Lower interest rates provide a timely mortgage refinancing opportunity to reduce monthly payments and build home equity faster. This guide explores how to craft effective communication to help homeowners capitalize on current market trends and secure better loan terms. Whether you are a lender or an advisor, below are some ready to use template.

Image cover: Save More Monthly: Professional Mortgage Refinance Offer Templates and Letter Samples

Letter Samples List

- Lower Interest Rate Mortgage Refinancing Opportunity Letter

- Cash-Out Home Equity Refinancing Opportunity Letter

- Debt Consolidation Mortgage Refinancing Proposal Letter

- Adjustable to Fixed Rate Mortgage Refinancing Letter

- Loan Term Reduction Mortgage Refinancing Opportunity Letter

- Private Mortgage Insurance Removal Refinancing Letter

- Home Improvement Cash-Out Refinancing Opportunity Letter

- Investment Property Purchase Mortgage Refinancing Letter

- Streamline Federal Housing Administration Refinancing Letter

- Veterans Affairs Streamline Mortgage Refinancing Letter

- Rising Home Value Mortgage Refinancing Opportunity Letter

- Annual Financial Review and Mortgage Refinancing Letter

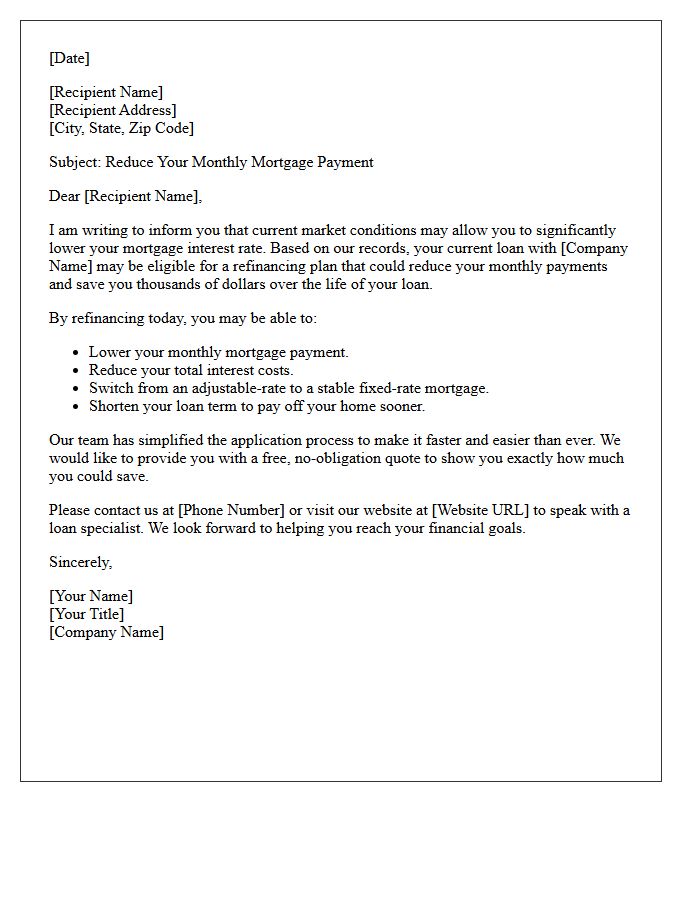

Lower Interest Rate Mortgage Refinancing Opportunity Letter

A Lower Interest Rate Mortgage Refinancing Opportunity Letter is a formal notification from a lender indicating you may qualify for a reduced APR. This document typically highlights potential savings on monthly payments and long-term interest costs. It is essential to verify the sender's credibility to avoid predatory lending. Always compare the closing costs and new loan terms against your current mortgage to ensure the financial benefit outweighs the fees. Reviewing your credit score before responding can help you secure the most competitive market rates available.

