A Letter of Intent for Asset Purchase outlines the preliminary terms of a business acquisition, focusing on specific assets rather than the entire entity. It establishes the purchase price, deal structure, and due diligence period to ensure both parties align before signing a formal agreement. This document serves as a critical roadmap for your transaction. Below are some ready to use templates.

Image cover: Essential Asset Purchase Letter of Intent Templates and Professional Samples

Letter Samples List

- Purpose of the Letter of Intent

- Description of Law Firm Assets to Be Purchased

- Excluded Assets and Client Files

- Purchase Price and Payment Terms

- Assumption of Specific Liabilities

- Due Diligence Review Period

- Transition of Clients and Active Cases

- Confidentiality and Non-Disclosure Agreement

- Non-Compete and Non-Solicitation Covenants

- Conditions Precedent to Closing

- Allocation of Purchase Price

- Governing Law and Dispute Resolution

- Exclusivity and No-Shop Provision

- Binding and Non-Binding Terms of This Letter

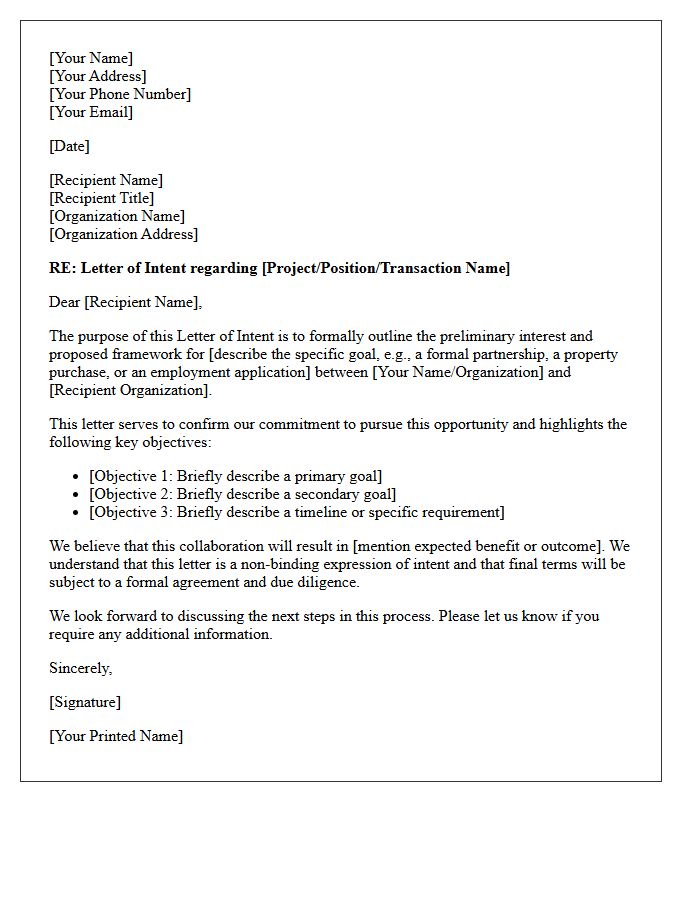

Purpose of the Letter of Intent

A Letter of Intent serves as a formal document outlining the preliminary commitment between two parties. Its primary purpose is to establish a mutual understanding of key terms before finalizing a binding contract. It clarifies the deal's structure, provides a framework for due diligence, and demonstrates serious intent to proceed. By defining essential expectations and milestones early on, it helps prevent future misunderstandings, ensuring both sides are aligned on the core objectives of the proposed transaction or business agreement.

