An Entity Classification Opinion Letter provides formal legal or tax confirmation regarding an entity's tax status under federal regulations. This critical document ensures compliance for complex business structures and clarifies tax treatment for investors or regulatory bodies. Understanding these legal opinions is essential for effective corporate structuring and risk management. Below are some ready to use template.

Image cover: Entity Classification Election: Opinion Letter Guide and Professional Templates

Letter Samples List

- Domestic Limited Liability Company Entity Classification Opinion Letter

- Foreign Corporate Equivalent Entity Classification Opinion Letter

- Disregarded Entity Tax Classification Opinion Letter

- Cross-Border Subsidiary Entity Classification Opinion Letter

- Statutory Partnership Entity Classification Opinion Letter

- Check-the-Box Election Entity Classification Opinion Letter

- Joint Venture Structure Entity Classification Opinion Letter

- Offshore Investment Vehicle Entity Classification Opinion Letter

- Real Estate Investment Trust Entity Classification Opinion Letter

- Dual-Qualified Statutory Entity Classification Opinion Letter

- Nonprofit Tax-Exempt Entity Classification Opinion Letter

- Merger Target Entity Classification Opinion Letter

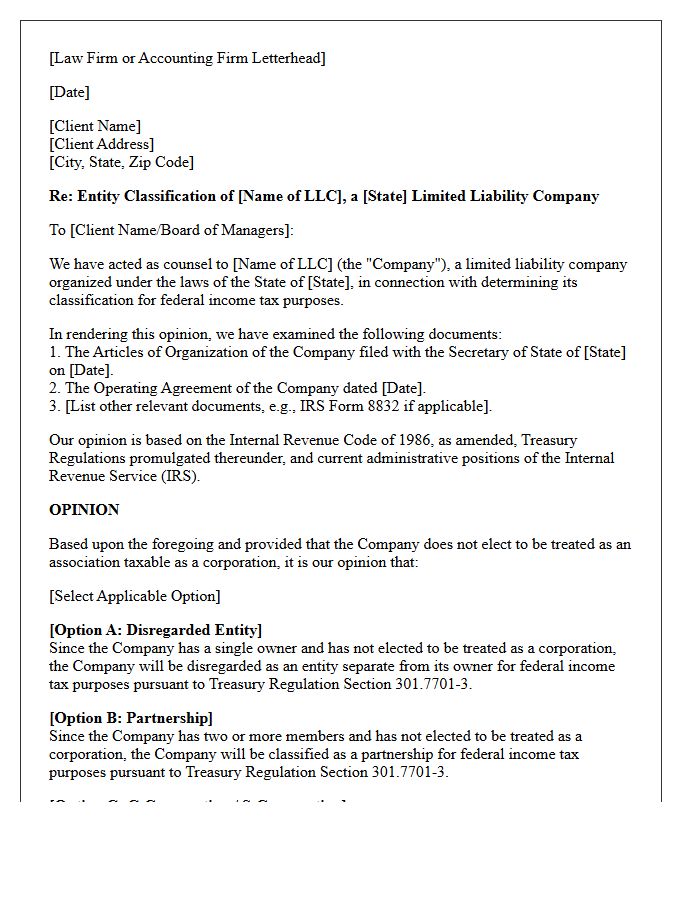

Domestic Limited Liability Company Entity Classification Opinion Letter

A Domestic Limited Liability Company Entity Classification Opinion Letter is a formal legal document verifying an LLC's federal tax status. It confirms whether the entity is classified as a corporation, partnership, or disregarded entity by the IRS. Lenders and title companies often require this professional opinion to mitigate risks during complex financial transactions, ensuring the entity has the legal authority to enter agreements. This letter provides assurance regarding tax liabilities and organizational structure, making it a critical component for regulatory compliance and securing institutional financing or real estate acquisitions.