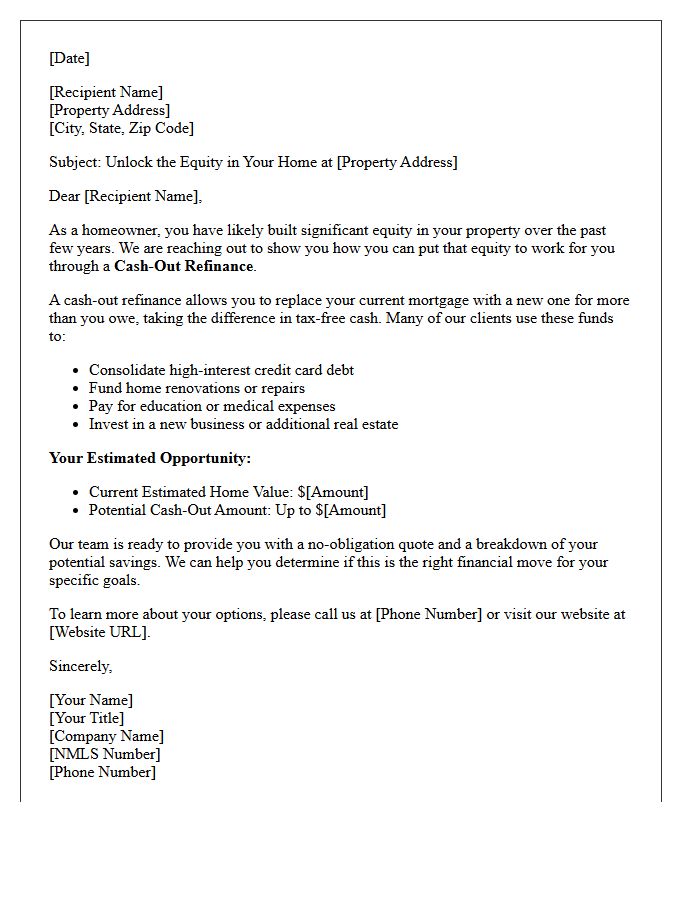

Cash-Out Home Equity Refinancing Opportunity Letter

A Cash-Out Home Equity Refinancing opportunity letter informs homeowners they may qualify to replace their current mortgage with a larger loan. This allows you to receive the difference in liquid cash for debt consolidation, home improvements, or emergency expenses. These offers typically highlight current interest rates and your estimated available equity. Before proceeding, evaluate the new loan terms, closing costs, and how the adjusted balance impacts your long-term financial stability. It is an invitation to leverage your property's value to improve your immediate cash flow while restructuring your primary debt.

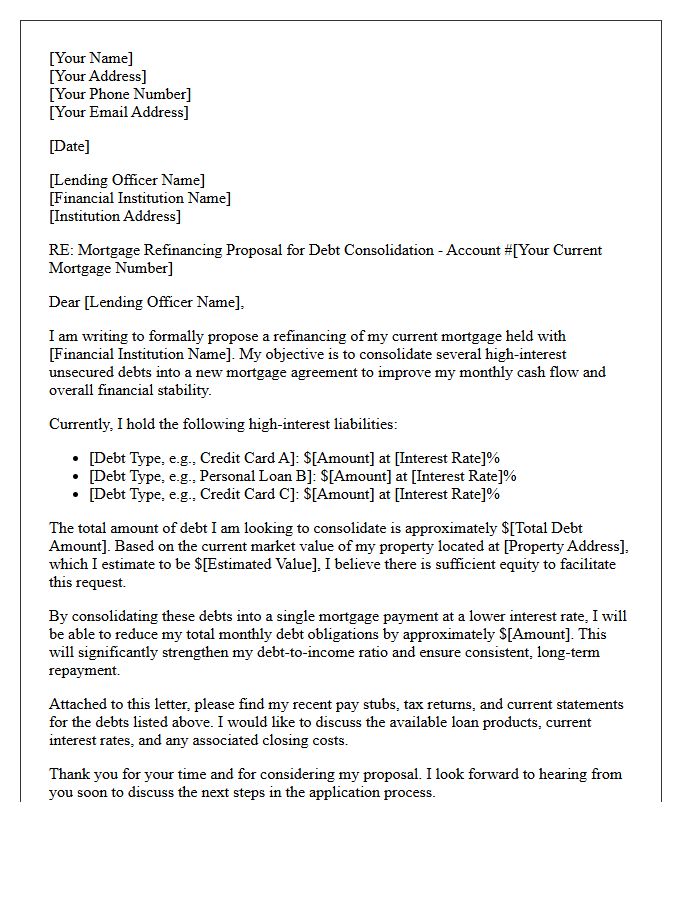

Debt Consolidation Mortgage Refinancing Proposal Letter

A Debt Consolidation Mortgage Refinancing Proposal Letter is a formal request to a lender to restructure high-interest liabilities into a single home loan. The primary goal is to leverage home equity to secure a lower overall interest rate and improve monthly cash flow. To be successful, the letter must clearly outline the current total debt, the requested loan-to-value ratio, and a stable repayment strategy. This document serves as a critical tool for demonstrating financial responsibility while seeking a more sustainable, consolidated financial structure through long-term mortgage financing.

