Secure your financial future by understanding how a Retirement Asset Protection Annuity Letter can safeguard your savings from creditors and market volatility. This essential document helps formalize your strategy for long-term wealth preservation and reliable income. Learn how to draft a professional request to shield your hard-earned nest egg effectively. To help you get started, below are some ready to use template.

Image cover: Securing Your Future: Essential Annuity Letter Templates for Retirement Asset Protection

Letter Samples List

- Initial Introduction To The Retirement Asset Protection Annuity Letter

- Post-Consultation Follow-Up Retirement Asset Protection Annuity Letter

- Annual Policy Review For Your Retirement Asset Protection Annuity Letter

- Market Volatility And Your Retirement Asset Protection Annuity Letter

- Approaching Retirement Milestone Asset Protection Annuity Letter

- Policy Delivery Confirmation For The Retirement Asset Protection Annuity Letter

- Tax Deferral Benefits Of The Retirement Asset Protection Annuity Letter

- Beneficiary Designation For Your Retirement Asset Protection Annuity Letter

- Income Rider Election On The Retirement Asset Protection Annuity Letter

- Spousal Continuation Of The Retirement Asset Protection Annuity Letter

- Required Minimum Distribution From Your Retirement Asset Protection Annuity Letter

- Contract Anniversary For The Retirement Asset Protection Annuity Letter

Initial Introduction To The Retirement Asset Protection Annuity Letter

The Retirement Asset Protection Annuity Letter serves as a vital guide for securing your financial future against market volatility. This document introduces strategies to shield savings from economic downturns while ensuring a steady income stream. By focusing on guaranteed returns and principal preservation, the letter explains how to mitigate risks associated with traditional investments. Understanding these protective measures is essential for anyone seeking long-term stability and peace of mind during their retirement years, effectively balancing growth potential with comprehensive capital security.

Post-Consultation Follow-Up Retirement Asset Protection Annuity Letter

A Post-Consultation Follow-Up Retirement Asset Protection Annuity Letter is a professional summary sent after a financial meeting. It outlines strategies to secure your savings from market volatility using annuities. This document serves as a formal record of the discussed income solutions, tax advantages, and death benefits. It ensures the client understands how guaranteed lifetime income products safeguard their future. Reviewing this letter is essential for confirming that the proposed asset protection alignment matches your long-term retirement goals and risk tolerance before finalizing any legal contracts.

Annual Policy Review For Your Retirement Asset Protection Annuity Letter

An Annual Policy Review is a critical evaluation of your retirement asset protection annuity to ensure alignment with your financial goals. This formal letter serves as a compliance notification, inviting you to assess current interest rates, beneficiary designations, and withdrawal provisions. Regular audits help safeguard your principal against market volatility while optimizing tax-deferred growth. Reviewing your statement annually ensures your contract remains a robust income security tool, adapting to legislative changes or personal life shifts. Promptly responding to this review helps maintain the integrity of your long-term wealth preservation strategy.

Market Volatility And Your Retirement Asset Protection Annuity Letter

Protecting your retirement savings from market volatility is essential for long-term financial security. Your Asset Protection Annuity Letter outlines strategies to shield your principal from stock market downturns while maintaining growth potential. By utilizing fixed or indexed annuities, you can ensure a guaranteed income stream that remains unaffected by economic instability. This document provides the necessary framework to mitigate risk, preserve your hard-earned capital, and achieve peace of mind during uncertain cycles. Understanding these protective measures allows for a more stable and predictable retirement transition.

Approaching Retirement Milestone Asset Protection Annuity Letter

When you receive an Approaching Retirement Milestone Asset Protection Annuity Letter, it serves as a critical notification to secure your financial future. This document highlights options for transitioning from wealth accumulation to guaranteed lifetime income. It emphasizes safeguarding your nest egg against market volatility through asset protection strategies. Reviewing these updates ensures your portfolio aligns with your current risk tolerance, providing a stable foundation for a worry-free retirement. Consult a financial professional to evaluate how these annuity provisions can protect your principal while maintaining essential liquidity as you exit the workforce.

Policy Delivery Confirmation For The Retirement Asset Protection Annuity Letter

The Policy Delivery Confirmation is a critical document for your Retirement Asset Protection Annuity. It serves as formal verification that you have received your contract, triggering the free-look period. During this timeframe, you can review all terms and conditions to ensure they meet your financial goals. Promptly signing and returning this letter is essential to activate coverage and finalize the transition of your assets. This process safeguards your investment by confirming your informed consent and legal acceptance of the annuity agreement.

