Receiving a Notice of Non-Renewal occurs when an insurer discovers your personal auto policy is being used for business activities. Standard policies typically exclude coverage for delivery or ride-sharing services without specific endorsements. This article explains how to address these violations and maintain your coverage eligibility. To help you respond effectively, below are some ready to use template.

Image cover: Notice of Non-Renewal: Unauthorized Commercial Use of Personal Vehicle Templates

Letter Samples List

- Insurance Agency Letterhead

- Official Letter Date

- Policyholder Name and Mailing Address

- Formal Letter Subject Line

- Insurance Policy Number and Coverage Period

- Notice of Non-Renewal Declaration

- Vehicle Identification Number and Description

- Discovery of Prohibited Commercial Use

- Violation of Personal Auto Policy Terms

- Effective Date of Policy Expiration

- State Department of Insurance Appeal Rights

- Instructions for Securing Commercial Coverage

- Insurance Agent Contact Information

- Official Letter Signature

Insurance Agency Letterhead

An Insurance Agency Letterhead serves as a vital tool for establishing professional authority and legal credibility. It must prominently display the agency name, physical address, and licensing information to ensure regulatory compliance. Using a clean design with high-quality branding reinforces client trust during formal policy correspondence. Including contact details like phone numbers and email addresses ensures seamless communication. A well-structured layout reflects accountability and helps distinguish official documentation from unsolicited mail, making it an essential component of professional insurance representation and long-term brand recognition.

Official Letter Date

The official letter date serves as a vital chronological marker for legal and professional records. It establishes when a document was formally issued, directly influencing deadlines, contractual obligations, and notice periods. To ensure clarity, use a full format like "October 24, 2023" to avoid international misinterpretation. Placing the date at the top of the correspondence creates an authoritative timeline, which is essential for tracking communication history and maintaining compliance in formal proceedings.

Policyholder Name and Mailing Address

The Policyholder Name and Mailing Address represent the primary identity and contact details linked to an insurance contract. It is crucial that the named insured reflects the legal entity or individual owning the policy to ensure valid coverage. Accurate mailing information guarantees the timely delivery of legal notices, billing statements, and renewal documents. Any discrepancy in these details can lead to communication failures or claims processing delays. Always verify that this information is current to maintain continuous protection and receive essential policy updates from your insurer.

Formal Letter Subject Line

A formal letter subject line must be concise and specific to ensure professional clarity. It serves as the first impression, summarizing the purpose of your correspondence in a single glance. Always place it between the salutation and the body text, using a clear font. Including relevant details like a job title or reference number helps the recipient categorize your request efficiently. A well-crafted subject line improves readability and ensures your message is prioritized, demonstrating respect for the reader's time while maintaining a structured, academic, or business-oriented tone.

Insurance Policy Number and Coverage Period

Your Insurance Policy Number is a unique identifier essential for accessing benefits and filing claims. It confirms your active status within the provider's database. The Coverage Period specifies the exact timeframe during which your protection remains valid. Understanding these details ensures you know when your legal protection begins and ends, preventing costly lapses in security. Always verify these dates to maintain continuous financial indemnity against unforeseen risks and to ensure you are fully protected during a loss.

Notice of Non-Renewal Declaration

A Notice of Non-Renewal Declaration is a formal legal document issued by an insurer or landlord stating that a contract will not be extended beyond its expiration date. Unlike a cancellation, non-renewal occurs at the end of the term, often requiring a specific notice period as mandated by local laws. It is essential to review the stated reasons and effective date to ensure compliance or to secure alternative coverage. Timely communication is critical to avoid a lapse in protection or legal tenancy rights.

Vehicle Identification Number and Description

A Vehicle Identification Number (VIN) is a unique 17-character code serving as a car's fingerprint. It provides a detailed vehicle description, including the manufacturer, engine type, and assembly plant. This alphanumeric string is essential for tracking vehicle history, identifying theft, and managing safety recalls. You can typically find the VIN on the driver's side dashboard or door pillar. Understanding this code ensures you verify the authenticity and legal status of any automobile before purchase or service.

