Receiving a Notice of Non-Renewal Due to Severe Loss History indicates that an insurer has declined to extend coverage because of frequent or high-cost claims. This formal notification highlights the increased risk profile of the policyholder, necessitating a search for alternative insurance providers. Understanding the reasons behind this decision is crucial for future eligibility. Below are some ready to use templates.

Image cover: Notice of Non-Renewal: Policy Termination Due to Excessive Claims History

Letter Samples List

- Notice of Non-Renewal Letter Due to Severe Loss History

- Severe Loss History Non-Renewal Notification Letter

- Commercial Auto Policy Non-Renewal Letter for Excessive Claims

- Property Insurance Non-Renewal Letter Due to High Claim Frequency

- Official Letter of Policy Non-Renewal Due to Adverse Loss Experience

- General Liability Non-Renewal Letter for Severe Loss History

- Homeowners Insurance Non-Renewal Letter Following Multiple Severe Losses

- Formal Agency Non-Renewal Letter Due to Excessive Loss History

- Workers Compensation Non-Renewal Letter for Poor Loss Record

- Commercial Property Non-Renewal Letter Due to Severe Loss History

- Personal Auto Insurance Non-Renewal Letter for High Claim Volume

- Standard Notice of Non-Renewal Letter for Unacceptable Loss History

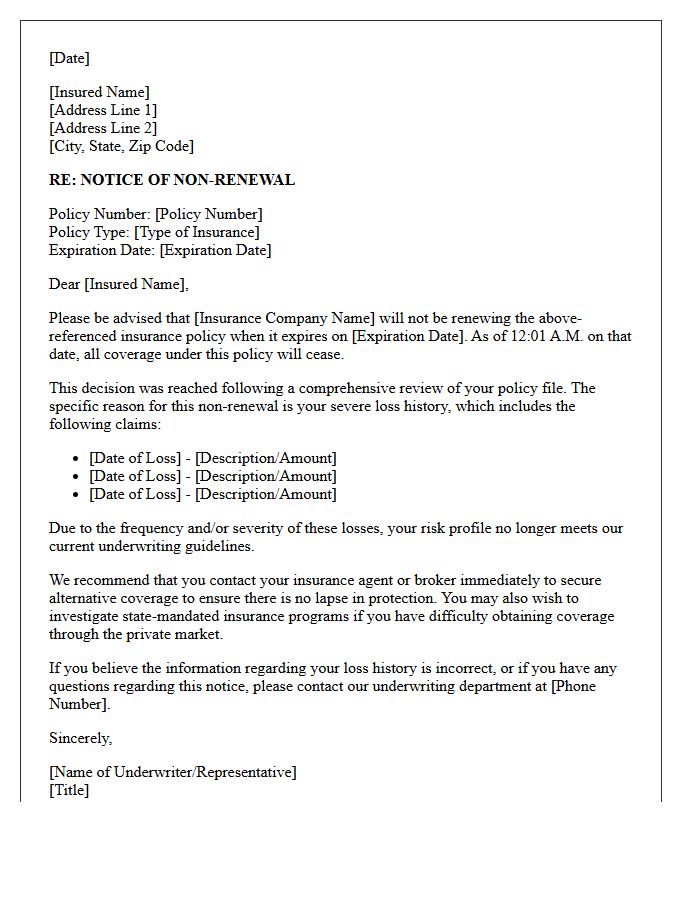

Notice of Non-Renewal Letter Due to Severe Loss History

A Notice of Non-Renewal due to severe loss history is a formal statement from an insurance provider terminating coverage at the end of the policy term. This typically occurs when a policyholder files frequent or high-value claims, making them a high-risk client. To maintain protection, you must immediately seek alternative coverage to avoid a lapse. It is essential to review your claims history and implement risk mitigation strategies, as a history of losses can lead to significantly higher premiums or difficulty securing a new policy with standard carriers.

