A Notice of Closing Cost Adjustment Letter is a formal document sent to borrowers to communicate changes in final settlement fees before a real estate transaction concludes. This letter ensures financial transparency and legal compliance by detailing any increases or credits applied to the initial estimate. To help you draft a professional notification, below are some ready to use templates.

Image cover: Official Notice of Closing Cost Adjustments: Professional Letter Templates and Samples

Letter Samples List

- Notice of Closing Cost Adjustment Letter

- Revised Closing Cost Disclosure Letter

- Final Closing Cost Reconciliation Letter

- Seller Closing Cost Concession Adjustment Letter

- Buyer Escrow Shortfall Adjustment Letter

- Lender Required Closing Cost Adjustment Letter

- Prorated Property Tax Adjustment Letter

- Title Insurance Premium Adjustment Letter

- Appraisal Fee Adjustment Notification Letter

- Brokerage Commission Adjustment Letter

- Homeowners Association Fee Adjustment Letter

- Third-Party Vendor Cost Adjustment Letter

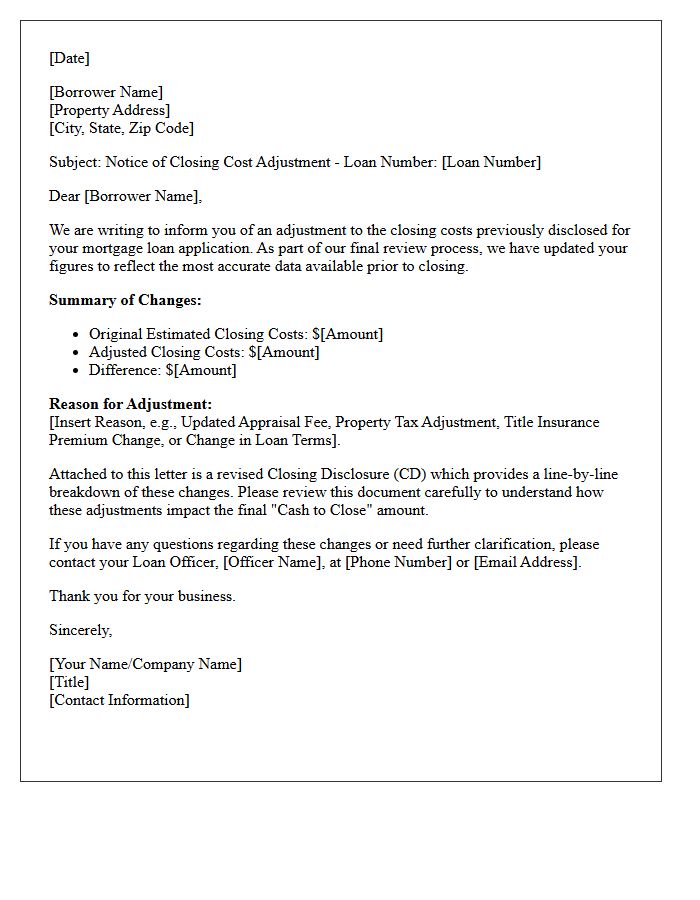

Notice of Closing Cost Adjustment Letter

A Notice of Closing Cost Adjustment is a critical document issued when there are material changes to your final settlement charges. This letter notifies borrowers that their Loan Estimate has been updated due to specific circumstances, such as appraised value shifts or credit score fluctuations. It ensures transparency under federal regulations by detailing why specific fees increased. Reviewing this notice immediately is essential because significant adjustments may trigger a mandatory three-day waiting period, potentially delaying your scheduled property closing date to ensure full financial disclosure and compliance.