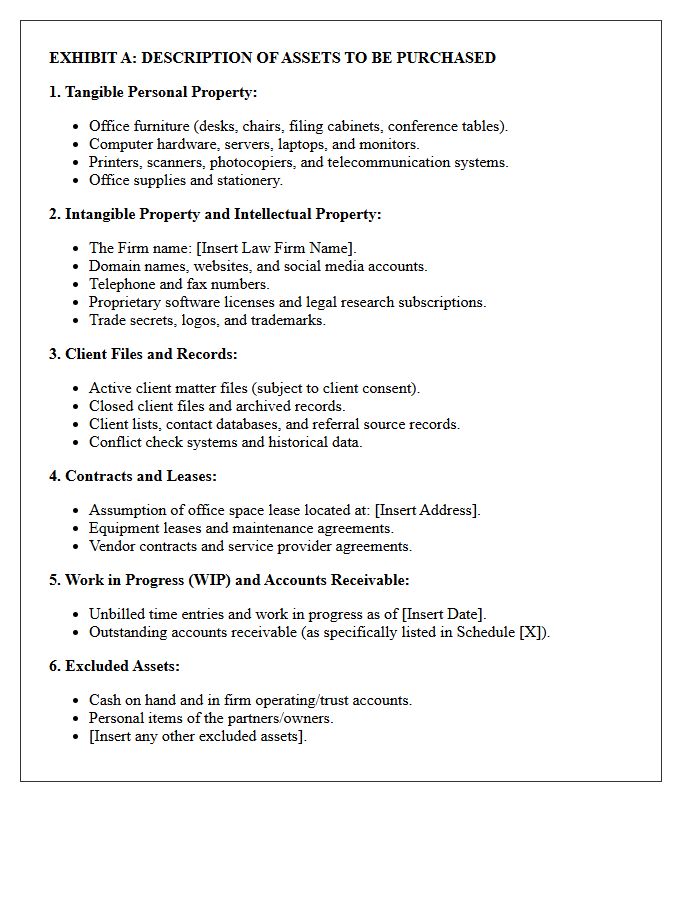

Description of Law Firm Assets to Be Purchased

When executing an Asset Purchase Agreement, identifying specific law firm assets is critical. Key components include tangible property like office equipment, furniture, and technology infrastructure. More importantly, intangible assets such as work-in-progress, client files, and goodwill define the firm's market value. Transitioning client contracts requires strict adherence to ethical obligations and privacy laws. Additionally, intellectual property, including trade names and digital domains, must be formally transferred to ensure brand continuity and operational success during the acquisition process.

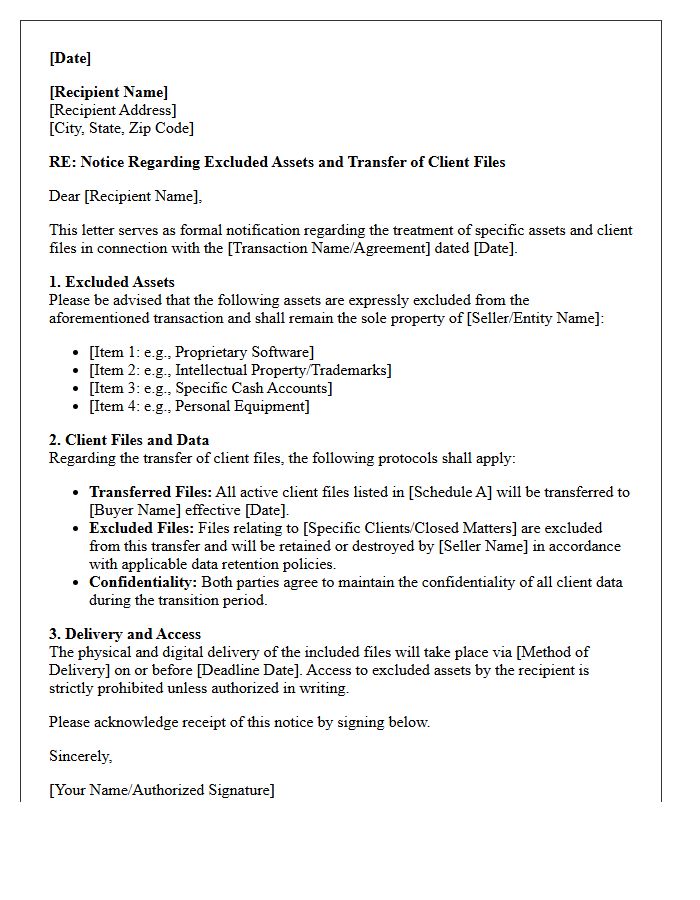

Excluded Assets and Client Files

When handling business divestitures, Excluded Assets refers to specific properties, contracts, or liabilities that remain with the seller rather than transferring to the buyer. A critical component involves Client Files, which may be withheld due to regulatory compliance, legal privilege, or data privacy laws. Parties must clearly define these exceptions in the purchase agreement to avoid operational disputes. Properly identifying excluded items ensures that proprietary intellectual property and sensitive historical records are protected while maintaining the integrity of the transaction structure during the ownership transition.

