A Notice of Cancellation for Material Misrepresentation is a formal legal document used by insurers to void a policy when a client provides false or withheld information. This action occurs because the hidden facts significantly impact risk assessment and underwriting decisions. Understanding your rights and policy clauses is essential during this process. Below are some ready to use templates.

Image cover: Sample Notice of Cancellation for Material Misrepresentation: Templates and Best Practices

Letter Samples List

- Standard Notice Of Cancellation Letter For Material Misrepresentation

- Auto Insurance Undisclosed Driver Cancellation Letter

- Homeowners Policy Property Condition Misrepresentation Cancellation Letter

- Commercial General Liability Business Operations Misrepresentation Letter

- Health Insurance Preexisting Condition Omission Cancellation Letter

- Life Insurance Application Fraud Notice Of Cancellation Letter

- Workers Compensation Payroll Misrepresentation Cancellation Letter

- Professional Liability Claim History Nondisclosure Cancellation Letter

- Watercraft Insurance Usage Misrepresentation Notice Of Cancellation Letter

- Renters Insurance Prior Loss Concealment Cancellation Letter

- Umbrella Policy Underlying Coverage Misrepresentation Cancellation Letter

- Cyber Liability Security Controls Nondisclosure Cancellation Letter

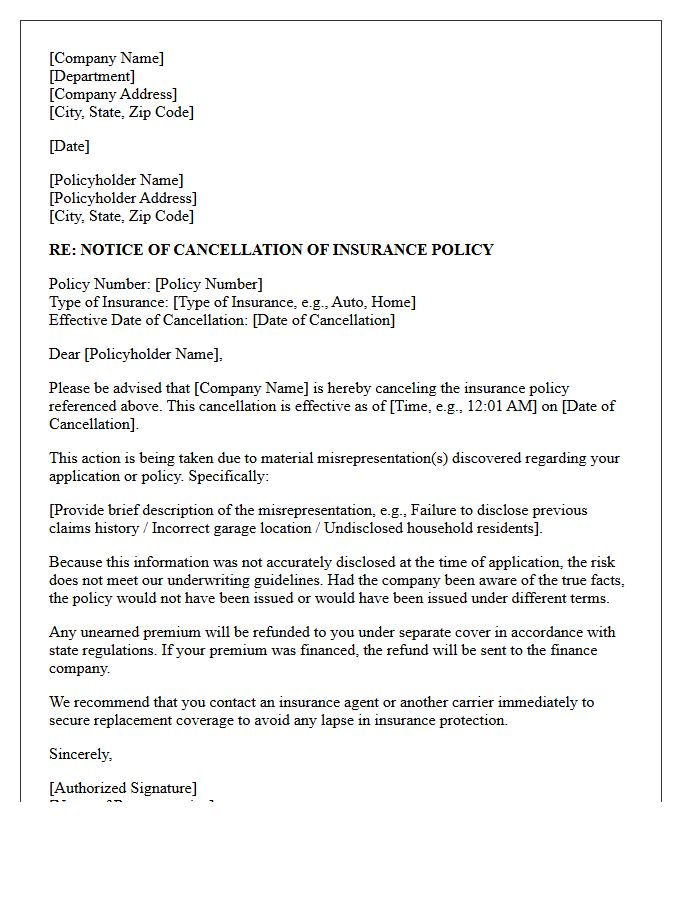

Standard Notice Of Cancellation Letter For Material Misrepresentation

A standard notice of cancellation for material misrepresentation is a formal legal document issued by an insurer to terminate a policy. This occurs when an insured individual provides false information or conceals critical facts that would have influenced the underwriting decision. Unlike standard lapses, this action often renders the contract void from inception, meaning claims can be denied retroactively. It is crucial to ensure all application data is accurate to maintain enforceable coverage and avoid the severe legal consequences associated with insurance fraud or nondisclosure.

