A Good Faith Demand is a critical legal tool used to encourage insurance carriers to settle claims within policy limits. By documenting clear liability and damages, you protect your client's rights and establish a basis for potential bad faith claims if the insurer acts unreasonably. Understanding the essential components of these demands ensures maximum recovery. Below are some ready to use templates.

Image cover: Policy Limit Demand Letter Templates: Securing Settlements through Good Faith Negotiation

Letter Samples List

- Law Firm Letterhead and Contact Information

- Date of the Good Faith Demand Letter

- Insurance Carrier Claims Adjuster Details

- Claim Number and Insured Party Identification

- Formal Declaration of Legal Representation

- Factual Summary of the Incident and Liability

- Comprehensive Description of Injuries Sustained

- Itemized Summary of Medical Bills and Expenses

- Calculation of Lost Wages and Future Damages

- Good Faith Demand for Insurance Policy Limits

- Time-Sensitive Deadline for Demand Acceptance

- Notice of Potential Bad Faith Litigation

- Index of Enclosed Supporting Documentation

- Executing Attorney Signature and Credentials

Law Firm Letterhead and Contact Information

A professional law firm letterhead serves as a critical branding tool and a legal requirement for formal correspondence. It must clearly display the firm's official name, physical office address, and direct contact details, including phone numbers and email. To ensure regulatory compliance, many jurisdictions also require listing licensed partners or specific jurisdictional disclosures. Consistent use of high-quality typography and layout establishes credibility and trust with clients and courts. Maintaining accurate contact information ensures seamless communication and reinforces the firm's professional identity in every legal document issued.

Date of the Good Faith Demand Letter

The Date of the Good Faith Demand Letter serves as the official starting point for legal notice in a dispute. It establishes a formal timeline for the recipient to respond before further litigation or insurance claims proceed. This specific date is critical because it proves the sender attempted to resolve the matter fairly without court intervention. In many jurisdictions, it also marks the commencement of potential accrued interest or statutory deadlines, making it a vital piece of evidence for demonstrating a sincere effort toward settlement.

Insurance Carrier Claims Adjuster Details

An insurance carrier claims adjuster is a professional employed by an insurer to evaluate property damage or personal injury. They determine the carrier's liability and calculate the settlement amount based on policy terms. Unlike public adjusters, they represent the company's financial interests. Understanding their investigation process is crucial, as they inspect evidence, interview witnesses, and review documentation to verify claims. Effective communication with them ensures a smoother claims resolution, but policyholders should always double-check the adjuster's assessment against their own records to ensure fair compensation under their specific coverage limits.

Claim Number and Insured Party Identification

A claim number is the unique identifier assigned by an insurance company to track a specific loss event. It is essential for all communication, ensuring your file is processed accurately. Parallel to this, insured party identification verifies the policyholder's identity using personal details like full name and policy number. Providing both accurately prevents administrative delays and protects against fraud. Always keep these references ready when contacting adjusters to ensure a seamless claims settlement process and timely reimbursement for your covered losses.

