Gaining a clear understanding of your insurance policy coverage and financial limits is essential for effective risk management. This guide explores how to interpret policy language, identify exclusions, and ensure your assets are adequately protected against unforeseen events. Learn to navigate complex terms to maximize your benefits. To help you get started, below are some ready to use template.

Image cover: Mastering Your Policy: Coverage and Limits Templates for Clear Protection

Letter Samples List

- Policy Welcome Letter Regarding Your Coverage and Limits

- Annual Review Letter on Insurance Policy Coverage Limits

- Auto Insurance Liability Coverage and Limits Explanation Letter

- Homeowners Policy Personal Property Coverage Limits Letter

- Policy Renewal Letter Detailing Coverage and Limits Adjustments

- Claim Decision Letter Based on Policy Coverage Limits

- Umbrella Policy Letter for Extended Coverage and Limits

- Clarification Letter on Specific Policy Exclusions and Limits

- Commercial Business Insurance Coverage Limits Breakdown Letter

- Health Insurance Out of Pocket Limits and Coverage Letter

- Notice of Exhausted Policy Coverage Limits Letter

- Mid-Term Policy Endorsement Letter on Coverage Limits Change

- Life Insurance Benefit Limits and Coverage Explanation Letter

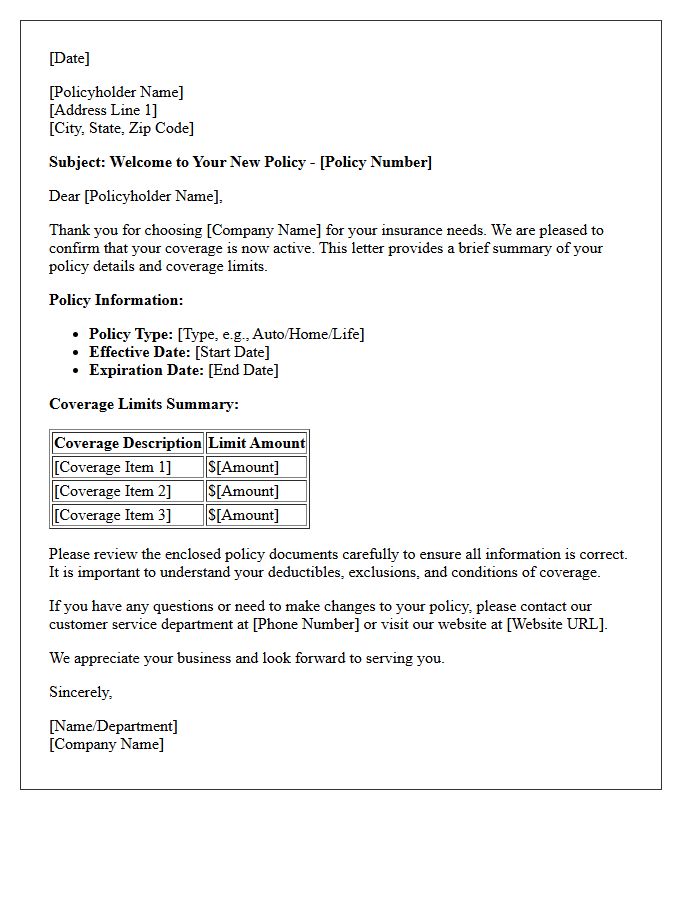

Policy Welcome Letter Regarding Your Coverage and Limits

Your Policy Welcome Letter serves as the official confirmation of your insurance protection. It is essential to verify your coverage limits to ensure the financial protection aligns with your specific needs. This document outlines your policy number, effective dates, and premium details. Carefully review the declarations page to understand what is included or excluded from your plan. Recognizing these boundaries helps prevent unexpected out-of-pocket costs during a claim. Always store this letter securely as it summarizes your legal agreement and provides contact information for immediate assistance or policy adjustments.