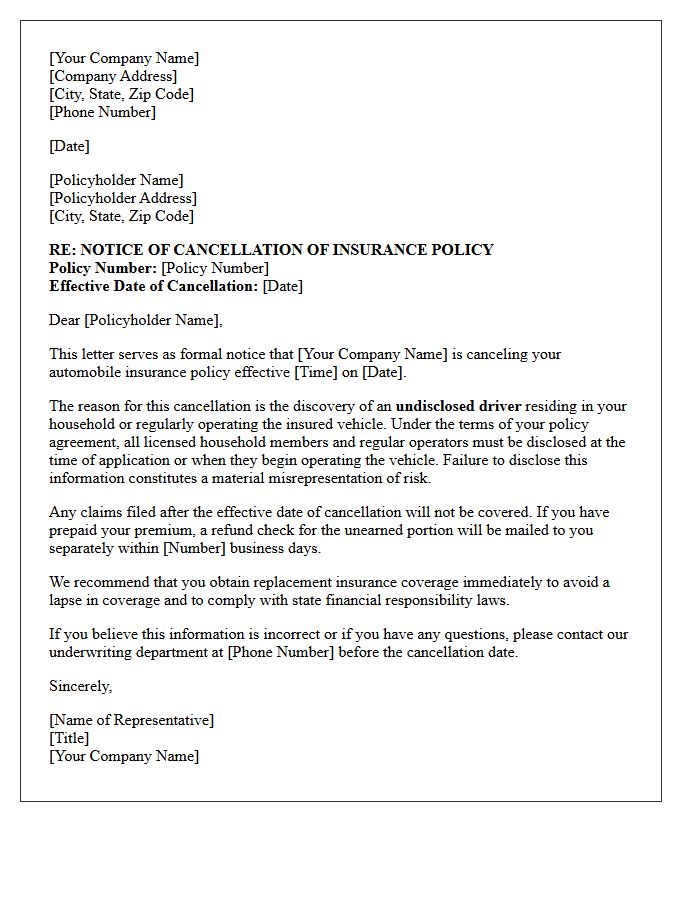

Auto Insurance Undisclosed Driver Cancellation Letter

An Auto Insurance Undisclosed Driver Cancellation Letter notifies policyholders that their coverage is being terminated due to material misrepresentation. Insurance companies require the disclosure of all licensed household residents to assess risk accurately. If an unlisted driver regularly uses the vehicle, it violates the policy terms. Receiving this notice means your insurance policy is voided, often leading to a lapse in coverage and higher future premiums. To prevent policy rescission, always update your insurer about new drivers in your home immediately to ensure continuous financial protection.

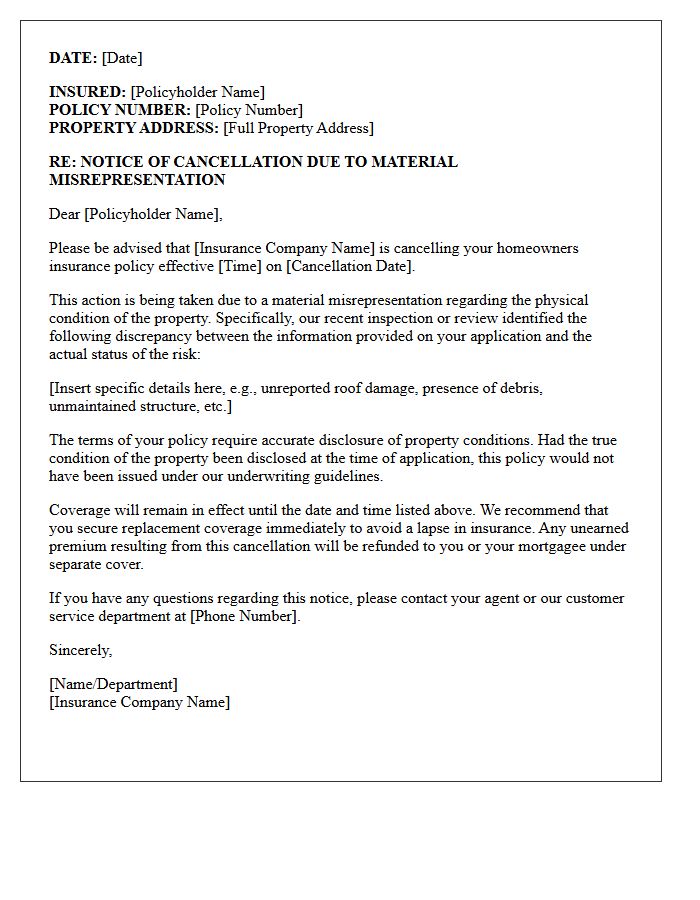

Homeowners Policy Property Condition Misrepresentation Cancellation Letter

Receiving a cancellation letter due to property condition misrepresentation is a serious matter. It indicates the insurer discovered discrepancies between your application and the home's actual state, such as unreported damage or outdated systems. This action often leads to a coverage void, leaving your assets unprotected. To resolve this, you must promptly provide documented proof of repairs or updates. Failure to address these concerns can make securing future homeowners insurance significantly more expensive or difficult, as you may be labeled a high-risk policyholder.