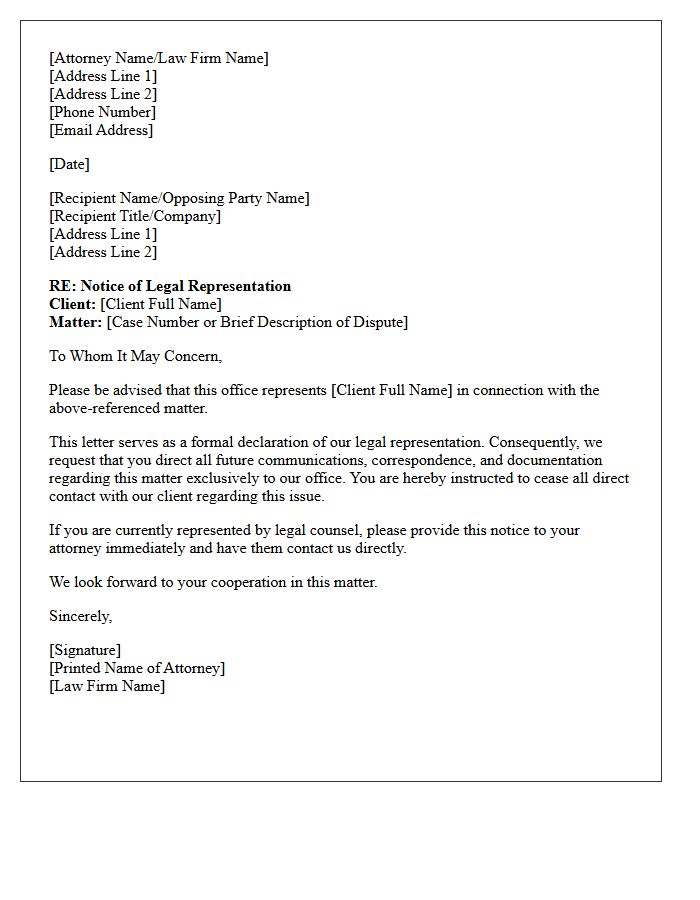

Formal Declaration of Legal Representation

A Formal Declaration of Legal Representation is a critical document notifying courts and opposing parties that an attorney is authorized to act on a client's behalf. This letter of representation establishes professional boundaries, ensuring all future communications are directed solely to the legal counsel. It protects the client's rights while providing the lawyer with the necessary standing to manage filings and negotiations. Filing this notice is essential for maintaining procedural integrity and ensuring that the legal system recognizes the official attorney-client relationship during litigation or administrative proceedings.

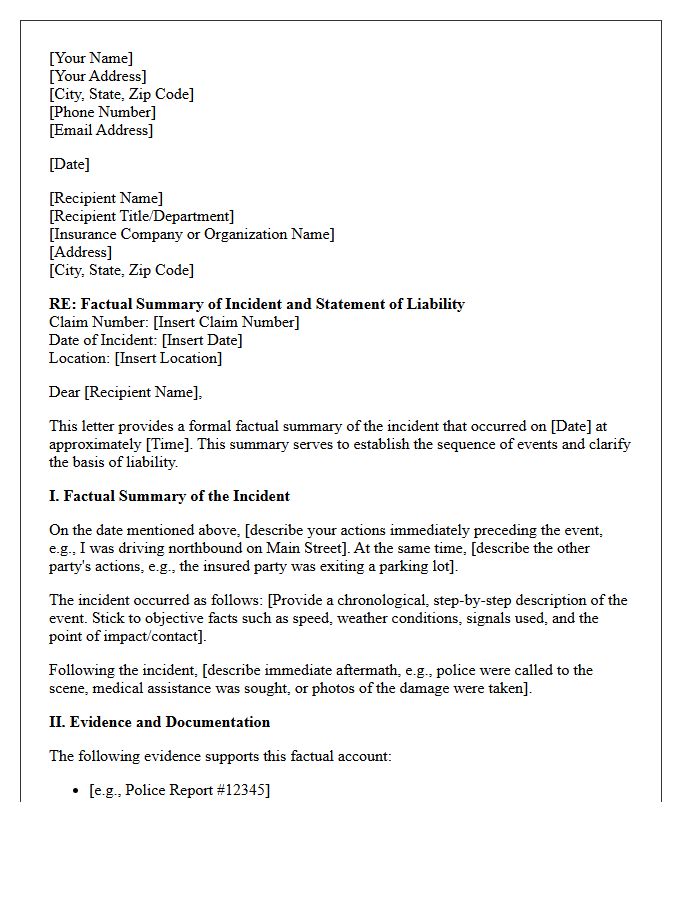

Factual Summary of the Incident and Liability

A factual summary establishes the objective sequence of events during an accident or dispute. It identifies the parties involved, chronological actions, and evidentiary findings. Determining liability is the most critical outcome, as it assigns legal responsibility for damages. This process relies on negligence analysis to prove a breach of duty. Clear documentation ensures that fault is accurately attributed based on state laws or contractual obligations. By consolidating facts and witness statements, legal professionals can assess financial accountability and resolve insurance claims or litigation effectively.

