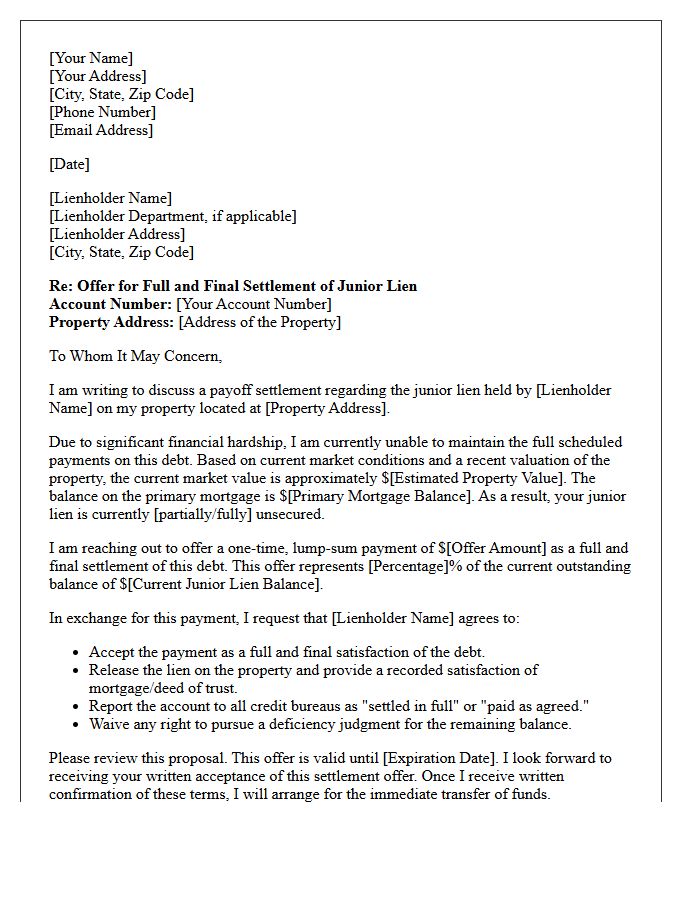

Negotiating a settlement with a secondary lender requires a strategic Junior Lienholder Payoff Negotiation Letter. Since these debts are often under-secured, lenders may accept a reduced lump-sum payment to release the lien. This process is essential for homeowners seeking to clear titles or avoid foreclosure through professional debt restructuring. To help you begin, below are some ready to use template.

Image cover: Settling Junior Liens: Negotiation Letter Templates and Proven Strategies

