Protecting your investment requires understanding how vacancy affects insurance coverage. A Notice of Cancellation for Vacant or Unoccupied Property is a critical document issued when a building remains empty beyond policy limits, often leading to terminated protection. This guide explains legal requirements, notice periods, and steps to mitigate risks. To help you draft professional correspondence, below are some ready to use templates.

Image cover: Essential Templates and Samples: Formal Notice of Cancellation for Vacant or Unoccupied Property

Letter Samples List

- Notice Of Cancellation For Vacant Property Letter

- Commercial Unoccupied Property Cancellation Notice Letter

- Residential Vacant Dwelling Policy Cancellation Letter

- Extended Vacancy Policy Termination Letter

- Undisclosed Unoccupied Property Cancellation Letter

- Pending Cancellation For Vacant Premises Warning Letter

- Post-Inspection Vacant Property Cancellation Letter

- Unoccupied Rental Property Insurance Cancellation Letter

- Final Notice Of Cancellation For Vacant Property Letter

- Vacancy Clause Breach Policy Cancellation Letter

- Vacancy Grace Period Expiration Cancellation Letter

- Abandoned Construction Site Property Cancellation Letter

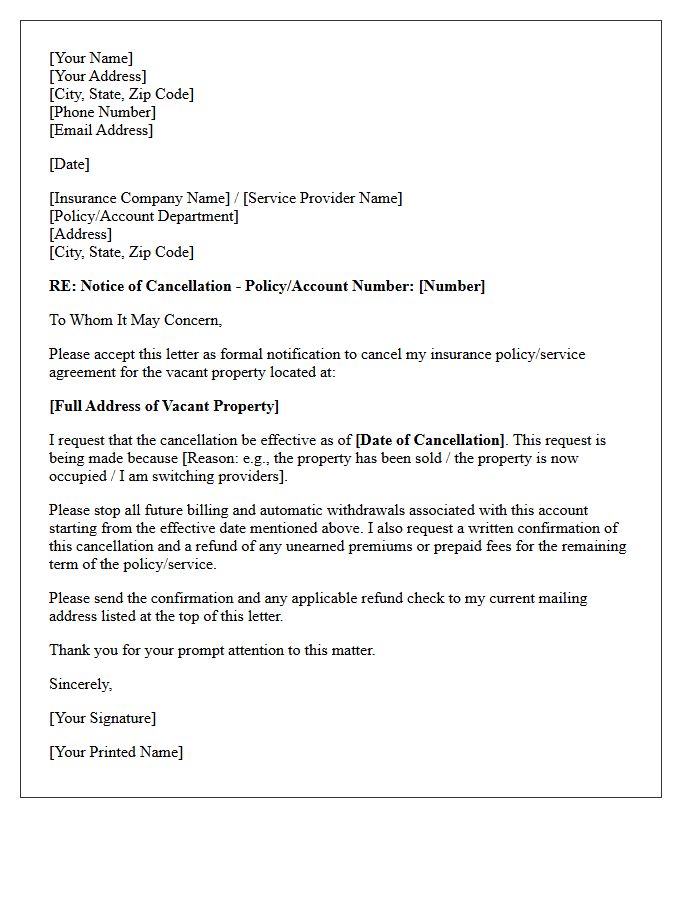

Notice Of Cancellation For Vacant Property Letter

A Notice of Cancellation for Vacant Property is a formal document issued by an insurance provider to terminate coverage when a building remains unoccupied. Most standard policies include a vacancy clause, typically triggered after 30 or 60 days, as empty structures face higher risks of theft, vandalism, and water damage. Policyholders must secure a vacancy permit or specialized insurance to maintain protection. Receiving this letter means your current policy is void, making it critical to find alternative coverage immediately to prevent significant financial loss.

