Transitioning to a smaller home after the kids leave requires updating your policy to reflect a reduced dwelling size and fewer belongings. Our guide explains how to notify your provider about these lifestyle changes to potentially lower premiums. Ensure your coverage matches your new lifestyle with an Empty Nester Downsizing Insurance Adjustment Letter. To help you get started, below are some ready to use template.

Image cover: Downsizing After the Kids Leave: Guide to Updating Your Home Insurance (With Letter Templates)

Letter Samples List

- Empty Nester Home Downsizing Insurance Adjustment Letter

- Auto Coverage Reduction for Empty Nesters Insurance Letter

- Comprehensive Empty Nester Insurance Downsizing Review Letter

- Empty Nester Policy Modification and Adjustment Letter

- Life Insurance Coverage Adjustment Letter for Downsizing Empty Nesters

- Downsizing Empty Nester Personal Property Adjustment Letter

- Condominium Transition Insurance Adjustment Letter for Empty Nesters

- Multi-Vehicle Policy Downsizing Adjustment Letter

- Empty Nester Umbrella Policy Adjustment Letter

- Retirement and Downsizing Insurance Adjustment Letter

- Relocation and Downsizing Coverage Adjustment Letter

- Empty Nester Premium Reduction Insurance Adjustment Letter

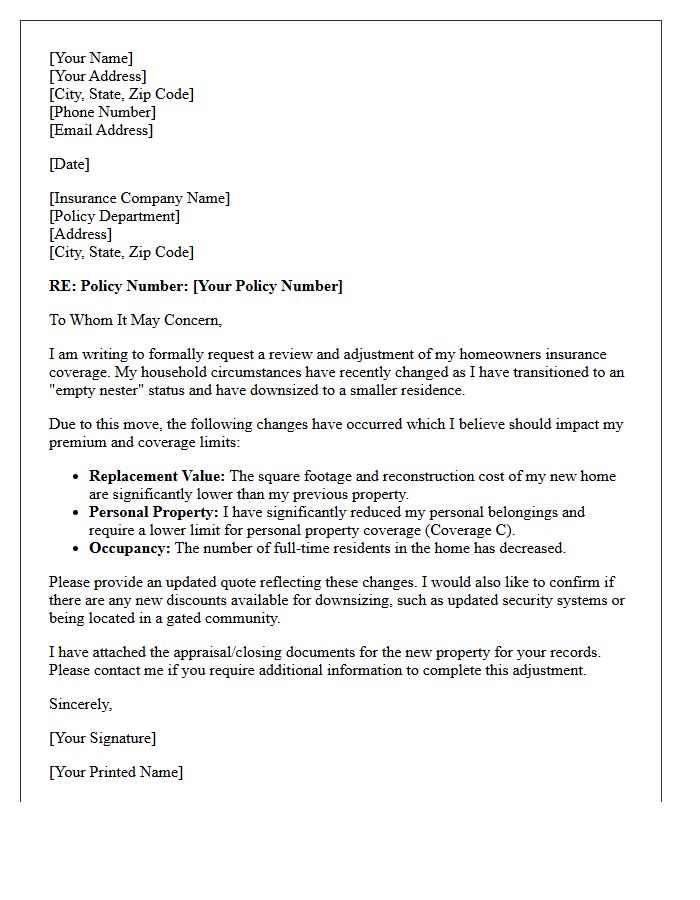

Empty Nester Home Downsizing Insurance Adjustment Letter

When sending an Empty Nester Home Downsizing Insurance Adjustment Letter, clearly notify your provider about your reduced liability risks and lower property value. Transitioning to a smaller residence or removing high-value items often warrants a premium reduction. Document your new square footage and updated inventory to ensure your coverage aligns with your current assets. Requesting a policy review helps prevent over-insuring your space while maintaining essential protection. Formalizing these lifestyle changes in writing ensures your insurance costs accurately reflect your simplified living situation and provides a paper trail for future claims.