Tax Deferral Benefits Of The Retirement Asset Protection Annuity Letter

The Retirement Asset Protection Annuity Letter highlights how tax-deferred growth maximizes long-term wealth accumulation. By postponing income taxes on investment gains, your principal remains fully invested to generate compound interest. This strategy protects your savings from immediate tax erosion, providing a robust financial cushion for the future. Understanding these tax deferral benefits is essential for optimizing retirement distributions and ensuring asset preservation. Efficient tax planning through this structure allows retirees to control their taxable income timing, ultimately lowering their overall lifetime tax liability while securing their financial legacy.

Beneficiary Designation For Your Retirement Asset Protection Annuity Letter

A beneficiary designation is the most critical component of your retirement asset protection annuity letter. This legal instruction determines who inherits your funds, bypassing the lengthy probate process. It is essential to name specific individuals or entities and keep these records updated after major life events like marriage or divorce. Because these designations typically override instructions in a will, ensuring accuracy guarantees that your wealth is transferred according to your current wishes while maximizing tax efficiency for your heirs and protecting your long-term legacy.

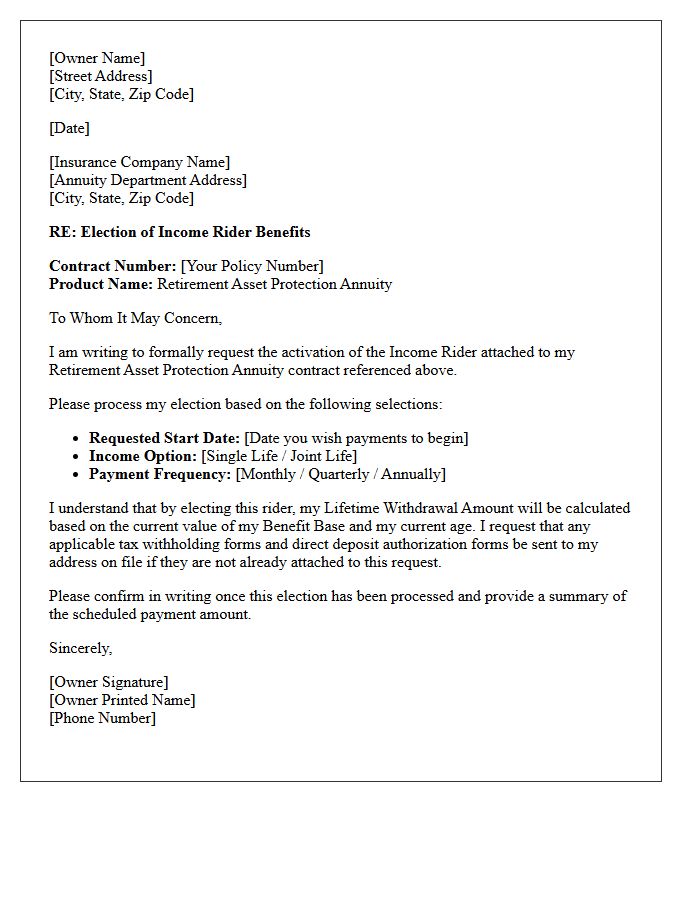

Income Rider Election On The Retirement Asset Protection Annuity Letter

The Income Rider Election is a critical decision point found within your Retirement Asset Protection Annuity letter. This feature allows you to secure a guaranteed lifetime income stream, regardless of market performance. By electing this rider, you ensure that your principal remains protected while establishing a predictable payout for the future. It is essential to review the specific fees and activation dates associated with this benefit to maximize your long-term financial security. Consulting with a specialist can help determine if this election aligns with your personal retirement goals and risk tolerance.

