A Notice of Payment Plan Default Letter is a formal notification sent to a debtor who has failed to meet agreed installment terms. This essential document outlines the missed payment, outstanding balance, and potential legal consequences if the breach is not rectified immediately. Maintaining clear records helps protect your financial interests. To assist you, below are some ready to use template.

Image cover: Payment Plan Default: Official Notice Templates and Compliance Guide

Letter Samples List

- Initial Notice of Payment Plan Default Letter

- Second Warning Payment Plan Default Letter

- Final Demand and Payment Plan Default Letter

- Breach of Fee Agreement Payment Default Letter

- Notice of Retainer Payment Plan Default Letter

- Suspension of Legal Services Default Letter

- Demand to Cure Payment Plan Default Letter

- Termination of Representation Default Letter

- Pre-Collection Payment Plan Default Letter

- Notice of Settlement Payment Default Letter

- Mediation Fee Payment Plan Default Letter

- Post-Judgment Payment Plan Default Letter

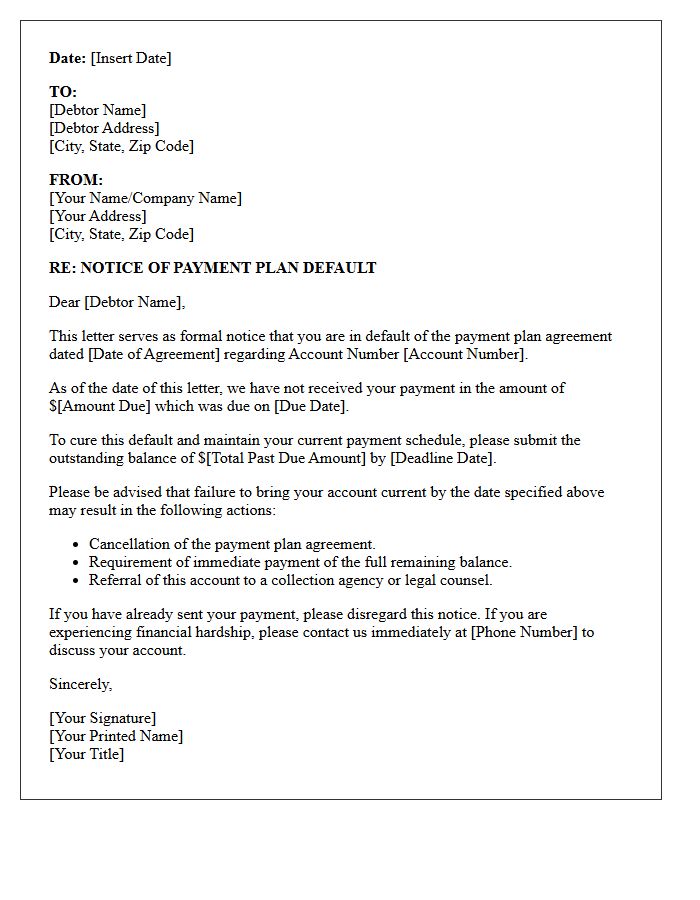

Initial Notice of Payment Plan Default Letter

An Initial Notice of Payment Plan Default Letter serves as a formal warning that you have breached your installment agreement. Receiving this document signifies that a scheduled payment was missed or underpaid, triggering a notice of intent to terminate the plan. It is crucial to act immediately by paying the arrears or contacting the creditor to reinstate the agreement. Ignoring this notice can lead to the acceleration of the total debt, additional penalties, and aggressive collection actions like wage garnishment or asset levies. Prompt communication is the best way to resolve the default.