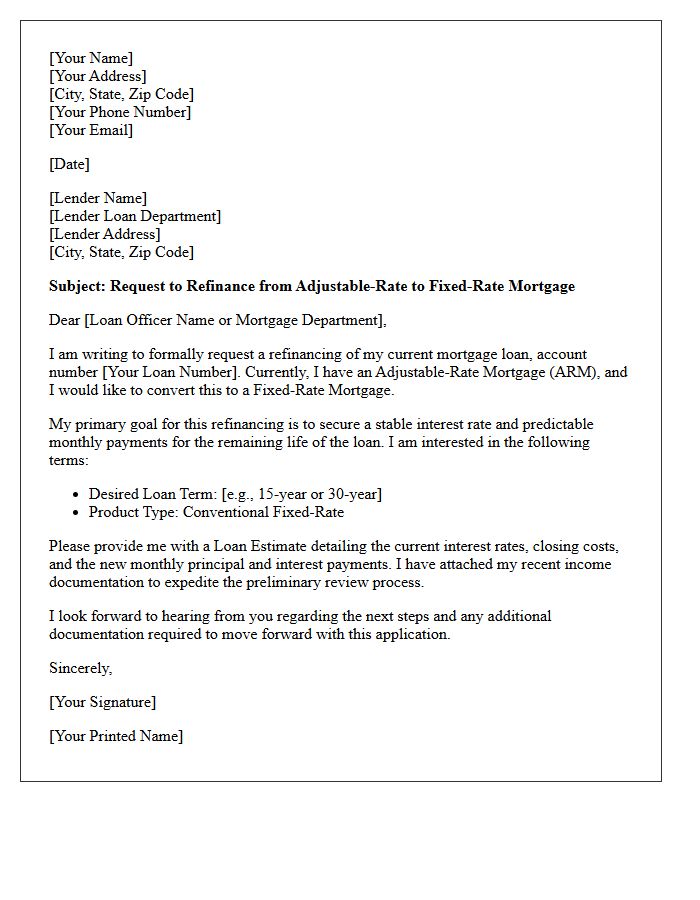

Adjustable to Fixed Rate Mortgage Refinancing Letter

An Adjustable to Fixed Rate Mortgage Refinancing Letter serves as a formal notification to borrowers regarding the opportunity to stabilize their monthly payments. Converting to a fixed-rate loan provides long-term financial security by eliminating risks associated with fluctuating interest rates. This document outlines the specific conversion terms, new interest rates, and updated repayment schedules. Understanding these changes is essential for homeowners seeking predictable budgeting. Always review the letter carefully to ensure the proposed transition aligns with your current financial goals and provides a lower cost of borrowing over time.

