A Letter of Instruction provides a formal framework for a forensic accountant to investigate financial discrepancies, fraud, or asset valuation. It clearly defines the scope of work, legal deadlines, and reporting requirements to ensure professional clarity and expert precision. To help you draft this essential document efficiently, below are some ready to use templates.

Image cover: Expert Templates and Guide: Drafting an Effective Letter of Instruction to a Forensic Accountant

Letter Samples List

- Letter of Instruction for Marital Asset Tracing

- Letter of Instruction for Corporate Embezzlement Investigation

- Letter of Instruction for Partnership Valuation Dispute

- Letter of Instruction for Shareholder Oppression Analysis

- Letter of Instruction for Lost Profits Calculation

- Letter of Instruction for Personal Injury Economic Damages

- Letter of Instruction for Bankruptcy Fraud Investigation

- Letter of Instruction for Trust Mismanagement Audit

- Letter of Instruction for Intellectual Property Royalties Review

- Letter of Instruction for Business Interruption Claim

- Letter of Instruction for Hidden Asset Discovery

- Letter of Instruction for Contract Breach Financial Analysis

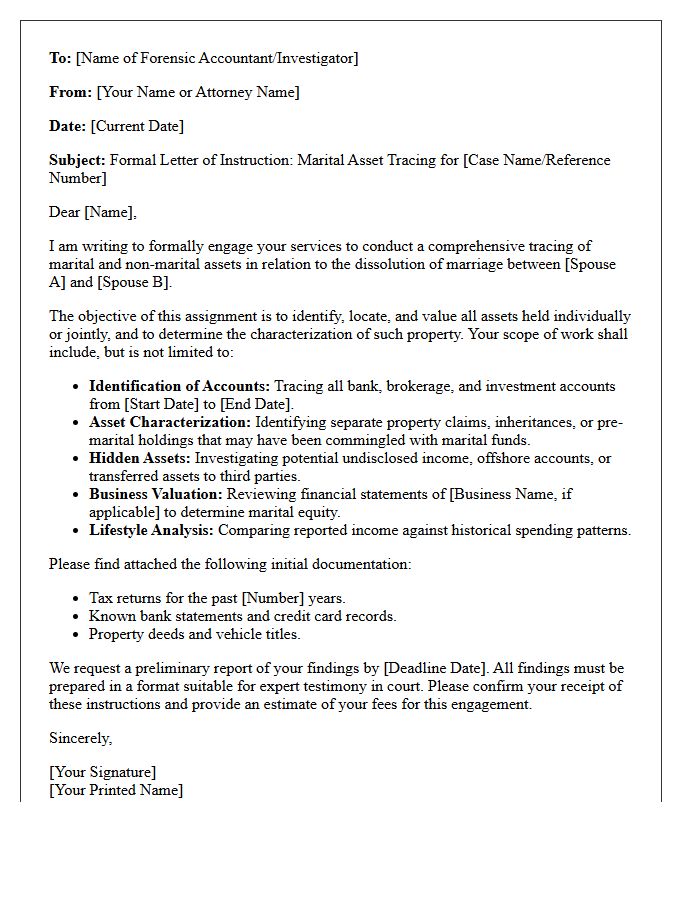

Letter of Instruction for Marital Asset Tracing

A Letter of Instruction for marital asset tracing is a formal mandate directing a forensic accountant to identify and value all joint and separate property. This document defines the scope of investigation, ensuring that hidden accounts, commingled funds, and dissipated assets are uncovered during divorce proceedings. By providing clear authority, it allows experts to scrutinize financial records to establish a fair equitable distribution. Understanding this letter is essential for protecting your financial interests and ensuring transparency throughout the legal discovery process.