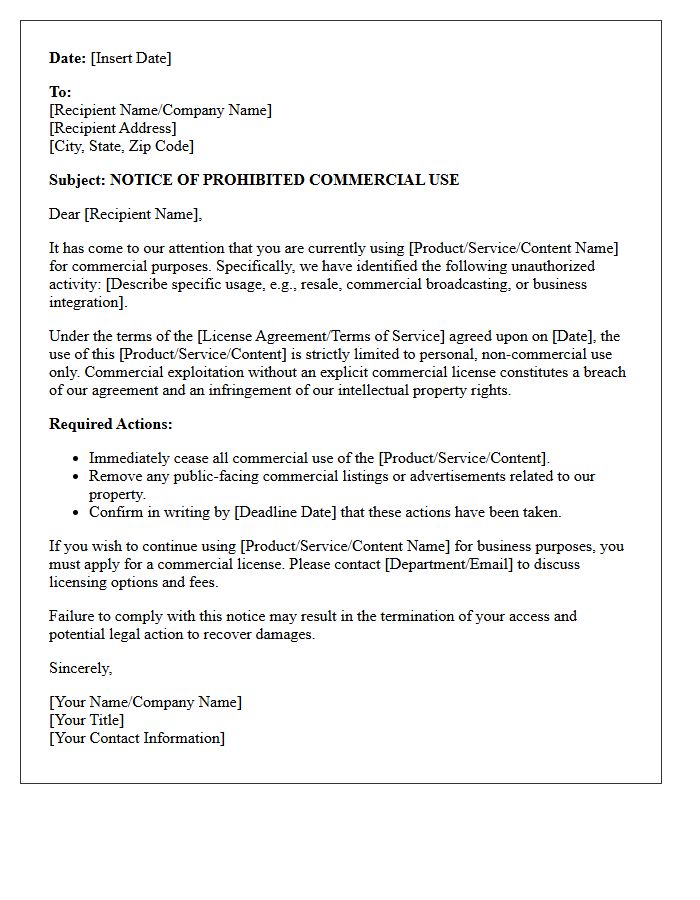

Discovery of Prohibited Commercial Use

The discovery of prohibited commercial use occurs when a licensor identifies that a product or service intended for personal or non-profit application is being utilized for financial gain without authorization. This breach often triggers legal consequences, including immediate license termination, statutory damages, and mandatory audits. Organizations must monitor compliance to avoid infringement claims. Understanding the specific terms of service is essential, as using proprietary assets for business purposes without a commercial license violates intellectual property rights and contractual agreements, leading to significant corporate liability.