Letter Samples List

- Initial Contact Junior Lienholder Payoff Negotiation Letter

- Short Sale Junior Lienholder Payoff Negotiation Letter

- Financial Hardship Junior Lienholder Payoff Negotiation Letter

- Lump Sum Settlement Junior Lienholder Payoff Negotiation Letter

- Second Mortgage Junior Lienholder Payoff Negotiation Letter

- Home Equity Line Junior Lienholder Payoff Negotiation Letter

- Foreclosure Avoidance Junior Lienholder Payoff Negotiation Letter

- Underwater Property Junior Lienholder Payoff Negotiation Letter

- Commercial Real Estate Junior Lienholder Payoff Negotiation Letter

- Residential Property Junior Lienholder Payoff Negotiation Letter

- Final Offer Junior Lienholder Payoff Negotiation Letter

- Debt Forgiveness Junior Lienholder Payoff Negotiation Letter

Initial Contact Junior Lienholder Payoff Negotiation Letter

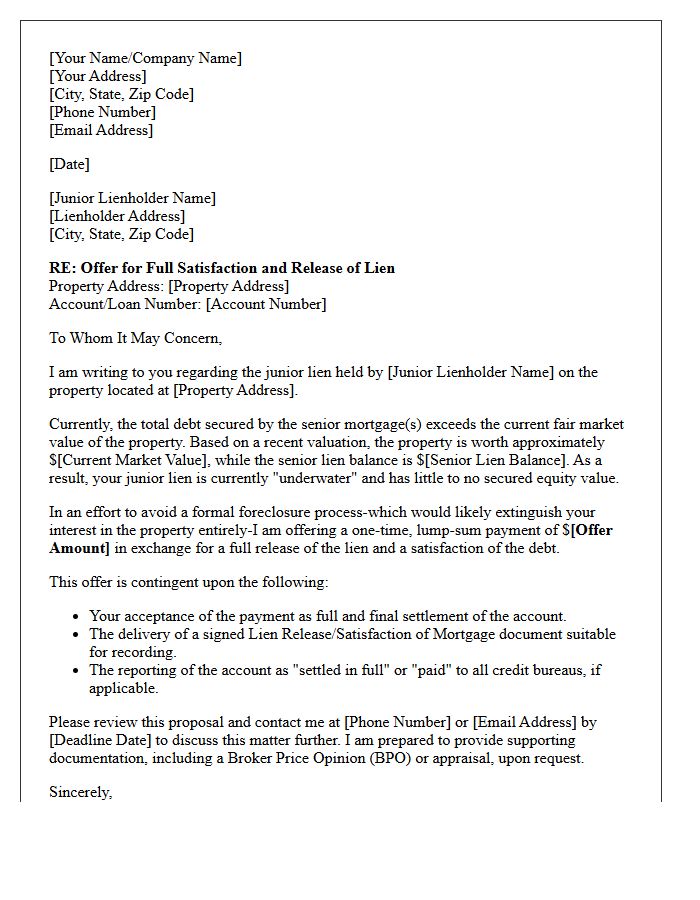

An Initial Contact Junior Lienholder Payoff Negotiation Letter is a strategic formal request sent to secondary lenders to settle debt for less than the full balance. This document initiates the short sale or settlement process by demonstrating the homeowner's financial hardship and the property's lack of sufficient equity to cover the junior lien. By proposing a pro-rata share or a specific settlement offer, you encourage the lender to accept a smaller payout rather than risking a total loss through a senior lienholder's foreclosure action.

Short Sale Junior Lienholder Payoff Negotiation Letter

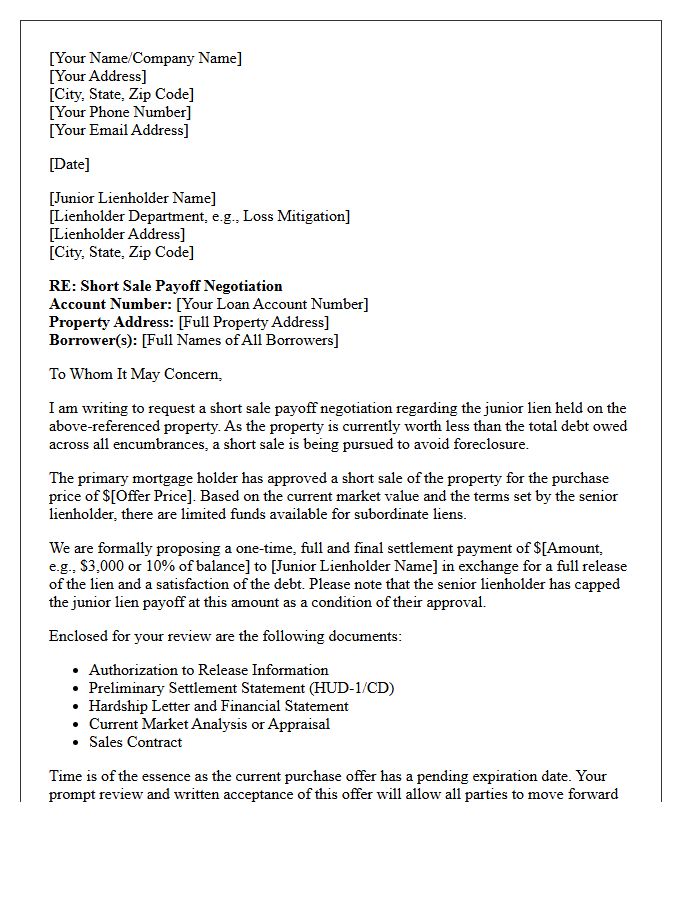

A short sale junior lienholder payoff negotiation letter is a formal request to subordinate lenders, like second mortgage holders, to accept a reduced settlement. Since junior liens are often wiped out in foreclosure, the letter emphasizes that a short sale offers a higher recovery than a total loss. To succeed, the proposal should include a specific payoff amount, a hardship statement, and an explanation of the property's diminished value. Securing a written lien release and a deficiency waiver is essential to ensure the homeowner is fully protected from future collection actions.