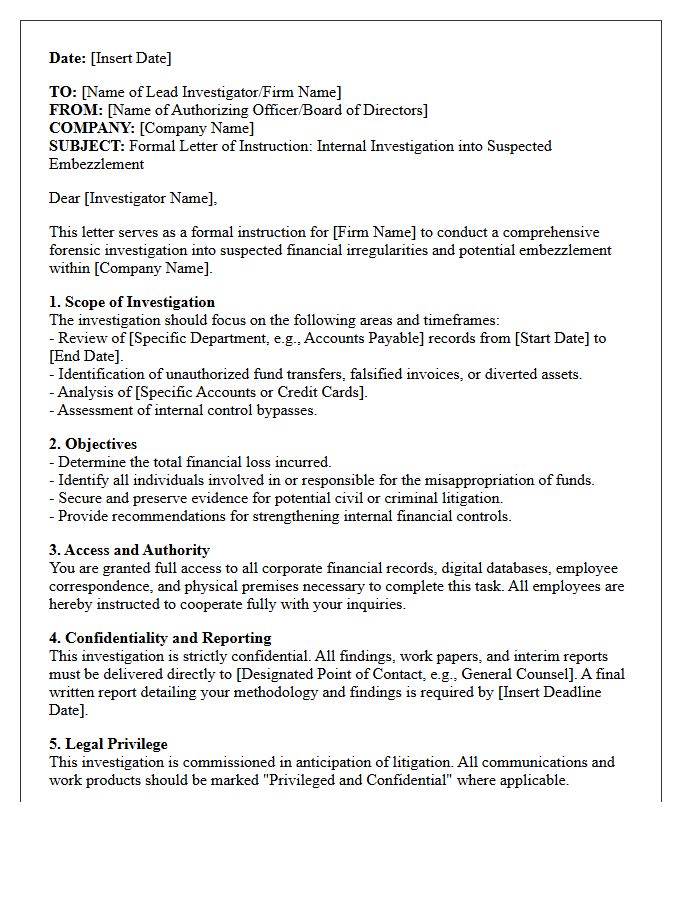

Letter of Instruction for Corporate Embezzlement Investigation

A Letter of Instruction provides the essential legal framework for a corporate embezzlement investigation. It defines the scope of work, granting forensic auditors or investigators authority to access confidential financial records. This document ensures clear communication between the board and the investigative team while maintaining evidentiary integrity. By outlining specific objectives and reporting protocols, it protects the organization from liability and ensures that findings remain admissible in court. Establishing these clear parameters is the most critical step in identifying internal fraud and initiating legal recovery actions against the perpetrators.

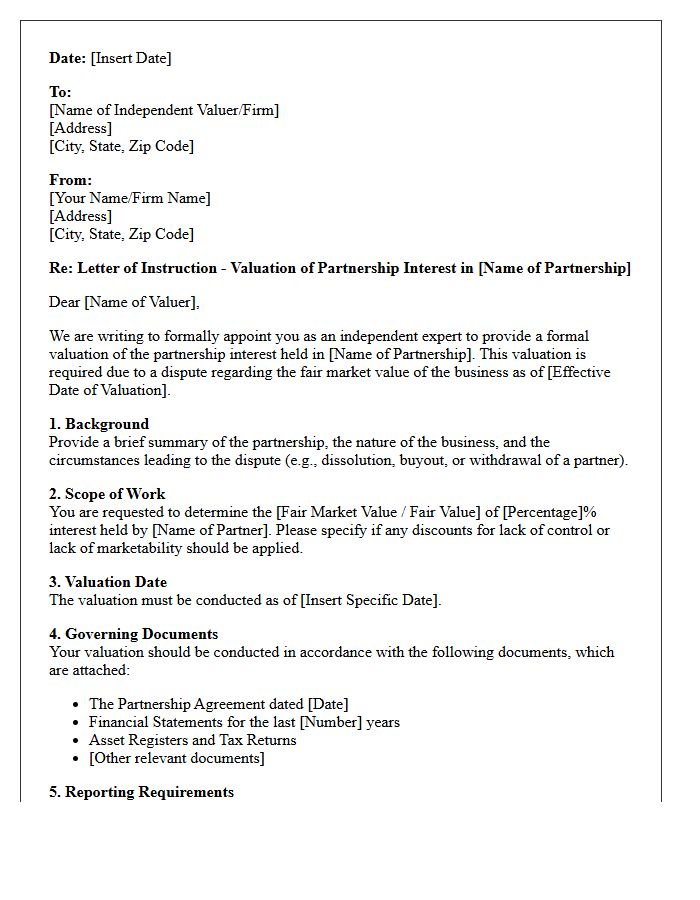

Letter of Instruction for Partnership Valuation Dispute

A Letter of Instruction is a critical document used to define the scope and methodology for an independent business appraiser during a partnership valuation dispute. It ensures transparency by outlining specific valuation dates, applicable legal standards, and the required valuation approach. By establishing clear guidelines, the letter minimizes bias and helps resolve conflicts regarding equity distribution or buyout terms. Providing precise instructions is essential for achieving a legally defensible and fair market value, ultimately facilitating a faster resolution and reducing potential litigation costs between disputing partners.