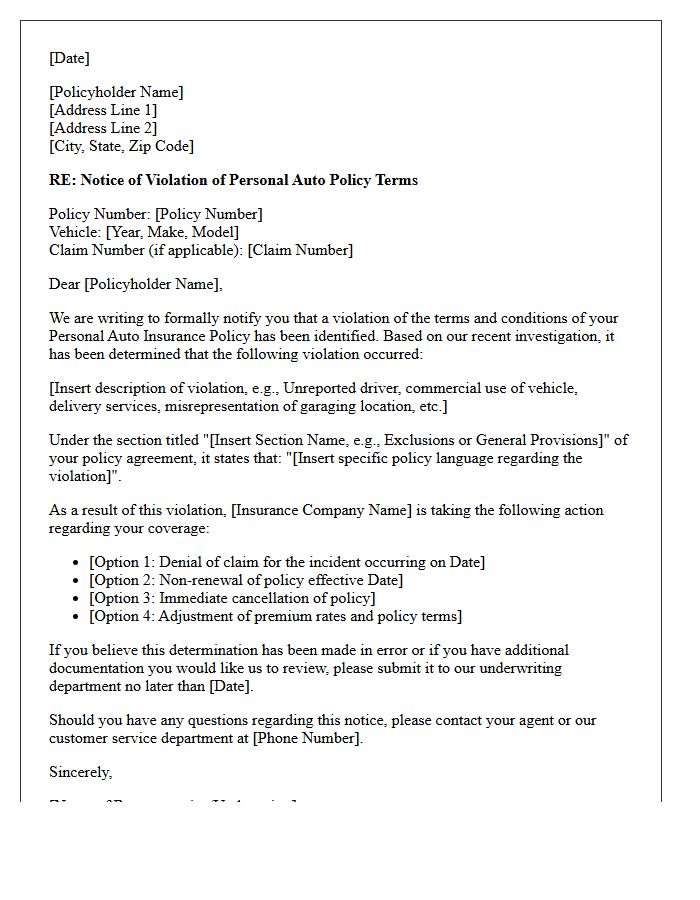

Violation of Personal Auto Policy Terms

A violation of Personal Auto Policy terms occurs when a policyholder breaches the contractual agreement with their insurer. Common triggers include material misrepresentation, failing to report accidents promptly, or using a private vehicle for commercial purposes like ride-sharing. Such violations can lead to a denial of coverage for claims, leaving the driver personally liable for damages. Furthermore, the insurance company may exercise its right to cancel the policy or refuse renewal, significantly impacting the individual's future insurability and premium rates. Always adhere to policy conditions to maintain valid financial protection.

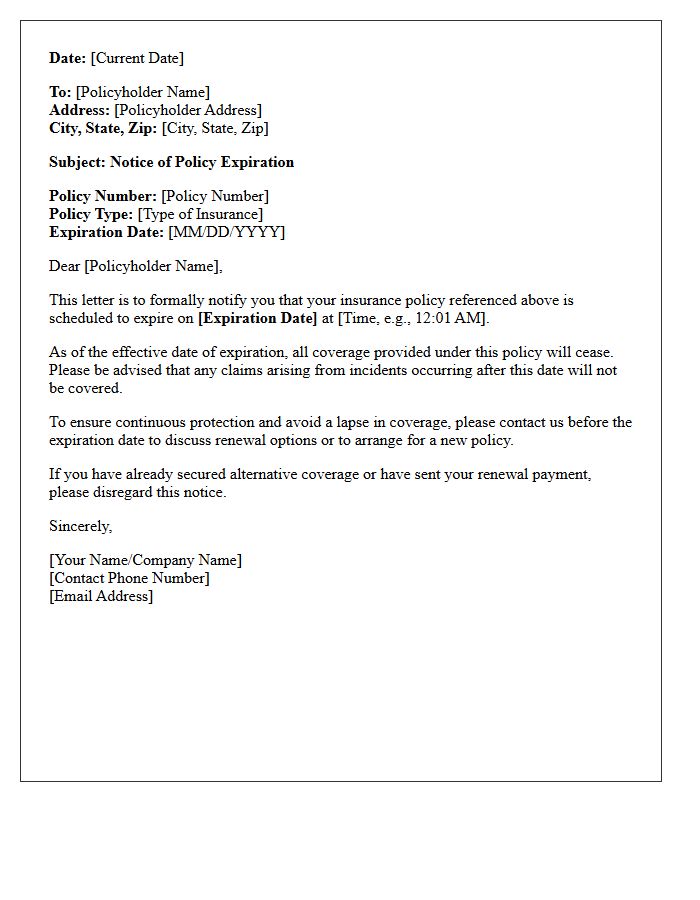

Effective Date of Policy Expiration

The Effective Date of Policy Expiration marks the exact moment insurance coverage terminates, leaving the policyholder without financial protection. This date is critical for maintaining continuous coverage to avoid risky gaps and potential legal penalties. It typically coincides with the end of a premium term, usually at 12:01 AM on the specified day. To prevent a lapse, policyholders must ensure a renewal or replacement policy begins immediately upon this expiration. Understanding this deadline is essential for maintaining seamless liability defense and asset protection throughout your insurance lifecycle.

