Removing a driver from your car insurance can lower premiums if they no longer reside in your home or use the vehicle. This driver removal from auto policy letter serves as formal notification to your insurer to adjust your coverage legally. Follow our guide to ensure a smooth administrative process. Below are some ready to use templates.

Image cover: Request for Driver Removal: Letter Templates and Samples

Letter Samples List

- Standard Driver Removal From Auto Policy Letter

- Voluntary Driver Removal From Auto Policy Letter

- Out Of Household Driver Removal From Auto Policy Letter

- Deceased Driver Removal From Auto Policy Letter

- Divorced Spouse Driver Removal From Auto Policy Letter

- Relocated Teen Driver Removal From Auto Policy Letter

- Military Deployment Driver Removal From Auto Policy Letter

- Excluded High-Risk Driver Removal From Auto Policy Letter

- Commercial Fleet Driver Removal From Auto Policy Letter

- License Suspension Driver Removal From Auto Policy Letter

- Underwriting Initiated Driver Removal From Auto Policy Letter

- Surrendered License Driver Removal From Auto Policy Letter

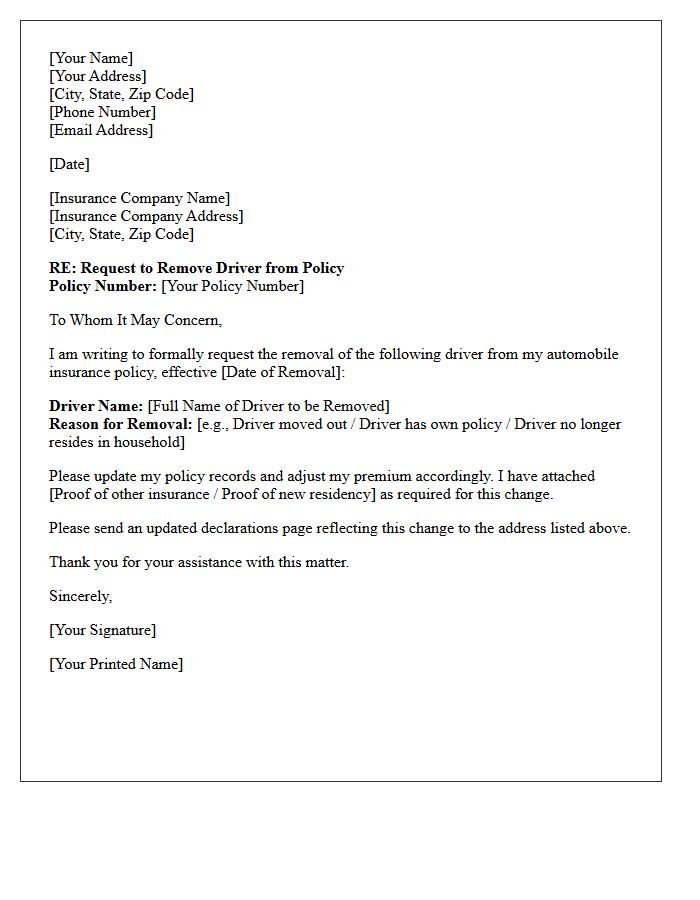

Standard Driver Removal From Auto Policy Letter

A standard driver exclusion endorsement is a formal legal document used to remove a specific person from your auto insurance coverage. By signing this letter, you acknowledge that the excluded driver is no longer permitted to operate your vehicle. This action is typically taken to lower premiums if a household member has a poor driving record. However, it is vital to understand that if the excluded individual drives and causes an accident, the insurer will deny all claims, leaving you personally liable for all damages and legal costs.