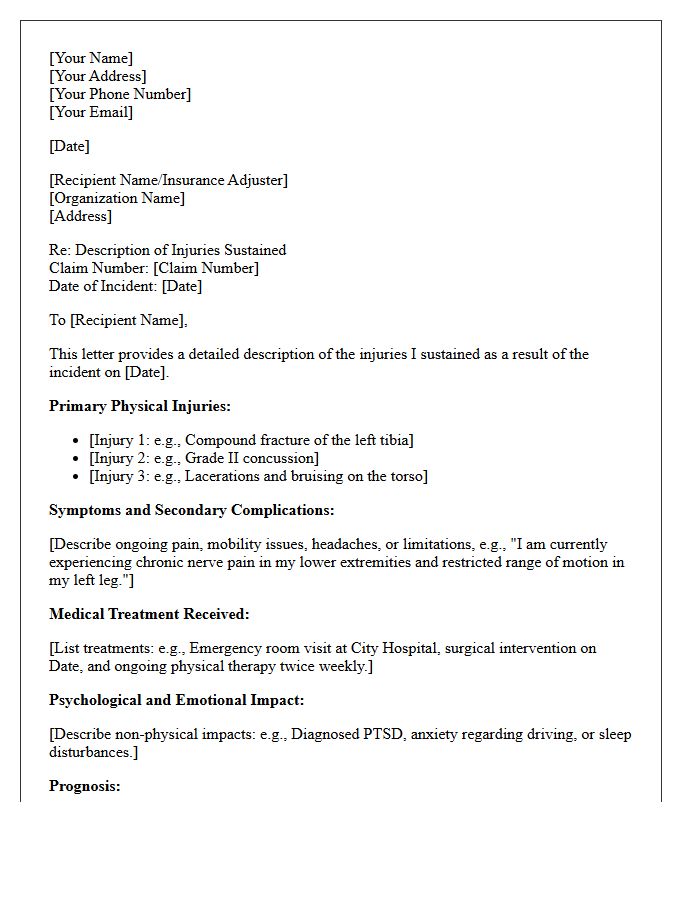

Comprehensive Description of Injuries Sustained

A Comprehensive Description of Injuries Sustained is a vital medical and legal document detailing every trauma identified after an accident. It systematically records primary injuries, secondary complications, and long-term prognosis to ensure clinical accuracy. For insurance claims or litigation, this report serves as definitive evidence, linking specific physical or psychological harm to the causative event. Precise terminology and diagnostic evidence, such as imaging and specialist evaluations, are essential to substantiate the severity, treatment requirements, and total impact on the victim's quality of life and future functional capacity.

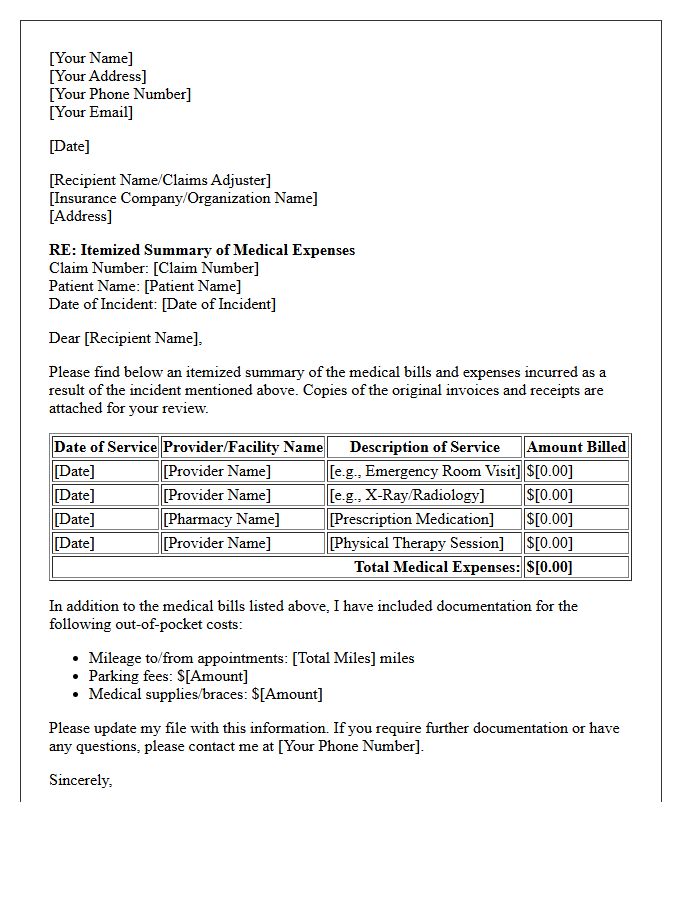

Itemized Summary of Medical Bills and Expenses

An Itemized Summary of Medical Bills and Expenses is a comprehensive document detailing every specific service, procedure, and medication provided during treatment. It is essential for verifying billing accuracy and identifying potential errors or duplicate charges. Patients should request this statement to reconcile costs with their insurance provider's Explanation of Benefits. Maintaining organized records ensures transparency, supports reimbursement claims, and serves as vital evidence for tax deductions or legal settlements. Always review each line item to ensure you only pay for the healthcare services you actually received.