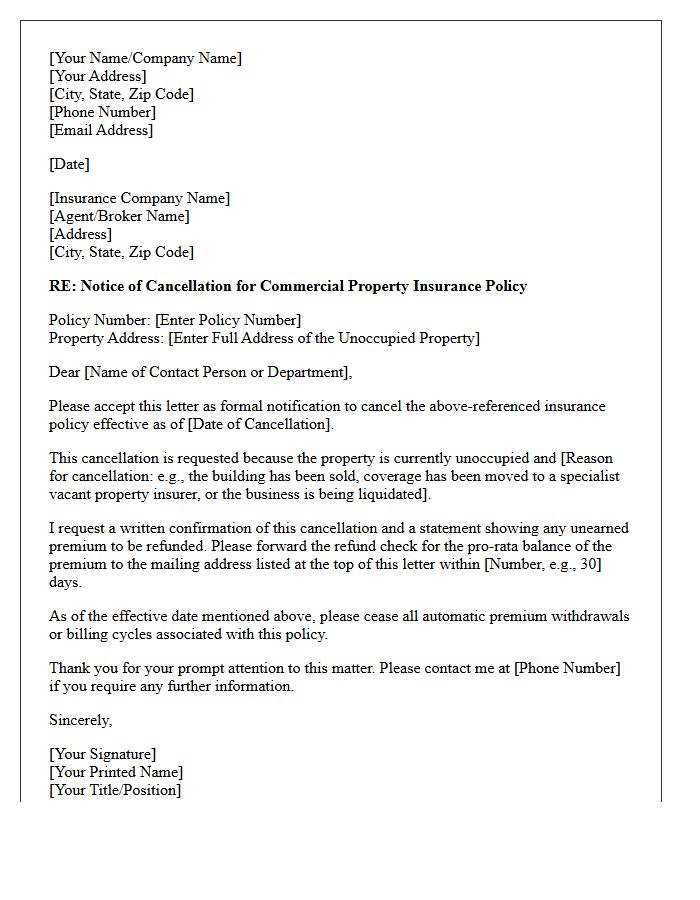

Commercial Unoccupied Property Cancellation Notice Letter

A Commercial Unoccupied Property Cancellation Notice Letter is a formal document sent by an insurer to terminate coverage when a building remains vacant beyond the specified policy limit, typically 30 to 60 days. Unoccupancy significantly increases risks like vandalism, fire, or water damage, often leading to a material change in risk. Property owners must understand that failure to maintain security or notify the provider can result in an immediate cancellation or claim denial. To protect investments, owners should seek specialized vacant property insurance to maintain continuous protection.

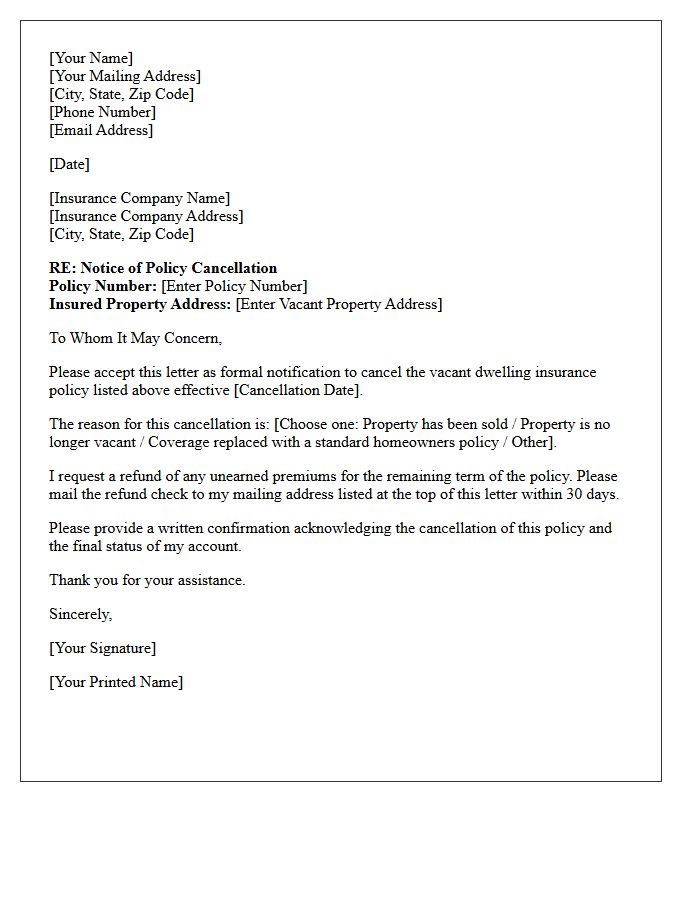

Residential Vacant Dwelling Policy Cancellation Letter

A Residential Vacant Dwelling Policy Cancellation Letter is a formal notice sent by an insurer to terminate coverage on an unoccupied property. It is crucial to understand that vacancy increases risk, often leading to policy non-renewal or mid-term cancellation if the home remains empty beyond the period specified in the vacancy clause. Homeowners must review the effective cancellation date to avoid a lapse in protection. To maintain security, property owners should immediately seek a specialized vacant home insurance policy tailored to the unique liabilities of uninhabited residences.

