Operating a commercial enterprise from a residential property often violates lease agreements and local zoning laws. Landlords must issue a Notice of Non-Renewal Due to Prohibited Business Operations to protect their property and ensure legal compliance. This guide explains how to document these violations professionally and legally terminate the tenancy. To simplify the process, below are some ready to use templates.

Image cover: Official Notice of Non-Renewal: Unauthorized Commercial Activity on Residential Premises

Letter Samples List

- Notice of Non-Renewal Letter for Prohibited Business Operations

- Personal Property Insurance Non-Renewal Letter Due to Business Use

- Letter of Non-Renewal for Unauthorized Commercial Activity on Residential Premises

- Insurance Agency Letter of Policy Non-Renewal for Prohibited Home Business

- Official Letter of Non-Renewal Due to Commercial Operations on Personal Property

- Prohibited Business Operations Non-Renewal Notice Letter

- Residential Policy Non-Renewal Letter Regarding Unauthorized Business Operations

- Letter of Insurance Non-Renewal for Unapproved Business Use of Personal Premises

- Notice Letter of Non-Renewal Due to Commercial Exposure on Personal Premises

- Policyholder Letter of Non-Renewal for Prohibited Commercial Operations

- Homeowners Insurance Non-Renewal Letter for Prohibited Business Activities

- Letter Declining Policy Renewal Due to Unauthorized Business on Premises

- Non-Renewal Letter for Prohibited Commercial Use of Personal Premises

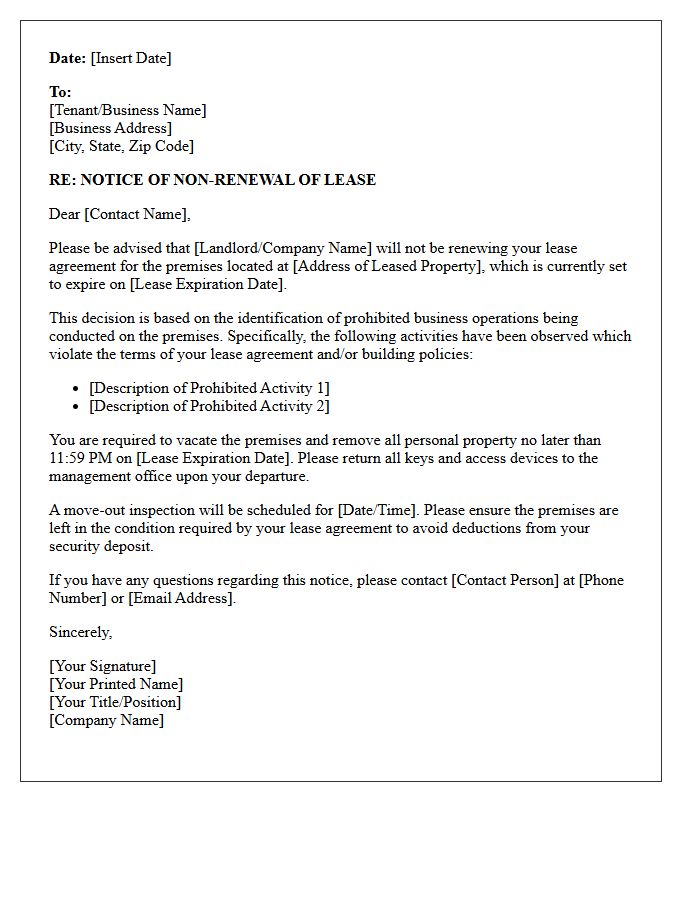

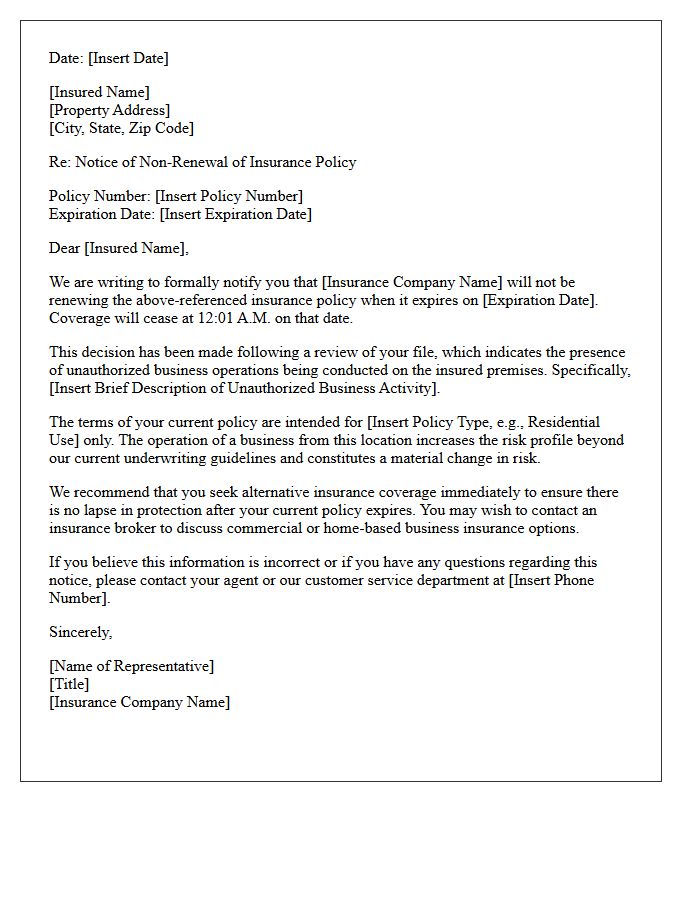

Notice of Non-Renewal Letter for Prohibited Business Operations

A Notice of Non-Renewal for prohibited business operations is a formal legal document issued by an insurer or landlord. It specifies that a contract will not be extended because current commercial activities violate specific policy terms or zoning laws. Receiving this notice means you must cease unauthorized operations or vacate the premises by the expiration date. To protect your interests, immediately review your original agreement to identify the exact compliance breach and consult legal counsel to negotiate a potential cure period or prepare for a structured operational transition.