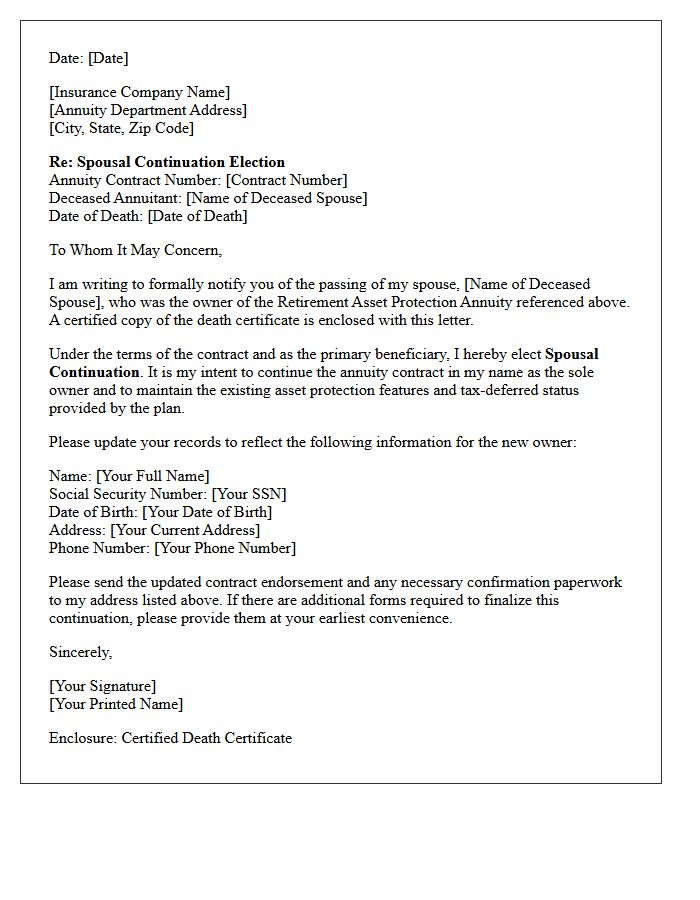

Spousal Continuation Of The Retirement Asset Protection Annuity Letter

The Spousal Continuation clause is a vital feature of the Retirement Asset Protection Annuity. It allows a surviving spouse to maintain the contract's tax-deferred status and guaranteed income benefits without triggering immediate surrender charges or tax penalties. This legal provision ensures financial stability by transferring ownership directly to the partner, preserving the original death benefit protections. Understanding this letter is essential for effective estate planning, as it secures long-term wealth preservation and prevents the loss of accumulated assets upon the primary policyholder's passing.

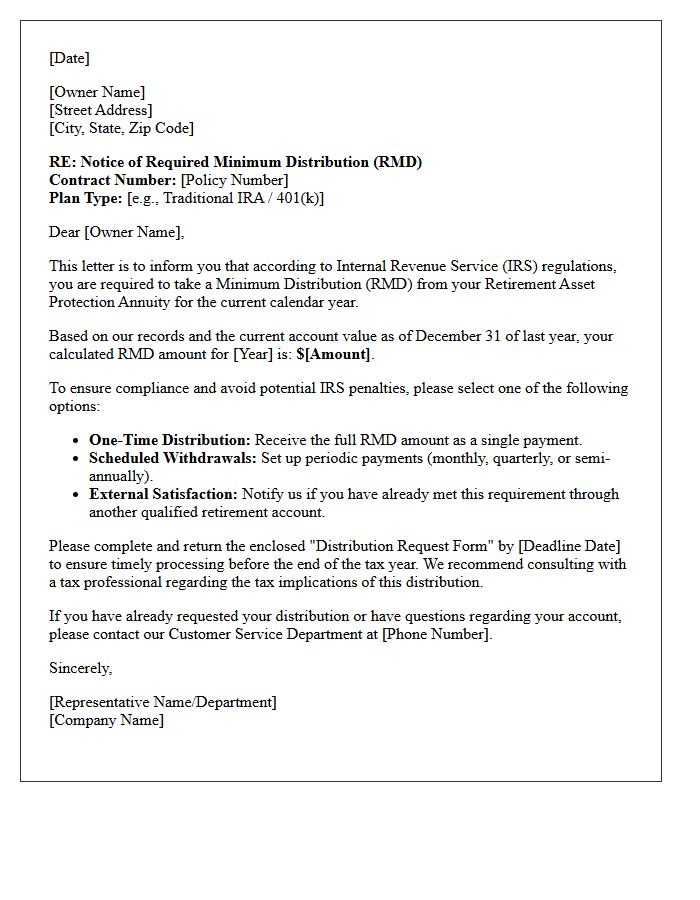

Required Minimum Distribution From Your Retirement Asset Protection Annuity Letter

If you receive a Required Minimum Distribution (RMD) notice regarding your retirement assets, it signifies that federal law mandates you begin withdrawing a specific percentage annually. Failure to comply results in significant IRS tax penalties. This letter typically outlines your payout obligations and deadlines based on your age. It is crucial to verify the calculations to ensure your retirement income remains compliant. Always distinguish official financial notices from unsolicited marketing offers to protect your asset security and avoid potential scams targeting your retirement savings.

