Enhance your advisory services by addressing the protection gap between professional and private life. A Business Owner Personal Life Insurance Cross-Sell Letter helps you transition commercial conversations into meaningful personal coverage discussions, securing your client's family legacy and financial future. Strengthen relationships by providing holistic security solutions. To help you get started, below are some ready to use template options.

Image cover: Protecting Your Success and Your Family: Personalized Life Insurance Solutions for Business Owners

Letter Samples List

- Securing Your Family Future Beyond the Business Letter

- Annual Commercial Review and Personal Life Insurance Letter

- Protecting Your Personal Assets and Family Wealth Letter

- Business Owner Personal Peace of Mind Life Insurance Letter

- Transitioning Business Success into Personal Security Letter

- Exclusive Agency Client Personal Life Insurance Offer Letter

- Safeguarding Your Loved Ones While Running Your Business Letter

- Comprehensive Coverage Gap Analysis and Personal Life Letter

- End of Year Financial Planning and Personal Life Insurance Letter

- Key Executive to Family Provider Personal Life Insurance Letter

- Upgrading Your Overall Protection with Personal Life Insurance Letter

- Business Continuity and Personal Estate Planning Life Letter

Securing Your Family Future Beyond the Business Letter

Securing your family's future beyond a business requires a robust estate plan that separates personal wealth from professional liabilities. Prioritizing financial diversification ensures your loved ones remain protected regardless of market volatility. Implementing a strategic succession framework and maintaining updated legal documents, such as wills or trusts, creates a lasting legacy. By prioritizing long-term stability over short-term gains, you safeguard your generational wealth and provide peace of mind for your family's long-term prosperity.

Annual Commercial Review and Personal Life Insurance Letter

An Annual Commercial Review ensures your business remains protected against evolving risks and regulatory changes. It evaluates coverage adequacy, asset valuation, and liability exposure to prevent costly gaps. Simultaneously, a Personal Life Insurance Letter serves as a vital policy audit. This document confirms beneficiary designations, verifies current death benefits, and adjusts coverage based on major life events like marriage or home purchases. Conducting these reviews annually guarantees that both professional interests and family legacies are secured through optimized protection strategies tailored to your current financial situation.

Protecting Your Personal Assets and Family Wealth Letter

A Protecting Your Personal Assets and Family Wealth Letter is a vital legal instrument designed to safeguard your estate from potential creditors, lawsuits, and financial instability. This document outlines strategic asset protection methods, such as establishing trusts or legal entities, to ensure your inheritance remains secure for future generations. By formalizing your intentions, you minimize tax liabilities and provide clear instructions for wealth preservation. Understanding these protocols is essential for maintaining long-term financial security and ensuring that your family wealth is insulated from unforeseen economic risks or legal challenges.

Business Owner Personal Peace of Mind Life Insurance Letter

A Business Owner Personal Peace of Mind Life Insurance Letter is a strategic communication designed to secure a founder's legacy. It highlights how a customized policy protects personal assets from professional liabilities while ensuring family financial stability. By formalizing succession planning and debt coverage, the letter provides clarity for stakeholders during transitions. This document serves as a vital bridge between corporate responsibilities and private security, offering the essential peace of mind needed to focus on long-term growth without risking personal insolvency or family hardship.