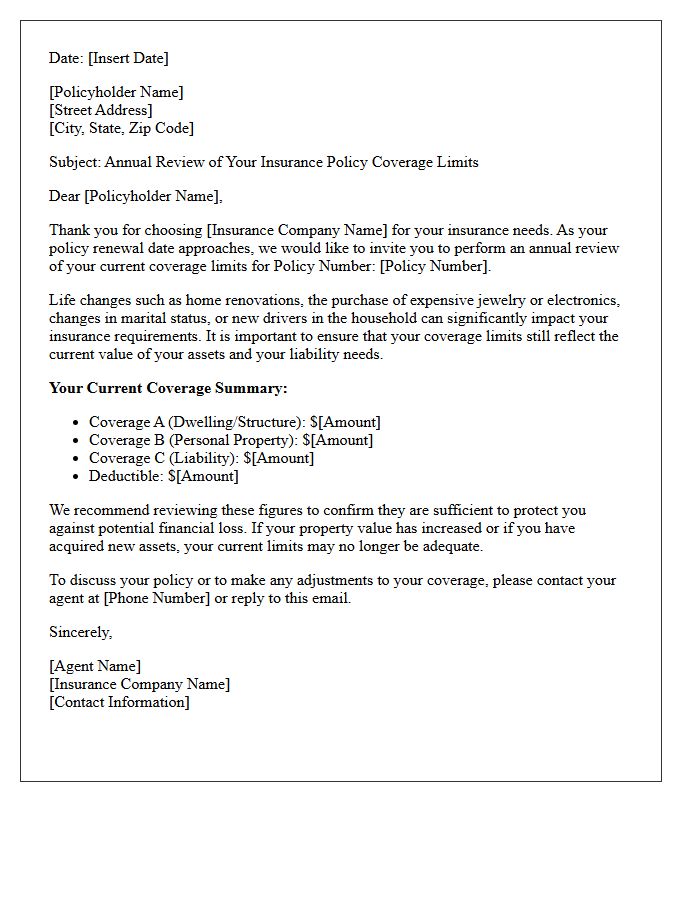

Annual Review Letter on Insurance Policy Coverage Limits

An annual review letter is a critical document for assessing your insurance policy coverage limits to ensure they align with current asset values. Over time, inflation or property improvements can lead to underinsurance, leaving you financially vulnerable during a claim. Reviewing these updates allows you to adjust protection levels, identify potential gaps, and confirm that your liability protection remains adequate. Regularly evaluating your policy ensures that your financial security evolves alongside your lifestyle changes, providing peace of mind and robust recovery options after an unexpected loss.

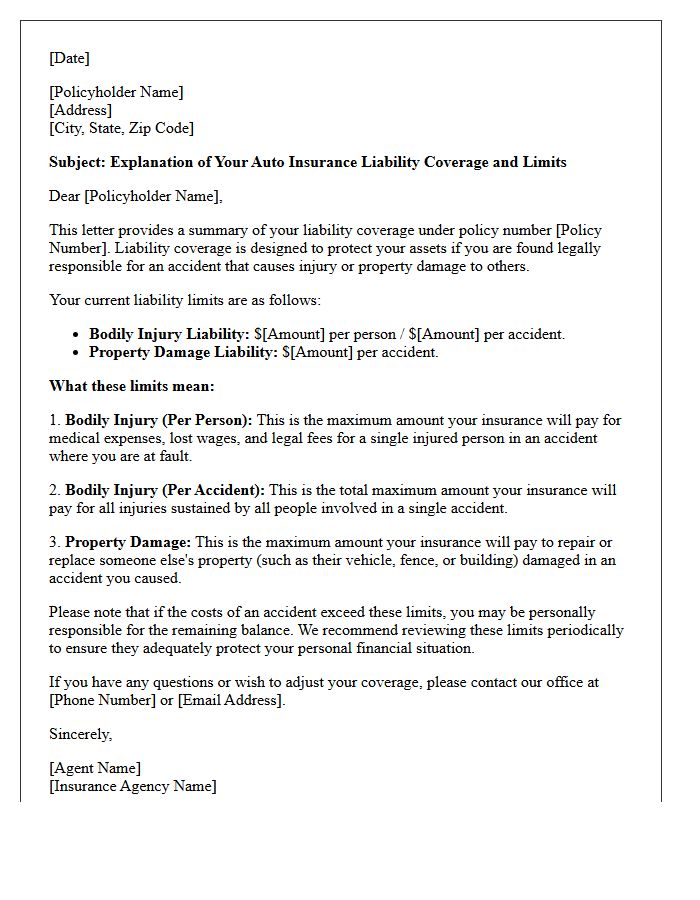

Auto Insurance Liability Coverage and Limits Explanation Letter

A liability coverage explanation letter details your financial protection against claims for bodily injury or property damage caused to others. It clarifies specific policy limits, which represent the maximum amount your insurer will pay per accident. Understanding these caps is essential, as any costs exceeding them become your personal legal responsibility. This document ensures you are aware of your minimum legal requirements and helps determine if your current coverage levels sufficiently safeguard your personal assets from potential lawsuits following an at-fault vehicle accident.