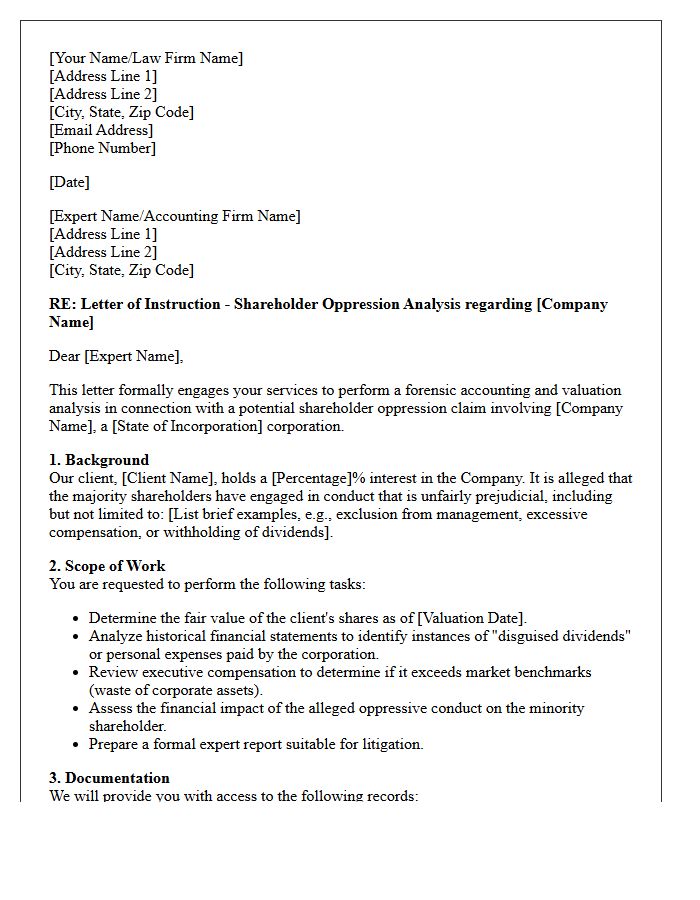

Letter of Instruction for Shareholder Oppression Analysis

A Letter of Instruction provides the essential framework for a forensic expert conducting a shareholder oppression analysis. This legal document defines the scope of the investigation, identifies specific prejudicial conduct, and outlines the valuation date. It ensures the expert focuses on unfairly crystalline actions, such as dividend withholding, exclusion from management, or waste of corporate assets. By clarifying the legal standards and financial records to be reviewed, the letter ensures the resulting report is robust, objective, and admissible for resolving internal corporate disputes or litigation.