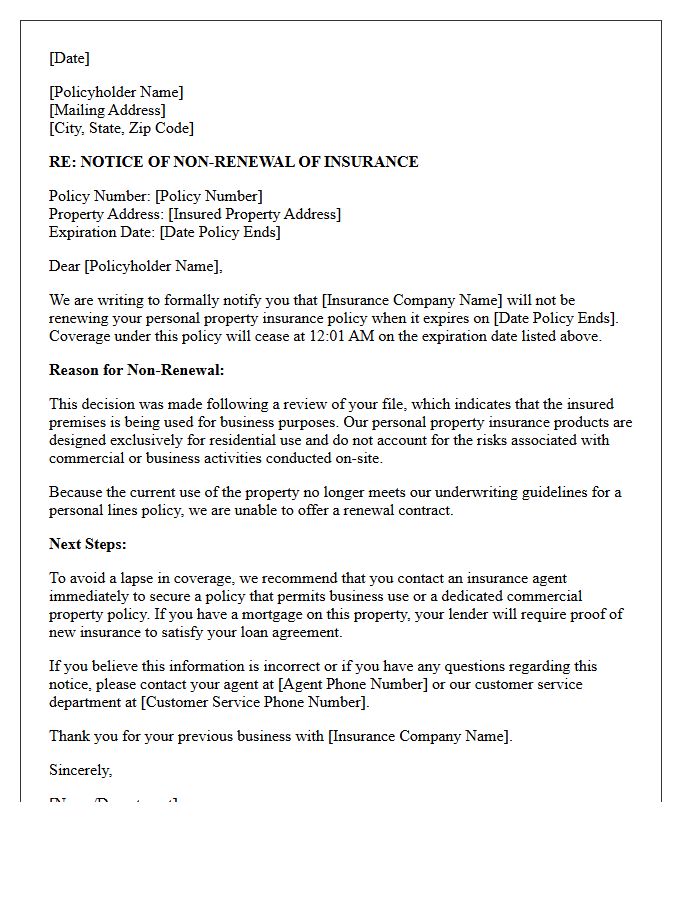

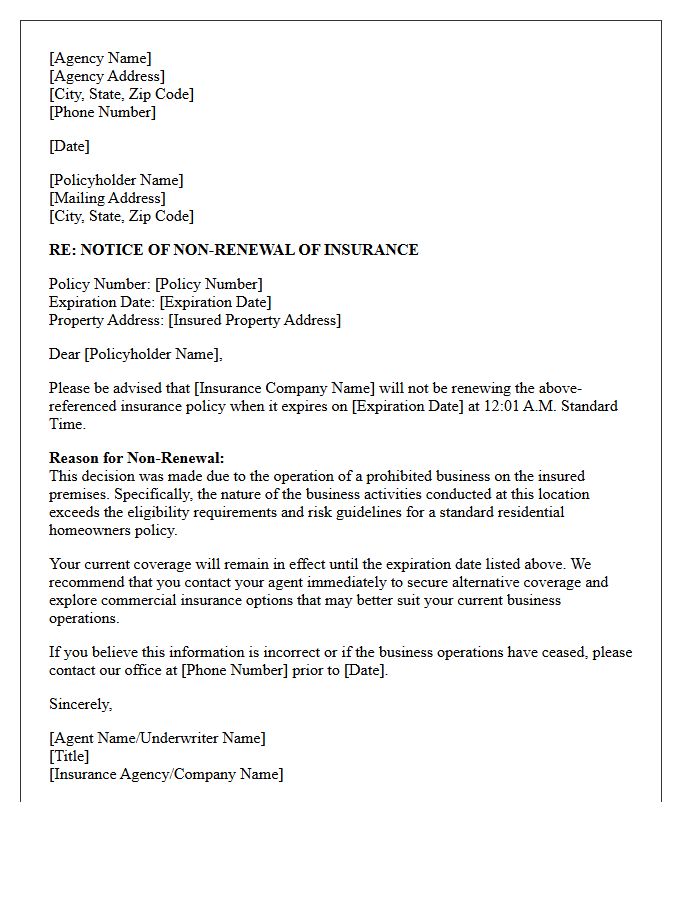

Personal Property Insurance Non-Renewal Letter Due to Business Use

Receiving a non-renewal letter for personal property insurance often occurs when a carrier discovers business use of the premises. Standard homeowners policies typically exclude high-risk commercial activities, such as client visits or inventory storage. To maintain coverage, you must disclose all home-based professional operations to your agent immediately. If your current policy is cancelled, you may need a specialized commercial endorsement or a separate business owners policy to protect your assets and liability. Always review your policy terms to ensure your professional equipment and activities are adequately insured without risking non-renewal.