Homeowners Policy Personal Property Coverage Limits Letter

A Homeowners Policy Personal Property Coverage Limits Letter is a crucial document that outlines the specific financial caps on your belongings. It is essential to understand that standard policies often have sub-limits for high-value items like jewelry, electronics, or art. Reviewing this letter ensures your protection aligns with the actual value of your assets. If your possessions exceed these established boundaries, you may need to schedule endorsements or floaters to guarantee full replacement cost coverage in the event of a total loss, theft, or damage.

Policy Renewal Letter Detailing Coverage and Limits Adjustments

A policy renewal letter is a critical legal document outlining coverage modifications and premium changes for the upcoming term. It is essential to review the Limits of Liability section to ensure your protection aligns with current asset values. Pay close attention to the Summary of Changes, which highlights adjustments to deductibles, exclusions, or endorsements. Failing to evaluate these updates may result in underinsurance or unexpected out-of-pocket costs. Always verify that the adjusted policy limits still meet your specific risk management needs before the renewal date.

Claim Decision Letter Based on Policy Coverage Limits

A Claim Decision Letter outlines the final determination of your insurance request. When a payout is capped, it is typically due to specific policy coverage limits defined in your contract. These limits represent the maximum amount an insurer will pay for a covered loss. Reviewing this document is essential to understand how indemnification was calculated and whether any exclusions applied. If the settlement does not fully cover your expenses, the letter explains the legal and contractual basis for the payment ceiling based on your chosen plan structure.

Umbrella Policy Letter for Extended Coverage and Limits

An umbrella policy letter serves as a formal notification of extended liability insurance beyond standard policy thresholds. It provides a vital safety net for catastrophic claims that exceed primary limits on home or auto coverage. This document outlines your expanded financial protection, ensuring personal assets remain secure against legal judgements or major lawsuits. By establishing excess liability limits, the policy letter confirms your defense against significant financial loss, offering peace of mind through broader risk management and higher coverage caps for diverse liability scenarios.

Clarification Letter on Specific Policy Exclusions and Limits

A Clarification Letter provides essential transparency regarding Specific Policy Exclusions and coverage limits within an insurance contract. This document explicitly defines what the insurer will not cover, preventing future disputes or claim denials. It serves to eliminate ambiguity by outlining precise financial caps and situational restrictions that apply to your policy. Understanding these limitations ensures policyholders maintain realistic expectations of their benefits. Reviewing this letter is critical for identifying potential protection gaps and ensuring comprehensive risk management before a loss occurs.