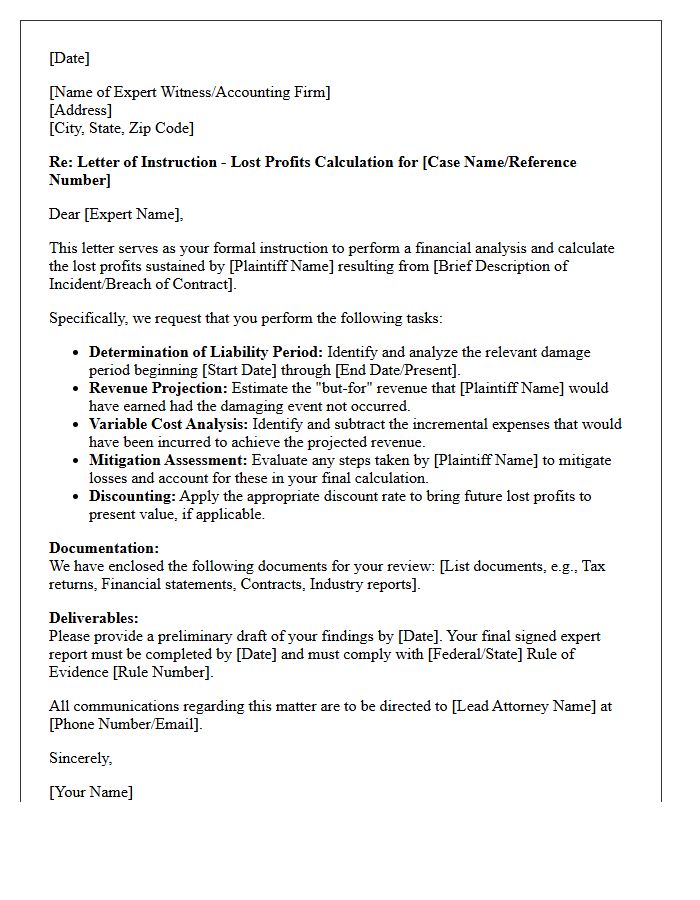

Letter of Instruction for Lost Profits Calculation

A Letter of Instruction provides a critical framework for experts calculating lost profits. It defines the legal standards, specific timeframes, and damage theories to be applied during the analysis. By clearly outlining allowable costs and revenue assumptions, the letter ensures the financial expert's testimony aligns with the case strategy. Precise instructions minimize methodological errors, helping to establish a credible link between the harmful act and the resulting economic loss, which is essential for a successful legal recovery in commercial litigation.

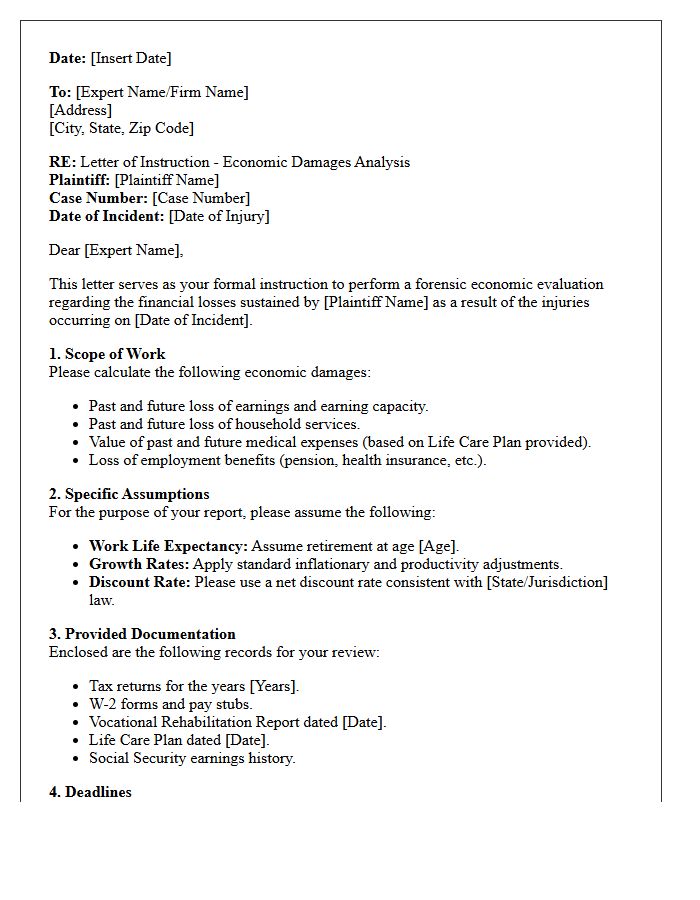

Letter of Instruction for Personal Injury Economic Damages

A Letter of Instruction acts as a critical roadmap for forensic experts calculating economic damages in personal injury litigation. This document outlines the specific scope of work, including the loss of earnings, medical expenses, and household services to be analyzed. It ensures the expert adheres to legal standards and uses accurate case facts to establish financial losses. Clear instructions prevent evidentiary challenges and help provide a defensible valuation of the plaintiff's past and future losses, ultimately supporting a fair settlement or trial verdict.