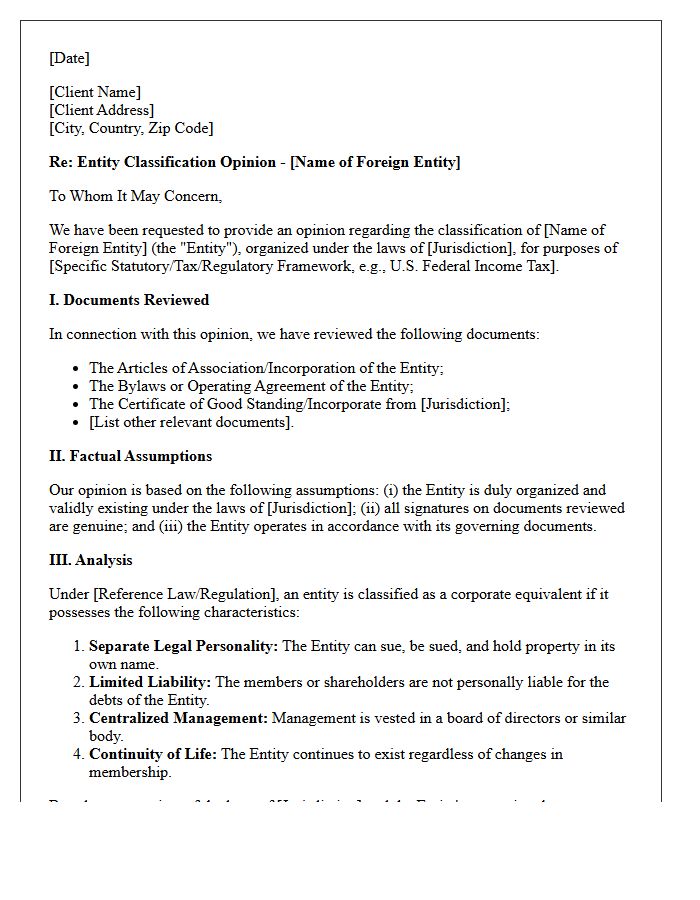

Foreign Corporate Equivalent Entity Classification Opinion Letter

A Foreign Corporate Equivalent Entity Classification Opinion Letter is a vital legal document used to determine how a non-U.S. business is treated for tax purposes. It provides an expert legal analysis to confirm if an overseas entity aligns with U.S. corporate structures, such as an association taxable as a corporation. This classification is essential for regulatory compliance, preventing double taxation, and ensuring accurate IRS reporting. Obtaining this letter mitigates financial risks by validating the entity's status before engaging in complex international transactions or filing federal tax returns.

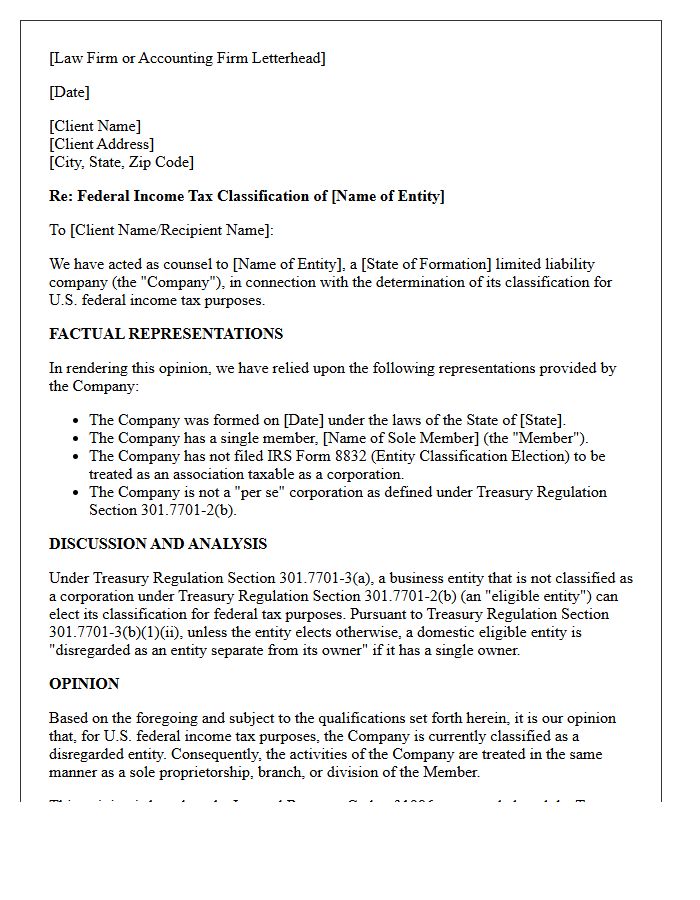

Disregarded Entity Tax Classification Opinion Letter

A Disregarded Entity Tax Classification Opinion Letter provides formal legal or tax verification of an entity's federal standing. It confirms that for IRS purposes, the business is tax-transparent, meaning its income and liabilities flow directly to the single owner's return. This document is essential for due diligence in real estate transactions, financing, and 1031 exchanges to ensure compliance. It serves as professional assurance that the entity is not taxed separately, simplifying the legal structure while maintaining limited liability protections for the beneficial owner.