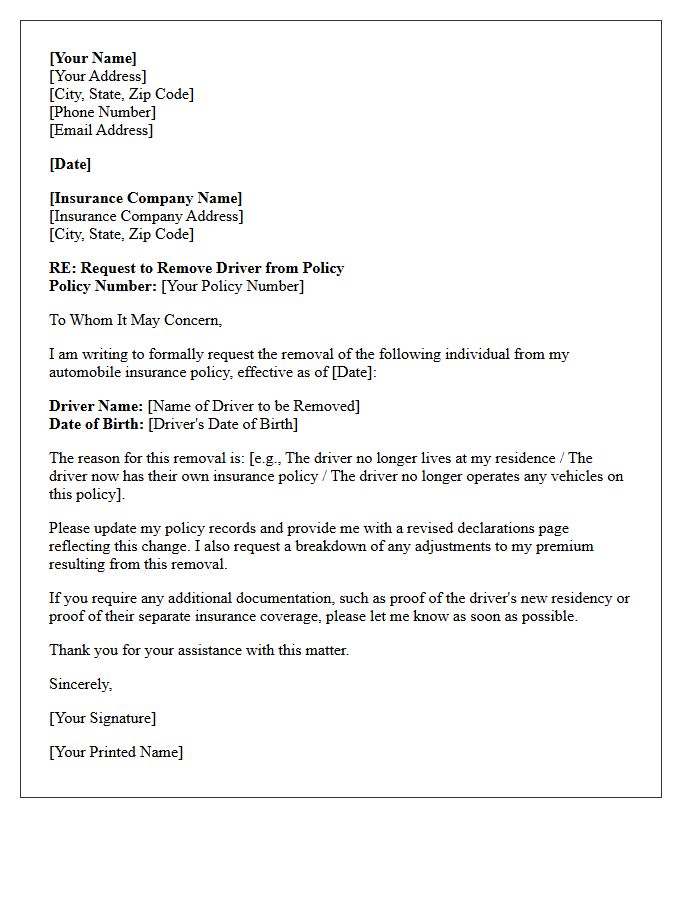

Voluntary Driver Removal From Auto Policy Letter

A voluntary driver removal letter is a formal document used to exclude a specific household member from your car insurance coverage. This process, often called a Named Driver Exclusion, ensures the insurance company will not provide protection or pay claims for that individual. It is commonly used to lower premiums if a resident has a poor driving record or does not use the vehicle. Once excluded, that person must never operate the insured car, as any resulting accidents will lead to a complete denial of coverage and personal financial liability.

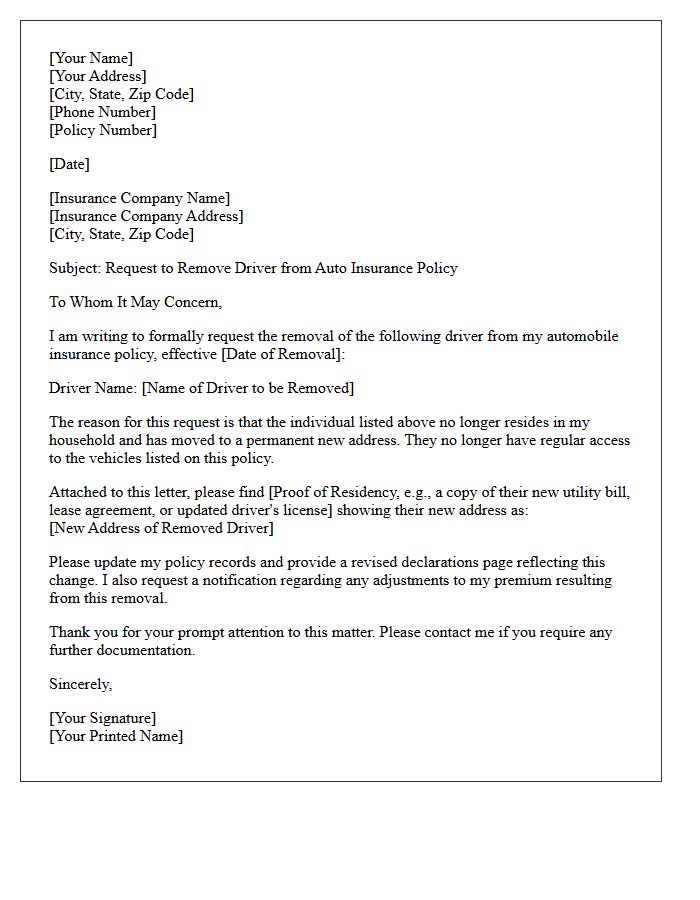

Out Of Household Driver Removal From Auto Policy Letter

An Out of Household Driver Removal letter is a formal request to exclude an individual from your auto insurance coverage because they no longer reside at your address. To process this, insurers typically require proof of new residency, such as a utility bill or a new lease agreement. Removing a non-resident driver is essential to ensure accurate premium ratings and prevent unnecessary costs. Clearly state the driver's name, the effective date of their move, and their new location to maintain policy integrity and avoid potential claims complications.