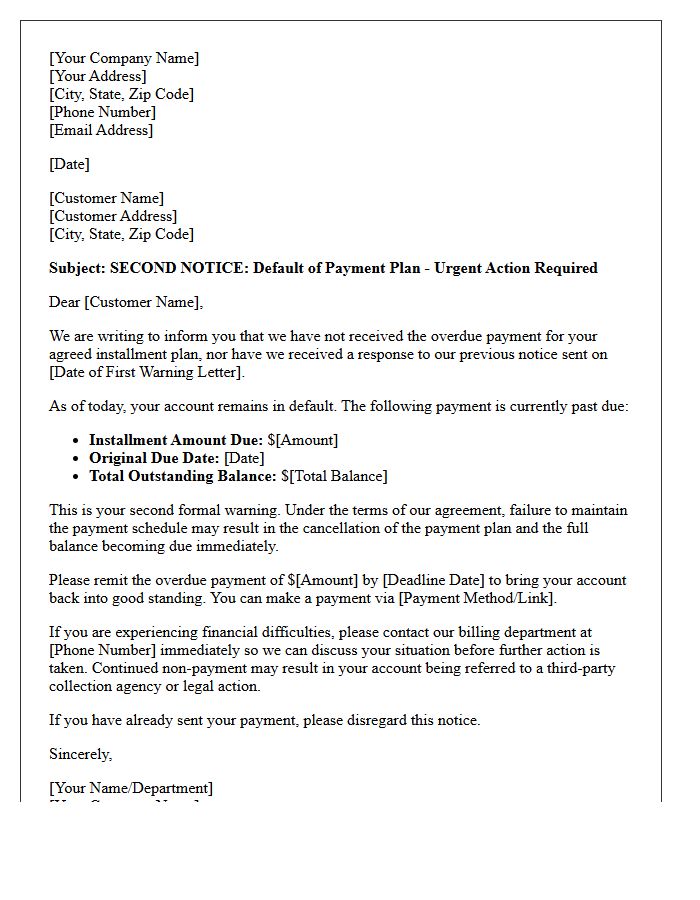

Second Warning Payment Plan Default Letter

A Second Warning Payment Plan Default Letter is a critical notification sent when a debtor fails to rectify missed payments after an initial alert. This document serves as a final opportunity to resolve the arrears before the agreement is officially terminated. It outlines the total outstanding balance, the consequences of continued non-compliance, and potential legal action or debt collection referrals. Prompt communication and immediate payment are essential to avoid damage to your credit score and the acceleration of the entire debt amount.

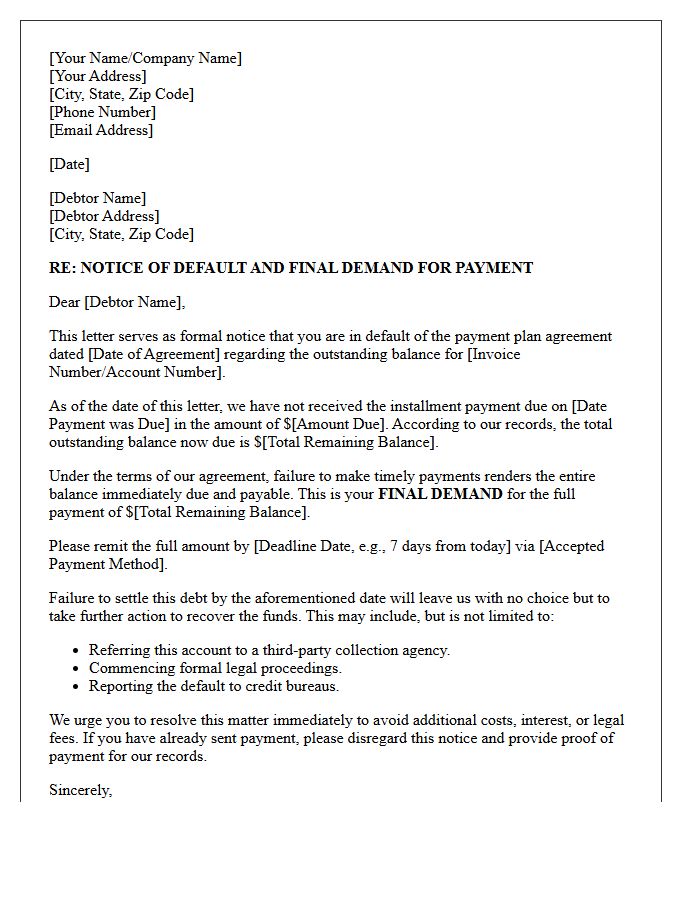

Final Demand and Payment Plan Default Letter

A Final Demand and Payment Plan Default Letter serves as a formal notification that a debtor has breached their repayment agreement. This legal document warns that unless the outstanding balance is settled immediately, the creditor will initiate debt recovery litigation or involve collection agencies. It clearly outlines the total arrears, the specific default date, and the deadline for final payment. Issuing this letter is a critical procedural step to demonstrate compliance before escalating the matter to court, providing a final opportunity to resolve the debt without further legal costs.

Breach of Fee Agreement Payment Default Letter

A Breach of Fee Agreement Payment Default Letter serves as a formal notice to a client who has failed to fulfill financial obligations. This legal document outlines the specific outstanding balance, references the original contract terms, and sets a strict deadline for remediation. It acts as a critical precursor to debt collection or litigation, providing evidence of non-payment. Clearly stating the consequences of continued default encourages immediate settlement while protecting your right to pursue further legal action to recover lost professional fees efficiently.