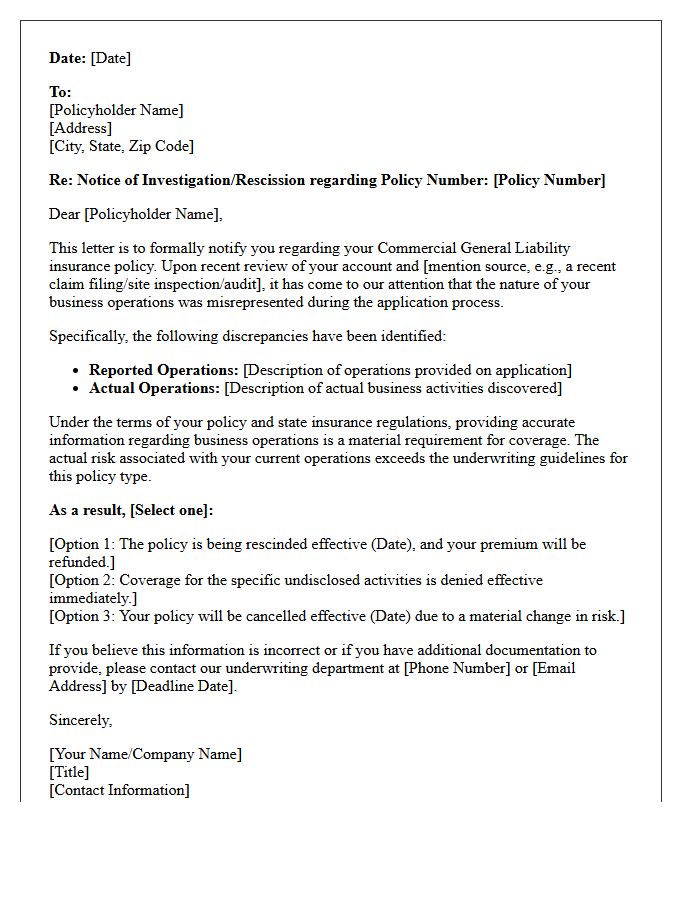

Commercial General Liability Business Operations Misrepresentation Letter

A Commercial General Liability Business Operations Misrepresentation Letter is a critical notice sent by insurers when they discover inaccuracies in a policy application. This document formalizes discrepancies between reported activities and actual daily operations. If a company misrepresents its risks, the insurer may void coverage or deny claims based on material misrepresentation. Business owners must respond promptly to verify facts, as unresolved issues can lead to policy rescission. Maintaining transparent communication and accurate risk assessment is essential to ensuring continuous legal protection and financial stability for the enterprise.