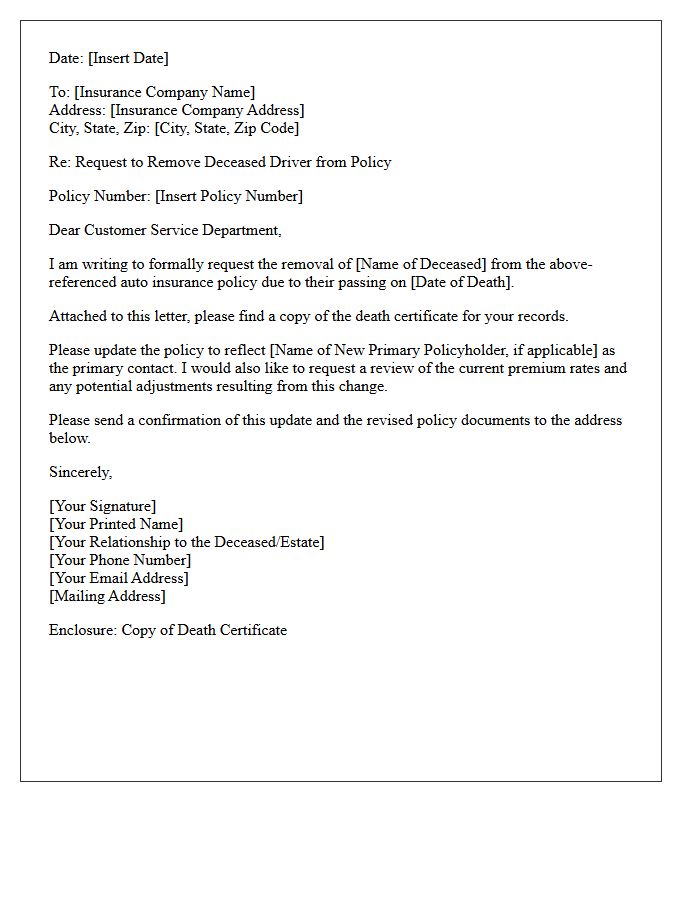

Deceased Driver Removal From Auto Policy Letter

When a policyholder passes away, notifying the insurance company via a Deceased Driver Removal Letter is essential to update legal records and adjust premiums. This formal notice ensures the surviving spouse or estate executor maintains continuous coverage while preventing potential fraud. You must include the policy number, date of passing, and a certified copy of the death certificate. Promptly submitting this documentation allows for the legal transfer of policy ownership or the formal cancellation of the decedent's name to reflect the current household risk accurately.