Extended Vacancy Policy Termination Letter

An Extended Vacancy Policy Termination Letter is a formal notice sent by an insurance provider to cancel or end coverage when a property remains unoccupied beyond a specified timeframe. Most standard policies include a vacancy clause that limits risk exposure for theft, vandalism, or water damage. If the owner fails to maintain active occupancy or secure a vacancy permit, the insurer may issue this termination. It is critical to review your policy limits and communicate with your agent to ensure continuous protection through specialized vacant property insurance before the termination date.

Undisclosed Unoccupied Property Cancellation Letter

When sending an Undisclosed Unoccupied Property Cancellation Letter, it is vital to understand that insurers can void coverage if a building is left vacant without prior notification. Most policies include a vacancy clause, typically triggering after 30 or 60 days. This formal notice confirms the termination of the insurance contract due to increased risk. To protect your interests, always ensure property inspections are documented and notify your provider immediately if a property becomes empty to avoid permanent denial of claims or unexpected policy cancellation.

Pending Cancellation For Vacant Premises Warning Letter

A Pending Cancellation For Vacant Premises Warning Letter is a formal notice from an insurer stating that coverage may be terminated because a property is unoccupied. Insurance policies often exclude vacant buildings due to increased risks like vandalism or water damage. To maintain protection, owners must act quickly to notify their agent, secure the property, or purchase a specific vacancy permit. Ignoring this warning can lead to a total loss of coverage, leaving the owner financially liable for any future incidents or structural damages occurring during the vacancy period.

Post-Inspection Vacant Property Cancellation Letter

A Post-Inspection Vacant Property Cancellation Letter is a formal notice sent by an insurer to terminate coverage after a physical assessment reveals a building is unoccupied. Insurers view vacancy as a high-risk factor due to increased vulnerability to theft, vandalism, and undetected water damage. Upon receipt, it is critical to act immediately, as a lapse in coverage leaves your asset unprotected. Property owners should seek specialized vacant property insurance or demonstrate the building is now occupied to potentially reverse the cancellation and maintain essential financial security.