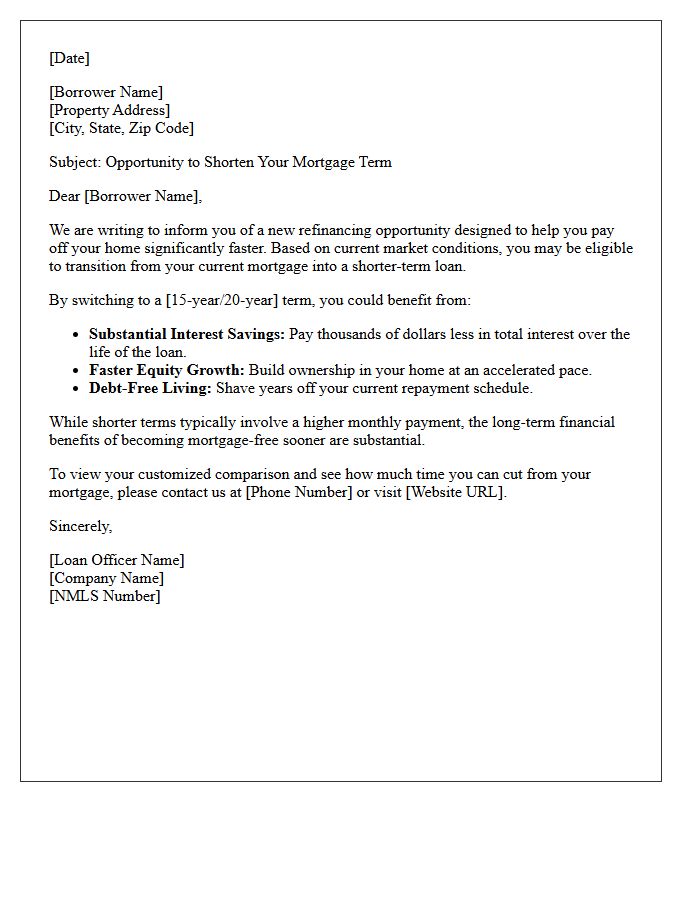

Loan Term Reduction Mortgage Refinancing Opportunity Letter

A Loan Term Reduction Mortgage Refinancing Opportunity Letter informs homeowners about options to shorten their debt duration. By transitioning from a 30-year to a 15-year term, you can save thousands in interest payments over the life of the loan. This process often involves a lower interest rate, though it may increase your monthly premium. Reviewing these offers helps you build home equity faster and achieve financial freedom sooner. Always verify the lender's credentials and compare closing costs before committing to a new agreement to ensure maximum long-term savings.

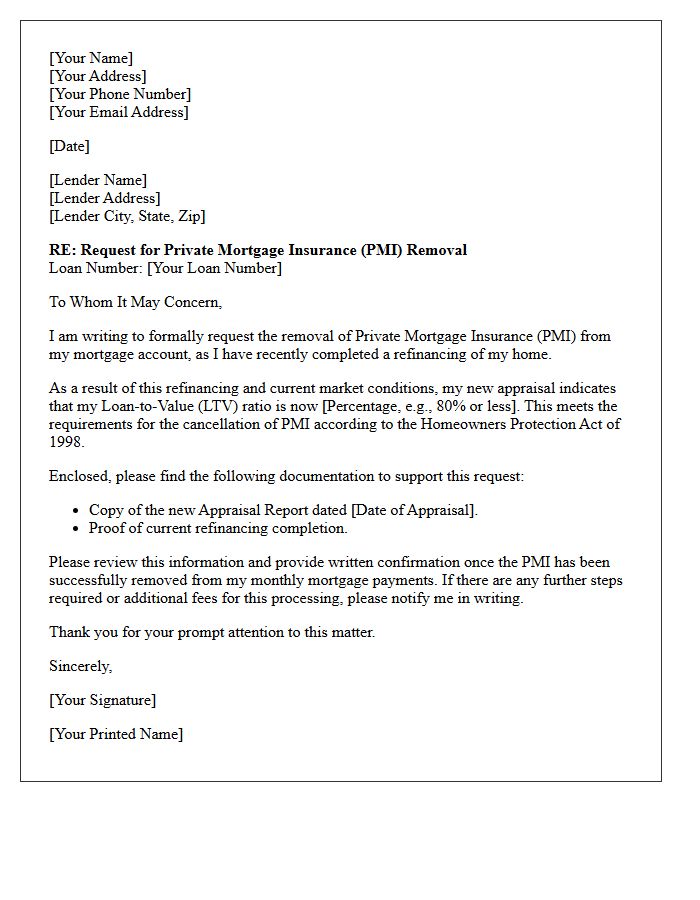

Private Mortgage Insurance Removal Refinancing Letter

A PMI removal refinancing letter is a formal request to your lender to cancel mortgage insurance after reaching 20% home equity. To optimize your chances, highlight your current property value and consistent payment history. If home prices have risen, an appraisal may prove you meet the 80% loan-to-value threshold without waiting years. This process is essential for reducing monthly housing costs. Always include your account number and a clear request for a valuation review to ensure the private mortgage insurance is legally terminated according to Homeowners Protection Act guidelines.