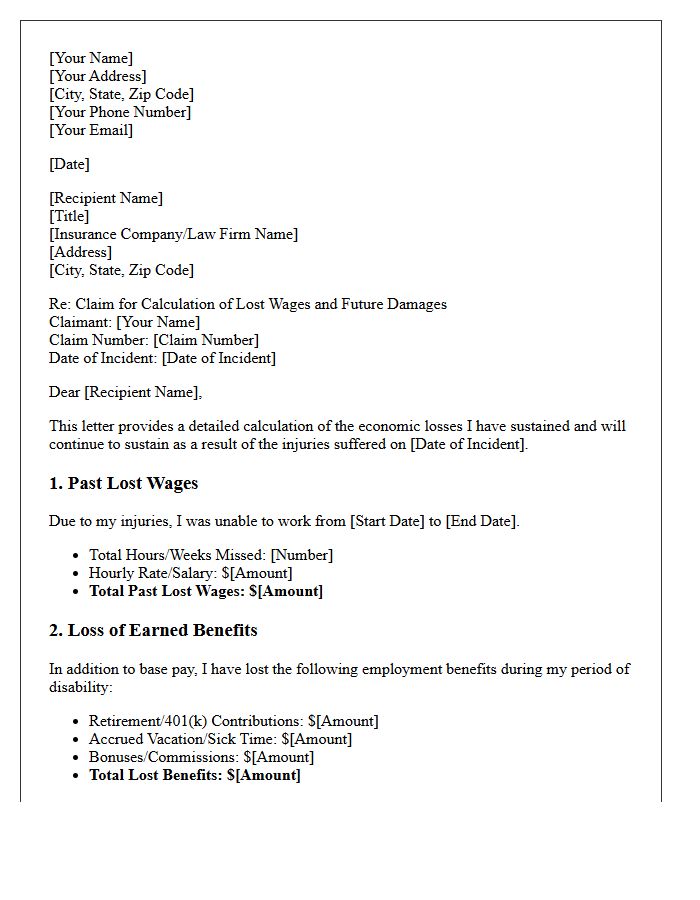

Calculation of Lost Wages and Future Damages

The calculation of lost wages involves documenting missed income from the time of injury until settlement. For long-term impacts, future damages account for diminished earning capacity, considering factors like career trajectory, inflation, and life expectancy. These calculations often require expert vocational or economic analysis to prove the total financial loss accurately. Ensuring all bonuses, commissions, and benefits are included is essential for a comprehensive personal injury claim. Accurate projections ensure victims receive fair compensation for the permanent loss of their professional livelihood and long-term financial stability.

