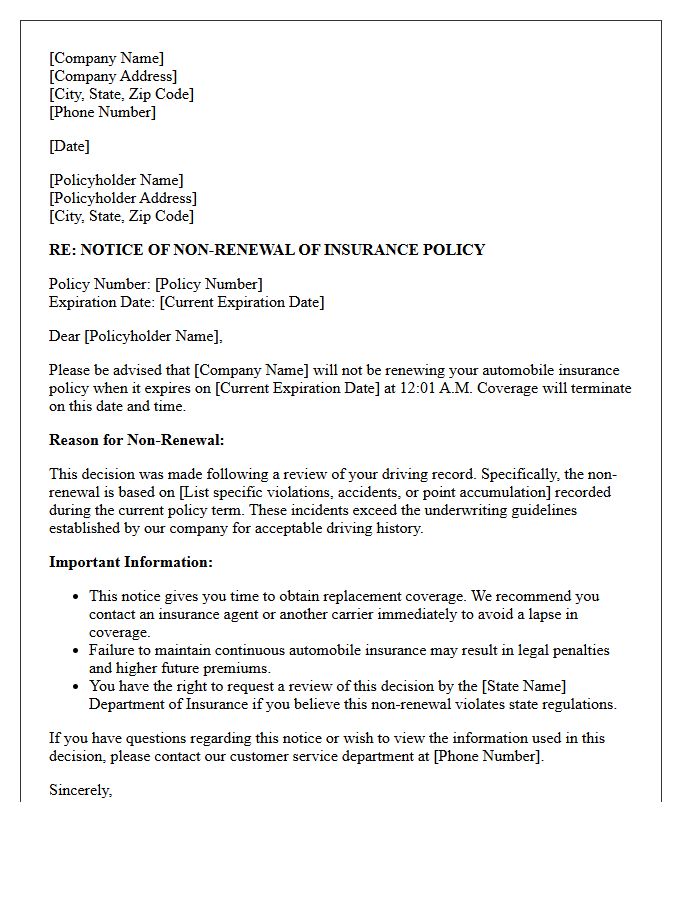

Official Letter of Policy Non-Renewal for Unacceptable Driving Record

An official letter of policy non-renewal for an unacceptable driving record serves as formal notice that your insurance provider will not extend coverage past the current expiration date. This decision typically results from multiple traffic violations, at-fault accidents, or serious infractions like a DUI. It is crucial to review the specified effective date to avoid a lapse in coverage. To maintain legal compliance, you should immediately compare alternative high-risk insurance providers or explore state-sponsored plans to secure new protection before your existing policy terminates.

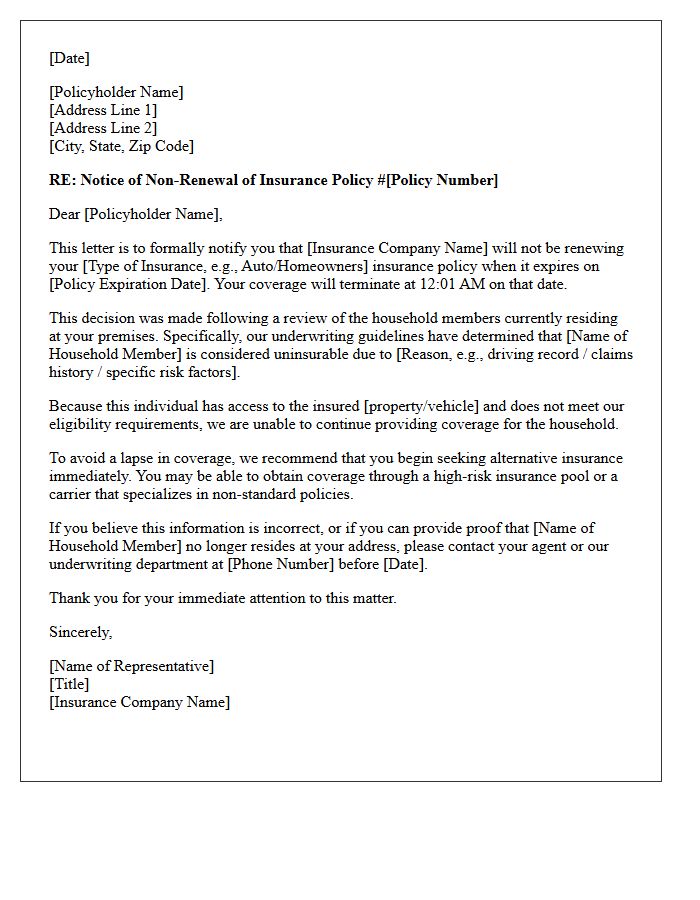

Uninsurable Household Member Non-Renewal Notification Letter

An Uninsurable Household Member Non-Renewal Notification Letter is a legal notice from an insurance carrier stating they will not renew a policy due to a high-risk individual in the home. This often occurs if a household member has a poor driving record, criminal history, or claims frequency that exceeds underwriting guidelines. To maintain coverage, homeowners or drivers may need to sign an Exclusion Endorsement, which legally removes the risky individual from the policy's protection. Failure to address this notice promptly can result in a total lapse in coverage.

Letter of Non-Renewal Regarding Addition of Excluded Driver

A Letter of Non-Renewal regarding an excluded driver informs you that your insurance policy will not be extended. This typically occurs because a high-risk individual in your household has a poor driving record, increasing the insurer's liability. By adding an exclusion, the company refuses to cover that person. If you fail to agree or the risk remains too high, the provider issues this formal notice. To maintain coverage, you must find a new carrier or prove the excluded driver no longer resides at your address.