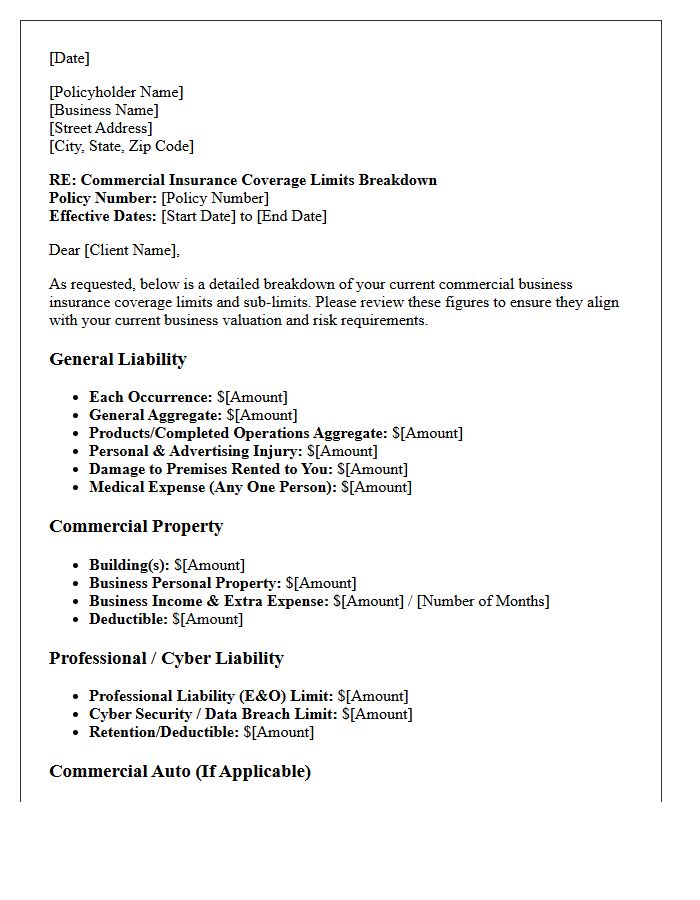

Commercial Business Insurance Coverage Limits Breakdown Letter

A Commercial Business Insurance Coverage Limits Breakdown Letter serves as a formal summary of liability thresholds and asset protection levels. This document explicitly outlines the maximum payout amounts for specific risks, including general liability, property damage, and professional indemnity. It is essential for verifying that your business meets contractual requirements when partnering with vendors or clients. Understanding these sub-limits ensures you identify potential coverage gaps before a loss occurs. Always review this breakdown to confirm your policy aggregates align with your current operational risks and financial obligations.

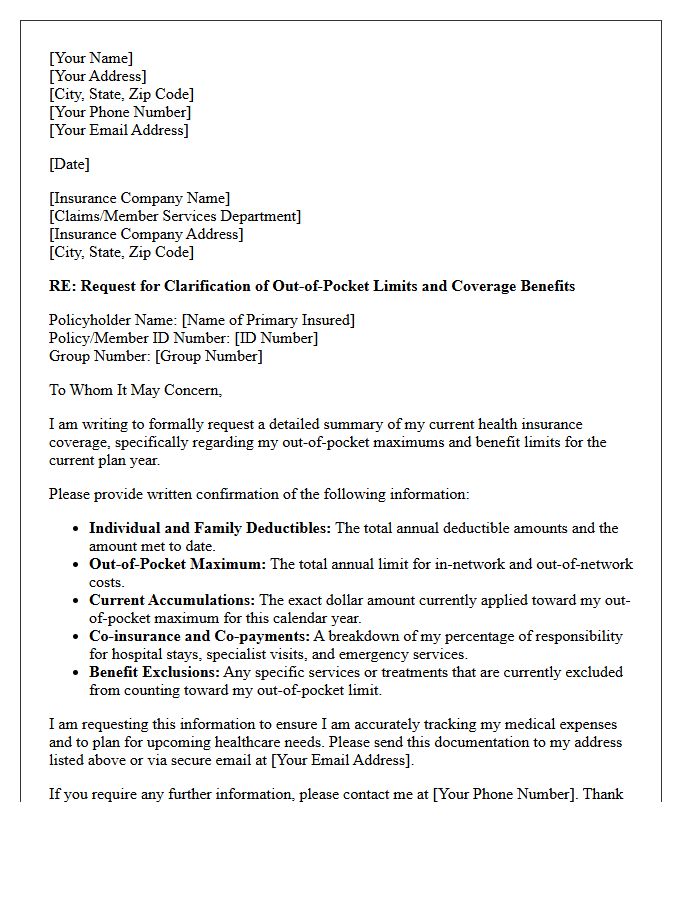

Health Insurance Out of Pocket Limits and Coverage Letter

A health insurance out-of-pocket maximum is the most you must pay for covered services per year. Once reached, the insurer pays 100% of allowed costs. A Coverage Letter, or Summary of Benefits, details these financial caps and included services. It is essential to review this document to understand your deductibles and copayments. Knowing your limit prevents unexpected financial burdens during medical emergencies. Always verify that your providers are in-network to ensure expenses count toward your limit and maintain full protection under your policy.