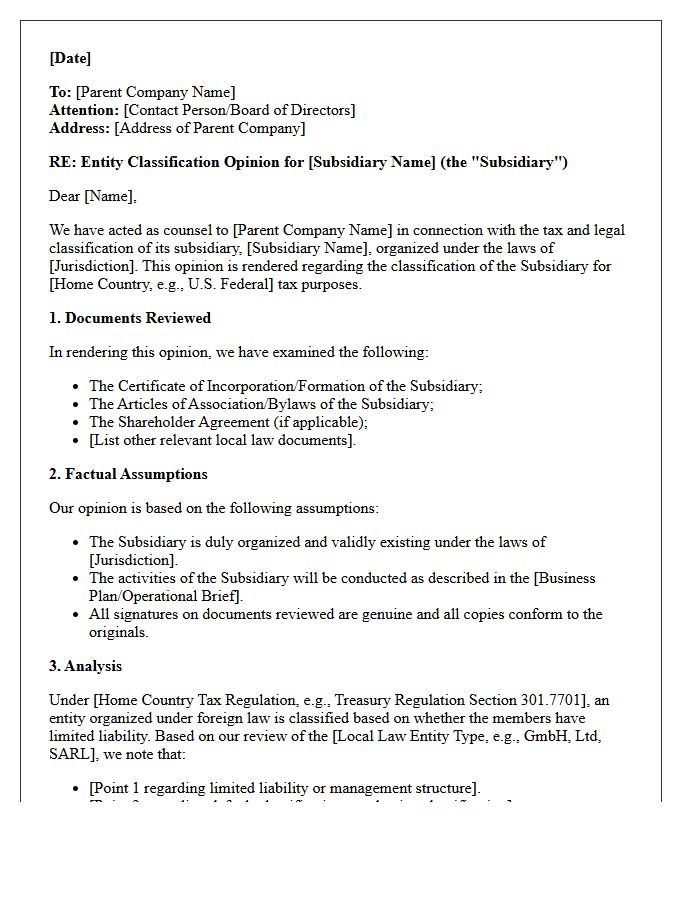

Cross-Border Subsidiary Entity Classification Opinion Letter

A Cross-Border Subsidiary Entity Classification Opinion Letter is a vital legal document used to confirm the tax status of a foreign business unit. It provides a formal legal analysis to ensure the subsidiary is correctly categorized as a corporation, partnership, or disregarded entity under domestic laws like the US IRC Check-the-Box rules. This letter is essential for regulatory compliance, mitigating audit risks, and optimizing international tax planning. It offers lenders and stakeholders assurance regarding the entity's structural legitimacy and liability frameworks across multiple jurisdictions.