Notice of Retainer Payment Plan Default Letter

A Notice of Retainer Payment Plan Default Letter is a formal legal notification sent when a client fails to meet agreed installment obligations. This document serves as a final warning, highlighting the outstanding balance and specified grace period before services are suspended. It is crucial for maintaining a clear paper trail, protecting the provider's right to seek remedies or terminate the professional relationship. Timely delivery of this notice ensures transparency regarding contractual breaches while providing the client a final opportunity to restore their account standing and prevent litigation.

Suspension of Legal Services Default Letter

A Suspension of Legal Services Default Letter is a formal notice issued by a law firm when a client fails to meet financial obligations. This document serves as a final warning, informing the recipient that all legal work will cease unless outstanding fees are paid immediately. It outlines the specific breach of the retainer agreement and provides a deadline for resolution. Understanding this letter is crucial, as a suspension can lead to missed court deadlines or the complete withdrawal of representation, potentially jeopardizing the outcome of your legal matter.

Demand to Cure Payment Plan Default Letter

A Demand to Cure Payment Plan Default Letter is a formal notice sent to a debtor who has failed to meet agreed installment terms. This legal document serves as a final opportunity for the recipient to reinstate their standing by paying the overdue balance within a specific timeframe. It clearly outlines the total amount owed, the nature of the breach, and potential legal consequences if the default persists. Providing this notice is often a mandatory procedural step before a creditor can accelerate the debt or initiate formal litigation for recovery.

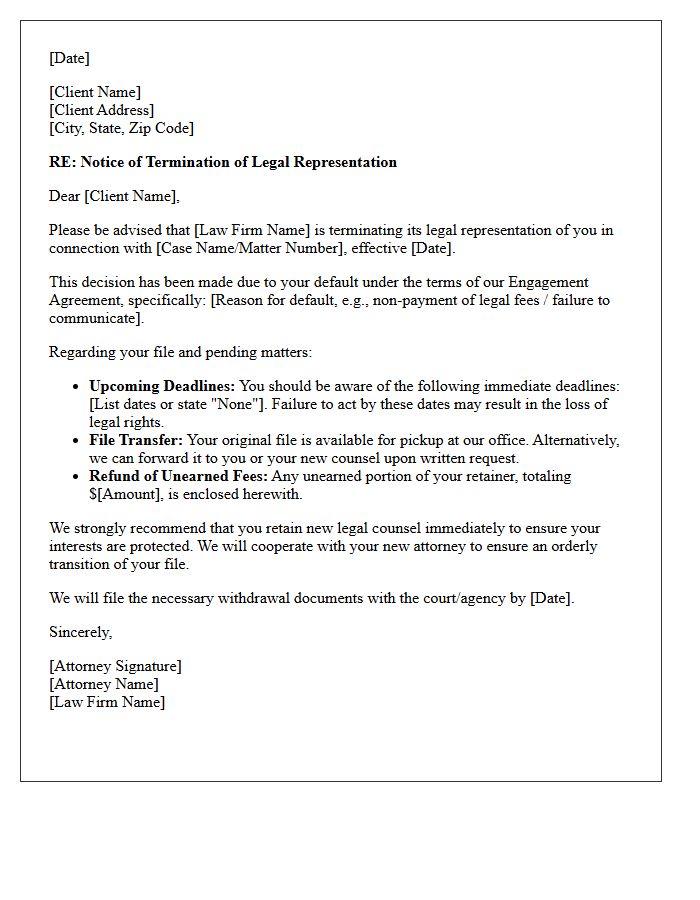

Termination of Representation Default Letter

A Termination of Representation Default Letter is a critical legal document issued when an attorney-client relationship ends due to a breach of contract, such as non-payment. It provides formal notice that legal services have ceased, protecting the lawyer from malpractice claims regarding future deadlines. To ensure compliance, the letter must clearly state the reason for withdrawal, outline pending court dates, and explain how the client can retrieve their case files. Properly documenting this transition is essential for maintaining professional standards and clarifying that the attorney is no longer responsible for the matter.