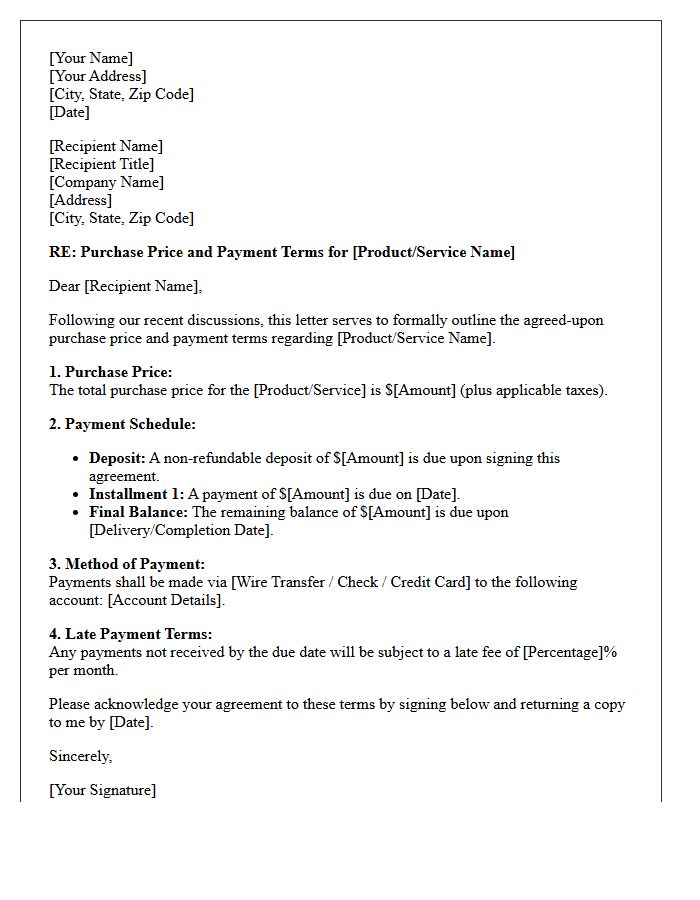

Purchase Price and Payment Terms

The Purchase Price is the total amount agreed upon for an asset, while Payment Terms define the schedule and methods of fund transfer. It is essential to clarify the down payment, installment dates, and any accrued interest within the contract. These terms dictate the financial obligations of the buyer and protect the seller's cash flow. Always verify if the price includes taxes or contingencies to avoid unexpected costs. Establishing clear legal language ensures both parties understand the binding commitment and timing for final settlement.

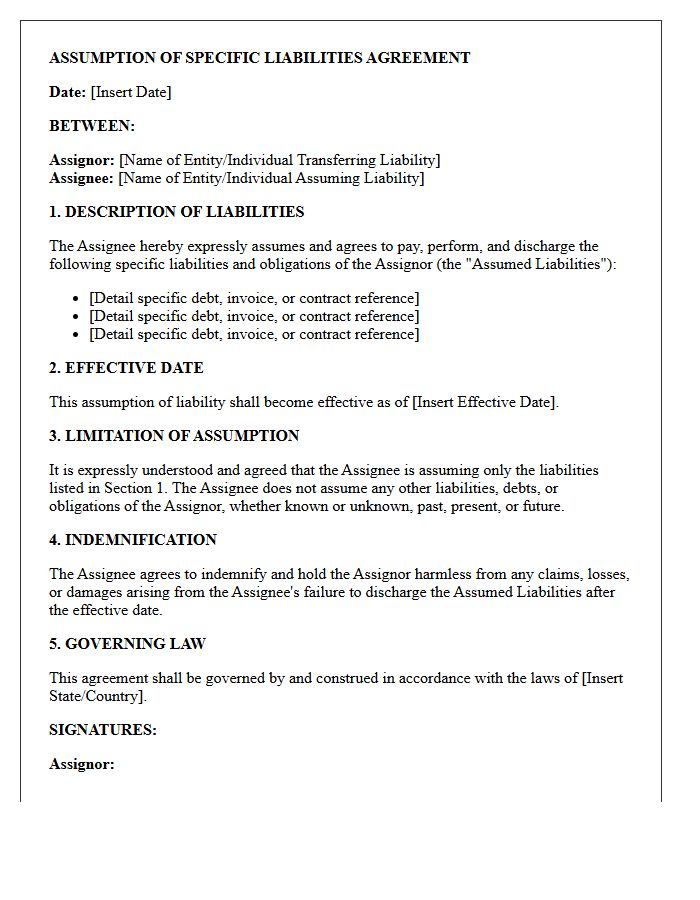

Assumption of Specific Liabilities

An Assumption of Specific Liabilities is a legal agreement where a buyer agrees to take responsibility for defined debts or obligations of a seller. Unlike a general assumption, this process allows the parties to explicitly list which financial burdens transfer and which remain with the original owner. This is a critical component of asset purchase agreements, ensuring clarity on future legal claims. By identifying carve-outs, buyers can mitigate risk and avoid inheriting undisclosed or unintended liabilities, protecting the value of the acquired business assets during the transaction.