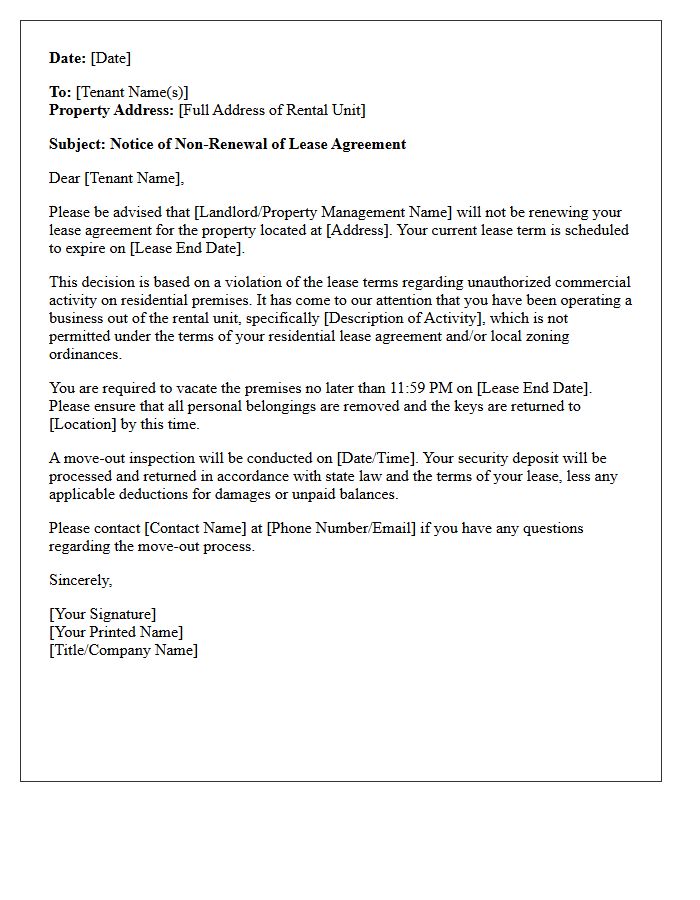

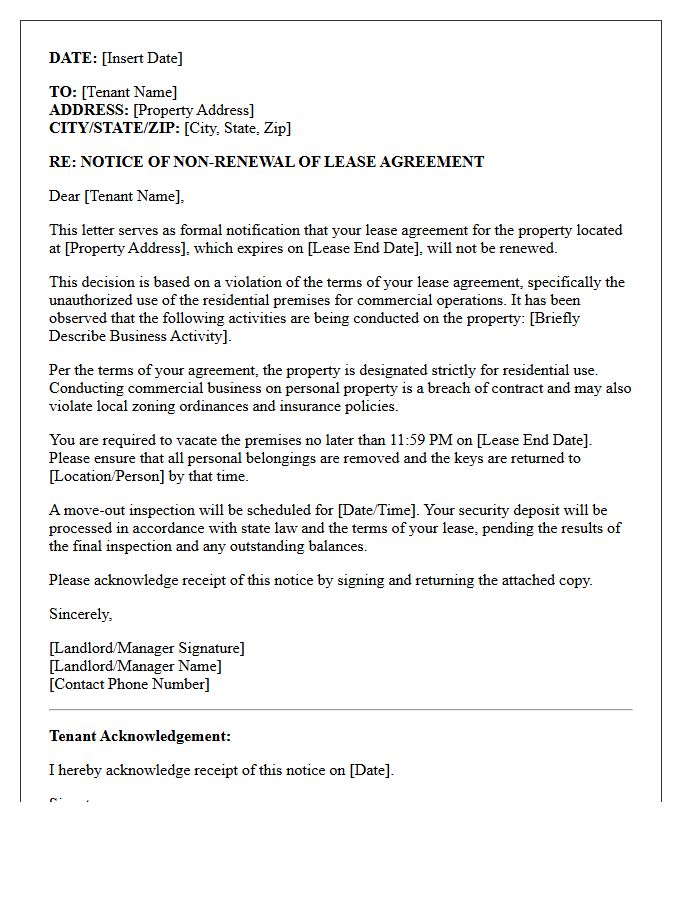

Letter of Non-Renewal for Unauthorized Commercial Activity on Residential Premises

A Letter of Non-Renewal for unauthorized commercial activity is a formal legal notice issued when a tenant operates a business from a residential property without permission. This document informs the occupant that their lease will not be extended due to a material breach of the rental agreement. Common triggers include excessive foot traffic, zoning violations, or increased liability risks. To ensure legal validity, landlords must provide clear evidence of the prohibited activity and adhere to specific notice periods required by local housing laws before the current lease term expires.

Insurance Agency Letter of Policy Non-Renewal for Prohibited Home Business

Receiving an insurance agency letter of policy non-renewal for a prohibited home business indicates your carrier discovered unapproved commercial activity on your property. Most standard homeowners policies strictly exclude liability and property risks associated with business operations. If your home-based venture violates underwriting guidelines, your coverage will terminate at the end of the term. To maintain protection, you must immediately seek a commercial endorsement or a separate business owner's policy to address these specific risks and avoid a dangerous lapse in coverage.

Official Letter of Non-Renewal Due to Commercial Operations on Personal Property

Receiving an Official Letter of Non-Renewal signifies that your insurance provider will not extend your policy due to commercial operations conducted on a residential property. Most personal homeowners policies strictly exclude business activities. If you run a trade, store inventory, or host clients at home without a specific endorsement, you violate standard policy terms. To maintain protection, you must immediately seek commercial liability insurance or a home-business rider to address these increased risks and ensure continuous legal compliance and financial coverage for your assets.