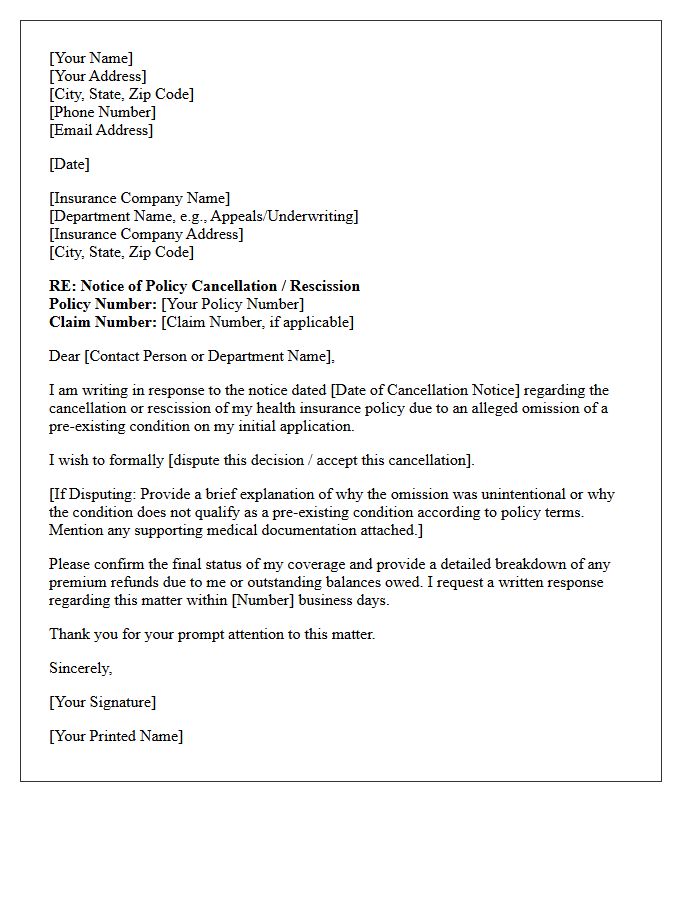

Health Insurance Preexisting Condition Omission Cancellation Letter

Receiving a cancellation letter for your health insurance due to a preexisting condition omission is a serious matter. This occurs when an insurer alleges you failed to disclose medical history during enrollment, leading to a policy rescission. It is crucial to act immediately by reviewing your original application for accuracy. You have the legal right to appeal this decision if the omission was unintentional or the condition was unknown. Promptly gather medical records and legal advice to prevent a coverage gap and protect your healthcare access.

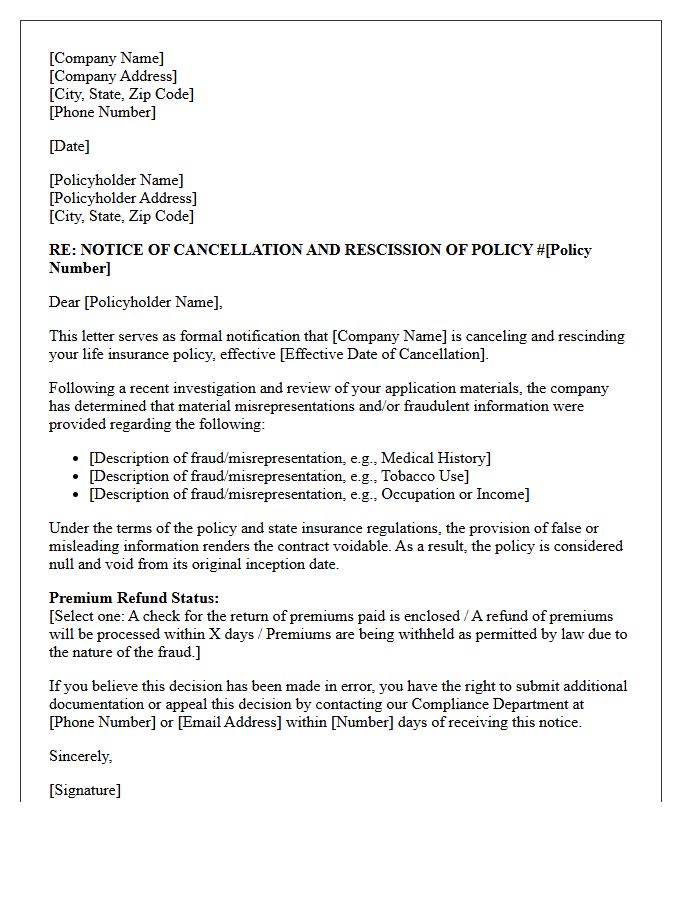

Life Insurance Application Fraud Notice Of Cancellation Letter

A Life Insurance Application Fraud Notice of Cancellation Letter is a formal document notifying the policyholder that their coverage is voided due to material misrepresentation. Insurance companies issue this when they discover dishonest information regarding medical history, lifestyle, or age during the underwriting process. This notice typically leads to a full rescission of the policy, meaning the insurer is no longer liable for claims. It is crucial to ensure all application data is accurate to avoid fraudulent claims allegations and the permanent loss of financial protection for your beneficiaries.