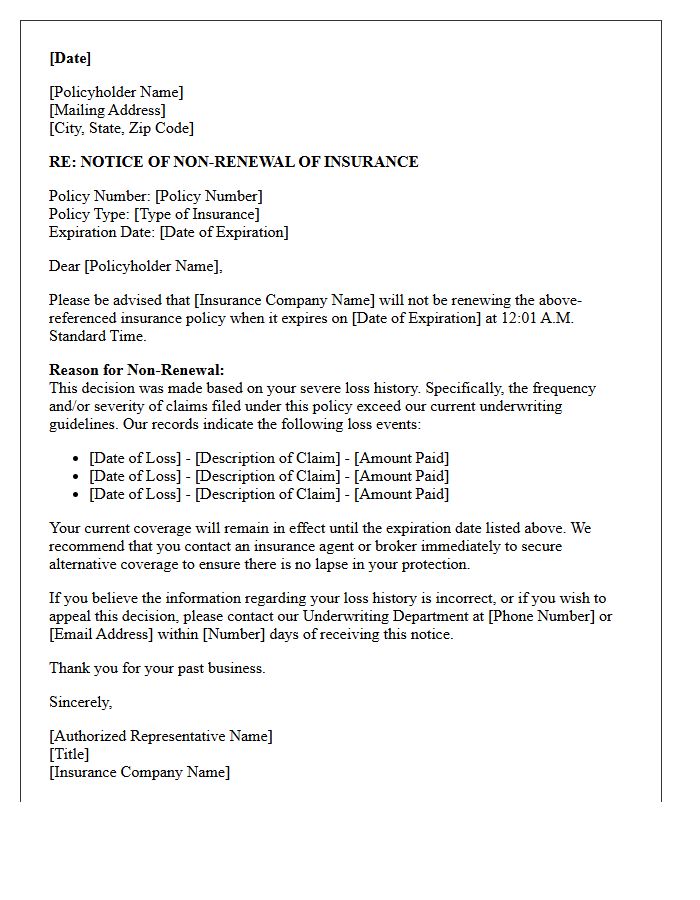

Severe Loss History Non-Renewal Notification Letter

A Severe Loss History Non-Renewal Notification Letter is a formal legal notice issued by an insurance carrier. It informs policyholders that their coverage will not be extended beyond the current term due to an excessive frequency or severity of past claims. This document is legally required to provide specific reasoning and clear effective dates. Receiving this notice signifies that the insurer deems the risk profile too high for renewal, necessitating that the insured seek alternative coverage immediately to avoid a protection gap.

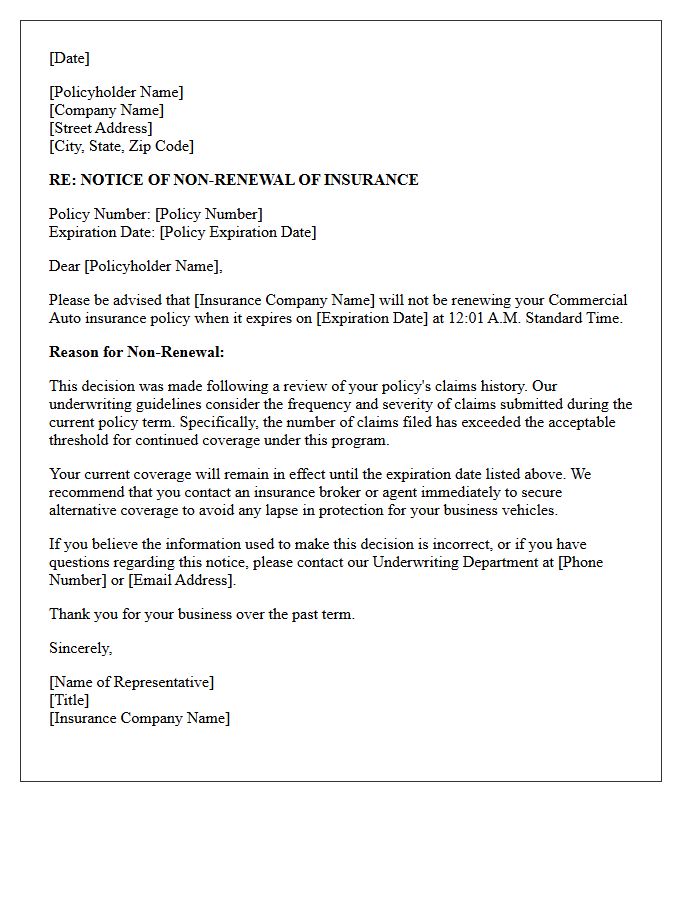

Commercial Auto Policy Non-Renewal Letter for Excessive Claims

A commercial auto policy non-renewal letter for excessive claims informs a business that their insurer will not extend coverage past the current expiration date. Receiving this notice is critical because it indicates the risk profile has exceeded underwriting guidelines due to high loss frequency or severity. Companies should immediately audit safety protocols and seek alternative coverage to avoid a lapse. To improve future eligibility, focus on risk mitigation, driver training, and maintaining a clean loss run report to demonstrate a commitment to safety and lower overall liability.

Property Insurance Non-Renewal Letter Due to High Claim Frequency

Receiving a non-renewal letter indicates your insurer will not extend coverage after the current policy expiration. When triggered by high claim frequency, the provider views multiple small or large losses as an increased financial risk. To protect your property, immediately review the specific effective date and reasons provided. It is crucial to shop for new coverage early, as a history of frequent claims can make finding standard insurance difficult. Consider consulting a specialist broker or exploring surplus lines options to ensure your assets remain continuously protected against future liabilities.

Official Letter of Policy Non-Renewal Due to Adverse Loss Experience

An official letter of policy non-renewal due to adverse loss experience signifies that an insurer will not extend coverage beyond the current term. This decision typically results from a high frequency or severity of claims, making the policyholder a high-risk client. It is crucial to review the specific reasons provided and begin seeking alternative coverage immediately to avoid a protection gap. Maintaining a clean claims history is essential for long-term eligibility and competitive premiums in the insurance market.