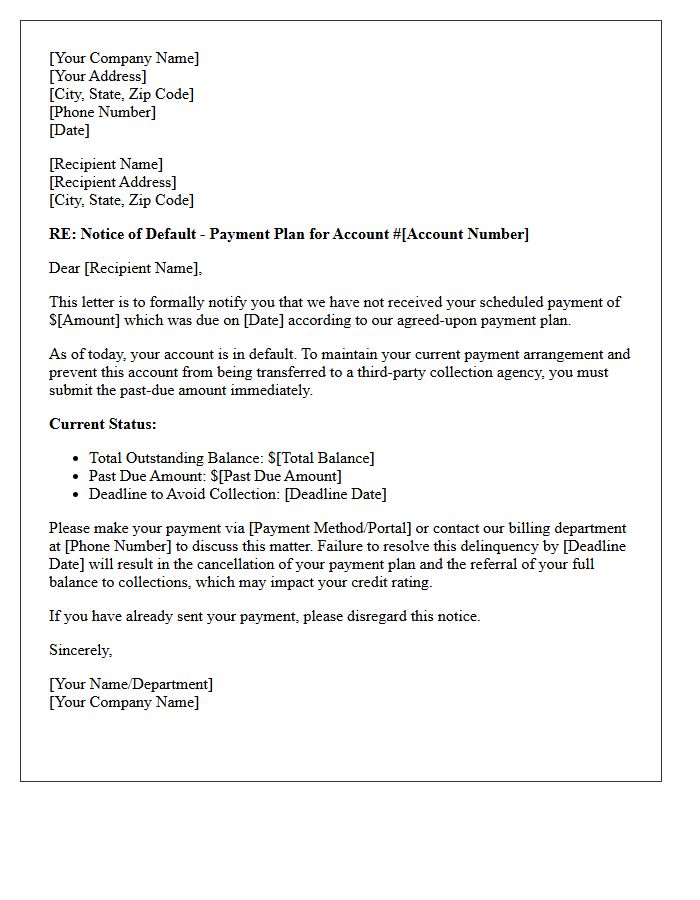

Pre-Collection Payment Plan Default Letter

A Pre-Collection Payment Plan Default Letter is a formal notice sent when a debtor fails to meet agreed installment terms. This document serves as a final warning before the account is escalated to a third-party collection agency or legal action is initiated. It outlines the missed payment details, the total outstanding balance, and a specific deadline for remediation. Receiving this letter is critical because it represents the last opportunity to preserve your credit score and avoid additional recovery fees by rectifying the breach of contract immediately.

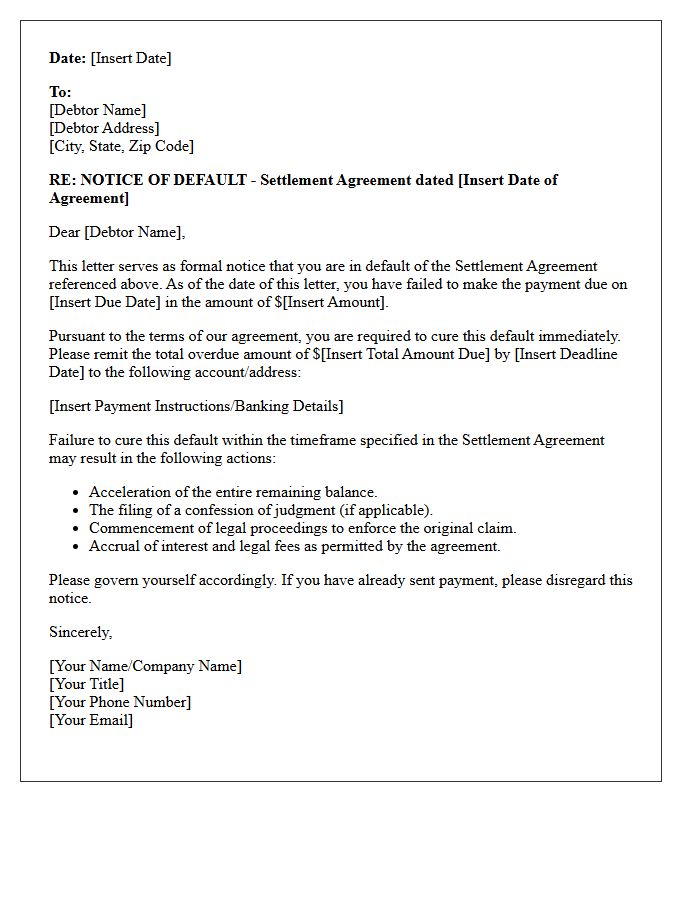

Notice of Settlement Payment Default Letter

A Notice of Settlement Payment Default Letter is a formal legal notification sent when a party fails to make a scheduled payment required by a settlement agreement. This document serves as an official warning that the recipient is in breach of contract. It typically outlines the missed amount, specifies a cure period to remedy the debt, and warns of impending legal consequences or the acceleration of the total balance. Issuing this letter is a critical procedural step to protect your rights before pursuing further litigation or enforcement actions to recover owed funds.