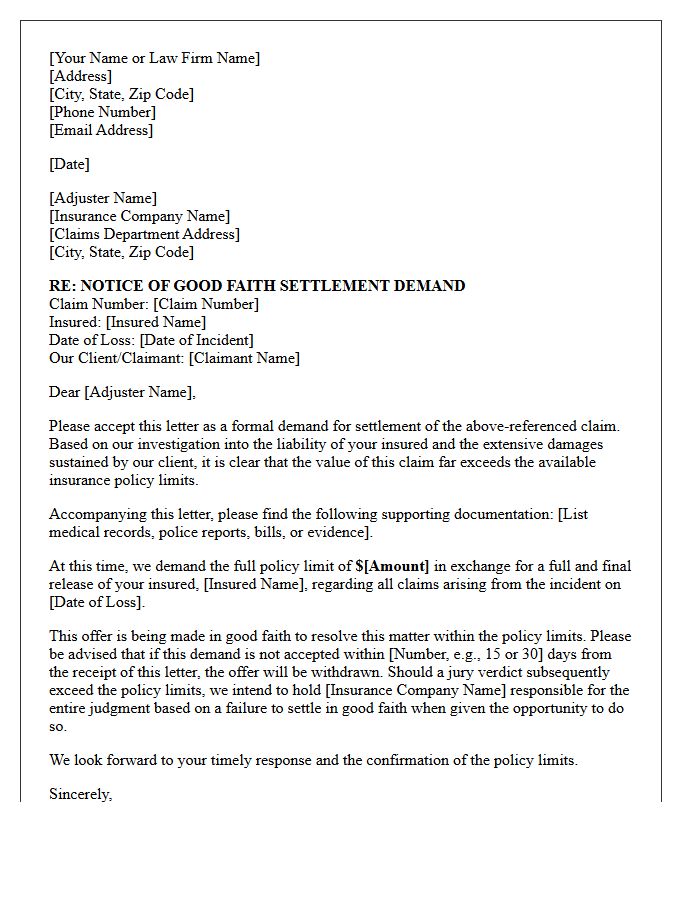

Good Faith Demand for Insurance Policy Limits

A good faith demand is a legal strategy used to settle a claim within insurance policy limits. It requires the insurer to evaluate a claim fairly and avoid exposing their policyholder to an excess judgment. If the insurance company unreasonably rejects a demand that meets all liability and damages criteria, they may be held liable for the entire court award, even if it exceeds the original coverage amount. This process protects victims from bad faith practices while ensuring insurers prioritize their duty to settle claims reasonably when liability is clear.

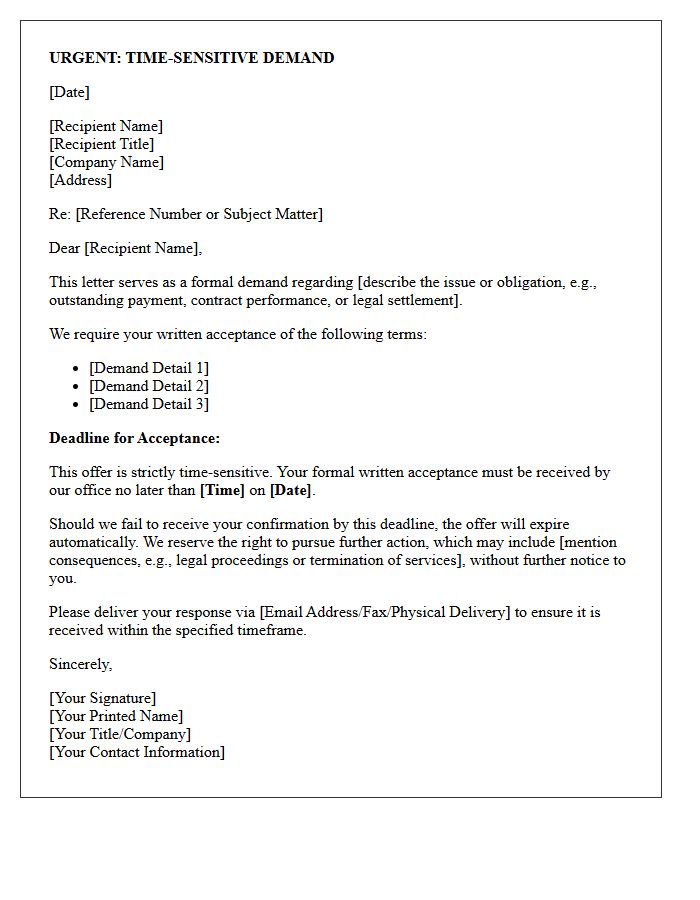

Time-Sensitive Deadline for Demand Acceptance

A time-sensitive deadline for demand acceptance is a critical legal window in settlement negotiations. If an insurance carrier fails to accept a reasonable offer within the specified timeframe, they may face bad faith claims for exposing their insured to excess liability. Properly documenting the offer and ensuring clear communication are essential for maintaining legal leverage. Missing this window can result in the loss of favorable settlement terms or increased litigation costs. Always prioritize strict compliance with the deadline to preserve your rights and maximize potential recovery outcomes.