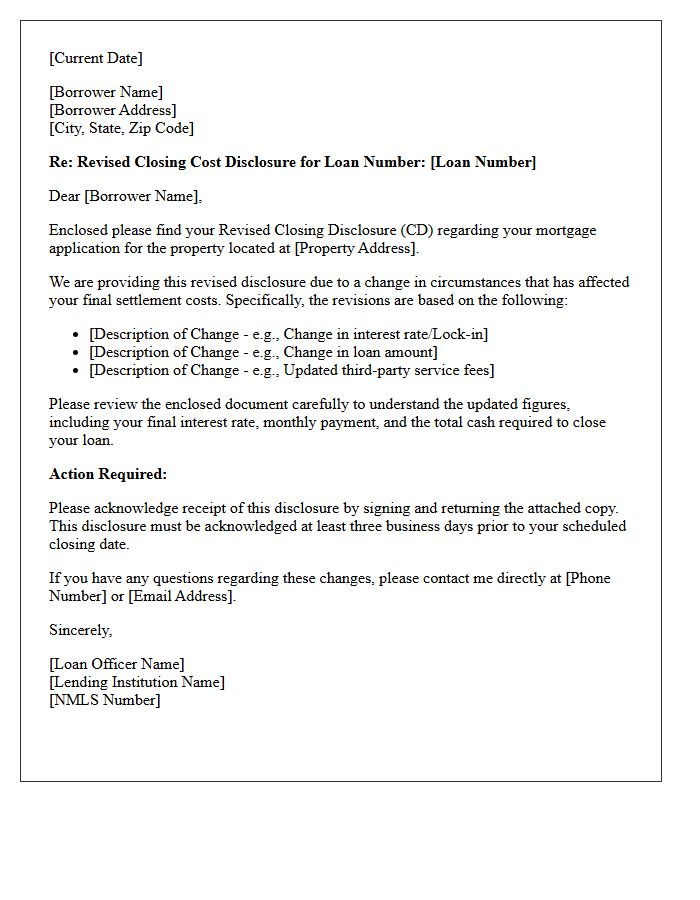

Revised Closing Cost Disclosure Letter

A Revised Closing Cost Disclosure Letter is a critical document issued when changed circumstances significantly alter your initial loan estimate. It ensures transparency by highlighting updates to origination fees, interest rates, or third-party charges. Borrowers must receive this at least three business days before consummation to review final figures. Understanding these modifications is essential to prevent unexpected financial burdens at the closing table, as it serves as the final legal verification of your total borrowing costs and monthly payment obligations before you sign the mortgage agreement.

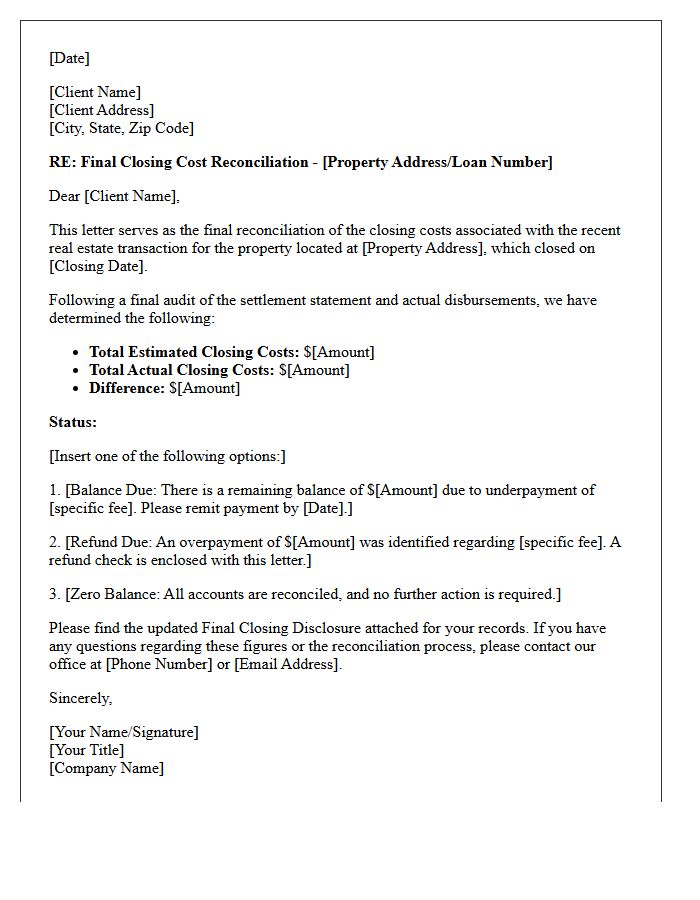

Final Closing Cost Reconciliation Letter

The Final Closing Cost Reconciliation Letter is a vital document issued after a real estate transaction to ensure financial accuracy. It compares the initial Closing Disclosure estimates with the actual final payments made. This process identifies potential overpayments or escrow discrepancies, often resulting in a refund check for the buyer. Reviewing this letter is essential to verify that all lender fees, taxes, and insurance premiums were calculated correctly. It serves as the definitive record of your final settlement costs, providing transparency and closing any outstanding balance gaps from the transition.