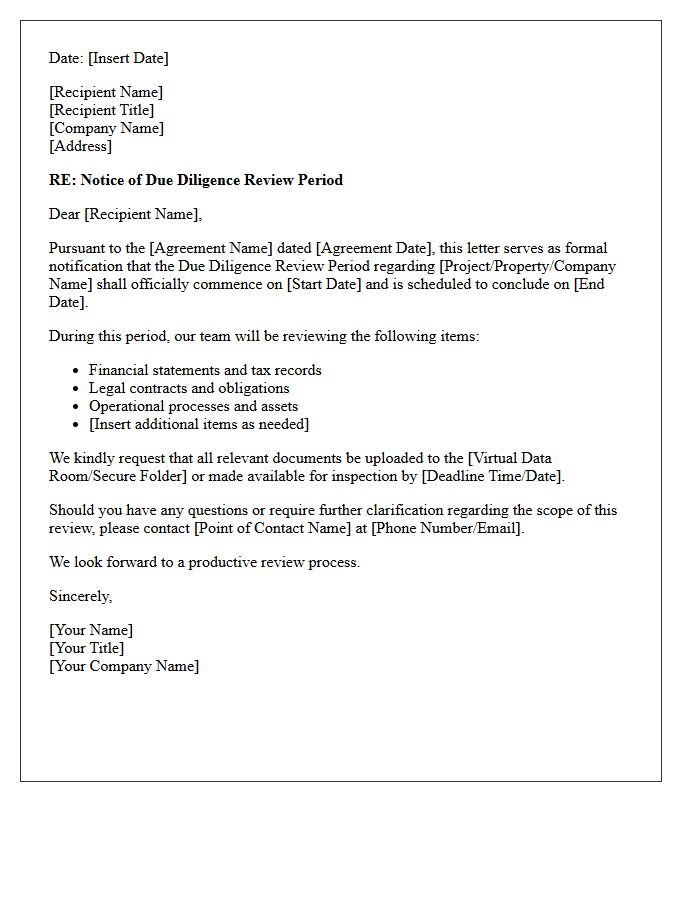

Due Diligence Review Period

A Due Diligence Review Period is a critical timeframe in a transaction allowing a buyer to investigate the asset's legal, financial, and physical condition. During this window, the purchaser verifies all claims made by the seller to mitigate potential risks. It serves as a contingency period, granting the buyer the right to terminate the contract or renegotiate terms if undisclosed liabilities or defects are discovered. Completing this rigorous assessment is essential to ensure the investment is sound before the deal becomes legally binding and non-refundable deposits are committed.

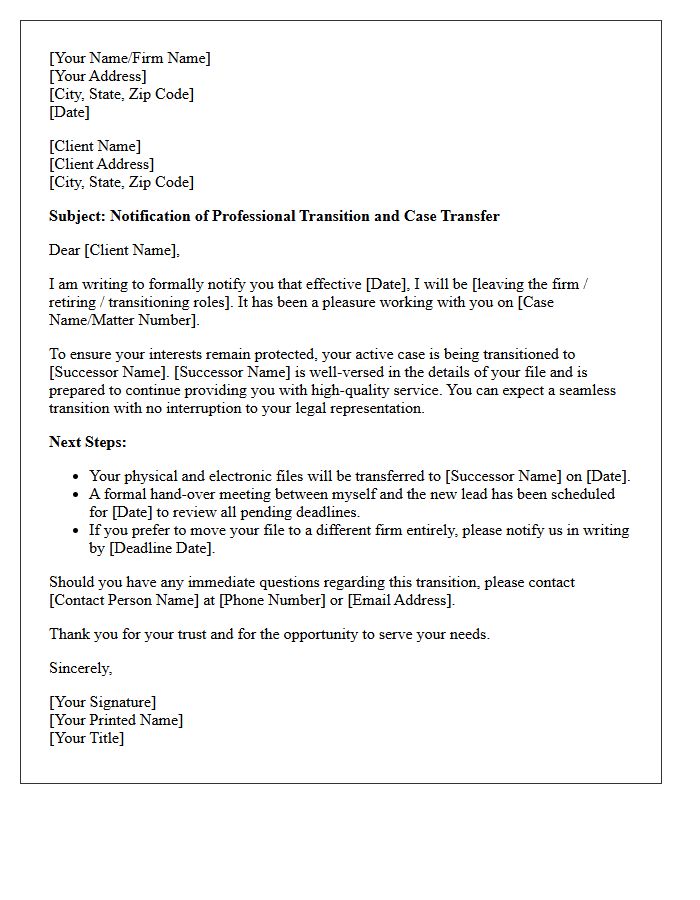

Transition of Clients and Active Cases

The transition of clients and active cases requires a structured handover to maintain continuity of care. Effective management ensures that vital documentation, current status, and upcoming deadlines are accurately transferred between practitioners. This process minimizes service gaps and protects client confidentiality through secure data migration. Clear communication with the client is essential to build trust during the shift. Prioritizing a seamless transition prevents information loss, ensuring that active cases remain on track while upholding professional standards and improving overall project outcomes within the organization.