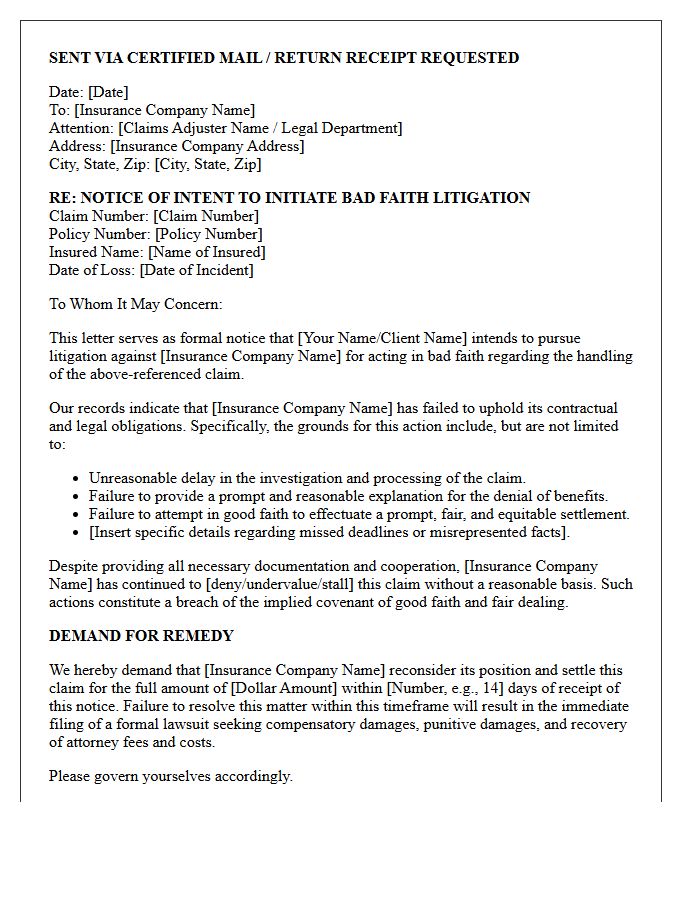

Notice of Potential Bad Faith Litigation

A Notice of Potential Bad Faith Litigation is a formal legal warning issued to an insurance provider. It asserts that the insurer failed to meet its fiduciary duty by unfairly denying, delaying, or underpaying a valid claim. This document serves as a prerequisite for seeking punitive damages beyond the policy limits. It alerts the company that their conduct is being monitored for unreasonable behavior or lack of investigation. Receiving this notice provides the insurer a final opportunity to settle the claim fairly before facing a high-stakes bad faith lawsuit in court.

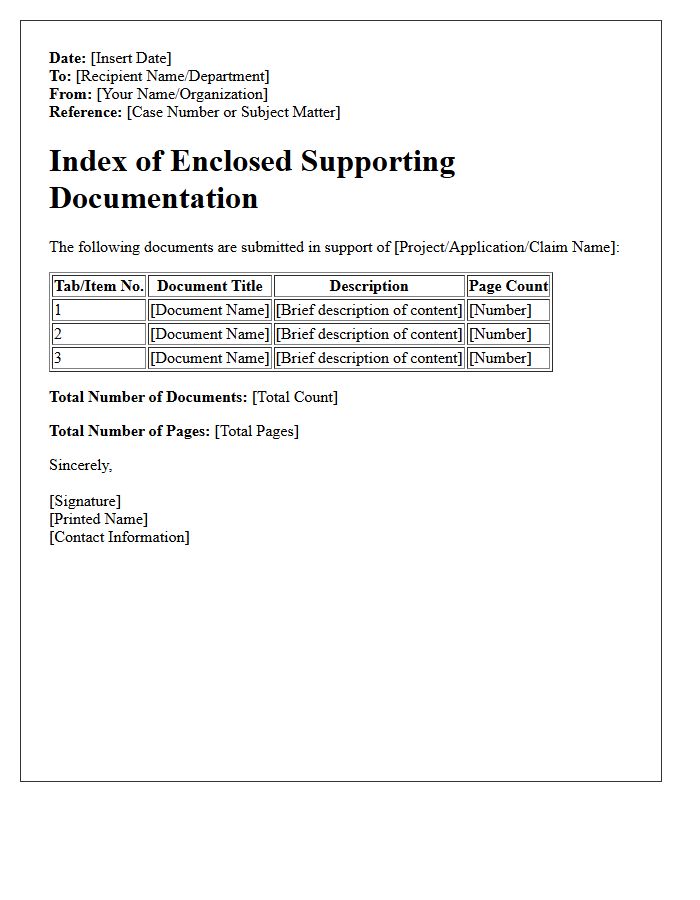

Index of Enclosed Supporting Documentation

The Index of Enclosed Supporting Documentation serves as a vital navigational tool for complex filings. It provides a structured list of all supplementary evidence, attachments, and exhibits included in a submission. By organizing records sequentially, it ensures that reviewers can quickly locate specific verification data. A precise index enhances clarity, professional credibility, and legal compliance, ensuring that every claim is backed by accessible, traceable proof within the primary document package.