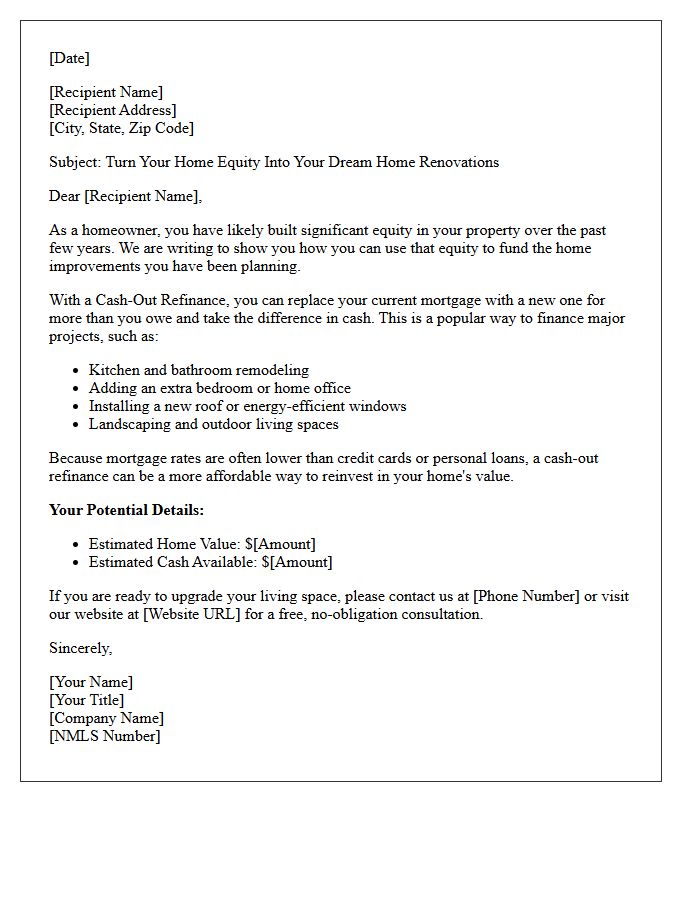

Home Improvement Cash-Out Refinancing Opportunity Letter

A home improvement cash-out refinance letter informs homeowners of the opportunity to leverage their built-in equity for property upgrades. This financial strategy replaces your existing mortgage with a larger loan, providing a lump sum of tax-free cash. It is an ideal solution for funding significant renovations while potentially securing a lower interest rate. Homeowners should review the loan-to-value requirements and terms offered to determine if current market conditions favor reinvesting in their property's value through this specific refinancing opportunity.