Insurance Agency Letter Informing Policyholder of Non-Renewal Due to High-Risk Driver

A non-renewal notice informs policyholders that their coverage will end upon the current term's expiration. This legal document specifies that the insurance agency will no longer provide protection due to a high-risk driver listed on the policy. Common triggers include excessive traffic violations, at-fault accidents, or major infractions like DUIs. Upon receiving this letter, it is vital to secure new coverage immediately to avoid a lapse in insurance, as being classified as high-risk often requires seeking specialized non-standard carriers to maintain legal compliance and financial protection.

High-Risk Driver Addition Policy Non-Renewal Letter

A High-Risk Driver Addition Policy Non-Renewal Letter is a formal notice from an insurer stating they will not extend coverage due to the addition of a high-risk motorist. This typically occurs when a new driver with a poor driving record, major traffic violations, or multiple claims is added to the policy. The letter outlines the specific reasons for non-renewal and provides a legal notice period. To maintain legal compliance and continuous protection, policyholders must secure alternative auto insurance before the current term expires to avoid coverage gaps.

Commercial Auto Non-Renewal Letter for Uninsurable Employee Addition

Receiving a Commercial Auto Non-Renewal Letter often occurs when an uninsurable employee is added to your policy. Insurers evaluate driving records for high-risk violations or excessive accidents. If a new driver fails to meet safety standards, the carrier may deem the entire business risk unacceptable, leading to policy termination. To protect your coverage, always perform MVR background checks before hiring. If a non-renewal notice arrives, you must either exclude the specific driver via a restrictive endorsement or quickly secure alternative high-risk commercial insurance to avoid a dangerous lapse in legal protection.

Personal Auto Insurance Non-Renewal Letter Due to License Suspension of Added Driver

Receiving a personal auto insurance non-renewal letter due to an added driver's license suspension is a critical notification. Insurers view a suspended license as a significant increase in underwriting risk, often leading to the termination of the entire policy. To maintain coverage, you may need to officially exclude the high-risk individual or seek a new carrier. It is essential to act quickly before your current term expires to avoid a lapse in coverage, which could result in higher future premiums and legal complications while driving.

Letter of Intent Not to Renew Following Uninsurable Driver Endorsement Request

A Letter of Intent Not to Renew serves as a formal notice that your insurer will terminate coverage unless specific actions are taken. This often occurs following an uninsurable driver endorsement request, where the company identifies a high-risk individual on your policy. To maintain your insurance, you must legally exclude the high-risk driver from all coverage. Failure to sign the exclusion endorsement typically results in a total policy non-renewal, leaving you without protection. Promptly addressing this request is essential to avoid a lapse in your automotive insurance history.

Final Notice Letter of Coverage Non-Renewal for Uninsurable Operator

A Final Notice Letter of Coverage Non-Renewal for Uninsurable Operator is a formal legal notification from an insurance carrier. It states that a specific driver no longer meets underwriting safety standards due to high-risk factors like accidents or serious traffic violations. This document serves as a final alert that the current policy will expire on a set date without the possibility of extension. To maintain legal compliance, vehicle owners must immediately secure alternative insurance or exclude the high-risk operator to avoid a lapse in essential protection.

Standard Letter of Non-Renewal Based on Underwriting Guidelines for Added Drivers

A standard non-renewal notice for added drivers occurs when a new operator fails to meet specific underwriting guidelines. Insurance companies issue these letters when a driver's risk profile, such as a poor claims history or serious traffic violations, exceeds the policy's eligibility criteria. This formal notification outlines the legal intent to terminate coverage for that individual or the entire policy upon expiration. Policyholders must review these documents immediately to address safety concerns, provide missing information, or seek alternative insurance coverage to avoid a lapse in protection.

Unacceptable Risk Driver Addition Policy Non-Renewal Letter

An Unacceptable Risk Driver Addition Policy Non-Renewal Letter is a formal notice from an insurer stating they will not renew your coverage due to an ineligible driver added to the policy. This typically occurs when a household member has a poor driving record, multiple accidents, or serious violations like a DUI. To maintain protection, you may need to exclude the high-risk driver or switch to a non-standard carrier. Timely action is essential to avoid a lapse in coverage and ensure continuous financial protection on the road.

What is a Notice of Non-Renewal due to an uninsurable driver?

A Notice of Non-Renewal is a formal communication from your insurance carrier stating they will not extend your policy coverage past its expiration date because a high-risk driver has been added to your household or policy.

Why was my policy non-renewed after adding a specific driver?

Insurance companies evaluate risk based on the driving history of all household members; if a newly added driver has multiple accidents, major violations (like a DUI), or a suspended license, they may exceed the company's risk threshold, making the entire policy ineligible for renewal.

Can I keep my insurance if I exclude the uninsurable driver?

In many states, you can sign a Named Driver Exclusion, which legally removes the high-risk individual from your coverage; however, if that excluded person drives your vehicle and has an accident, the insurance company will provide no coverage for the claim.

How much notice must an insurance company give before non-renewing?

The required notice period varies by state but typically ranges from 30 to 60 days before the policy's expiration date to ensure you have sufficient time to find alternative coverage for your household.

What should I do if I receive a non-renewal notice for this reason?

You should immediately begin shopping for a new policy through a high-risk insurance specialist or an independent agent who can help you navigate "non-standard" carriers or explore state-sponsored Fair Access to Insurance Requirements (FAIR) plans.

Comments