Financial Hardship Junior Lienholder Payoff Negotiation Letter

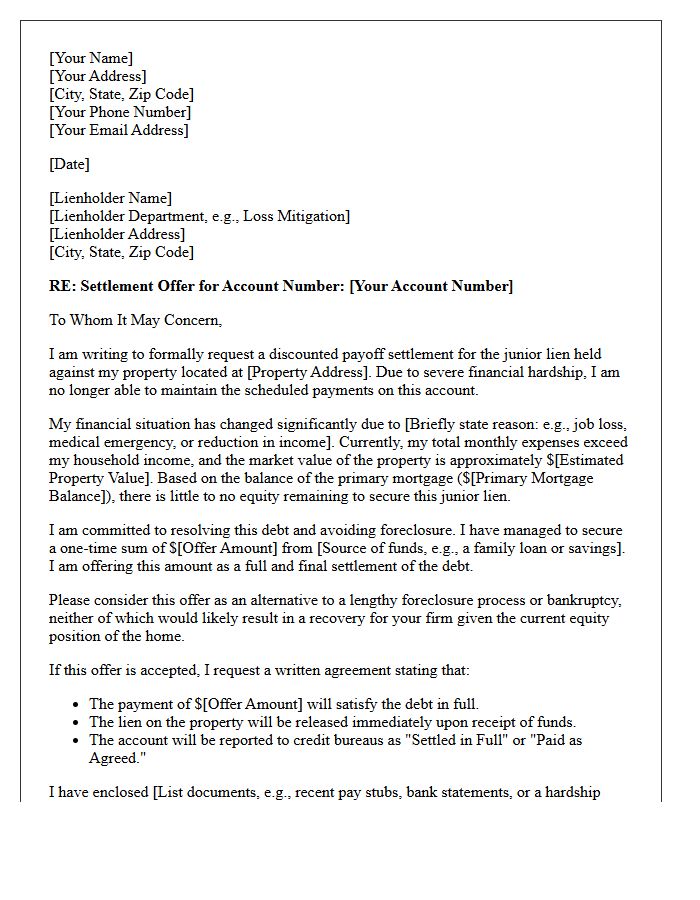

A Financial Hardship Junior Lienholder Payoff Negotiation Letter is a formal request to settle a secondary mortgage for less than the total balance. To succeed, clearly document your insolvency or lack of equity, proving the creditor would recover nothing through foreclosure. Emphasize that a short payoff is a mutually beneficial alternative to bankruptcy. Clearly state your specific settlement offer and provide supporting financial evidence. Securing a written release of the lien is the primary goal to clear your property title and resolve the debt permanently.