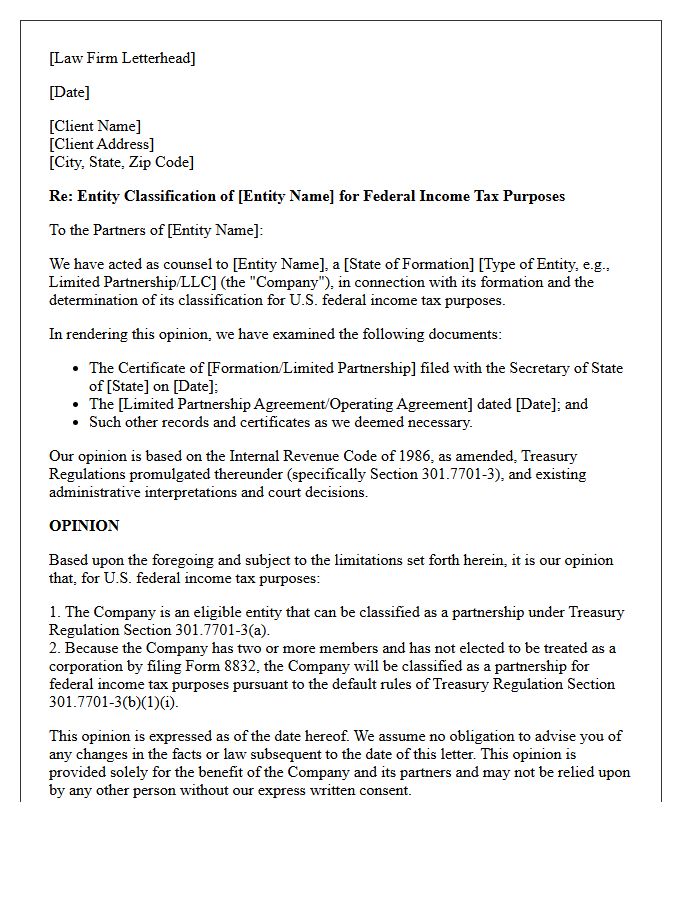

Statutory Partnership Entity Classification Opinion Letter

A Statutory Partnership Entity Classification Opinion Letter is a critical legal document providing tax certainty regarding a business's structure. It formally confirms that a statutory partnership meets specific IRS criteria to be treated as a pass-through entity rather than a corporation. This prevents double taxation and ensures tax obligations flow directly to partners. Investors and lenders often require this letter during due diligence to mitigate risks associated with potential reclassification by tax authorities. Obtaining this legal opinion protects the entity's financial integrity and validates its operational framework under prevailing tax laws.

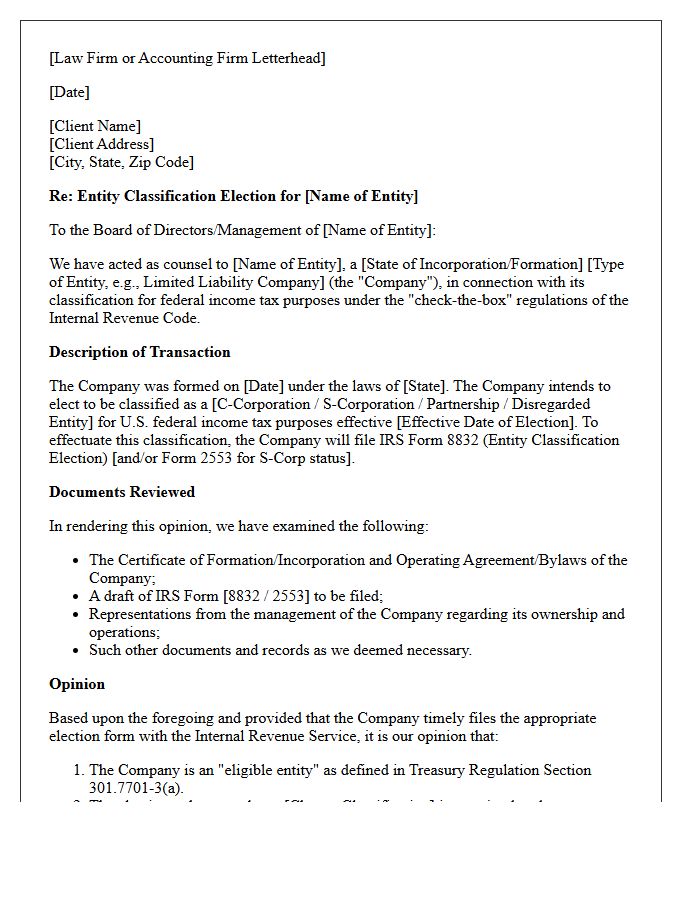

Check-the-Box Election Entity Classification Opinion Letter

A Check-the-Box Election Entity Classification Opinion Letter provides a formal legal tax opinion regarding a business entity's federal tax status. This document validates the IRS Form 8832 filing, confirming whether an entity is classified as a corporation, partnership, or disregarded entity. It is crucial for regulatory compliance and cross-border transactions, ensuring that investors and lenders have written assurance of the entity's tax treatment. This letter mitigates tax liability risks by documenting the legal basis for the chosen classification under Treasury Regulations, providing essential protection during audits or complex restructuring.