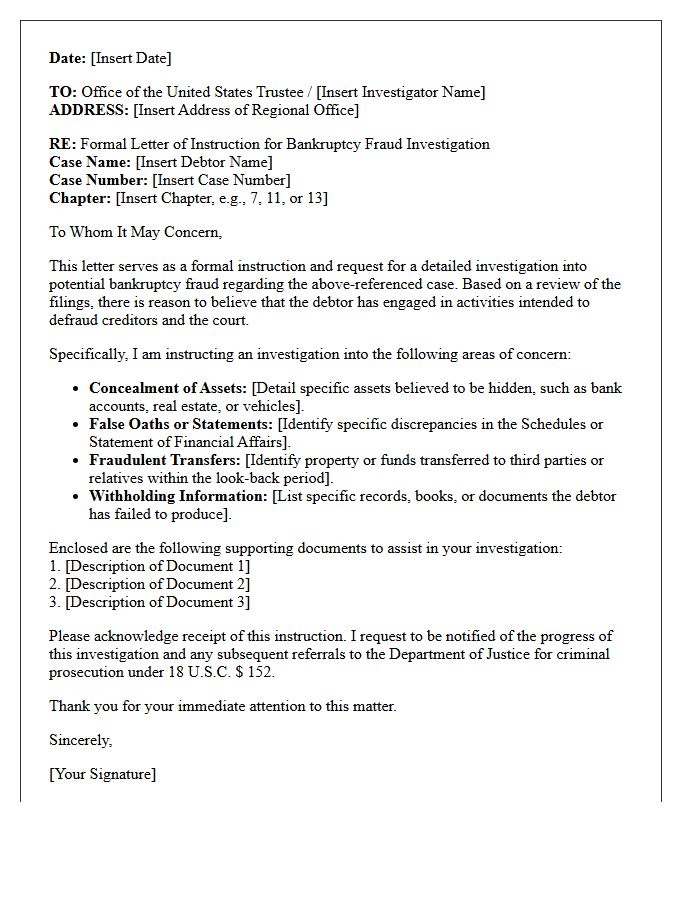

Letter of Instruction for Bankruptcy Fraud Investigation

A Letter of Instruction is a critical document directing a trustee or investigator to examine potential bankruptcy fraud. It outlines specific assets, undisclosed income, or suspicious transfers that require formal scrutiny. By providing clear evidence and actionable leads, this letter initiates a targeted investigation to ensure legal compliance. Creditors often use it to challenge a debtor's discharge if they suspect misrepresentation or concealment of property. Providing precise details helps authorities recover hidden value and maintain the integrity of the judicial process against fraudulent filings.