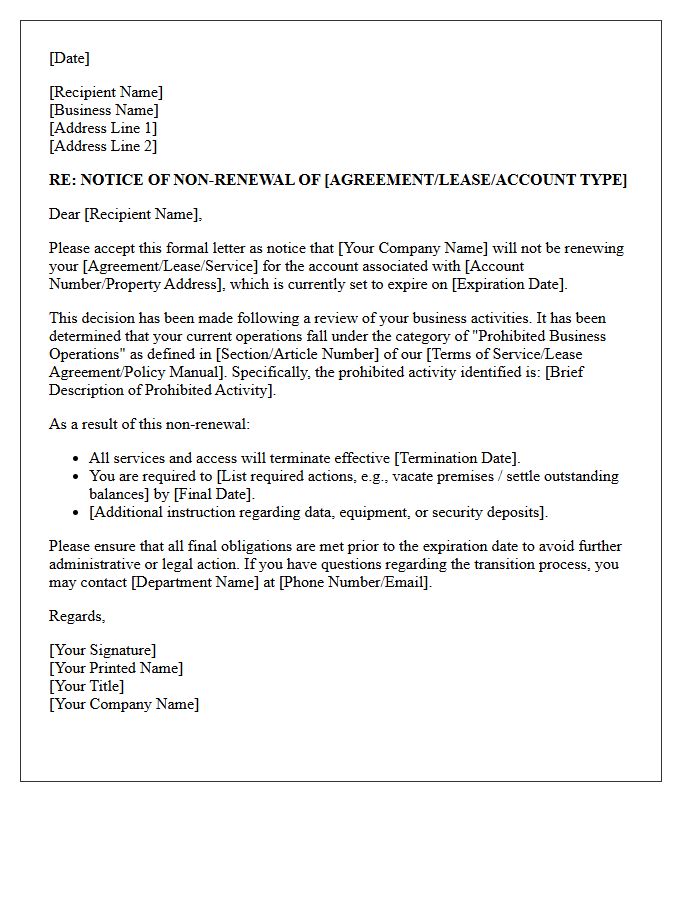

Prohibited Business Operations Non-Renewal Notice Letter

A Prohibited Business Operations Non-Renewal Notice Letter is a formal document notifying a policyholder that their insurance coverage will not be extended. This typically occurs when a company determines that the client's activities fall under restricted categories or high-risk sectors defined by underwriting guidelines. Key information includes the specific termination date and the regulatory reasons for the decision. It is crucial to review this notice immediately to secure alternative coverage and avoid a lapse in protection for your business assets and liabilities.