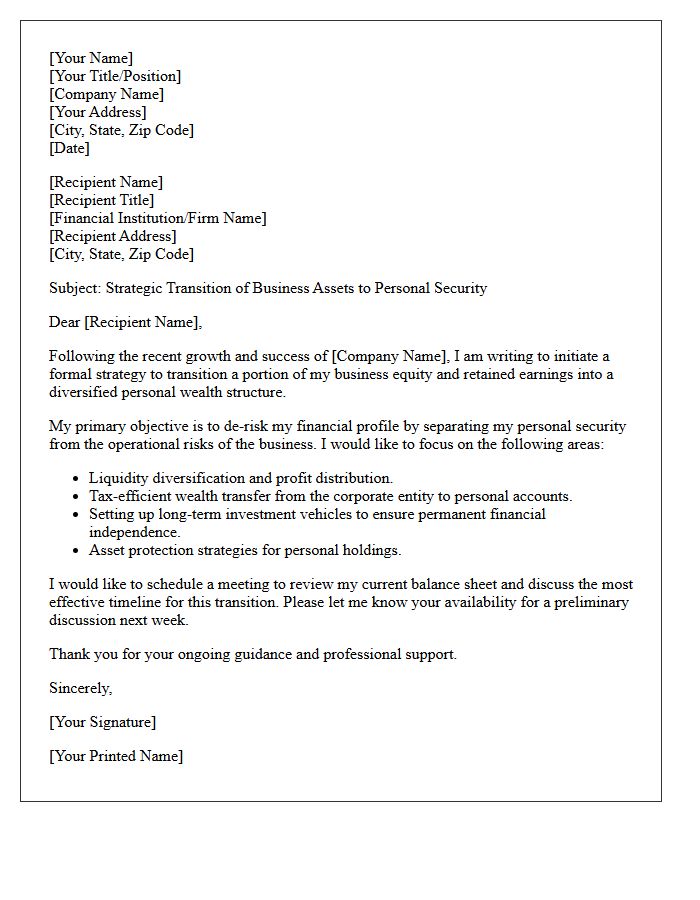

Transitioning Business Success into Personal Security Letter

A Transitioning Business Success into Personal Security Letter is a strategic document used to redeploy corporate wealth into protected private assets. This process ensures that liquidity events or exit proceeds are shielded from business liabilities and market volatility. By formalizing the transfer of ownership stakes into diversified investment vehicles, business owners establish long-term financial independence. It serves as a roadmap for converting operational achievements into generational wealth, prioritizing risk management and tax efficiency to secure a stable future beyond the company's lifecycle.

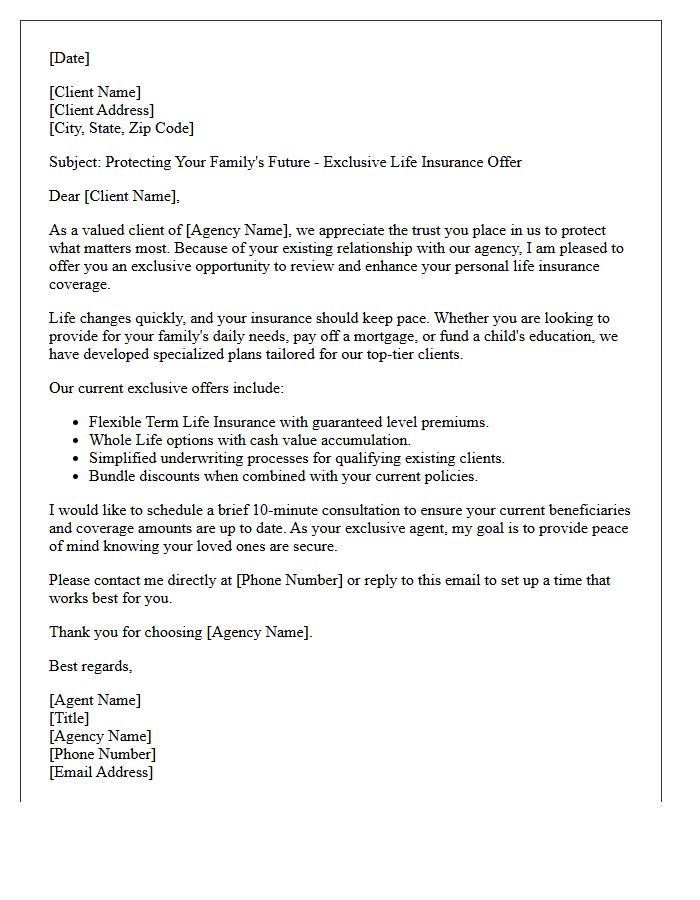

Exclusive Agency Client Personal Life Insurance Offer Letter

An Exclusive Agency Client Personal Life Insurance Offer Letter is a targeted proposal providing customized coverage for existing policyholders. It outlines unique benefits, such as guaranteed issue options or premium discounts, tailored to your financial history. This formal notification serves as an invitation to enhance your protection without redundant paperwork. Review the policy riders and death benefit limits carefully to ensure the plan meets your current estate goals. This exclusive offer typically features preferential underwriting, making it a time-sensitive opportunity to secure your family's financial future through a trusted provider.