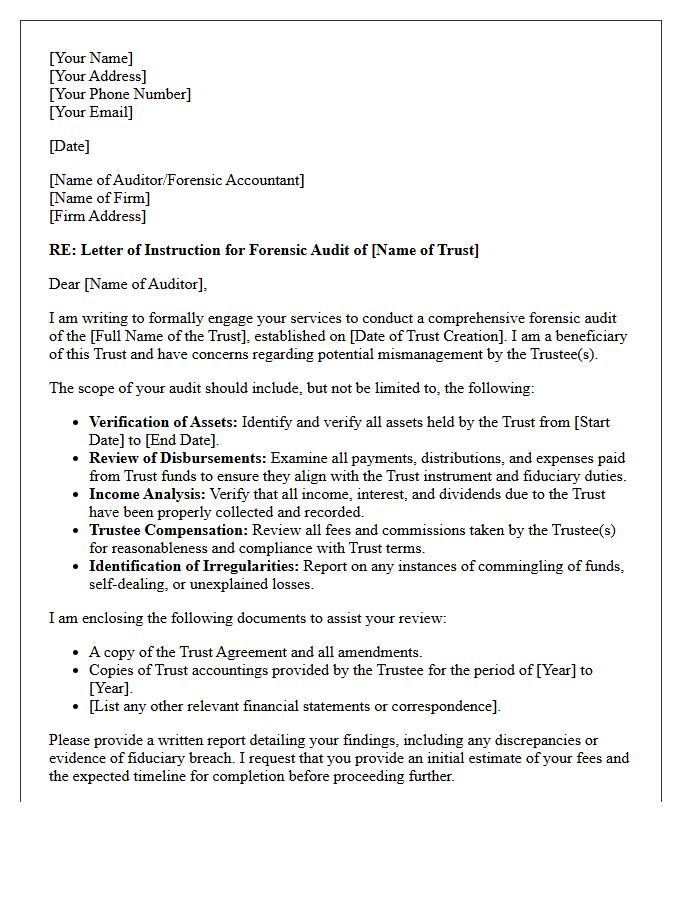

Letter of Instruction for Trust Mismanagement Audit

A Letter of Instruction initiates a formal Trust Mismanagement Audit to investigate potential breaches of fiduciary duty. This legal document authorizes an independent professional to examine financial records, investment choices, and distribution patterns. It highlights specific concerns regarding transparency or asset depletion. Providing clear directives ensures the auditor identifies accounting errors, self-dealing, or excessive fees. A well-drafted letter is the essential first step for beneficiaries seeking to hold trustees accountable, recover lost assets, and ensure the trust is administered according to its original terms and legal requirements.

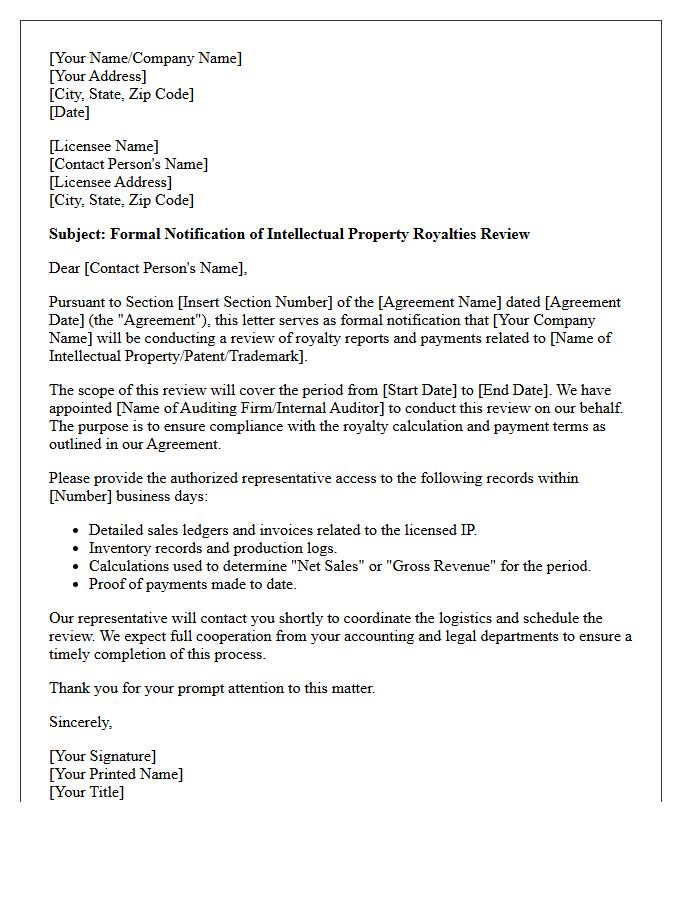

Letter of Instruction for Intellectual Property Royalties Review

A Letter of Instruction is a formal directive used to authorize an independent Intellectual Property Royalties Review. This document grants auditors the legal power to examine a licensee's financial records, ensuring accurate royalty payments and compliance with licensing agreements. It serves as the official trigger for a royalty audit, identifying underpayments or reporting errors. By clearly outlining the scope and access requirements, it protects the licensor's revenue streams and ensures transparency in legal obligations, making it a critical tool for protecting valuable intellectual property assets.