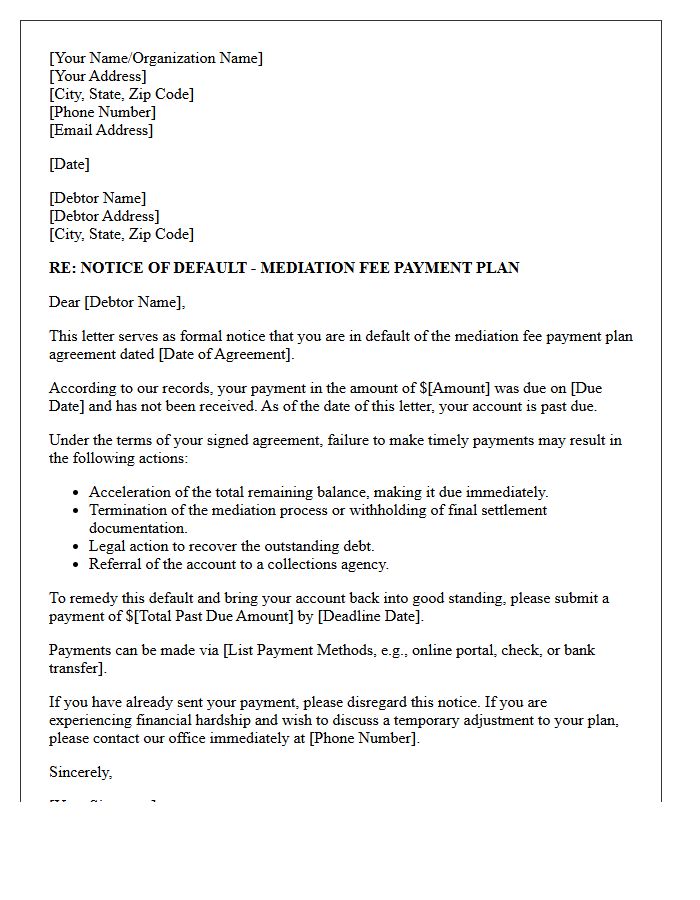

Mediation Fee Payment Plan Default Letter

A Mediation Fee Payment Plan Default Letter serves as a formal notice that a participant has failed to meet their scheduled financial obligations. This document outlines the outstanding balance and specifies a deadline to rectify the arrears to avoid further action. Receiving this letter indicates that the mediation agreement is at risk of being terminated, potentially leading to legal escalation or the suspension of dispute resolution services. It is crucial to respond immediately to negotiate a revised payment schedule or settle the debt to maintain the mediation process.

Post-Judgment Payment Plan Default Letter

A Post-Judgment Payment Plan Default Letter is a formal notification sent when a debtor fails to meet court-ordered installments. This legal document serves as notice of breach, informing the recipient that their repayment agreement is now void. Sending this letter is a critical step before escalating to aggressive enforcement actions, such as wage garnishment or asset seizure. It provides a final opportunity for the debtor to cure the default or face immediate judgment execution. Documenting this communication is essential for maintaining a clear evidentiary trail during ongoing legal recovery processes.

What is a Notice of Payment Plan Default Letter?

A Notice of Payment Plan Default Letter is a formal written notification sent to a debtor stating that they have failed to meet the agreed-upon terms of their installment agreement. This document serves as legal evidence that a breach of contract has occurred due to missed or incomplete payments.

What happens after receiving a notice of default on a payment plan?

After receiving the notice, the debtor typically has a specific "cure period" to pay the overdue balance. If the default is not rectified within the timeframe mentioned in the letter, the creditor may accelerate the debt, terminate the agreement, and pursue legal action or debt collection services.

Can I stop a payment plan default after receiving the letter?

Yes, most default notices include a provision to "cure" the default by paying the outstanding arrears by a certain date. It is highly recommended to contact the creditor immediately to discuss a reinstatement of the plan or to negotiate a one-time settlement to prevent further escalation.

What information should be included in a formal Notice of Default?

A valid notice must include the date of the default, the specific amount currently past due (including any late fees), the deadline to remedy the breach, and the specific actions the creditor will take if payment is not received, such as credit reporting or litigation.

Does a payment plan default letter affect my credit score?

While the letter itself is a private communication, the underlying default often leads to the creditor reporting the delinquency to major credit bureaus. If the account is handed over to a collection agency following the notice, it can significantly lower your credit score and remain on your report for up to seven years.

Comments