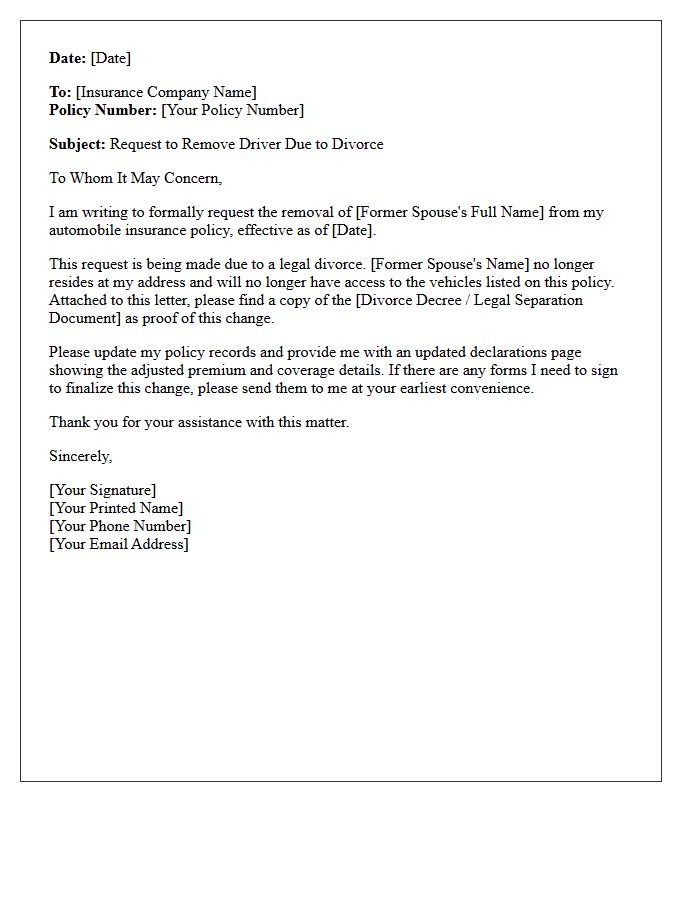

Divorced Spouse Driver Removal From Auto Policy Letter

A Divorced Spouse Driver Removal From Auto Policy Letter is a formal request to your insurance provider to terminate coverage for an ex-partner. It is essential to submit this written notice promptly to ensure accurate billing and clear legal liability. You may be required to provide a divorce decree or proof of separate residency to process the change. Removing a driver can significantly impact your insurance premiums and prevents you from being held responsible for their future accidents or traffic violations under a shared policy.

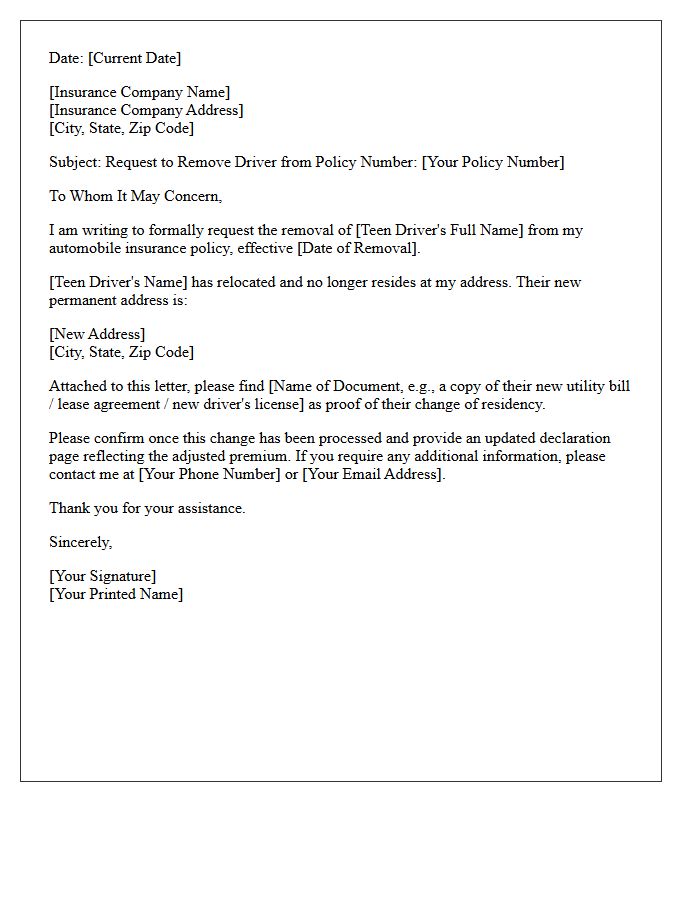

Relocated Teen Driver Removal From Auto Policy Letter

When a teenager moves away permanently, a Relocated Teen Driver Removal From Auto Policy Letter is essential to reduce insurance premiums. To process this request, providers typically require proof of the teen's new residency, such as a utility bill or updated license. Clearly state the effective date and confirm the driver no longer has access to the insured vehicles. Formally notifying your agent ensures your policy coverage remains accurate and prevents unnecessary charges for a high-risk driver who is no longer part of your household.