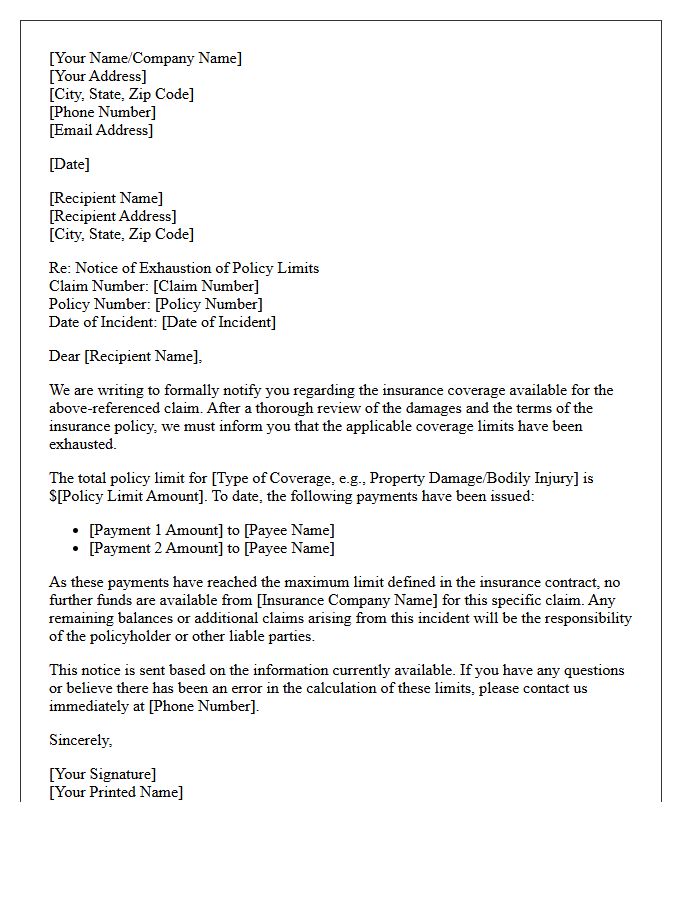

Notice of Exhausted Policy Coverage Limits Letter

A Notice of Exhausted Policy Coverage Limits Letter is a critical formal document from an insurance company stating that the maximum payout amount under your policy has been reached. This signifies that the insurer will no longer cover additional costs or legal defenses for a claim. It is essential to review this notice immediately, as you may become personally liable for any remaining expenses or judgments. Always consult a legal professional to explore excess insurance or personal asset protection options when coverage is fully depleted.

Mid-Term Policy Endorsement Letter on Coverage Limits Change

A Mid-Term Policy Endorsement Letter is a formal amendment to an active insurance contract. It officially documents a Coverage Limits Change, adjusting the maximum amount an insurer will pay for claims. This update ensures your protection aligns with current asset values or risk exposure. It is crucial to review the updated declarations page to confirm the effective date and premium adjustments. Keeping this document alongside your original policy ensures continuous, accurate legal proof of your financial protection and prevents potential gaps in coverage during the remaining policy term.

Life Insurance Benefit Limits and Coverage Explanation Letter

A Life Insurance Benefit Limits and Coverage Explanation Letter provides critical transparency regarding your policy's financial protection. It details the specific death benefit amount, identified beneficiaries, and any exclusions that might void a claim. Understanding these coverage limits is essential to ensure your family's long-term security. Always review the waiting period and premium schedules mentioned to maintain active status. This document serves as legal clarification, helping policyholders verify that the indemnity levels align with their intended estate planning goals and debt obligations.

What is the difference between policy coverage and policy limits?

Policy coverage refers to the specific types of risks or events your insurance protects against, such as theft or fire, while policy limits represent the maximum dollar amount the insurance company will pay out for a covered claim.

How do I identify exclusions in my insurance policy?

Exclusions are typically listed in a dedicated section of your policy document labeled "Exclusions" or "What Is Not Covered." These are specific situations, items, or types of damage that the insurer will not provide financial protection for under any circumstances.

What is an aggregate limit versus a per-occurrence limit?

A per-occurrence limit is the maximum amount paid for a single claim or accident, whereas an aggregate limit is the total maximum amount the insurer will pay for all claims combined during the entire policy period, usually one year.

Does my policy coverage include actual cash value or replacement cost?

Replacement cost coverage pays to replace items with new ones of similar quality at today's prices, while actual cash value (ACV) only pays the depreciated value of the item at the time of loss. You can find which method applies to you in your policy declarations page.

How can I determine if my current limits are sufficient for my needs?

To evaluate if your limits are adequate, compare your total asset value and potential liability risks against the "Limit of Liability" shown on your declarations page. If your assets exceed your limits, you may need to increase your coverage or add an umbrella policy for extra protection.

Comments