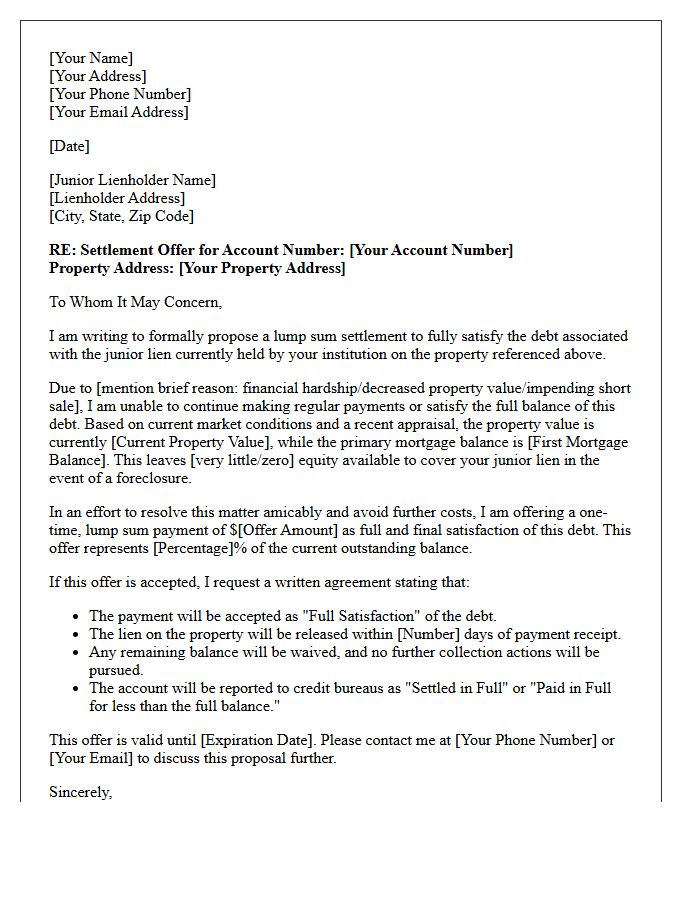

Lump Sum Settlement Junior Lienholder Payoff Negotiation Letter

A Lump Sum Settlement Junior Lienholder Payoff Negotiation Letter is a formal proposal sent to a secondary mortgage lender to settle a debt for less than the full balance. This strategy is vital during a short sale or foreclosure avoidance process. Because junior liens are high-risk in default, lenders may accept a smaller cash payment to release the lien. The letter must clearly demonstrate financial hardship and provide a specific offer amount to incentivize the lender to cooperate and waive their right to a deficiency judgment.

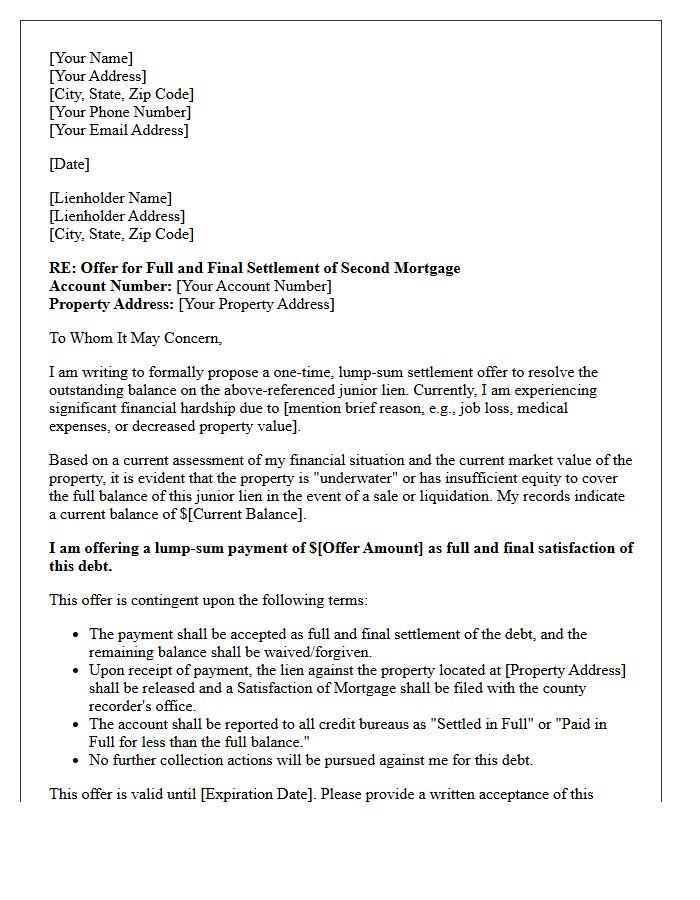

Second Mortgage Junior Lienholder Payoff Negotiation Letter

A second mortgage payoff negotiation letter is a formal request to settle a junior lien for less than the full balance. Since secondary lenders risk receiving nothing during a foreclosure, they may accept a discounted lump-sum payment to release the claim. Your letter should clearly demonstrate financial hardship, provide a specific settlement offer, and highlight the short sale or foreclosure risk. Ensuring the agreement is documented in writing is essential to verify that the debt is fully satisfied and the lien release is recorded with the county to clear the property title.