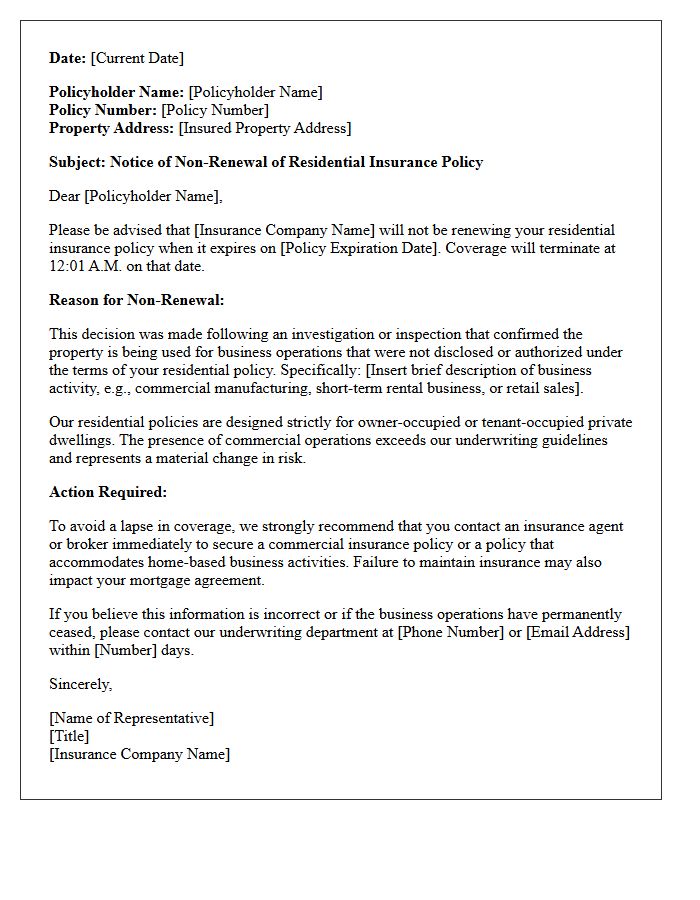

Residential Policy Non-Renewal Letter Regarding Unauthorized Business Operations

A residential policy non-renewal letter regarding unauthorized business operations serves as formal notice that an insurer is terminating coverage. This occurs when a policyholder operates a commercial enterprise from a home without proper disclosure or endorsements. Standard homeowners insurance typically excludes liability and property risks associated with business activities. Receiving this non-renewal notice means the carrier has determined the increased risk exceeds their underwriting guidelines. To protect your assets, you must secure a specialized business policy or seek a high-risk provider to maintain continuous protection before the current term expires.

Letter of Insurance Non-Renewal for Unapproved Business Use of Personal Premises

A Letter of Insurance Non-Renewal for unapproved business use occurs when a carrier discovers commercial activities on a residential property without a valid endorsement. Personal homeowner policies typically exclude coverage for business-related liabilities or equipment. If an inspection or claim reveals your home is used for unauthorized commercial purposes, the insurer may deem the risk too high to continue coverage. To maintain protection, always disclose home-based businesses to ensure your policy is properly rated or to secure a commercial rider that prevents unexpected policy termination and coverage gaps.

Notice Letter of Non-Renewal Due to Commercial Exposure on Personal Premises

A Notice Letter of Non-Renewal is issued when an insurer identifies commercial exposure on a property covered by a personal homeowners policy. This typically occurs when a business is operated from the premises, increasing liability risks beyond standard residential limits. To protect your coverage, you must address the underwriting concerns or transition to a commercial insurance policy. Failure to secure appropriate coverage may lead to a lapse, leaving your assets unprotected against business-related claims or property damage. Professional risk assessment is essential to ensure your policy aligns with your property's actual use.

Policyholder Letter of Non-Renewal for Prohibited Commercial Operations

A Policyholder Letter of Non-Renewal for prohibited commercial operations is a formal notice issued by an insurer terminating coverage. This action typically occurs when a policyholder engages in unauthorized business activities that exceed the policy's risk profile or legal boundaries. It is crucial to review the specified underwriting guidelines to understand the violation. Receiving this letter requires immediate action to secure alternative insurance, as a gap in coverage can lead to significant financial liability and legal complications for your enterprise. Always ensure your operations align with your policy terms to maintain continuous protection.

Homeowners Insurance Non-Renewal Letter for Prohibited Business Activities

Receiving a non-renewal letter for prohibited business activities means your insurer has identified commercial operations on your property that exceed policy limits. Standard residential coverage excludes high-risk business ventures, such as frequent client visits, hazardous material storage, or manufacturing. To maintain protection, you must immediately address these concerns or transition to a specialized commercial insurance policy. Failure to secure alternative coverage following a non-renewal can lead to a dangerous lapse in insurance, leaving your property and personal assets vulnerable to significant financial loss and liability claims.

Letter Declining Policy Renewal Due to Unauthorized Business on Premises

If you receive a notice declining your policy renewal, it is typically because an unauthorized business was discovered operating on your residential premises. Standard homeowners insurance excludes commercial activities due to increased liability risks and zoning violations. This breach of contract makes the property ineligible for standard coverage. To resolve this, you must cease all business operations or transition to a commercial insurance policy that specifically covers business-related equipment, visitors, and professional liability. Promptly addressing this non-renewal is essential to avoid a lapse in mandatory property protection.