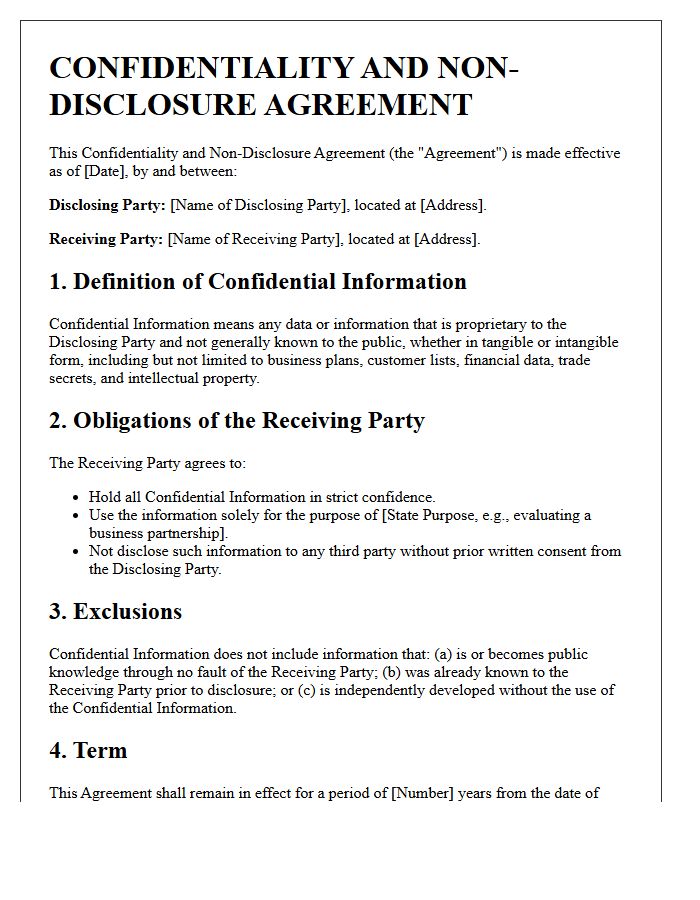

Confidentiality and Non-Disclosure Agreement

A Confidentiality and Non-Disclosure Agreement (NDA) is a legally binding contract used to protect sensitive information from unauthorized exposure. It ensures that parties involved keep proprietary data, trade secrets, and internal business strategies private. By signing this document, recipients agree not to disclose specified materials to third parties, safeguarding a company's intellectual property and competitive advantage. Whether used for partnerships, employment, or investor pitches, the agreement establishes clear legal boundaries and consequences for any confidentiality breach occurring during or after a professional relationship.

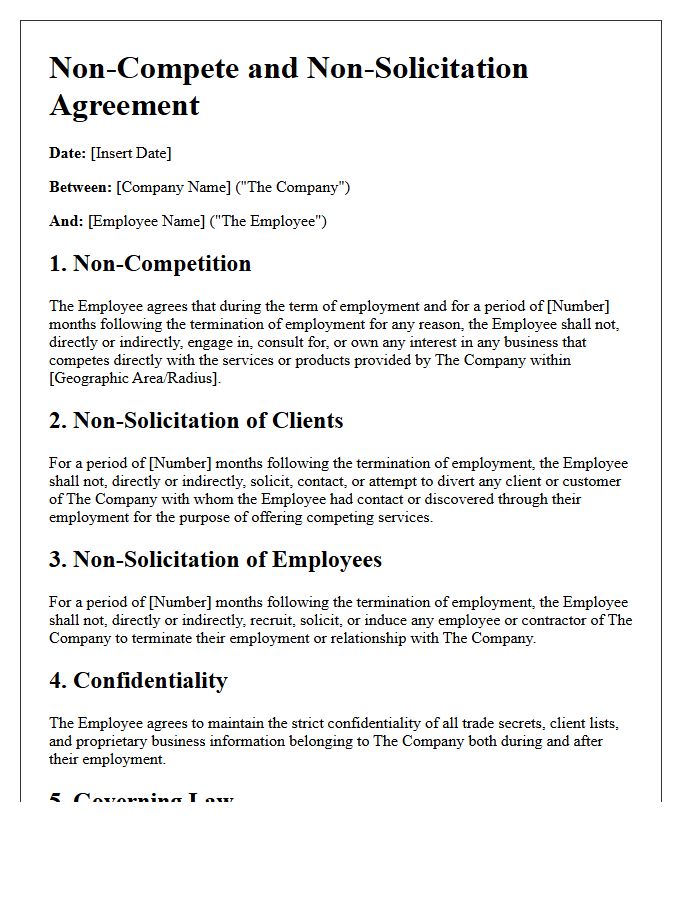

Non-Compete and Non-Solicitation Covenants

Navigating employment agreements requires understanding restrictive covenants. A non-compete clause prohibits an individual from working for direct rivals within a specific geographic area and timeframe. Conversely, a non-solicitation agreement prevents former employees from poaching clients or staff. Courts increasingly scrutinize these terms for reasonableness; overly broad restrictions that impede one's livelihood may be deemed unenforceable. Protecting legitimate business interests and trade secrets is the primary goal, but legal standards vary significantly by jurisdiction, making it essential to review the specific scope and duration of any signed mandate.