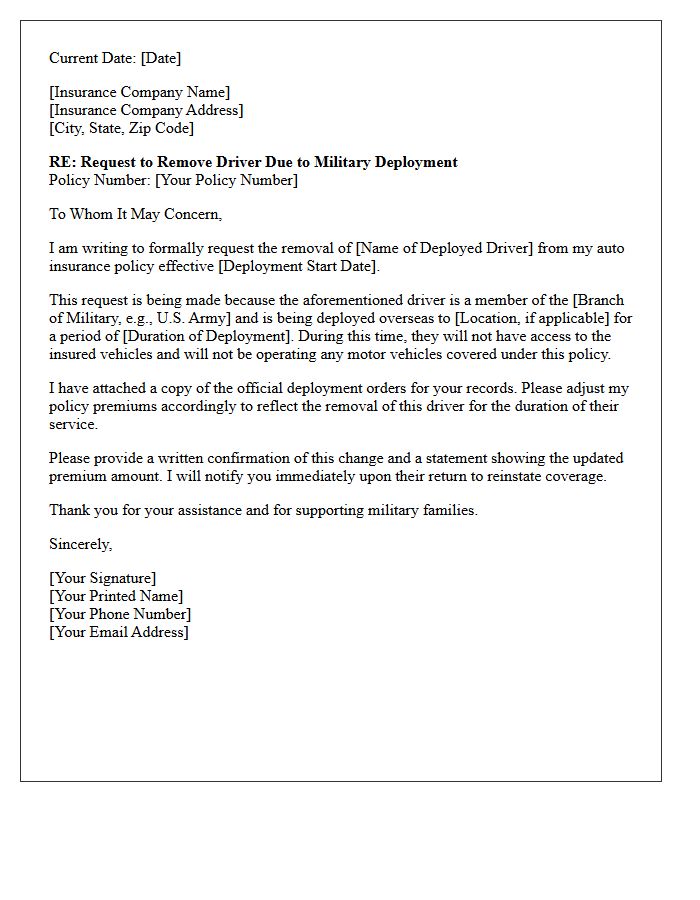

Military Deployment Driver Removal From Auto Policy Letter

A military deployment letter serves as official proof to request a driver removal from your auto insurance policy. By submitting these orders, service members can significantly reduce premiums while stationed away from home. Ensure the document includes the deployment start and end dates to justify the vehicle's non-operational status. Most providers allow you to maintain comprehensive coverage for protection against theft or damage while suspending liability costs. This administrative adjustment is a critical step for financial readiness during active duty assignments or overseas tours.

Excluded High-Risk Driver Removal From Auto Policy Letter

An Excluded High-Risk Driver Removal letter is a formal notification sent to an insurance company to officially reinstate a previously restricted individual. This document confirms that a high-risk driver is no longer part of the household or is no longer operating the vehicle. Providing verifiable proof, such as a new utility bill or an updated license, is essential to validate the change. Successfully processing this request ensures proper coverage for all operators while potentially lowering premium costs by removing high-risk variables from the policy rating.

Commercial Fleet Driver Removal From Auto Policy Letter

A commercial fleet driver removal letter is a formal notification sent to an insurance provider to exclude a specific individual from coverage. This typically occurs due to license suspension, high-risk violations, or employment termination. Promptly submitting this request ensures accurate premium calculations and protects the company from liability associated with unauthorized operators. The letter must include the driver's full name, license number, and the specific effective date of removal. Maintaining an updated driver roster is essential for risk management and maintaining fleet policy compliance.

License Suspension Driver Removal From Auto Policy Letter

When a driver faces a license suspension, insurance companies often issue a formal Driver Removal notice to exclude them from coverage. It is vital to understand that this letter legally confirms the individual is no longer insured to operate any vehicles under your auto policy. Failure to acknowledge this exclusion can lead to policy cancellation or denied claims. To restore their status later, you must provide proof of reinstatement from the DMV to your insurer. Always review these letters immediately to ensure your remaining household coverage stays active and compliant with state laws.