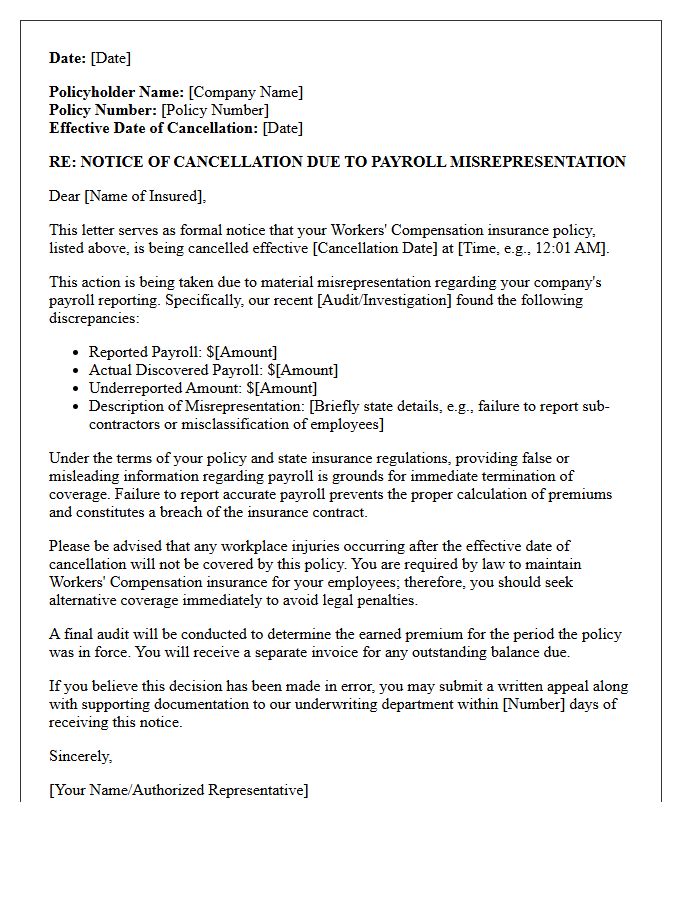

Workers Compensation Payroll Misrepresentation Cancellation Letter

A Workers Compensation Payroll Misrepresentation Cancellation Letter is a formal legal notice issued by an insurer when an employer provides inaccurate wage data. Underreporting payroll or misclassifying employees is considered premium fraud, leading to immediate policy termination. This document outlines the specific discrepancies found during audits. Receiving this letter is critical because it results in a coverage gap, potential state penalties, and difficulty securing future insurance. Employers must ensure accurate reporting to maintain compliance and avoid severe financial liabilities or criminal charges associated with insurance misrepresentation.