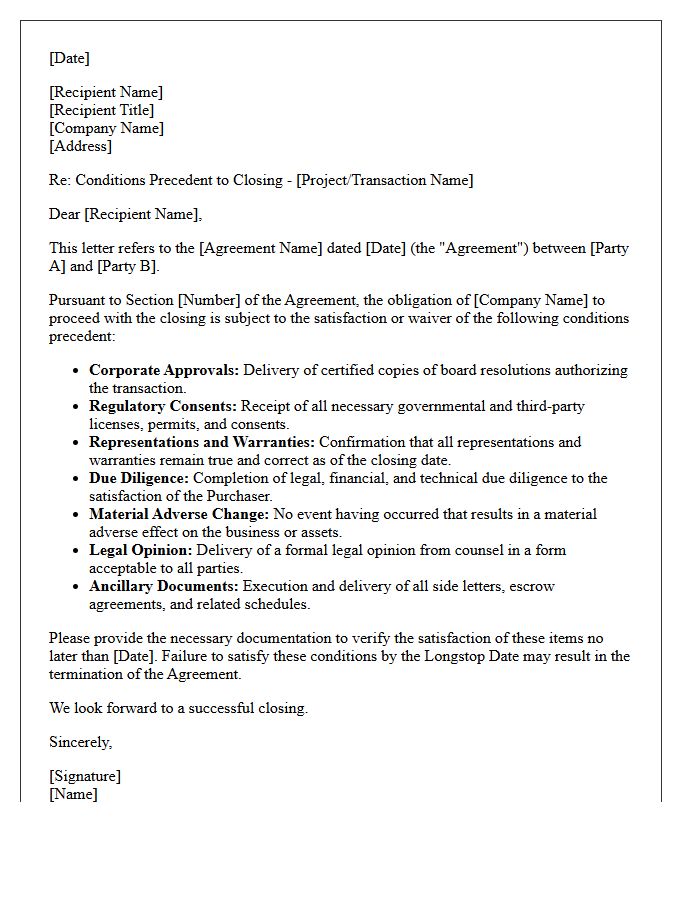

Conditions Precedent to Closing

Conditions Precedent are specific requirements that must be satisfied or waived before a transaction can legally conclude. These contingencies typically include securing financing, obtaining regulatory approvals, and verifying the accuracy of representations. If these legal benchmarks are not met, a party may have the right to terminate the agreement without penalty. Understanding these obligations is vital to ensuring a successful closing, as they act as a safeguard to confirm all contractual terms and operational prerequisites are fulfilled before the final transfer of ownership or funds occurs.

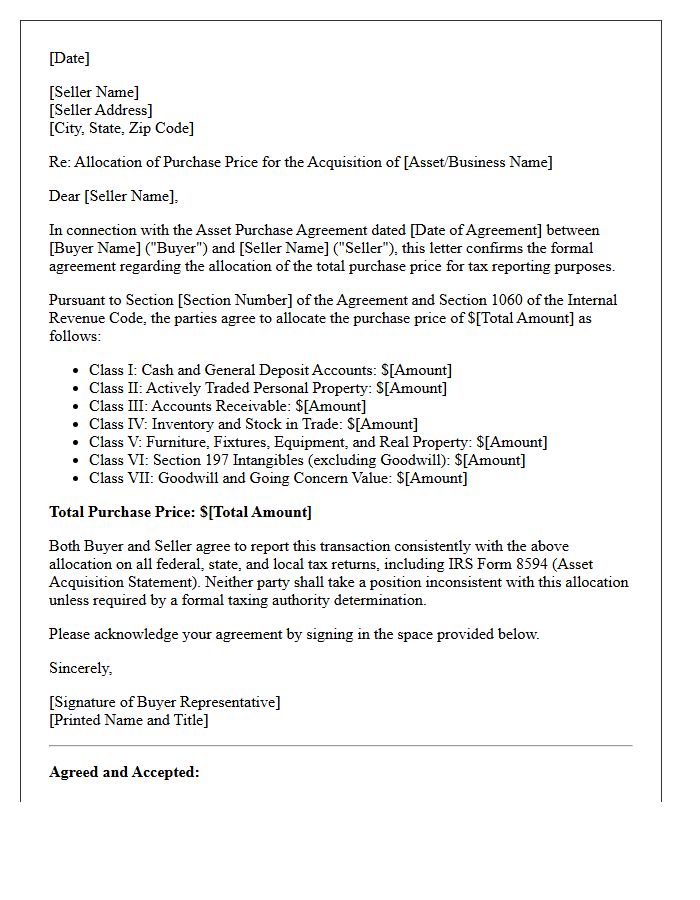

Allocation of Purchase Price

The Allocation of Purchase Price is a critical accounting process used during a business acquisition to assign the total cost to specific identifiable assets and liabilities. Both buyers and sellers must report these values to tax authorities using IRS Form 8594. This process directly impacts future tax liabilities, depreciation schedules, and the calculation of goodwill. Proper allocation ensures compliance with financial standards and optimizes the after-tax proceeds for the seller while maximizing future deductions for the buyer, making it a vital step in any commercial transaction.