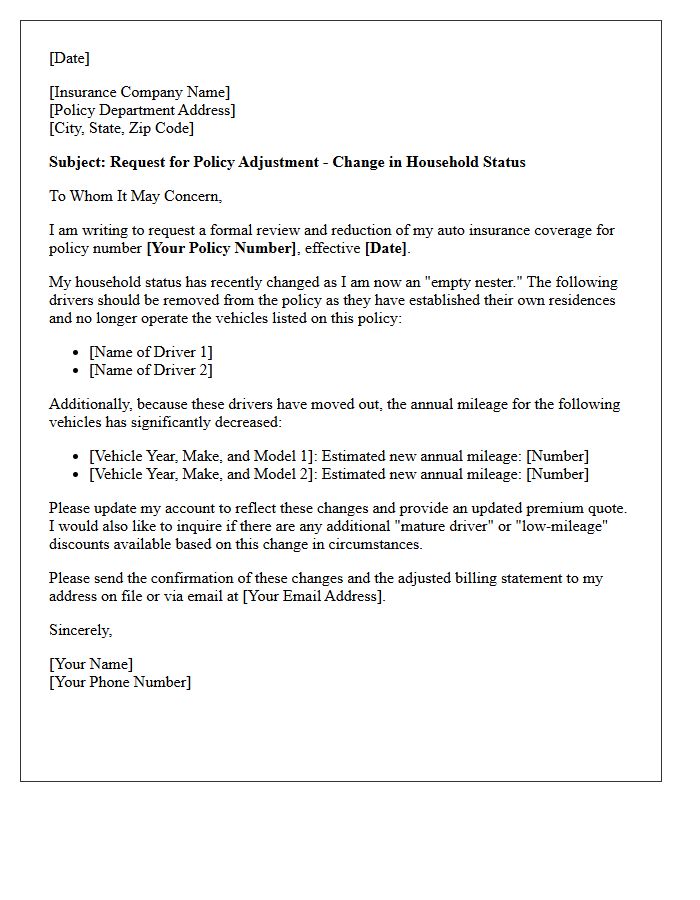

Auto Coverage Reduction for Empty Nesters Insurance Letter

An Auto Coverage Reduction letter informs policyholders that their insurance needs have changed. When children move out, parents can often remove them as listed drivers or adjust mileage estimates to lower monthly premiums. It is essential to review your liability limits and potential multi-car discounts to ensure your policy reflects your current lifestyle. Reducing unnecessary coverage helps empty nesters save money while maintaining adequate protection for their remaining vehicles. Always verify that household changes are accurately reported to your provider to avoid coverage gaps during this transition.

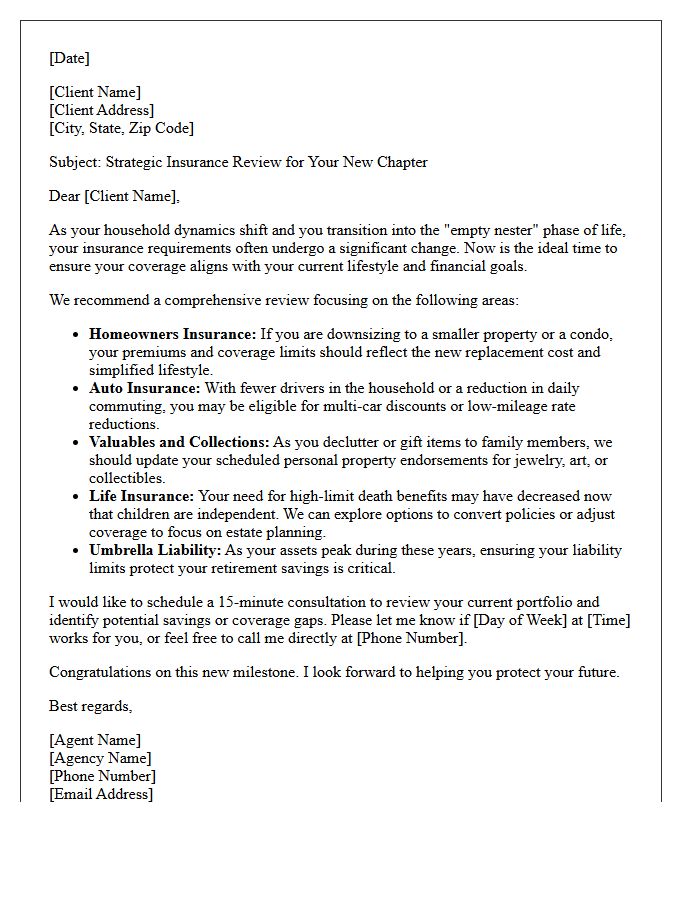

Comprehensive Empty Nester Insurance Downsizing Review Letter

A Comprehensive Empty Nester Insurance Downsizing Review Letter is a vital document for homeowners transitioning to smaller properties. It outlines necessary adjustments to liability coverage, personal property limits, and potential multi-policy discounts. This review ensures your protection aligns with a reduced lifestyle while addressing asset protection for high-value items kept after moving. By evaluating policy updates during this life stage, you can secure optimized premiums and eliminate redundant costs, providing peace of mind as you simplify your living arrangements and financial responsibilities.

Empty Nester Policy Modification and Adjustment Letter

An Empty Nester Policy Modification and Adjustment Letter is a formal request to update your homeowners or auto insurance coverage after children move out. This adjustment reflects a reduced household risk profile, often leading to lower premiums. Key updates include removing drivers from auto policies and reassessing property limits. Notifying your provider ensures your policy accurately matches your current lifestyle while maximizing potential savings. Promptly sending this letter prevents overpaying for unnecessary coverage and ensures your insurance legalities remain fully compliant with your updated living situation and occupancy status.

Life Insurance Coverage Adjustment Letter for Downsizing Empty Nesters

A Life Insurance Coverage Adjustment Letter helps empty nesters align their policy with reduced financial obligations. When children become independent and mortgages are paid off, you may no longer require high death benefits. Use this formal request to lower your premium costs by reducing the face value of your plan. This ensures your coverage remains cost-effective while still providing necessary protection for a surviving spouse. This strategic downsizing optimizes your retirement cash flow by eliminating unnecessary insurance expenses while maintaining essential peace of mind for your current lifestyle needs.