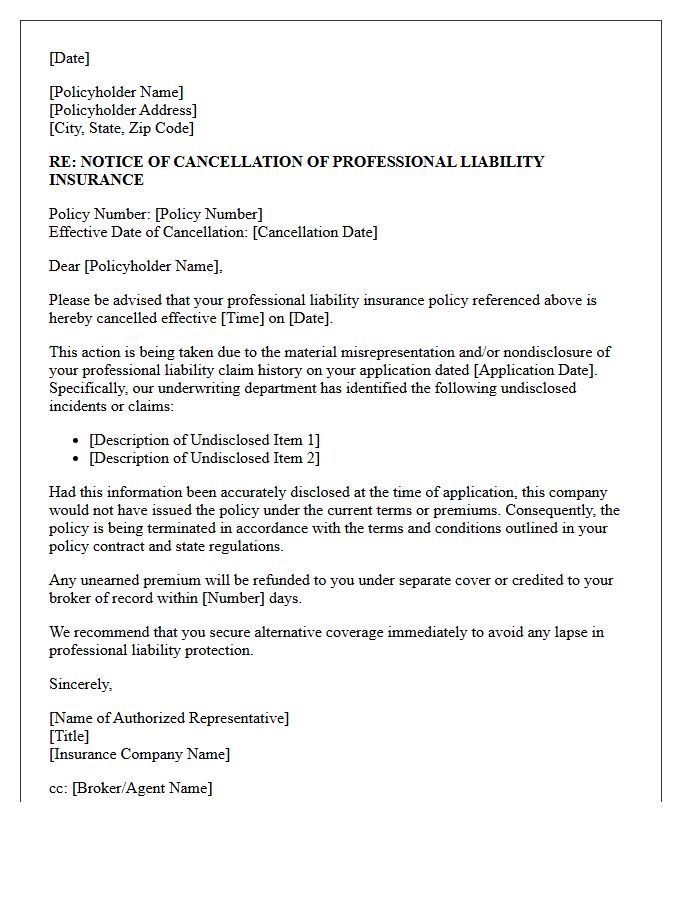

Professional Liability Claim History Nondisclosure Cancellation Letter

A professional liability claim history nondisclosure cancellation letter is a formal notice terminating an insurance policy due to material misrepresentation. Insurers issue this when a policyholder fails to report previous legal claims or incidents during the application process. Nondisclosure compromises the underwriting integrity, leading to a retroactive rescission or immediate policy cancellation. It is crucial to understand that failing to disclose your full history can result in a denial of coverage for future claims, leaving your business exposed to significant financial and legal risks without protection.

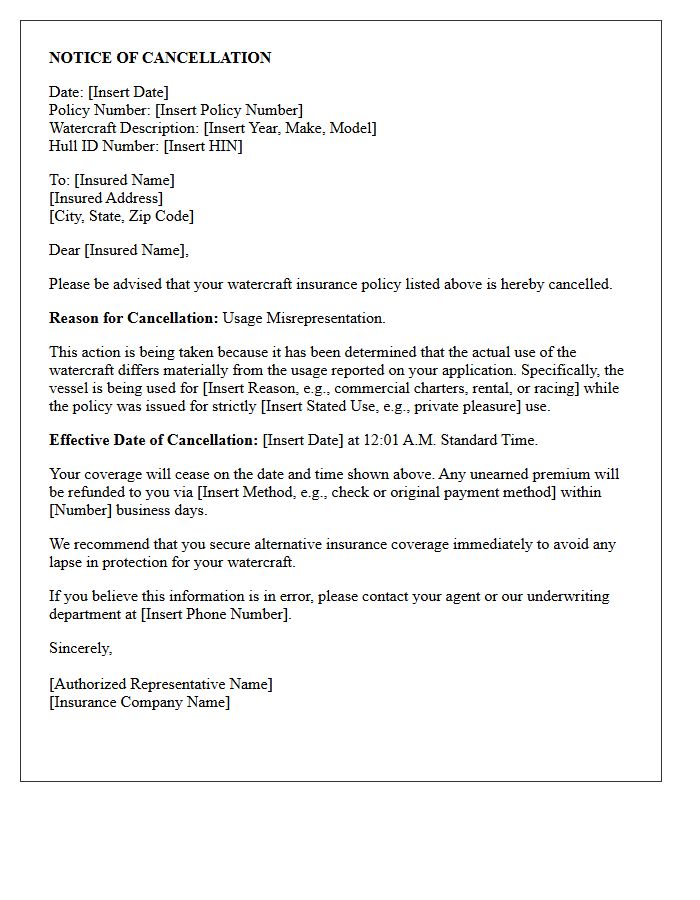

Watercraft Insurance Usage Misrepresentation Notice Of Cancellation Letter

A Notice of Cancellation for watercraft insurance is issued when a policyholder provides false information regarding vessel usage. This typically occurs if a personal boat is used for commercial purposes, racing, or outside agreed geographical limits. Misrepresentation violates the insurance contract, leading to a mandatory termination of coverage. Insurers send this formal letter to notify the owner that protection will cease on a specific date. It is critical to ensure your usage declarations are accurate to avoid claim denials and permanent loss of insurance eligibility.