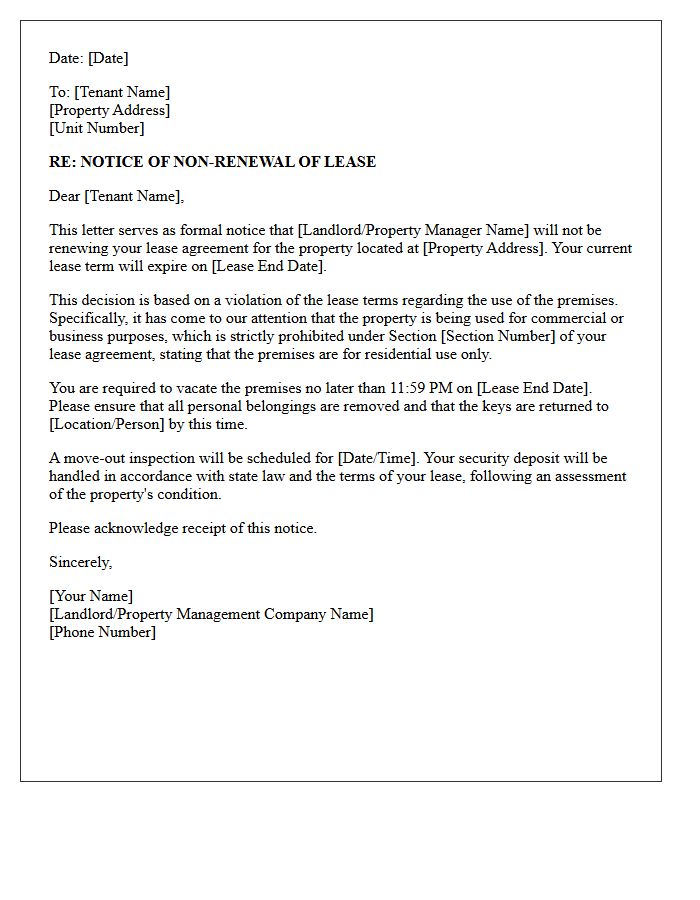

Non-Renewal Letter for Prohibited Commercial Use of Personal Premises

A non-renewal letter for prohibited commercial use notifies a tenant that their lease will not be extended due to unauthorized business activities on residential property. Landlords issue this notice when a tenant violates zoning laws or lease terms by operating a commercial enterprise from a personal dwelling. This legal document protects owners from liability and potential fines. It is essential to provide the specific termination date and evidence of the breach to ensure compliance with local housing regulations and to facilitate a smooth transition during the eviction process or move-out period.

What is a Notice of Non-Renewal for prohibited business operations?

A Notice of Non-Renewal for prohibited business operations is a formal legal document issued by a landlord or property manager informing a tenant that their lease agreement will not be extended because they are conducting unauthorized commercial activities on a property zoned or leased strictly for residential use.

Can I be evicted for running a business out of my apartment?

Yes, if your lease agreement contains a "residential use only" clause, operating a business can be considered a material breach of contract. While a non-renewal notice ends the lease at its natural expiration, continued violation of business prohibitions can lead to formal eviction proceedings before the lease ends.

What types of business activities typically trigger a non-renewal notice?

Activities that typically trigger non-renewal include those that increase foot traffic, create noise disturbances, involve hazardous materials, or violate local zoning ordinances. Common examples include operating a retail storefront, professional daycare services without permits, or using a residential garage for automotive repair.

How much notice must a landlord provide for non-renewal due to business use?

The notice period varies by state and local jurisdiction, but it typically ranges from 30 to 60 days before the lease expiration date. The specific timeframe must adhere to both the terms outlined in your original lease agreement and local landlord-tenant laws.

Can I dispute a non-renewal notice if my business is remote or digital?

Generally, "passive" home office use (such as remote computer work) is permitted in most residential leases. However, if the non-renewal is based on specific prohibited operations, you may dispute it by providing evidence that your activity does not violate zoning laws, impact neighbors, or breach the specific "prohibited business" definitions in your lease.

Comments