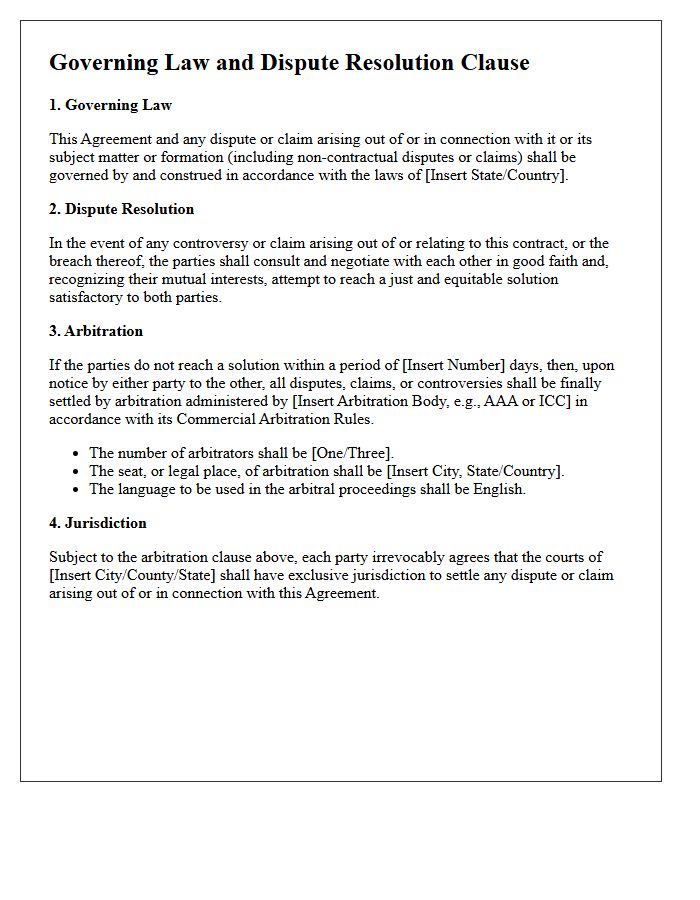

Governing Law and Dispute Resolution

The Governing Law clause determines which jurisdiction's statutes regulate a contract's legal interpretation. Equally vital is the Dispute Resolution section, which outlines how conflicts are settled, whether through traditional litigation, binding arbitration, or mediation. These provisions provide legal certainty, helping parties avoid unpredictable jurisdictional battles and high procedural costs. When drafting agreements, always specify the legal venue to ensure any potential litigation occurs in a favorable or neutral location, maintaining control over the enforcement of contractual obligations and protecting your long-term legal interests effectively.