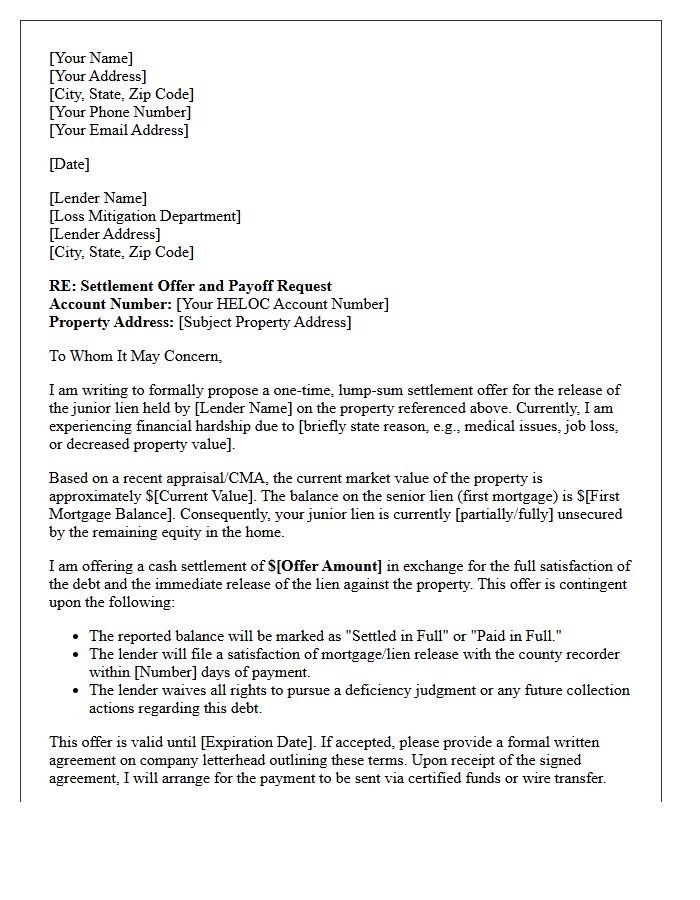

Home Equity Line Junior Lienholder Payoff Negotiation Letter

A Home Equity Line Junior Lienholder Payoff Negotiation Letter is a formal request sent to a secondary lender to settle a debt for less than the full balance. This strategy is essential during a short sale or foreclosure when property value cannot cover all debts. The goal is to convince the junior lienholder to release their claim in exchange for a smaller, lump-sum payment. Successful letters emphasize the lender's risk of receiving nothing if a senior creditor forecloses, making a settlement the most practical financial recovery option for all parties involved.

Foreclosure Avoidance Junior Lienholder Payoff Negotiation Letter

A Foreclosure Avoidance Junior Lienholder Payoff Negotiation Letter is a formal proposal sent to secondary lenders to settle debt for less than the full balance. Since junior liens are unsecured during short sales or foreclosures, lenders often accept a small percentage of the loan to release their claim. Effective letters highlight the lack of equity and the financial hardship of the homeowner. Successful negotiation removes the lien, allowing a property sale to proceed while preventing personal liability for the remaining deficiency balance. Professional documentation is essential for securing a lien release.