Downsizing Empty Nester Personal Property Adjustment Letter

A Downsizing Empty Nester Personal Property Adjustment Letter is a formal document notifying insurance providers about significant lifestyle changes. When children move out and you reduce possessions, your asset valuation decreases. Sending this letter helps adjust coverage limits to reflect your current inventory, potentially lowering monthly premiums. It serves as essential documentation for updated policy schedules, ensuring you aren't overpaying for coverage on items no longer in the home. Always include a revised inventory list to guarantee your homeowners insurance accurately aligns with your new, minimalist living situation.

Condominium Transition Insurance Adjustment Letter for Empty Nesters

Empty nesters moving to a condo must provide their insurer with a Condominium Transition Insurance Adjustment Letter. This document confirms the building's master policy coverage, allowing you to adjust your personal HO-6 policy accordingly. It prevents dual coverage and ensures you aren't overpaying for structural protection already managed by the association. By aligning these policies, you secure adequate protection for your personal property, liability, and unique loss assessment risks. Always submit this letter promptly to your agent to streamline your coverage transition and maximize monthly savings during your downsizing move.

Multi-Vehicle Policy Downsizing Adjustment Letter

A Multi-Vehicle Policy Downsizing Adjustment Letter notifies policyholders of premium changes following the removal of a vehicle from their coverage. This document outlines the revised billing schedule, updated liability limits, and the loss of multi-car discounts. It serves as legal confirmation that the specific vehicle is no longer insured under the master policy. Reviewing this adjustment is essential to ensure accurate coverage for remaining assets while confirming the refund amount or credit applied to future payments due to the reduced risk profile.

Empty Nester Umbrella Policy Adjustment Letter

An Empty Nester Umbrella Policy Adjustment Letter notifies your insurance provider that adult children have moved out, potentially reducing your liability risks. This formal request aims to lower premiums by updating household driver information and adjusting coverage limits to reflect your current lifestyle. Ensuring your policy accurately matches your reduced household size is essential for cost-effective protection. Clearly state your policy number and the specific changes to occupants to ensure your liability coverage remains optimized for your new financial situation.

Retirement and Downsizing Insurance Adjustment Letter

A retirement and downsizing insurance adjustment letter is a formal notification to your provider regarding a reduction in risk. When moving to a smaller home or disposing of assets, you must reassess coverage limits to avoid overpaying premiums. This document highlights changes in property value, inventory loss, and potential eligibility for senior discounts. Properly updating your policy ensures that your remaining assets are adequately protected while optimizing your financial liability. Always include a detailed inventory list and the specific effective date to guarantee a seamless transition into your new lifestyle phase.

Relocation and Downsizing Coverage Adjustment Letter

A Relocation and Downsizing Coverage Adjustment Letter is a formal notification sent to policyholders when changes in living arrangements impact insurance needs. This document highlights a reduction in liability or personal property limits following a move to a smaller residence. It ensures that premiums accurately reflect current asset values, preventing overpayment for unnecessary coverage. Reviewing this letter is essential to confirm that replacement cost evaluations remain sufficient for your new environment while maintaining comprehensive financial protection during significant life transitions.

Empty Nester Premium Reduction Insurance Adjustment Letter

An Empty Nester Premium Reduction letter informs your insurer that children have moved out, reducing your household risk profile. This insurance adjustment often leads to significant savings because fewer drivers are active on your policy. To qualify, you must formally notify your provider of the change in residency. This premium reduction reflects lower annual mileage and decreased liability. Proactively sending this letter ensures your coverage rates are optimized for your current lifestyle, potentially lowering monthly costs while maintaining essential protection for your simplified household needs.

How do I notify my insurance company about downsizing as an empty nester?

To notify your insurer, you must submit a formal "Notice of Risk Change" letter. This document should detail your move from a larger family home to a smaller residence, providing your new address, the reduced square footage, and updated replacement cost estimates to ensure your premiums are adjusted downward to reflect the smaller property.

What details should be included in an Empty Nester Downsizing Insurance Adjustment Letter?

Your letter should include your current policy number, the effective date of your move, the specifications of your new smaller home, and a request for a "Contents Coverage" re-evaluation. Since downsizing usually involves disposing of furniture and belongings, your personal property limits should be lowered to avoid paying for unnecessary coverage.

Can downsizing to a smaller home lower my homeowners insurance premiums?

Yes, downsizing often leads to lower premiums because the cost to rebuild a smaller home is typically less than a large family home. Your adjustment letter serves as the formal request for the underwriter to recalculate your rate based on the reduced liability, smaller footprint, and potentially newer, more efficient building materials in a downsized property.

Do I need to update my personal property floater when downsizing?

Absolutely. When writing your adjustment letter, specifically mention any high-value items you sold or donated during the move. Removing scheduled items-such as jewelry, art, or specialized equipment no longer in your possession-from your policy will significantly reduce your monthly insurance costs.

How does moving to a "55 plus" community affect my insurance adjustment?

If your downsizing move is into a retirement or 55+ community, you should highlight this in your letter. Many insurance providers offer "Mature Homeowner" discounts for empty nesters in these communities, as they are statistically viewed as lower risk due to increased security and a constant presence on the property.

Comments