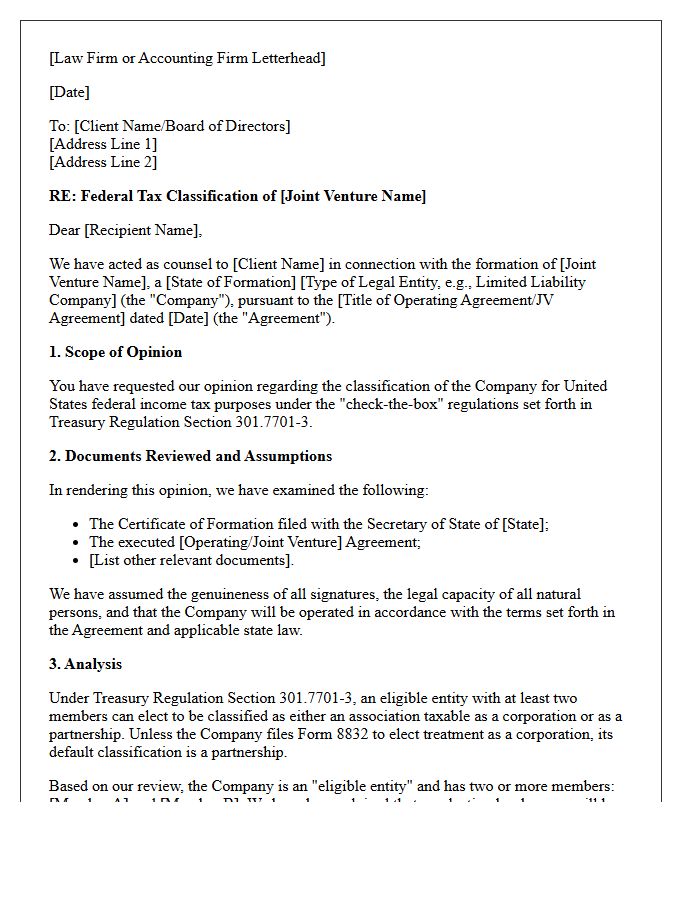

Joint Venture Structure Entity Classification Opinion Letter

A Joint Venture Structure Entity Classification Opinion Letter is a vital legal document used to confirm the tax status of a partnership or corporate entity. It provides a formal legal opinion on whether a venture will be treated as a pass-through entity or a corporation by tax authorities. This letter is crucial for mitigating liability and ensuring regulatory compliance during complex transactions. By establishing clear entity classification, partners can secure financing, optimize tax benefits, and provide essential legal certainty for investors and stakeholders involved in the collaborative business arrangement.

Offshore Investment Vehicle Entity Classification Opinion Letter

An Offshore Investment Vehicle Entity Classification Opinion Letter is a vital legal document confirming a fund's tax status under FATCA and CRS regulations. It provides a formal legal opinion regarding whether an entity is classified as a Financial Institution or a Passive NFFE. This letter ensures regulatory compliance, assists with global reporting obligations, and mitigates withholding tax risks. Investors and banks rely on this classification to confirm that the offshore structure meets international transparency standards and internal due diligence requirements, preventing costly administrative penalties and ensuring smooth cross-border financial operations.

Real Estate Investment Trust Entity Classification Opinion Letter

A Real Estate Investment Trust (REIT) Entity Classification Opinion Letter is a vital legal document confirming that a business satisfies specific IRS tax requirements. This letter serves as formal legal assurance that the entity qualifies for pass-through taxation, effectively avoiding double taxation on corporate profits. It provides investor confidence by verifying that the structure complies with complex federal tax codes. Obtaining this professional opinion is essential during capital raises or property acquisitions to guarantee the trust's REIT status remains legally defensible and operationally sound under current regulatory standards.

Dual-Qualified Statutory Entity Classification Opinion Letter

A Dual-Qualified Statutory Entity Classification Opinion Letter provides a critical legal analysis for businesses organized under two jurisdictions. This document verifies the entity's legal status and tax classification, ensuring compliance with both local and foreign regulations. It is essential for complex corporate structures to mitigate jurisdictional risks and validate organizational standing during international transactions or financing. By clarifying the interplay between different legal systems, the letter offers necessary legal certainty for stakeholders and regulatory bodies regarding the entity's governing framework and operational legitimacy.

Nonprofit Tax-Exempt Entity Classification Opinion Letter

A Nonprofit Tax-Exempt Entity Classification Opinion Letter is a formal legal document issued by qualified counsel to verify an organization's regulatory status. It provides legal assurance to donors, lenders, or government agencies that the entity meets specific IRS requirements under section 501(c). This letter is crucial for securing grant funding and validating tax-deductible contributions. By confirming operational compliance and tax-exempt eligibility, it mitigates financial risk and ensures transparency during complex transactions or audits, establishing a definitive record of the nonprofit's standing within the internal revenue code.