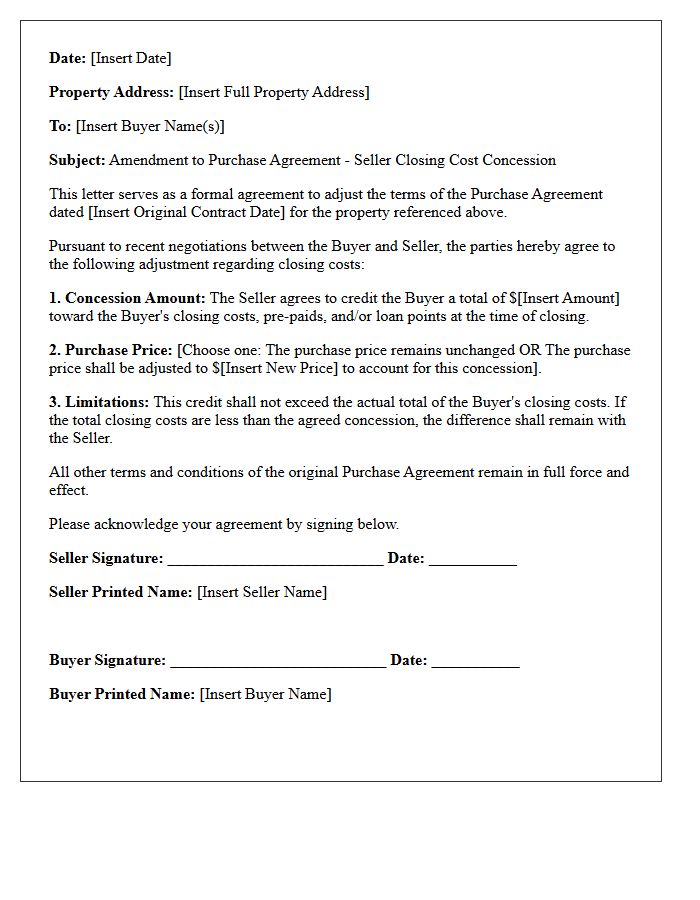

Seller Closing Cost Concession Adjustment Letter

A Seller Closing Cost Concession Adjustment Letter is a formal document used to modify the amount a seller contributes toward a buyer's settlement charges. This addendum is essential when appraisal values or repair negotiations change the final sale terms. It ensures the mortgage lender receives accurate figures to update the Closing Disclosure. Properly documenting these adjustments prevents funding delays and maintains legal compliance during the real estate escrow process. Both parties must sign this letter to validate the updated financial obligations before the final transfer of property title occurs.

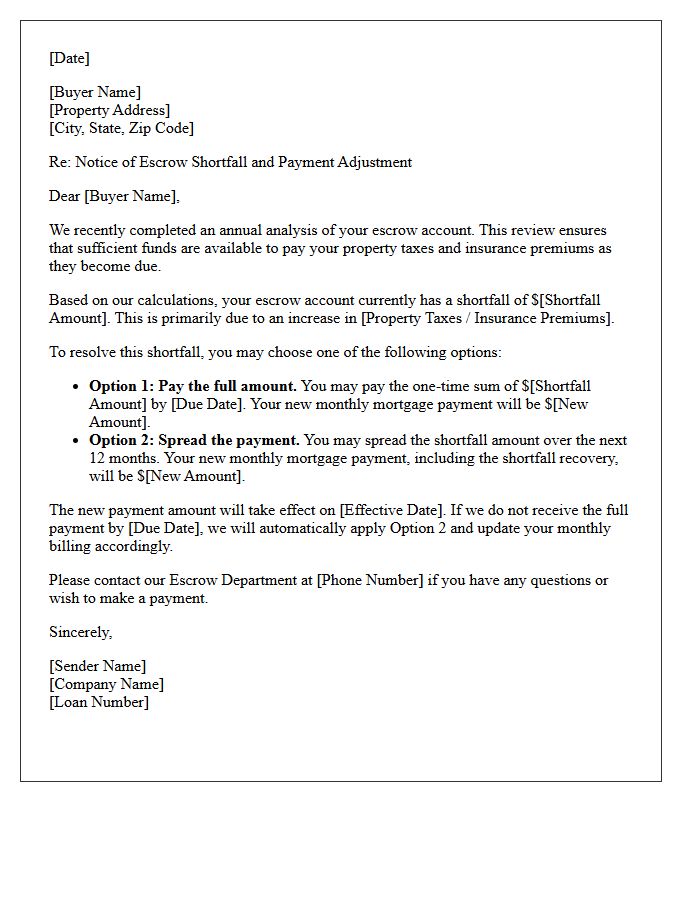

Buyer Escrow Shortfall Adjustment Letter

A Buyer Escrow Shortfall Adjustment Letter notifies a homeowner that their escrow account has insufficient funds to cover rising property taxes or insurance premiums. This formal notice details a required payment increase to rectify the deficit and ensure future obligations are met. Homeowners typically choose between a one-time lump sum payment or spreading the shortage across monthly mortgage installments. Addressing this adjustment promptly is essential to maintain a balanced account and avoid potential lapses in coverage or legal complications regarding your home loan agreement.