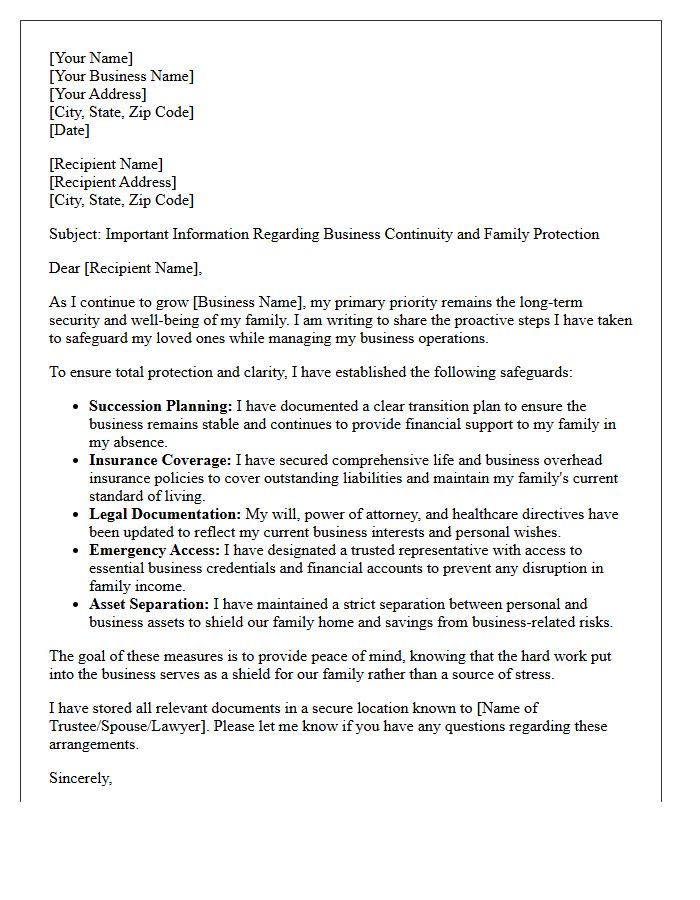

Safeguarding Your Loved Ones While Running Your Business Letter

Balancing entrepreneurship with family security requires a comprehensive succession plan to ensure stability during transitions. It is essential to draft a legally binding letter of instruction that outlines operational procedures, emergency contacts, and financial access for your heirs. Clearly defining asset protection strategies and business continuity goals prevents confusion and preserves your legacy. This proactive approach safeguards your family's future by providing a roadmap for managing the enterprise and protecting personal wealth should you become unable to oversee daily operations yourself.