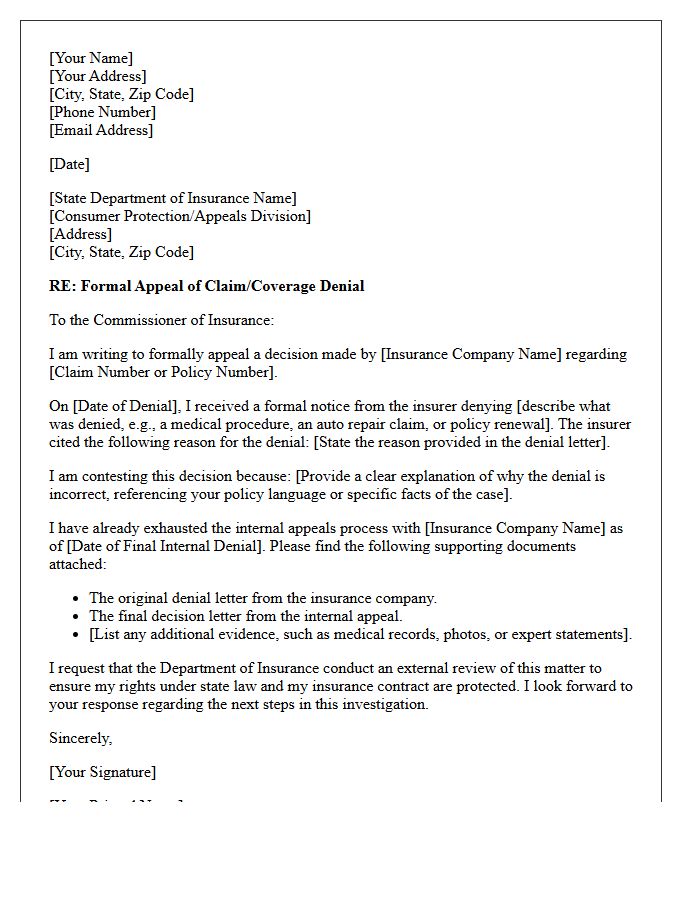

State Department of Insurance Appeal Rights

If your health claim is denied, you have protected appeal rights through your State Department of Insurance. After exhausting an internal review with your carrier, you can request an External Review. This process involves an independent third party who evaluates the medical necessity of the services. It is a vital consumer protection that ensures insurance companies follow state regulations and policy terms. Always monitor strict deadlines and keep detailed documentation, as this regulatory oversight provides a final pathway to overturn unfair denials and secure necessary coverage.

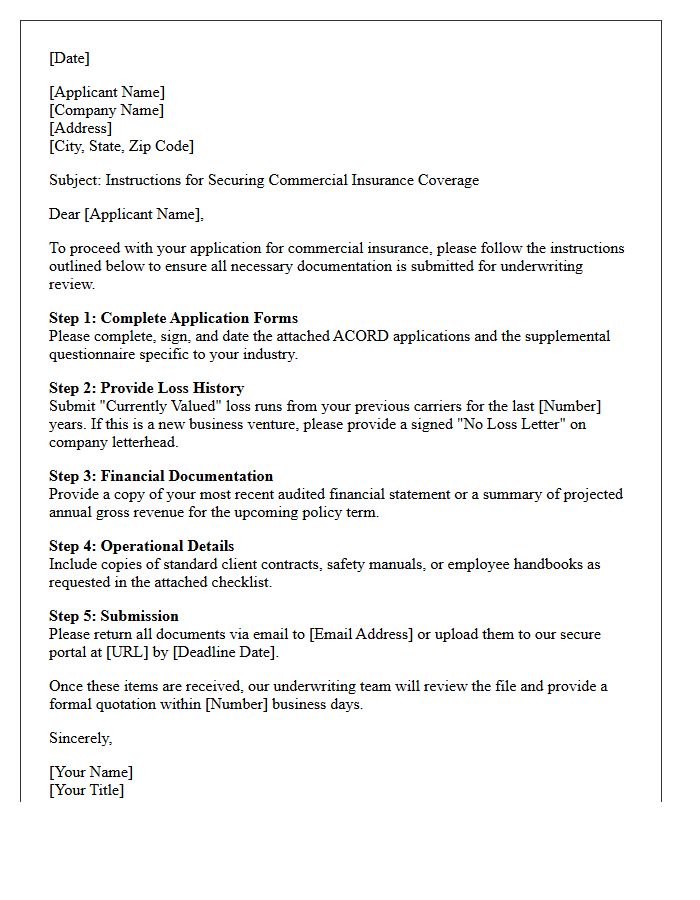

Instructions for Securing Commercial Coverage

To obtain commercial insurance, businesses must first perform a comprehensive risk assessment to identify specific liabilities. Organizations should prepare detailed financial records, loss history reports, and safety protocols to present to underwriters. It is essential to compare quotes from multiple providers to ensure competitive pricing and adequate protection. For optimal results, consulting a licensed broker helps navigate complex policy terms and endorsements. Providing accurate data during the application process prevents coverage gaps and ensures that the final policy effectively mitigates potential financial losses and legal claims against the enterprise.