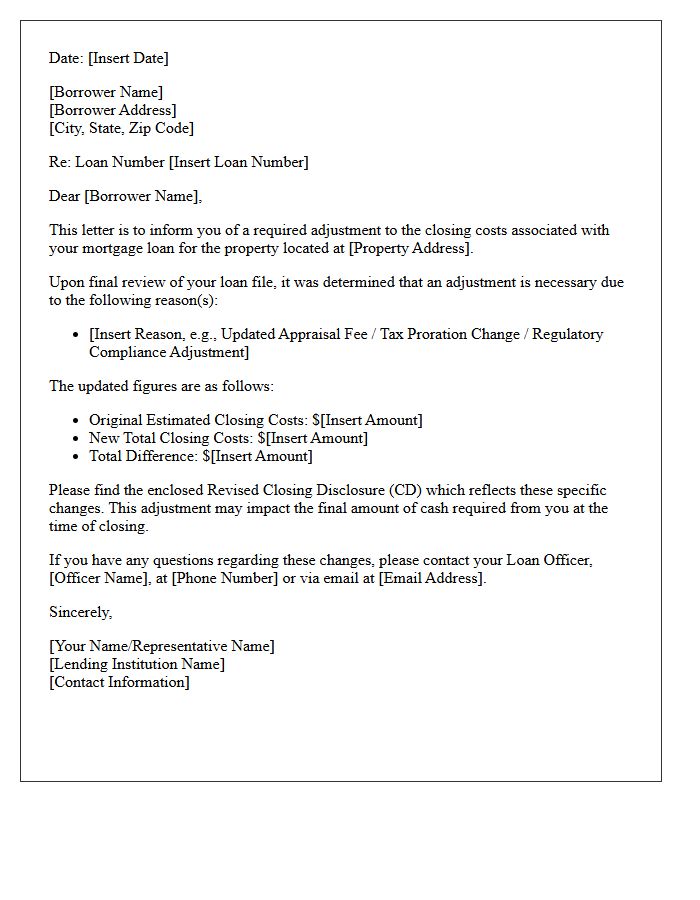

Lender Required Closing Cost Adjustment Letter

A Lender Required Closing Cost Adjustment Letter is a formal document issued when final loan fees deviate from the initial Loan Estimate. It serves as a compliance tool to ensure the lender adheres to legal tolerance limits. This letter notifies the borrower of specific credits or adjustments applied to offset unexpected fee increases. By signing this document, you acknowledge the corrected financial terms, ensuring that the closing process remains transparent and aligns with federal consumer protection regulations regarding mortgage transparency and cost accuracy.