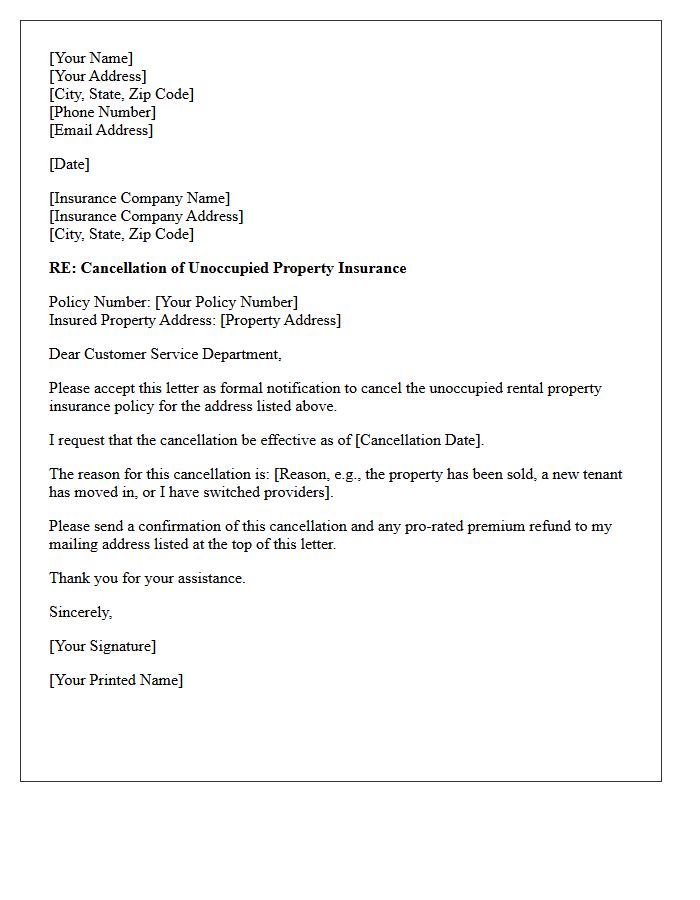

Unoccupied Rental Property Insurance Cancellation Letter

When sending an Unoccupied Rental Property Insurance Cancellation Letter, you must notify your provider in writing to terminate coverage officially. Most standard policies exclude protection after a property remains vacant for over 30 to 60 days. Ensure your letter includes the specific policy number, the requested cancellation date, and a forwarding address. To maintain protection against unique risks like vandalism or pipe bursts during vacancy, always secure specialized unoccupied home insurance before your current policy ends to avoid a dangerous lapse in coverage.

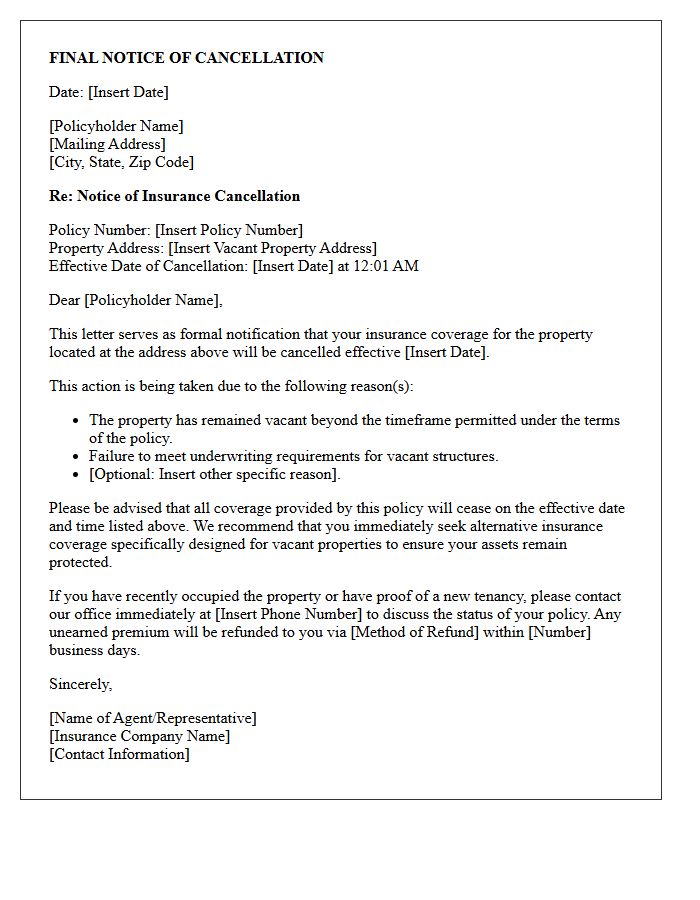

Final Notice Of Cancellation For Vacant Property Letter

A Final Notice of Cancellation for vacant property is a critical legal document informing the owner that their insurance coverage is terminating. This usually occurs because the property remained unoccupied beyond the policy's allowed limit, significantly increasing risks like vandalism or pipe bursts. To protect your investment, you must immediately secure a specialized vacant home policy or resolve the occupancy issue before the effective date. Failure to act results in a lapse of coverage, leaving the property owner financially vulnerable to total loss without any insurance protection.