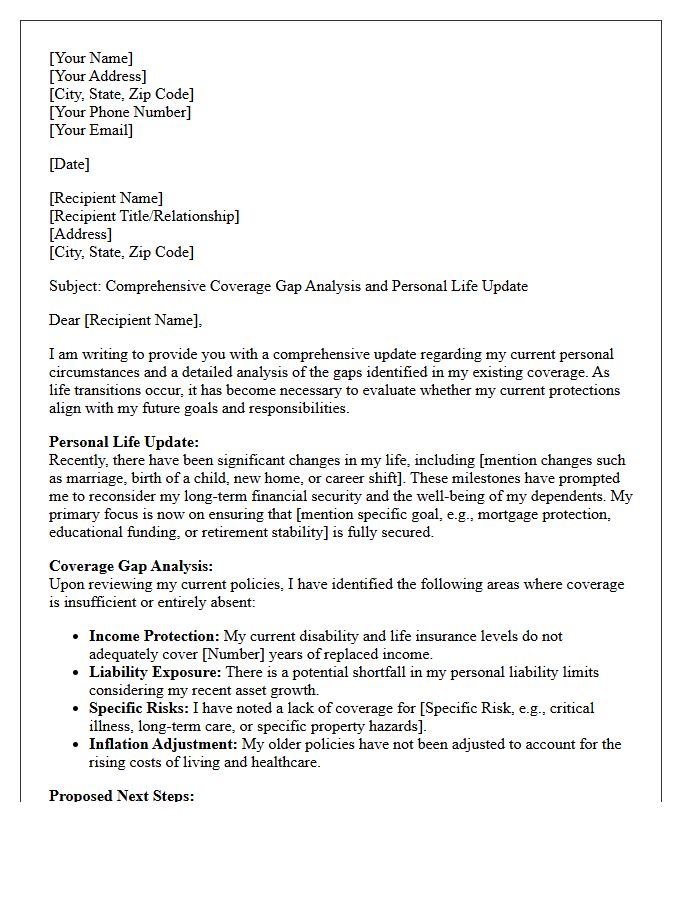

Comprehensive Coverage Gap Analysis and Personal Life Letter

A Comprehensive Coverage Gap Analysis identifies hidden vulnerabilities in your insurance portfolio, ensuring financial security against unforeseen risks. When paired with a Personal Life Letter, it provides loved ones with vital instructions and clarity regarding asset distribution and final wishes. This combined approach bridges the gap between complex legal policies and practical family needs. By evaluating current protections and documenting intentions, you eliminate uncertainty and safeguard your legacy. Prioritizing this strategic review protects your wealth while offering peace of mind through organized, accessible information for your beneficiaries.

End of Year Financial Planning and Personal Life Insurance Letter

An end-of-year letter is essential for reviewing financial planning goals and securing your family's future. It provides a formal record to update beneficiaries, assess coverage gaps, and maximize tax advantages before the deadline. Evaluating your personal life insurance ensures your policy aligns with recent life changes like marriage or home purchases. Use this opportunity to coordinate your estate strategy with your financial advisor, ensuring comprehensive protection and peace of mind for the coming year.

Key Executive to Family Provider Personal Life Insurance Letter

A key executive to family provider personal life insurance letter is a vital document used to reassign beneficiary rights from a corporation to a private household. This formal notification ensures that high-value coverage, initially intended for business protection, now serves as a financial safety net for dependents. It clarifies the transfer of ownership or death benefits, securing the policyholder's legacy. This transition is essential for maintaining long-term stability and providing immediate liquidity to survivors during a transition, effectively turning a professional asset into a personal security instrument.

Upgrading Your Overall Protection with Personal Life Insurance Letter

An upgrade letter for your personal life insurance is a vital tool to address evolving financial needs. It allows you to increase coverage limits or add riders that protect against unforeseen circumstances like critical illness or disability. By formalizing these changes, you ensure your policy remains aligned with current life milestones, such as marriage or homeownership. Proactively updating your protection guarantees that your beneficiaries receive the maximum intended support, securing your family's long-term financial stability through enhanced and comprehensive policy terms.

Business Continuity and Personal Estate Planning Life Letter

A Life Letter is a vital Business Continuity and estate planning tool designed to guide survivors through complex transitions. It acts as a comprehensive instruction manual, detailing critical passwords, financial accounts, legal contacts, and operational procedures often missing from a formal will. By documenting these essential logistics, you ensure the seamless management of your legacy and protect your professional interests. This informal yet powerful document minimizes confusion, reduces administrative burdens, and provides peace of mind for both family members and business partners during a crisis.

Why should I consider personal life insurance if I already have business coverage?

While business policies like Buy-Sell or Key Person insurance protect your company's continuity, personal life insurance is specifically designed to secure your family's lifestyle, pay off private debt, and fund your children's education independently of your business assets.

Can I use my business to pay for my personal life insurance premiums?

Generally, personal life insurance premiums are paid with post-tax dollars to ensure a tax-free death benefit for your beneficiaries. However, there are specific executive bonus plans (Section 162) that allow a business to subsidize coverage as a tax-deductible benefit for the owner.

How does personal life insurance help with business succession planning?

Personal life insurance provides the necessary liquidity to equalize an inheritance. If one child inherits the business, personal policy proceeds can provide an equivalent cash inheritance for children not involved in the company, preventing family conflict and the forced sale of business assets.

Is my business value included when determining how much personal coverage I need?

Yes. A comprehensive needs analysis looks at your total estate, including the fair market value of your business. Personal coverage ensures that if the business cannot be sold quickly or for its full value after your passing, your family remains financially stable.

What happens to my personal life insurance if I sell or retire from my business?

Unlike group term life insurance or business-owned policies, a personal life insurance policy is portable. You own the contract individually, meaning your coverage remains in force regardless of your professional status, providing permanent peace of mind throughout your retirement.

Comments