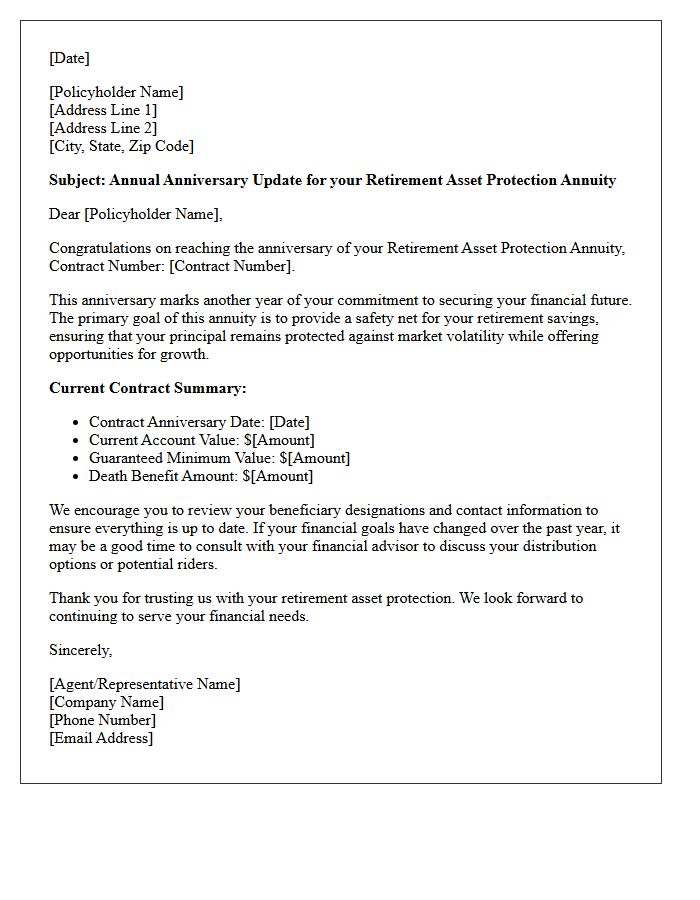

Contract Anniversary For The Retirement Asset Protection Annuity Letter

The Contract Anniversary letter for your Retirement Asset Protection Annuity is a vital annual update. It provides a detailed account summary, including your current contract value, earned interest, and any applicable guaranteed minimums. This document is essential for monitoring your long-term financial security and retirement goals. Reviewing this letter ensures you understand your policy's performance and allows you to make informed decisions regarding future withdrawals or beneficiary designations to maintain optimal asset protection throughout your golden years.

What is a Retirement Asset Protection Annuity Letter?

A Retirement Asset Protection Annuity Letter is a formal document issued by an insurance carrier or financial institution that confirms the placement of retirement funds into a protected annuity contract, designed to safeguard principal from market volatility and provide guaranteed lifetime income.

How does an annuity letter help protect my retirement savings?

The letter serves as legal certification that your assets are housed within a structured insurance product, which typically offers protection from creditors, lawsuit judgments (depending on state law), and downside market risk through fixed or indexed interest rate guarantees.

Are the funds mentioned in my protection letter accessible in an emergency?

While the letter outlines the protective structure of the annuity, most contracts include liquidity features such as penalty-free annual withdrawals or crisis waivers for long-term care, though early surrenders may be subject to fees and tax implications.

What is the difference between a standard account statement and a protection letter?

A standard statement tracks fluctuating market values, whereas a Retirement Asset Protection Annuity Letter specifically highlights the "floor" or minimum guaranteed value of your account, ensuring that your retirement baseline remains intact regardless of economic downturns.

Does a Retirement Asset Protection Annuity Letter guarantee lifetime income?

Yes, most protection letters verify the activation of an income rider or a life-contingency clause, which converts your protected principal into a predictable, monthly distribution that you cannot outlive.

Comments