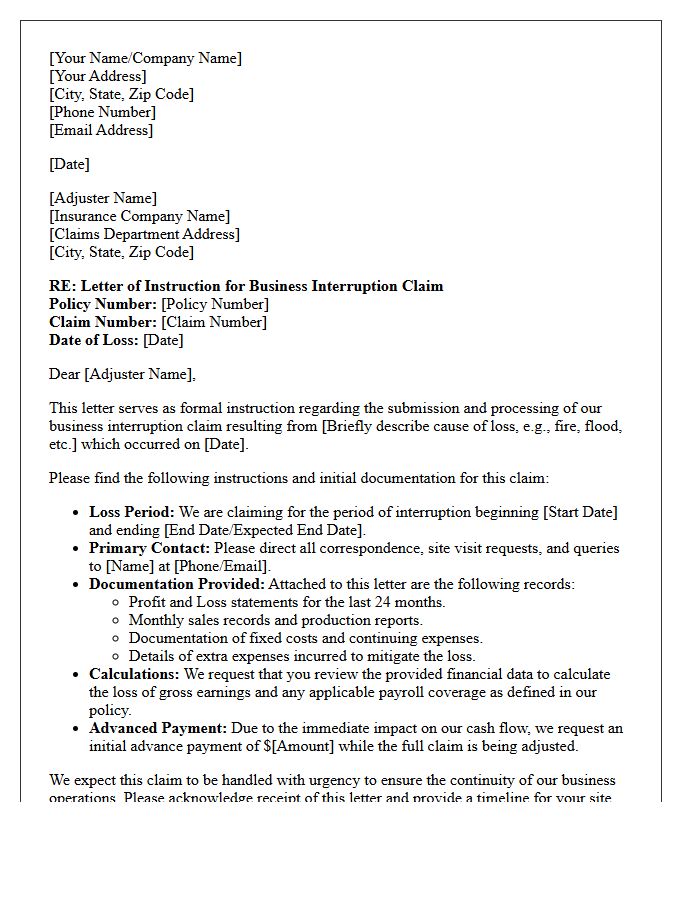

Letter of Instruction for Business Interruption Claim

A Letter of Instruction is a critical document that formally authorizes experts, such as forensic accountants, to quantify financial losses. It defines the scope of work, specific timeframes, and legal parameters required to validate a business interruption claim. Providing clear guidance ensures that the methodology aligns with policy terms, helping to prove lost profits and necessary operating expenses. This document serves as the foundation for a transparent, evidence-based recovery process, ensuring your insurance provider receives accurate data to facilitate a fair settlement and minimize processing delays.

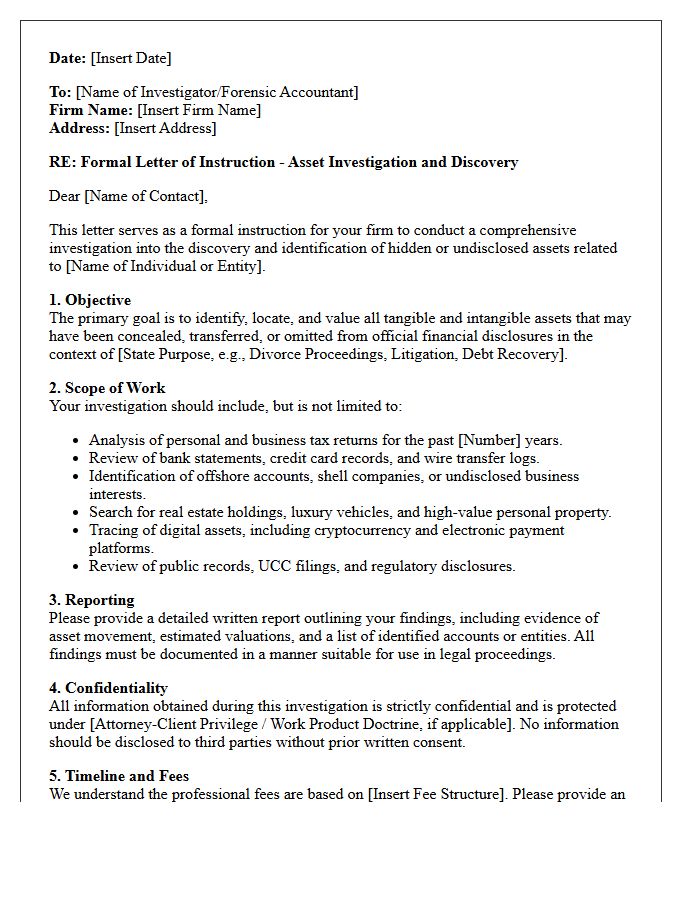

Letter of Instruction for Hidden Asset Discovery

A Letter of Instruction for hidden asset discovery serves as a formal mandate authorizing investigators to locate concealed wealth. It outlines the specific scope of the search, including offshore accounts, real estate, and shell companies. By providing clear legal standing, this document ensures that forensic accountants can access restricted financial records during divorce or litigation. Establishing a precise chain of custody and defining the search parameters are essential steps to uncover diverted funds and ensure an equitable distribution of marital or corporate property.