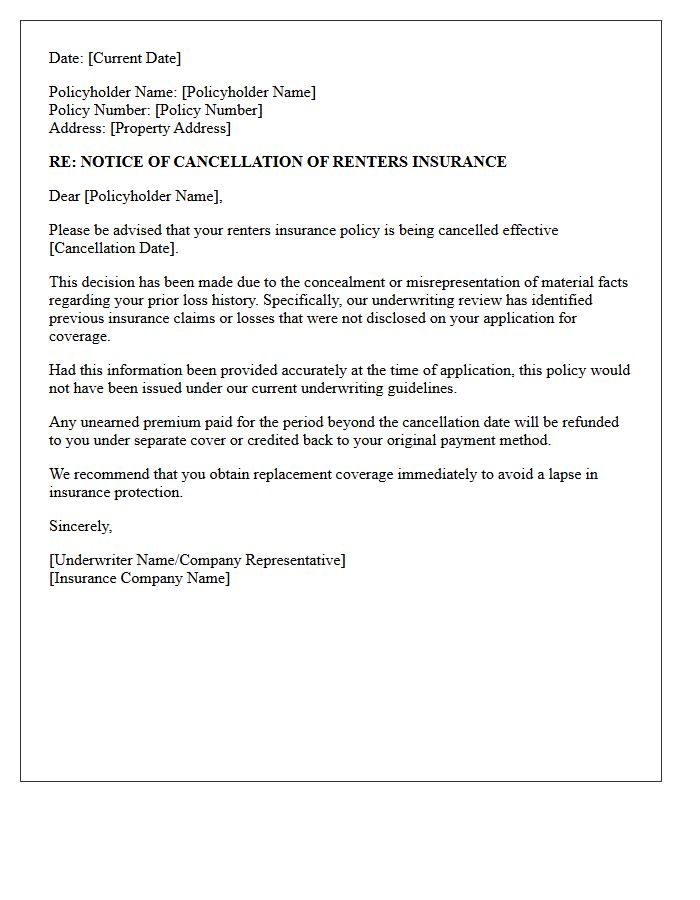

Renters Insurance Prior Loss Concealment Cancellation Letter

Receiving a Renters Insurance Cancellation Letter for prior loss concealment indicates that the insurer discovered undisclosed claims history. Insurance companies utilize comprehensive databases to verify past incidents. If an applicant fails to report previous losses, it is considered material misrepresentation, leading to immediate policy rescission. This action negatively impacts your insurance score and makes securing future coverage significantly more expensive. If you receive this notice, review your claims report for accuracy and ensure full disclosure on all future applications to maintain eligibility and protect your personal property effectively.

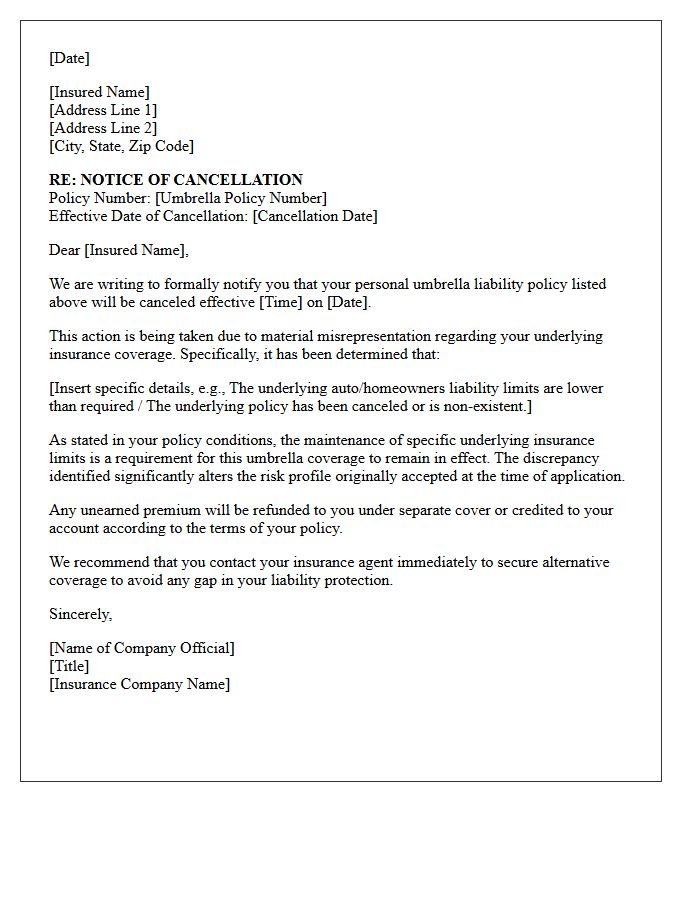

Umbrella Policy Underlying Coverage Misrepresentation Cancellation Letter

An Umbrella Policy Cancellation Letter is a formal notice issued when underlying coverage misrepresentation occurs. This typically happens if a policyholder provides false information regarding their primary auto or homeowners limits. Since an umbrella policy requires specific base liability levels to function, any discrepancy constitutes a material breach of contract. Such misrepresentation leads to immediate policy termination or claim denial. Maintaining accurate records of your underlying insurance is essential to prevent a coverage gap and ensure your supplemental liability protection remains legally valid and active.