Underwriting Initiated Driver Removal From Auto Policy Letter

An Underwriting Initiated Driver Removal letter is a formal notice from your insurer stating that a specific person is being excluded from your auto policy. This typically occurs due to high-risk factors like serious traffic violations, multiple accidents, or a suspended license. To maintain your overall coverage and prevent policy cancellation, you must formally agree to remove the risky driver. Once excluded, that individual is no longer insured to operate your vehicles, and any claims resulting from their driving will be denied by the insurance company.

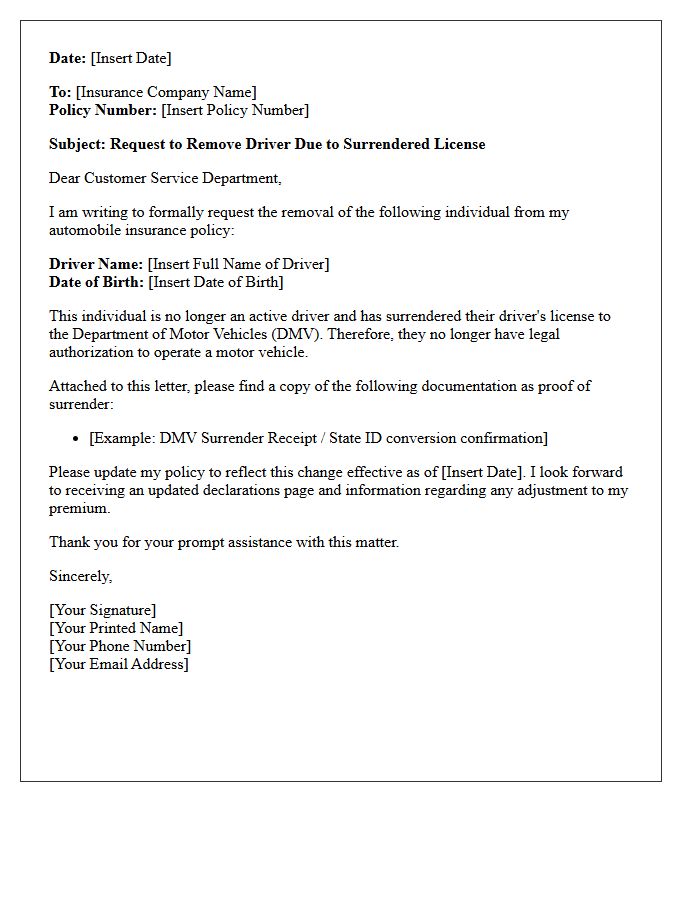

Surrendered License Driver Removal From Auto Policy Letter

A Surrendered License Driver Removal letter is a formal request to exclude an individual from your auto insurance. This process is essential when a household member voluntarily returns their driving credentials to the DMV. Providing proof of surrender allows insurers to adjust risk profiles, potentially lowering your premiums. You must include the driver's full name, policy number, and the official cancellation receipt from the licensing authority. Once processed, the insurance company will no longer provide coverage or charge for that specific individual, ensuring your policy reflects only active, authorized operators.

How do I write a formal letter to remove a driver from my auto insurance policy?

To remove a driver, draft a letter including your policy number, the full name of the driver to be removed, the effective date of the change, and the reason for removal (such as the driver moving out or obtaining their own insurance). Ensure the primary policyholder signs the document.

What supporting documents are required when requesting a driver removal?

Insurance companies often require proof that the individual no longer resides at your address or has coverage elsewhere. Common documents include a copy of their new insurance declarations page, a utility bill in their name at a new address, or a surrendered driver's license.

Can I remove a high-risk household member from my car insurance via letter?

Yes, you can request to remove a high-risk driver, but if they still live in your household, the insurer may require a "Named Driver Exclusion" endorsement instead. This legally stipulates that the individual is not covered to drive your vehicles under any circumstances.

Does a driver removal letter automatically lower my insurance premiums?

While removing a driver (especially one with a poor driving record or a young driver) often lowers premiums, it is not guaranteed. The final rate depends on the remaining drivers' risk profiles and whether the removed individual was contributing to a multi-driver discount.

What is the effective date for a driver removal request?

The effective date is typically the date the letter is received by the agent or a future date specified by the policyholder. Most insurers cannot backdate a driver removal further than 30 days without significant proof that the driver was insured elsewhere during that period.

Comments