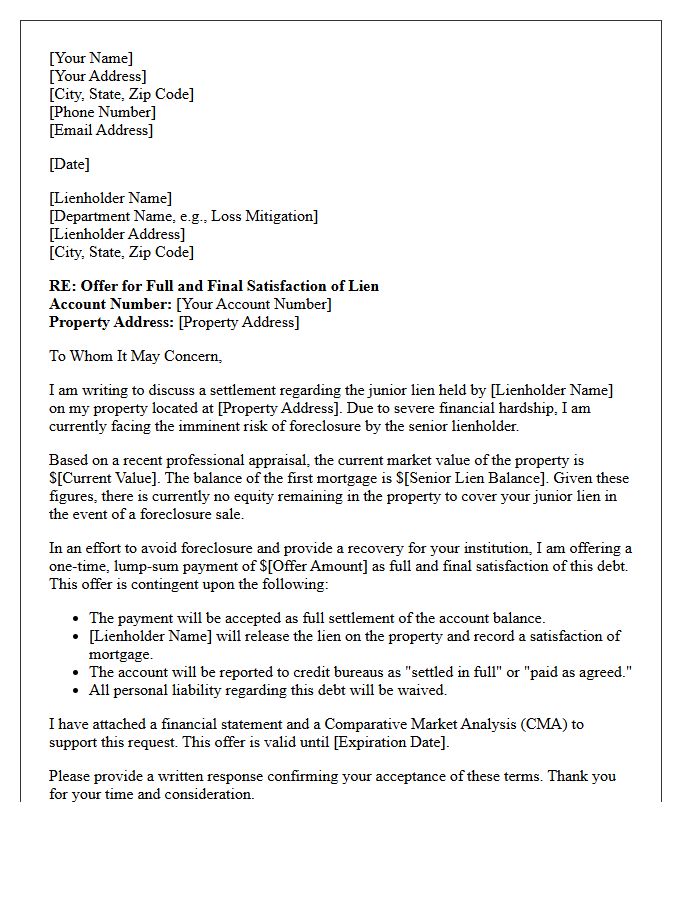

Underwater Property Junior Lienholder Payoff Negotiation Letter

An Underwater Property Junior Lienholder Payoff Negotiation Letter is a formal proposal sent to secondary lenders when a home's value is less than the total debt. This document aims to secure a short sale approval or a discounted settlement. Key elements include demonstrating financial hardship, proving the lack of equity, and offering a specific pro-rata share of proceeds. Successful negotiation requires showing the lienholder that accepting a smaller payment is more profitable than risking a total loss through a senior lender's foreclosure action.

Commercial Real Estate Junior Lienholder Payoff Negotiation Letter

A commercial real estate junior lienholder payoff negotiation letter is a formal proposal to settle subordinate debt for less than the full balance. This document is essential during a short sale or debt restructuring to clear the title. It should emphasize the property's current market value, the senior lender's position, and the risk of total loss through foreclosure. Successfully negotiating a discounted payoff requires transparency regarding financial hardship. Providing a clear justification for the reduced payment helps convince junior creditors that accepting a smaller sum is more beneficial than receiving nothing.

Residential Property Junior Lienholder Payoff Negotiation Letter

A residential property junior lienholder payoff negotiation letter is a formal proposal sent to secondary lenders, such as HELOC providers, to settle outstanding debt for less than the full balance. This strategy is essential during short sales or foreclosures when property value cannot cover all debts. The letter must demonstrate the borrower's financial hardship and prove that the junior lienholder risks receiving nothing if the senior lender forecloses. Successful negotiations result in a lien release, allowing for a clear title transfer while significantly reducing the homeowner's total deficiency liability.

Final Offer Junior Lienholder Payoff Negotiation Letter

A Final Offer Junior Lienholder Payoff Negotiation Letter is a formal proposal used to settle secondary debt for a fraction of the balance. To succeed, the letter must clearly demonstrate insolvency or lack of equity, proving the creditor would receive nothing through foreclosure. It represents a strategic ultimatum, typically offering a one-time cash payment in exchange for a full lien release. This document is essential for homeowners pursuing a short sale or loan modification, as it establishes a definitive paper trail for debt satisfaction and title clearance.

Debt Forgiveness Junior Lienholder Payoff Negotiation Letter

A Debt Forgiveness Junior Lienholder Payoff Negotiation Letter is a formal request to settle a secondary mortgage for less than the full balance. To succeed, emphasize that the current home value is insufficient to cover the primary loan, leaving the junior lienholder unsecured. Highlight financial hardship and the risk of foreclosure, which would result in zero recovery for them. Proposing a lump-sum settlement encourages the lender to release the lien quickly. Professionalism and clear evidence of negative equity are vital for securing a successful debt discharge and clear title.

What is a Junior Lienholder Payoff Negotiation Letter?

A Junior Lienholder Payoff Negotiation Letter is a formal written proposal sent by a homeowner or their representative to a secondary mortgage holder, such as a second mortgage or HELOC provider, requesting to settle the debt for less than the full balance owed.

When should I use a payoff negotiation letter for a second mortgage?

You should use this letter when the current market value of your property is less than the total debt owed on all liens, or when you are attempting a short sale or loan modification and need the junior lienholder to release their claim for a reduced settlement amount.

What key information must be included in a junior lien settlement proposal?

The letter must include the account number, the property address, a detailed hardship statement, a comparative market analysis (CMA) showing the home's current value, and a specific "bottom line" settlement offer backed by evidence of your inability to pay the full amount.

Can a junior lienholder refuse a payoff negotiation?

Yes, junior lienholders are not legally required to accept a reduced payoff. However, if the primary mortgage is in default and there is no equity in the home to cover the second lien during a foreclosure, they may be incentivized to accept a settlement rather than receiving nothing.

How does a successful junior lien negotiation affect my credit score?

Settling a junior lien for less than the full balance typically results in the account being reported to credit bureaus as "Settled for less than full balance," which can negatively impact your credit score, though often less severely than a full foreclosure or bankruptcy.

Comments