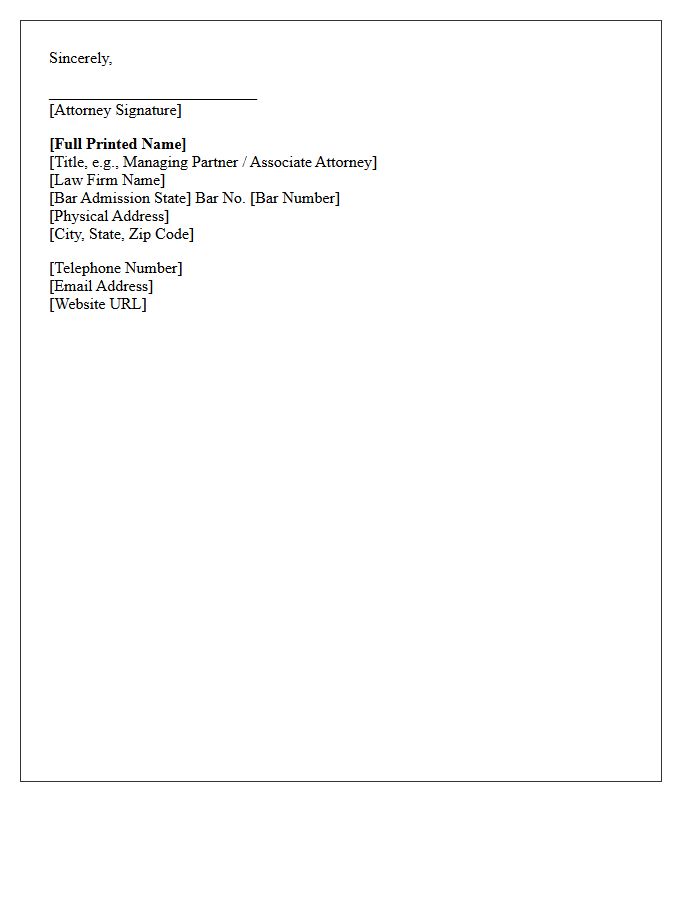

Executing Attorney Signature and Credentials

An executing attorney signature serves as a formal verification of a legal document's authenticity and compliance. It is essential that the signature is accompanied by professional credentials, such as a state bar number or jurisdictional identification, to confirm the lawyer's authority. This process ensures the instrument is legally binding and meets specific statutory requirements. Proper execution prevents fraud and establishes a clear chain of accountability within the legal system, making the inclusion of precise titles and licensing details a mandatory step for any enforceable agreement.

What is a good faith demand for policy limits?

A good faith demand is a formal legal request sent to an insurance carrier offering to settle a claim for the maximum amount of the available insurance coverage. It provides the insurer with a clear opportunity to resolve a claim within policy limits when liability is clear and damages exceed those limits.

What essential elements must be included in a policy limit demand letter?

To be legally effective, the demand must include a specific settlement amount, a clear deadline for acceptance, a complete release of the insured party, and comprehensive supporting documentation of liability and medical damages that justify the full policy amount.

How does a policy limit demand protect the claimant?

By making a reasonable demand within policy limits, the claimant sets the stage for a potential "bad faith" claim. If the insurer rejects a fair offer and a subsequent trial results in a verdict exceeding the policy limits, the insurer may be held liable for the entire judgment, regardless of the original coverage cap.

What is the "Stowers Doctrine" in the context of insurance demands?

The Stowers Doctrine (and similar legal principles in various states) imposes a duty on insurance companies to settle claims when an ordinarily prudent insurer would do so. If the carrier fails to accept a reasonable settlement offer within policy limits, they may be responsible for "excess judgments" rendered against their insured.

What constitutes "bad faith" by an insurance carrier after a demand is made?

Bad faith occurs when an insurance carrier prioritizes its own financial interests over the interests of its insured by failing to properly investigate a claim, ignoring clear evidence of liability, or refusing to settle within policy limits when the risks of an excess verdict are evident.

Comments