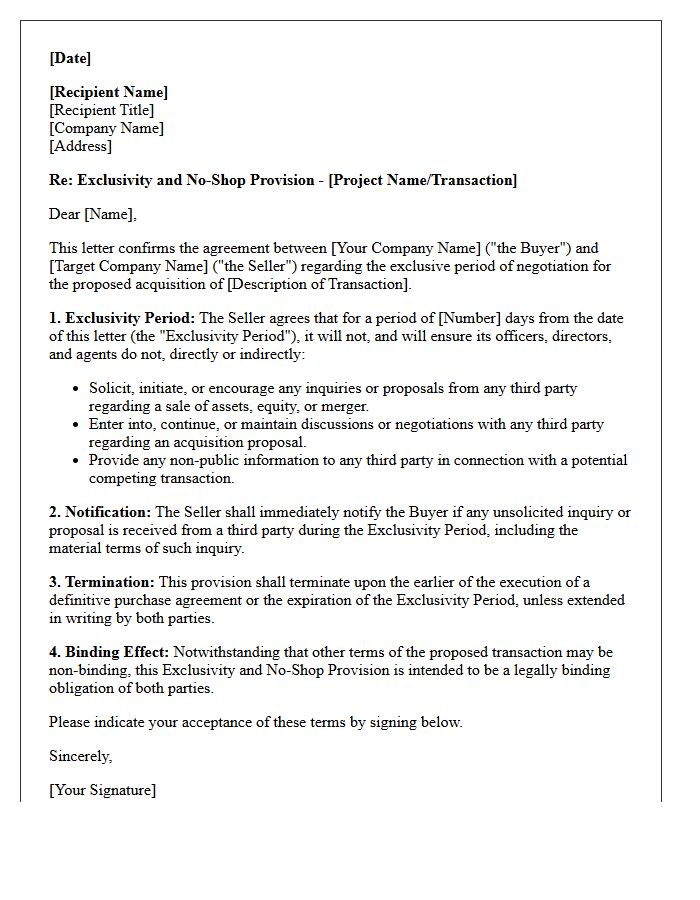

Exclusivity and No-Shop Provision

An exclusivity provision, often called a no-shop clause, restricts a seller from soliciting or negotiating alternative offers from other potential buyers for a specific duration. This legal commitment ensures deal certainty by protecting the buyer's investment in due diligence and legal costs. While it prevents competitive bidding once a letter of intent is signed, it allows both parties to focus exclusively on closing the transaction. Violating these terms can lead to significant legal liability or termination fees, making it a critical component of high-stakes mergers and acquisitions.

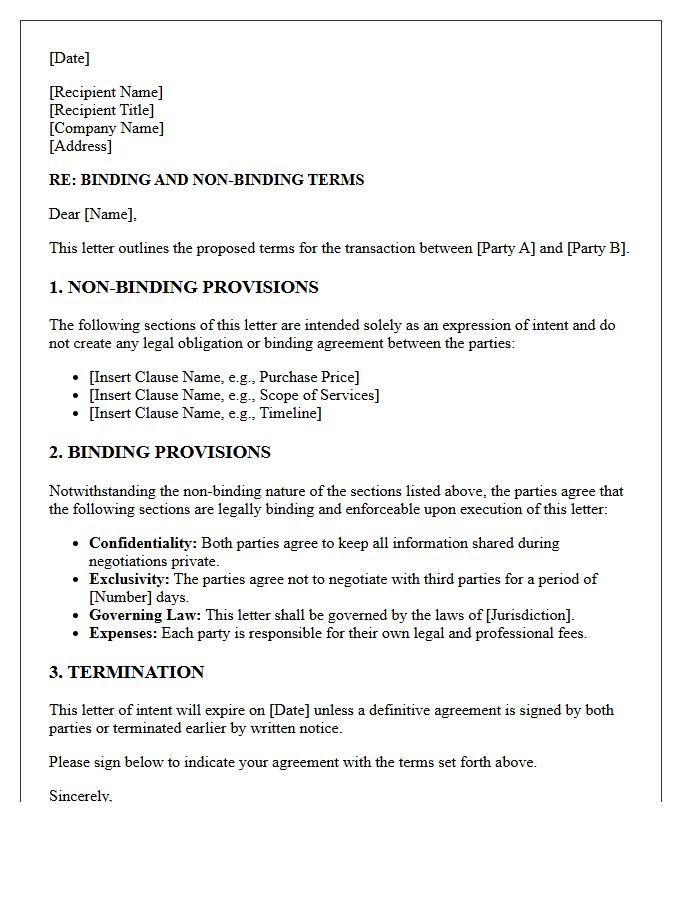

Binding and Non-Binding Terms of This Letter

In legal agreements, distinguishing between binding and non-binding terms is essential. Typically, a letter of intent outlines the proposed framework for a deal without creating a final legal obligation to close. While core commercial terms like price are often non-binding, specific clauses such as confidentiality, exclusivity, and governing law are usually legally enforceable. Parties must use precise language to ensure that preliminary discussions do not inadvertently become a mandatory contract before final due diligence and formal execution are completed.

What is a Letter of Intent for an asset purchase?

A Letter of Intent (LOI) for an asset purchase is a formal document outlining the preliminary agreement between a buyer and a seller. It details the proposed terms, purchase price, and specific assets to be acquired before the final definitive purchase agreement is drafted.

Is a Letter of Intent for an asset purchase legally binding?

Generally, most provisions of an LOI are non-binding, serving as a framework for negotiations. However, certain sections-such as confidentiality, exclusivity (no-shop clauses), and governing law-are typically explicitly stated as legally binding to protect both parties during due diligence.

What should be included in a Letter of Intent for an asset purchase?

A standard LOI should include the identification of specific assets (inventory, equipment, IP), the proposed purchase price and payment structure, the timeline for due diligence, a target closing date, and any contingencies or conditions precedent that must be met before the sale.

What is the difference between an asset purchase and a stock purchase in an LOI?

In an asset purchase LOI, the buyer selects specific assets and liabilities to acquire, allowing for a "step-up" in tax basis. In a stock purchase, the buyer acquires the entire legal entity, including all undisclosed liabilities and historical obligations, which typically involves a different risk profile and tax treatment.

Why is an exclusivity period important in an asset purchase LOI?

The exclusivity or "no-shop" clause prevents the seller from negotiating with other potential buyers for a set period. This protects the buyer's investment of time and resources during the expensive due diligence phase, ensuring they have a fair window to finalize the transaction.

Comments