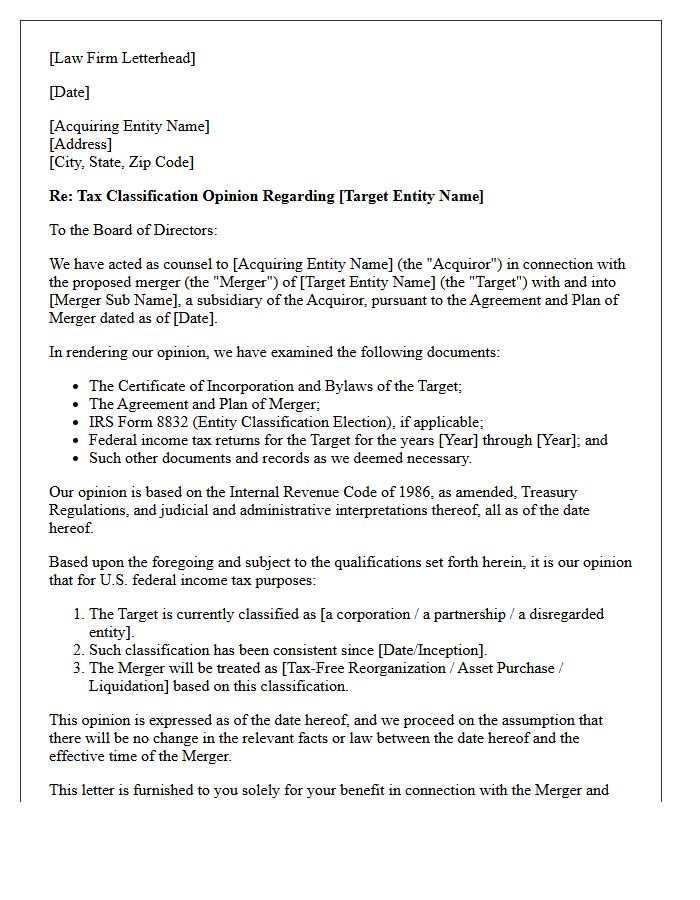

Merger Target Entity Classification Opinion Letter

A Merger Target Entity Classification Opinion Letter is a critical legal document used in corporate acquisitions to confirm a company's federal tax status. It provides formal assurance that the target entity is correctly classified as a corporation or partnership under IRS Treasury Regulations. This verification is essential for structural planning, ensuring the merger qualifies for intended tax-deferred treatment. By identifying potential entity classification errors early, parties mitigate significant risks related to successor liability and unforeseen corporate-level taxes, ultimately protecting the financial integrity of the transaction.

What is an Entity Classification Opinion Letter?

An Entity Classification Opinion Letter is a formal legal or tax document issued by a qualified professional that provides a definitive analysis and conclusion on how a specific business entity (such as an LLC, LP, or foreign corporation) is classified for federal tax purposes under the IRS "check-the-box" regulations.

Why do lenders require an Entity Classification Opinion Letter for commercial loans?

Lenders require this opinion to mitigate risk by confirming the borrower's tax status and legal structure. This ensures the entity is properly authorized to enter into the loan agreement and that there are no hidden tax liabilities or structural ambiguities that could jeopardize the collateral or repayment.

How does the IRS "check-the-box" regulation affect entity classification?

The "check-the-box" regulations (Treasury Regulation Section 301.7701-3) allow eligible business entities to choose their classification as either a corporation, partnership, or disregarded entity for tax purposes. An opinion letter verifies that the entity has filed the correct elections, such as Form 8832, to maintain its intended status.

What key components are included in a formal Entity Classification Opinion?

A standard opinion letter includes a detailed review of the entity's organizational documents, a factual summary of its operations, a legal analysis of relevant Internal Revenue Code sections, and a formal conclusion stating whether the entity is treated as a disregarded entity, partnership, or association taxable as a corporation.

Can an Entity Classification Opinion Letter be used for foreign entities?

Yes, it is frequently used for foreign entities operating in the U.S. to determine if they are classified as "per se" corporations or if they are eligible to elect their classification. This is critical for international tax compliance and determining withholding requirements under FATCA or treaty protocols.

Comments