General Liability Non-Renewal Letter for Severe Loss History

A General Liability non-renewal letter for severe loss history informs a policyholder that their coverage will not be extended due to excessive or high-cost claims. This formal notice indicates the insurer deems the risk profile too high for their current underwriting guidelines. Receiving this letter requires immediate action to find alternative coverage before the expiration date to avoid a gap. To secure new insurance, businesses should implement a safety improvement plan and prepare a detailed explanation of past incidents to demonstrate proactive risk management to prospective carriers.

Homeowners Insurance Non-Renewal Letter Following Multiple Severe Losses

Receiving a homeowners insurance non-renewal letter after multiple severe losses means your carrier has deemed your property a high-risk profile. To maintain coverage, you must immediately review the underwriting reasons cited in the notice. Insurance companies often terminate policies when frequent claims suggest future instability. It is crucial to document all completed repairs and seek alternative coverage through excess lines or state-backed FAIR plans before your current term expires. Addressing property mitigation quickly can help improve your eligibility with new insurers during this transition period.

Formal Agency Non-Renewal Letter Due to Excessive Loss History

A formal agency non-renewal letter serves as legal notification that an insurance carrier is terminating its relationship with a producer. The primary reason is often an excessive loss history, indicating that the agency's portfolio carries unsustainable risk levels. Carriers evaluate the loss ratio to determine if claims payouts exceed premium income. Receiving this notice requires immediate action to secure new appointments and protect client coverage. Understanding these underwriting guidelines is essential for maintaining a profitable partnership and avoiding sudden contract termination due to poor performance metrics.

Workers Compensation Non-Renewal Letter for Poor Loss Record

A Workers Compensation Non-Renewal Letter is a formal notice sent by an insurer stating they will not extend coverage after the policy expires. This action is typically triggered by a poor loss record, indicating that the frequency or severity of past workplace injury claims exceeds acceptable risk thresholds. Upon receiving this notice, businesses must act quickly to improve safety protocols and secure alternative coverage to avoid legal penalties for being uninsured. High claim volumes suggest systemic safety issues that must be addressed to find competitive rates in the future market.

Commercial Property Non-Renewal Letter Due to Severe Loss History

A commercial property non-renewal letter signifies that an insurer will not extend coverage past the current expiration date. The primary reason for this action is a severe loss history, indicating a high frequency or severity of past claims. This data suggests an unacceptable level of risk for the provider. Policyholders must act quickly to secure alternative insurance, as a non-renewal notice can make obtaining new coverage more difficult and expensive. Reviewing the loss runs and implementing risk mitigation strategies is essential to restore insurability in a hardening market.

Personal Auto Insurance Non-Renewal Letter for High Claim Volume

Receiving a non-renewal letter indicates your insurance provider will not extend your policy beyond its current expiration date. For drivers with a high claim volume, carriers often view the frequent loss history as an unacceptable financial risk. Unlike a cancellation, non-renewal occurs at the end of a term, providing a window to find alternative coverage. It is essential to act quickly, as a history of multiple claims can lead to higher premiums or the need for a specialized high-risk insurer to maintain continuous legal protection for your vehicle.

Standard Notice of Non-Renewal Letter for Unacceptable Loss History

A Standard Notice of Non-Renewal for unacceptable loss history is a formal legal notification issued by an insurance provider. It informs the policyholder that their coverage will not be extended past the current expiration date due to a high frequency or severity of claims. State laws typically require this notice to be sent within a specific timeframe, such as 30 to 60 days before termination. Recieving this document signifies that the insurer views the risk as too high, often necessitating the search for alternative coverage through high-risk pools or different carriers.

What is a Notice of Non-Renewal due to severe loss history?

A Notice of Non-Renewal is a formal communication from an insurance carrier stating they will not extend your policy coverage beyond its current expiration date because the frequency or severity of your past claims exceeds their risk underwriting guidelines.

Can I appeal a non-renewal decision based on my loss history?

Yes, you can request a formal review by providing documentation of repairs, proof of implemented safety measures, or evidence that the losses were caused by non-recurring catastrophic events rather than poor maintenance or negligence.

How many claims lead to an insurance non-renewal for loss history?

While thresholds vary by carrier and state, most insurers flag policies for non-renewal if there are three or more at-fault claims within a three-year period, or if a single large loss suggests a high probability of future liability.

Will a non-renewal for loss history make it harder to find new insurance?

Yes, a history of frequent claims can lead to higher premiums or require you to seek coverage through "surplus lines" or high-risk insurance pools, as standard carriers may view the loss history as an indicator of future risk.

How long does a severe loss history affect my insurance eligibility?

Most insurance companies evaluate your "CLUE" report or loss history over a rolling three to five-year window; as older claims fall off your record, you will likely qualify for more competitive rates and standard policy forms again.

Comments