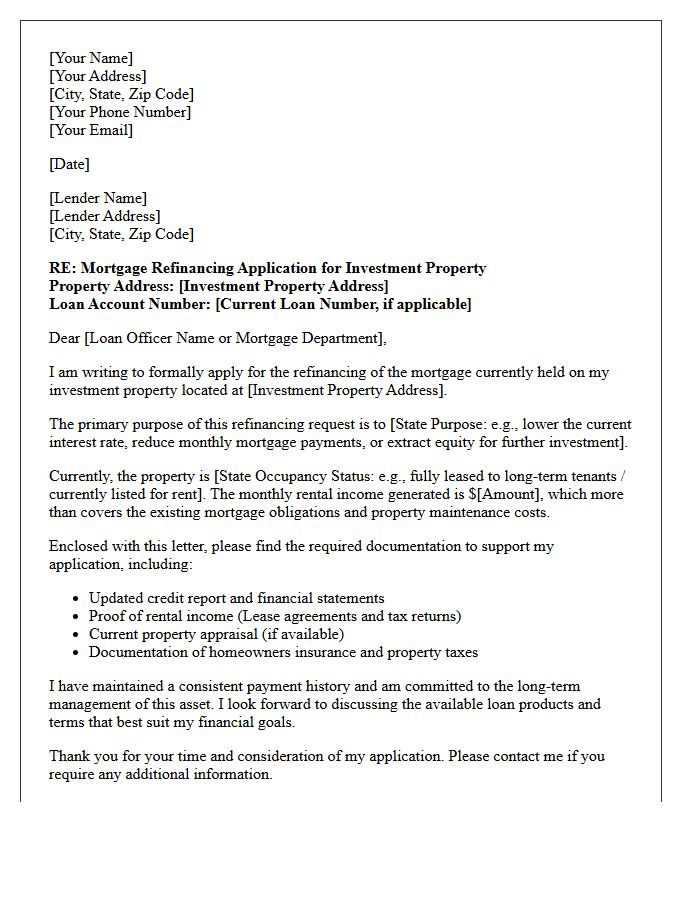

Investment Property Purchase Mortgage Refinancing Letter

An Investment Property Purchase Mortgage Refinancing Letter is a formal document used to explain the financial intent behind restructuring a loan. Lenders require this to verify your investment strategy, property management plans, and rental income potential. A well-drafted letter clarifies why you are seeking new terms, such as lowering interest rates or extracting equity for further acquisitions. It serves as a vital justification for credit underwriters to assess risk, ensuring the borrower demonstrates professional stability and a clear path toward maintaining positive cash flow on the asset.

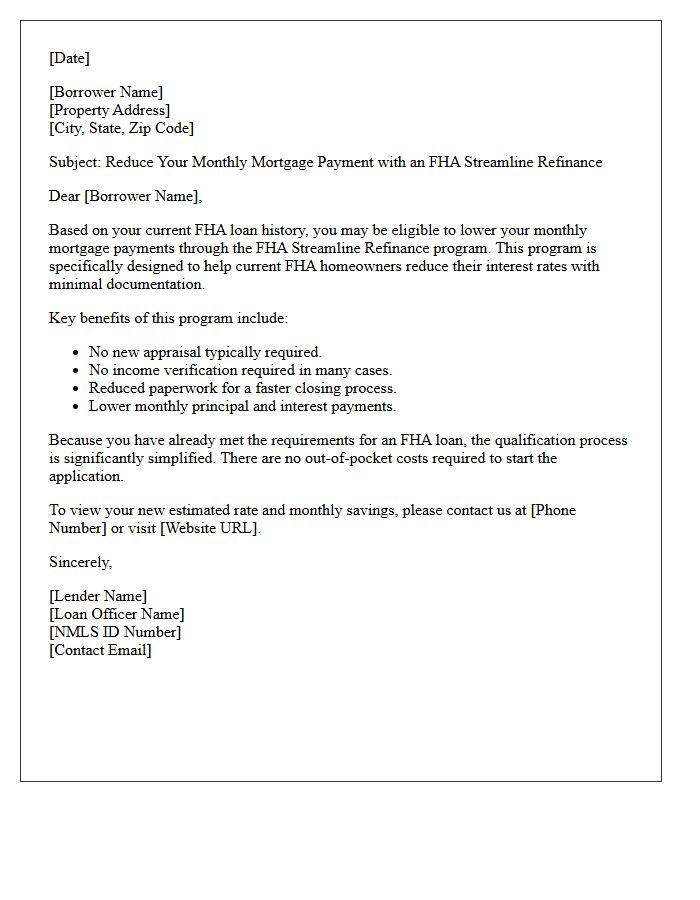

Streamline Federal Housing Administration Refinancing Letter

An FHA Streamline Refinance letter informs homeowners about an efficient way to lower their mortgage interest rates with minimal documentation. This process is designed for borrowers with existing FHA loans who want to reduce monthly payments without a new appraisal or extensive credit checks. To qualify, your mortgage must be current, and the refinance must provide a tangible net tangible benefit, such as a lower rate or shorter term. Receiving this letter indicates you may be eligible to save money through a simplified closing process with reduced paperwork and faster approval times.