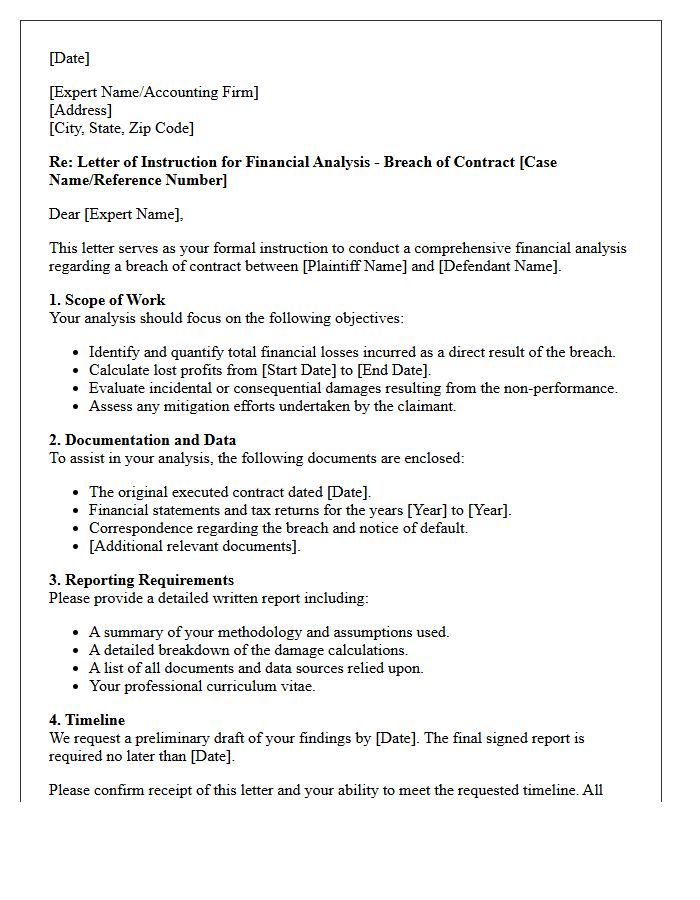

Letter of Instruction for Contract Breach Financial Analysis

A Letter of Instruction (LOI) is a critical document that directs a forensic accountant to perform a financial analysis regarding a contract breach. It must clearly define the scope of work, specific timeframes, and the methodology for calculating economic damages. By outlining the exact quantification of losses, such as lost profits or consequential damages, the LOI ensures the expert's findings are legally admissible and objective. Providing precise instructions and access to relevant financial records is essential for establishing a credible causation link between the breach and the resulting monetary impact.

What is a Letter of Instruction to a forensic accountant?

A Letter of Instruction (LOI) is a formal document issued by a legal professional or client that defines the scope, objectives, and parameters of a forensic accounting engagement. It serves as a guiding framework to ensure the expert's investigation aligns with legal requirements and the specific needs of the case.

What key components should be included in a Letter of Instruction for forensic accounting?

A comprehensive Letter of Instruction should include the background of the dispute, the specific questions the accountant must answer, a list of available financial records, the expected deadline, and the required format of the final report-whether it is for settlement purposes or expert witness testimony in court.

How does a Letter of Instruction ensure the admissibility of a forensic report in court?

By clearly defining the expert's duty to the court rather than the instructing party, the LOI reinforces the forensic accountant's independence. It ensures the expert follows relevant procedural rules (such as CPR Part 35 in the UK or Federal Rules of Evidence in the US), which is critical for the report to be accepted as evidence.

Can a Letter of Instruction be used to limit the scope of a financial investigation?

Yes. An LOI is essential for preventing "scope creep" by specifying exactly which accounts, time periods, and transactions the forensic accountant should analyze. This helps manage costs and ensures the expert focuses only on the financial issues relevant to the legal dispute.

Why is it important to update a Letter of Instruction during an ongoing forensic audit?

As new financial discrepancies or undisclosed assets are discovered, the original scope may become insufficient. Issuing a supplemental Letter of Instruction allows the client to formally expand the investigation's parameters, ensuring the forensic accountant has the authority to pursue new leads discovered during the initial review.

Comments