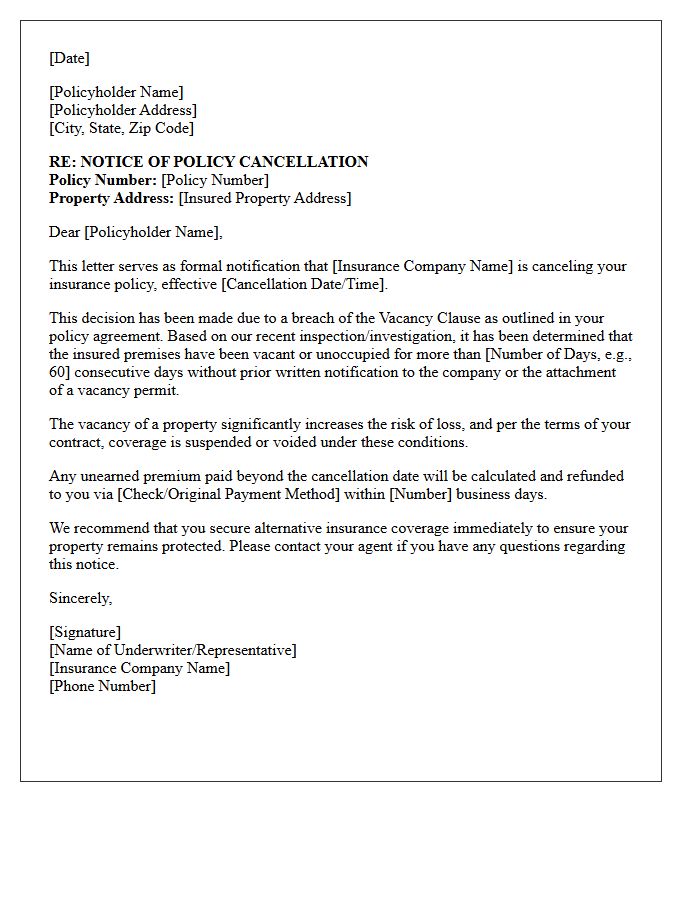

Vacancy Clause Breach Policy Cancellation Letter

A Vacancy Clause Breach Policy Cancellation Letter is a formal notice issued by an insurer to terminate coverage because a property remained unoccupied beyond the specified limit, typically 30 to 60 days. Uninhabited buildings pose higher risks for vandalism, theft, and undetected water damage. When this vacancy provision is violated, the insurance company reserves the right to cancel the policy or deny claims. To maintain protection, owners must notify their agent early to secure a vacancy permit or specialized unoccupied property insurance before a breach occurs.

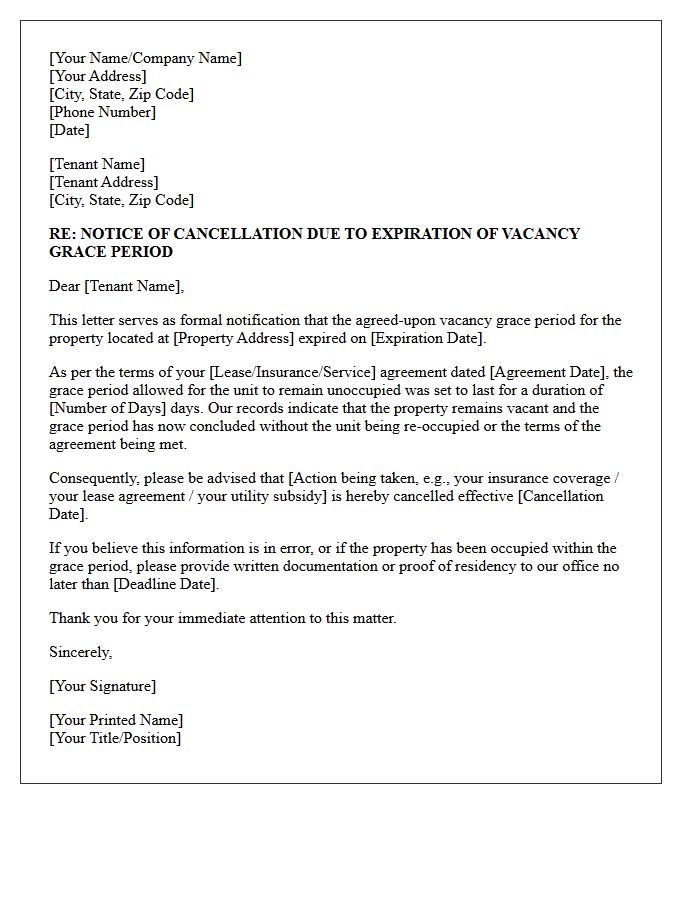

Vacancy Grace Period Expiration Cancellation Letter

A Vacancy Grace Period Expiration Cancellation Letter is a formal notice sent by an insurer when a policyholder fails to occupy a property within the stipulated timeframe. Standard insurance contracts typically limit coverage for properties vacant for over 60 days. Once the grace period expires, the risk profile changes significantly, leading to potential policy cancellation or coverage restrictions. Property owners must act quickly to secure vacancy insurance or provide proof of occupancy to avoid a total loss of financial protection against perils like theft or vandalism.