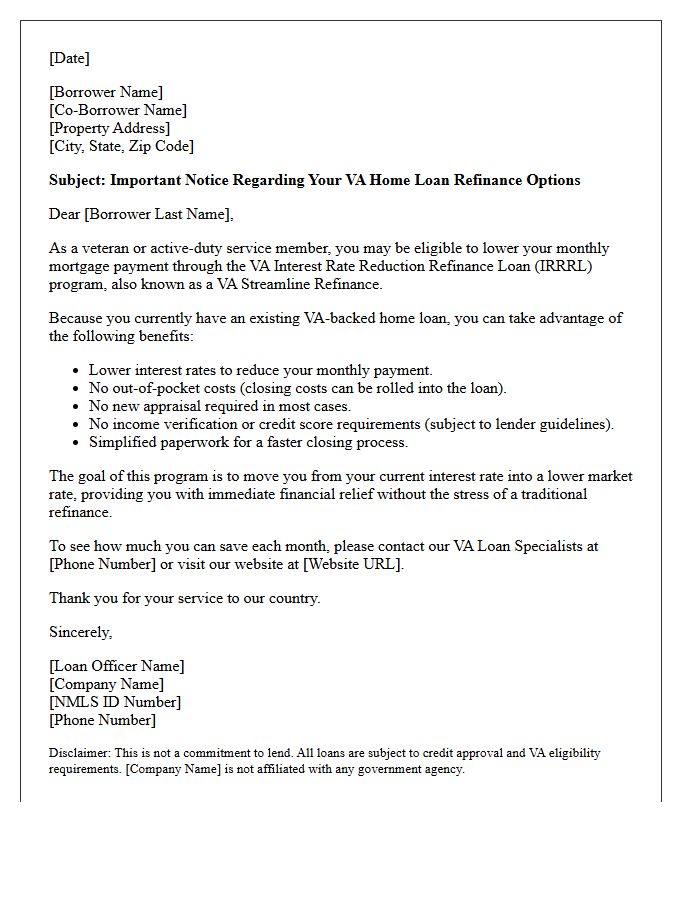

Veterans Affairs Streamline Mortgage Refinancing Letter

A Veterans Affairs Streamline Mortgage Refinancing Letter, formally known as an Interest Rate Reduction Refinance Loan (IRRRL), is a notification regarding your eligibility to lower monthly payments. This program allows veterans with existing VA loans to refinance with no appraisal and minimal paperwork. It is designed to reduce your interest rate or transition from an adjustable-rate to a fixed-rate mortgage. To qualify, you must demonstrate a net tangible benefit, ensuring the refinance provides immediate financial savings. Always verify offers through a VA-approved lender to ensure terms are legitimate and beneficial.

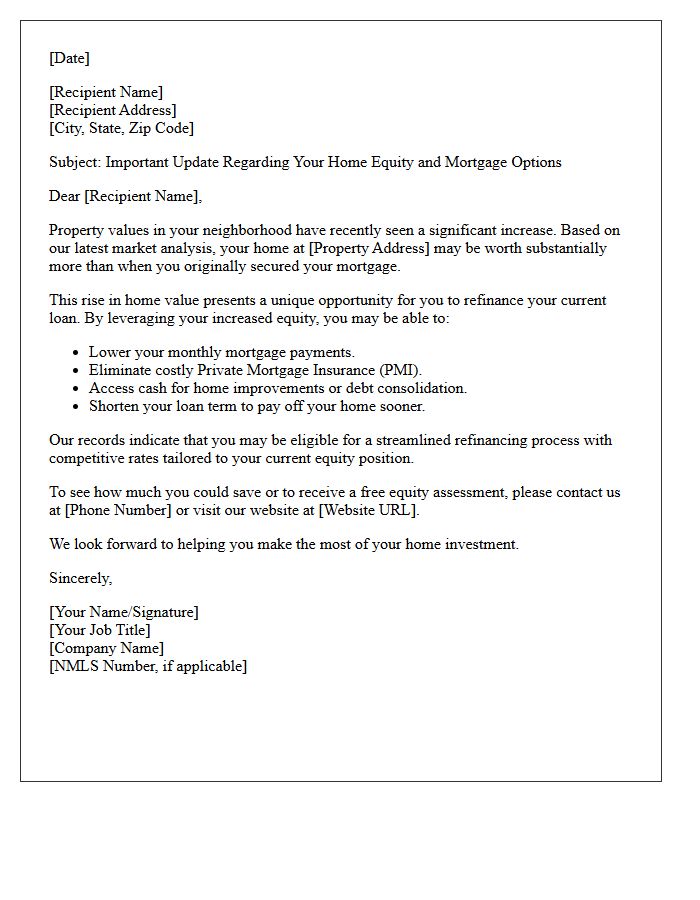

Rising Home Value Mortgage Refinancing Opportunity Letter

A rising home value mortgage refinancing opportunity letter informs homeowners that their increased equity allows for better loan terms. This document typically highlights the chance to secure a lower interest rate or cancel private mortgage insurance. It is a financial solicitation often triggered by local market growth. Recipients should verify the lender's credibility and compare current market rates before proceeding. Understanding your current loan-to-value ratio is essential to determine if this offer provides genuine savings or if closing costs outweigh the long-term benefits of the new mortgage structure.