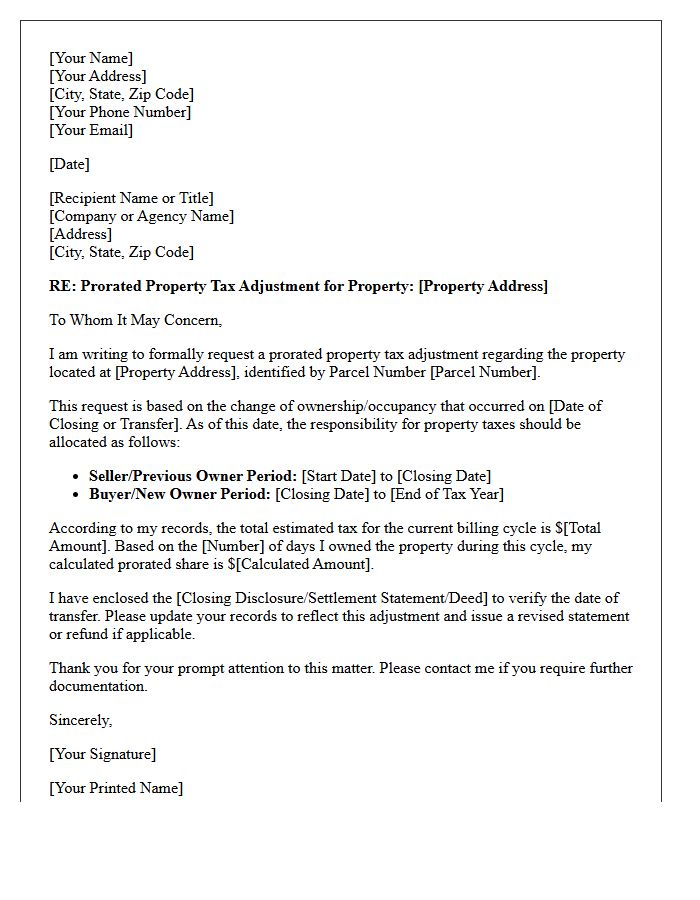

Prorated Property Tax Adjustment Letter

A Prorated Property Tax Adjustment Letter is a formal document used during real estate closings to reconcile tax obligations between buyers and sellers. Since property taxes are often paid in advance or arrears, this letter calculates the exact daily rate to ensure each party pays only for their period of ownership. It protects you from overpaying and serves as vital closing documentation for future tax audits. Reviewing this adjustment ensures that the final settlement statement accurately reflects credits or debits based on the specific closing date and local fiscal cycles.

Title Insurance Premium Adjustment Letter

A Title Insurance Premium Adjustment Letter is a formal document issued when the final loan amount or property value differs from the initial estimate. It ensures the underwriter receives the correct payment based on actual risk exposure. This adjustment may result in a refund to the borrower or a request for additional funds to finalize the policy. Accuracy is vital for legal compliance and protecting ownership rights. Always review this letter to confirm that your closing costs align with the final terms of your real estate transaction.

Appraisal Fee Adjustment Notification Letter

An Appraisal Fee Adjustment Notification Letter informs borrowers that the final cost of a property valuation has changed. This formal document is essential for transparency and compliance with lending regulations. It details why the initial estimate increased, often due to property complexity or market demand. Lenders must issue this disclosure promptly to ensure the borrower understands the updated closing costs. Reviewing this notice carefully is vital, as it directly impacts the total loan expenses required to finalize a real estate transaction.

Brokerage Commission Adjustment Letter

A Brokerage Commission Adjustment Letter is a formal document used to notify clients about changes in transaction fees or service charges. This notice ensures transparency and maintains regulatory compliance within financial agreements. It typically outlines the new fee structure, the effective date, and the specific reasons for the modification, such as market shifts or service upgrades. Clients should review these adjustments carefully, as they directly impact investment returns and overall portfolio costs. Timely communication helps preserve the professional relationship between the broker and the investor.

Homeowners Association Fee Adjustment Letter

A Homeowners Association Fee Adjustment Letter is a formal notice informing residents of changes to their monthly assessments. This document must clearly state the new fee amount, the effective date, and the specific reasons for the increase, such as rising utility costs or reserve fund requirements. To ensure legal compliance, the board should reference the community's governing documents. Providing a detailed budget summary helps maintain transparency, allowing homeowners to understand how their contributions support property maintenance, long-term repairs, and the overall stability of the neighborhood infrastructure.

Third-Party Vendor Cost Adjustment Letter

A Third-Party Vendor Cost Adjustment Letter is a formal notification sent to clients regarding an upcoming price increase for products or services. This document outlines the specific rationale behind the change, such as rising inflation, labor costs, or supply chain disruptions. To maintain professional relationships, the letter should specify the effective date and any modified contract terms. Clear communication helps manage client expectations and ensures transparency during budgetary transitions. Providing a point of contact for further negotiation or clarification is essential for successful vendor management and long-term partnership retention.

What is a Notice of Closing Cost Adjustment?

A Notice of Closing Cost Adjustment is a formal communication sent to a homebuyer when there is a change in the estimated settlement charges previously disclosed on the Loan Estimate. It outlines specific increases or decreases in fees associated with finalizing the mortgage loan.

Why did my closing costs change after the initial Loan Estimate?

Closing costs may change due to "changed circumstances," such as an updated property appraisal, changes in the borrower's credit score, a different interest rate lock, or adjustments to third-party service fees like title insurance and government recording taxes.

Does a closing cost adjustment affect my mortgage interest rate?

Not necessarily. While a closing cost adjustment focuses on the administrative and legal fees of the transaction, your interest rate only changes if the adjustment is related to a rate lock extension, the purchase of additional discount points, or a shift in the loan program.

What are "allowable increases" in a closing cost adjustment letter?

Under federal TRID regulations, some fees have a 10% tolerance limit for increases, while others (like prepaid interest or homeowner's insurance) can change without limit. The adjustment letter will specify which charges have exceeded original estimates and if the lender is required to provide a credit to cover the difference.

How soon before settlement must I receive a closing cost adjustment notice?

Lenders are generally required to provide a revised disclosure within three business days of receiving information that established a changed circumstance. Additionally, you must receive the final Closing Disclosure at least three business days before the scheduled closing date to review all final adjustments.

Comments