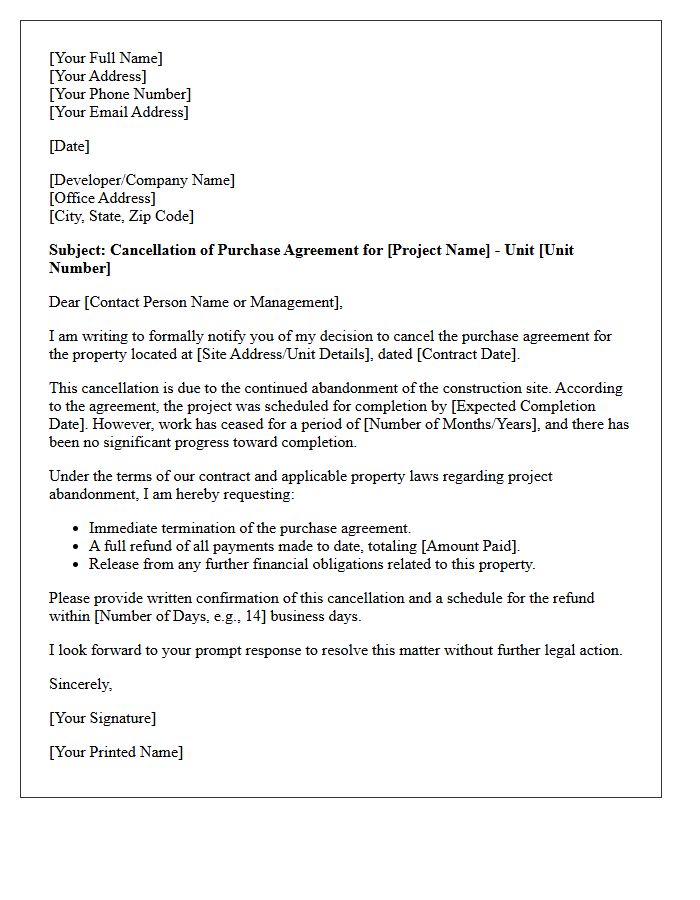

Abandoned Construction Site Property Cancellation Letter

An Abandoned Construction Site Property Cancellation Letter is a formal legal document used to terminate a purchase agreement due to developer default. It serves as official notice that the buyer is withdrawing from the contract because work has ceased indefinitely. To ensure validity, the letter must clearly state the breach of contract, reference specific clauses regarding completion timelines, and demand a full refund of deposits. Sending this via certified mail creates a vital paper trail for potential litigation or insurance claims when recovering financial losses from failed developments.

What is a Notice of Cancellation for vacant or unoccupied property?

A Notice of Cancellation for vacant or unoccupied property is a formal document sent by an insurance provider to terminate a policy because the insured building has been left empty beyond the timeframe permitted in the policy terms, typically 30 to 60 days.

Why does vacancy lead to an insurance policy cancellation?

Insurers view vacant or unoccupied properties as higher risks because they are more susceptible to undetected damage from water leaks, vandalism, theft, or fire, which falls outside the risk profile of a standard homeowner's policy.

How many days of vacancy trigger a cancellation notice?

While specific timelines vary by provider, most standard insurance contracts include a "vacancy clause" that triggers a cancellation or a denial of coverage if the property is left unoccupied for more than 60 consecutive days.

Can I prevent a cancellation if my property becomes vacant?

Yes, you can prevent cancellation by notifying your agent immediately and requesting a "vacancy permit" or "unoccupied property endorsement," which adjusts your premium and coverage to reflect the change in occupancy status.

What is the difference between "vacant" and "unoccupied" in a cancellation notice?

In insurance terms, "unoccupied" means the inhabitants are gone but their belongings remain (such as a vacation), while "vacant" means the occupants and their belongings have been removed; both statuses can lead to a cancellation notice if not properly disclosed.

Comments