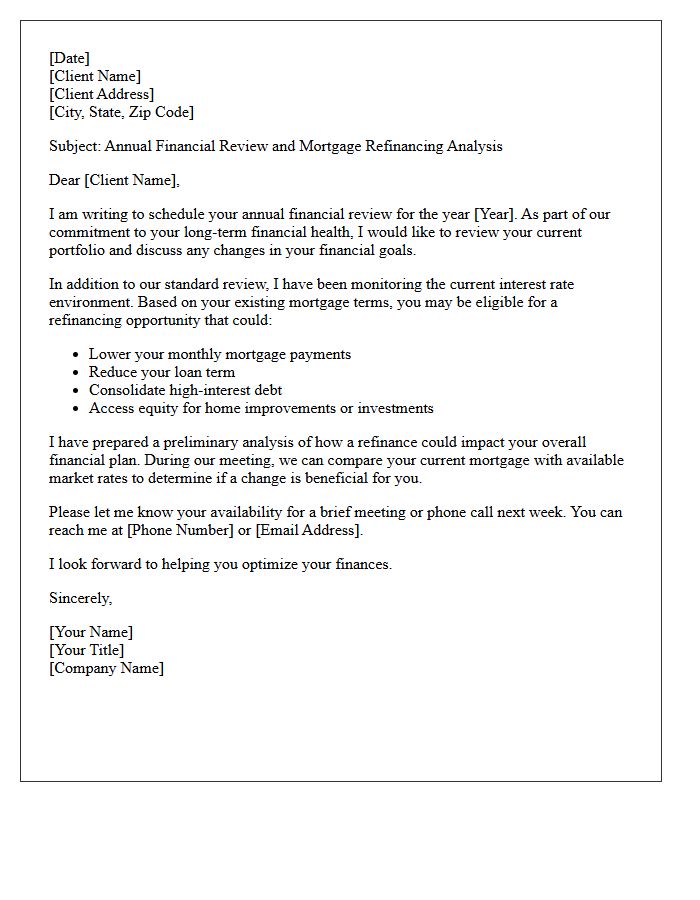

Annual Financial Review and Mortgage Refinancing Letter

An Annual Financial Review is a vital assessment of your fiscal health, ensuring your budget and investments align with long-term goals. Integrating a Mortgage Refinancing Letter into this process allows homeowners to formally request better loan terms. By evaluating current interest rates and equity, you can potentially lower monthly payments or shorten loan durations. This proactive strategy optimizes your debt management, enhances cash flow, and secures your financial future through informed interest rate adjustments and strategic equity utilization.

What is a mortgage refinancing opportunity letter?

A mortgage refinancing opportunity letter is a formal notification sent by a lender to inform a homeowner that they may qualify for a new loan with better terms, such as a lower interest rate or reduced monthly payments, based on current market conditions.

How do I know if the refinance offer in the letter is legitimate?

To verify a refinancing letter, check that the sender is your current mortgage servicer or a reputable licensed lender. Cross-reference the contact information with your official monthly statements and avoid offers that demand upfront fees before any paperwork is signed.

What are the benefits of responding to a refinancing opportunity letter?

Responding to a legitimate refinance offer can lead to significant financial benefits, including lowering your annual percentage rate (APR), switching from an adjustable-rate to a fixed-rate mortgage, or tapping into home equity for debt consolidation.

Does receiving a refinance letter mean I am pre-approved?

Receiving a letter usually indicates you are "pre-qualified" based on soft credit data, but it is not a guaranteed approval. You must still submit a formal application, undergo a full credit check, and provide income documentation to meet the lender's underwriting guidelines.

Are there costs associated with the refinancing opportunities mentioned in these letters?

Yes, refinancing typically involves closing costs, which can include appraisal fees, title insurance, and origination charges. Even if the letter advertises a "no-cost refinance," these expenses are often rolled into the new loan balance or covered by a slightly higher interest rate.

Comments