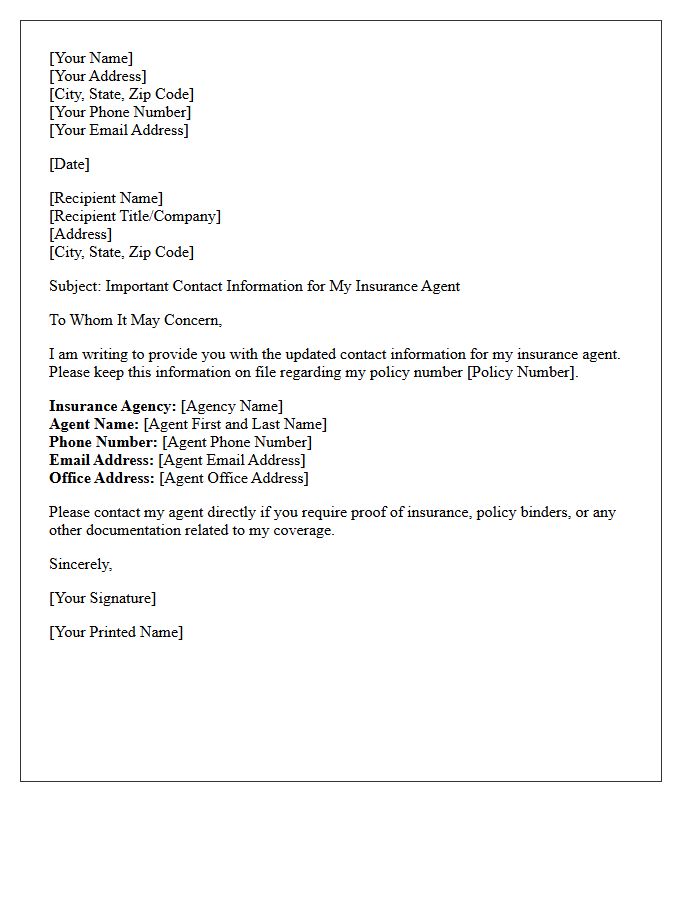

Insurance Agent Contact Information

Keeping your insurance agent contact information readily accessible is vital for emergency situations. Always store your agent's direct phone number and email address in your smartphone and a physical backup. This ensures you can report claims immediately, receive professional guidance during accidents, and clarify policy coverage details. Updated contact data simplifies the renewal process and allows for quick adjustments to your premiums. Proactive communication with your representative helps safeguard your financial security by ensuring your insurance policies remain accurate and active when you need them most.

Official Letter Signature

An official letter signature serves as a formal validation of the document's content and the sender's authority. It must include your full name, professional title, and organization to ensure clear accountability. For physical letters, leave space for a handwritten ink signature between the complimentary close and your typed details. In digital correspondence, a professional signature block with contact information is essential. Maintaining a consistent format demonstrates credibility and ensures your communication adheres to established business protocols and legal standards.

What is a Notice of Non-Renewal for prohibited commercial use?

A Notice of Non-Renewal for prohibited commercial use is a formal notification from an insurance provider stating they will not extend your personal auto policy because the vehicle was used for business purposes, such as ridesharing or delivery, which violates the terms of a personal insurance contract.

Why was my personal auto insurance canceled for commercial activity?

Most personal auto policies specifically exclude coverage for "livery" or commercial transport. If an insurer discovers you are using your private vehicle for profit-making activities without a commercial endorsement or business policy, they may choose to non-renew the policy due to the increased risk and breach of contract.

Can I dispute a non-renewal notice regarding commercial vehicle use?

Yes, you can dispute the notice if you can provide evidence that the vehicle was not being used for commercial purposes. You should contact your agent or the insurance company's underwriting department to provide documentation, such as mileage logs or proof that you do not work for a delivery service.

What should I do if my insurance is non-renewed for business use?

If your policy is non-renewed, you must secure new insurance immediately to avoid a lapse in coverage. You should look for a provider that offers a "Rideshare Endorsement" for personal policies or transition to a dedicated commercial auto insurance policy that legally covers your business activities.

Will a non-renewal for commercial use affect my future insurance rates?

A notice of non-renewal becomes part of your insurance history and may be visible to future insurers through reports like LexisNexis or CLUE. This can lead to higher premiums or being classified as a high-risk driver, making it essential to find a policy that accurately reflects your vehicle usage.

Comments