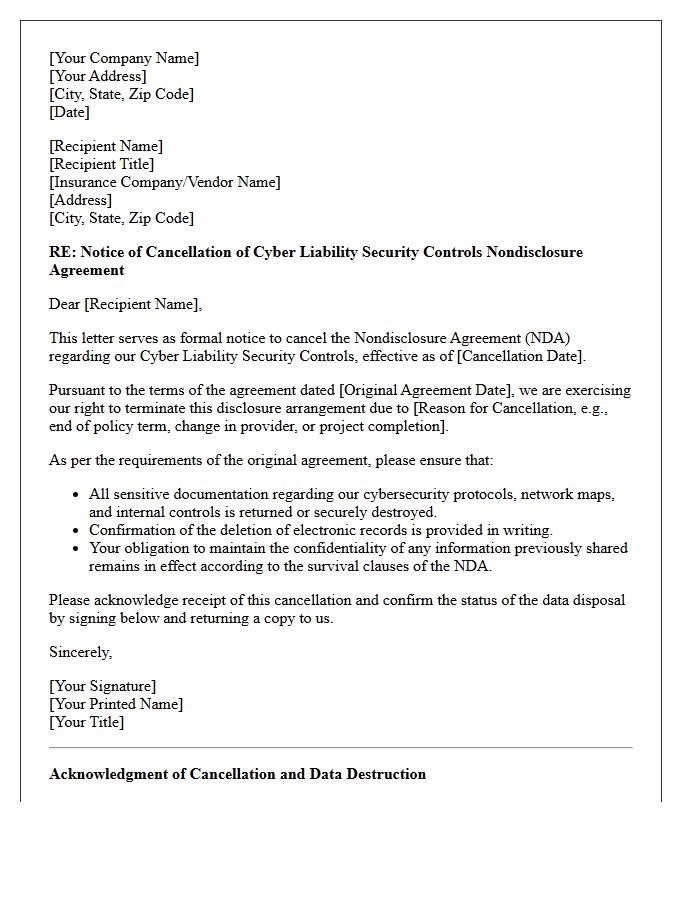

Cyber Liability Security Controls Nondisclosure Cancellation Letter

A Cyber Liability Security Controls Nondisclosure Cancellation Letter is a formal notice sent by an insurer to terminate coverage due to a policyholder's failure to maintain agreed-upon security protocols. Insurers conduct periodic audits to ensure businesses uphold mandatory safeguards like multi-factor authentication or encryption. If these minimum security controls are neglected or misrepresented, the carrier issues this letter to void the policy. To prevent coverage gaps and financial exposure, organizations must rectify security deficiencies immediately and maintain transparent communication with their insurance provider regarding their technical infrastructure.

What is a Notice of Cancellation for Material Misrepresentation?

A Notice of Cancellation for Material Misrepresentation is a formal document issued by an insurance company to terminate a policy because the policyholder provided false, incomplete, or misleading information during the application process that affected the insurer's risk assessment.

How does material misrepresentation affect my insurance coverage?

Material misrepresentation renders the original insurance contract void or voidable. If an insurer discovers that key facts-such as claims history, property usage, or driver information-were misrepresented, they have the legal right to cancel the policy and deny any pending claims associated with that misinformation.

Can an insurance company cancel a policy immediately for misrepresentation?

Yes, insurance companies can cancel a policy if they discover material misrepresentation, though state laws typically require them to provide a specific notice period (often 10 to 30 days). In cases of proven fraud, the insurer may rescind the policy entirely, treating it as if it never existed from the effective date.

What is the difference between an innocent mistake and material misrepresentation?

An innocent mistake is a minor clerical error that does not impact the premium or eligibility. Material misrepresentation involves withholding or falsifying information that, if known by the insurer, would have resulted in a higher premium, different terms, or a refusal to issue the policy altogether.

What should I do if I receive a cancellation notice for misrepresentation?

If you receive this notice, you should immediately contact your insurance agent to clarify the discrepancy. If the information is correct and the cancellation stands, you must secure new coverage immediately, as a cancellation for misrepresentation can make it difficult and more expensive to find a new carrier.

Comments