Retaining existing policyholders requires offering comprehensive protection that evolves with their needs. Integrating Long-Term Care coverage into your life insurance portfolio provides clients with essential financial security against rising healthcare costs. This strategy strengthens relationships while diversifying your business. To help you initiate these vital conversations and boost your cross-selling success, below are some ready to use template.

Image cover: Proven Long-Term Care Cross-Sell Templates for Life Insurance Clients

Letter Samples List

- Life Insurance Policy Review And Long Term Care Introduction Letter

- Protecting Your Legacy With A Long Term Care Cross-Sell Letter

- Comprehensive Coverage Assessment And Long Term Care Letter

- Existing Client Long Term Care Awareness Letter

- Enhancing Your Life Insurance With A Long Term Care Letter

- Future Care Planning And Life Insurance Upgrade Letter

- Long Term Care Solutions For Valued Life Insurance Clients Letter

- Securing Your Retirement Health With A Long Term Care Letter

- Life Insurance Policy Anniversary And Long Term Care Letter

- Bridging The Gap With A Long Term Care Protection Letter

- Aging Gracefully Long Term Care Cross-Sell Letter

- Family Wealth Protection And Long Term Care Advisory Letter

- Long Term Care Rider Addition Inquiry Letter

- Financial Security And Long Term Care Evaluation Letter

Life Insurance Policy Review And Long Term Care Introduction Letter

A Life Insurance Policy Review is a vital financial audit to ensure your current coverage aligns with evolving personal goals. Over time, changes in health, income, or family structure can render existing plans obsolete. This process introduces Long-Term Care options, addressing the rising costs of extended medical support or assisted living. By evaluating your death benefit and living benefits together, you can bridge coverage gaps and secure comprehensive protection for your legacy. Use this introduction letter to start a professional assessment of your financial security and future healthcare preparedness today.

Protecting Your Legacy With A Long Term Care Cross-Sell Letter

A Long Term Care Cross-Sell Letter is a strategic tool designed to help clients safeguard their financial legacy from the rising costs of extended healthcare. By educating policyholders on how asset-based coverage or traditional LTC riders can prevent the depletion of life insurance death benefits or retirement savings, advisors provide essential protection. This proactive communication identifies gaps in coverage, ensuring that medical expenses do not erode an inheritance. It positions long-term care as a vital component of a comprehensive estate plan, securing peace of mind for both the client and their beneficiaries.

Comprehensive Coverage Assessment And Long Term Care Letter

A Comprehensive Coverage Assessment is a crucial evaluation determining an individual's eligibility for Long-Term Care benefits based on functional needs. Following this review, the official Long-Term Care Letter serves as formal notification regarding your approved level of assistance. It details specific benefit entitlements, coverage limits, and any required cost-sharing responsibilities. Understanding this document is essential for coordinating medical services and ensuring financial support for extended nursing or home-based care. Always verify that the assessment accurately reflects your daily living requirements to secure maximum available support.

Existing Client Long Term Care Awareness Letter

An Existing Client Long Term Care Awareness Letter is a vital communication tool designed to educate current policyholders about the financial risks of aging. The primary goal is to initiate proactive planning for future nursing home or home health care needs. By highlighting potential gaps in retirement strategies, this letter encourages clients to protect their assets from being depleted by medical expenses. Providing timely information strengthens the advisor-client relationship while ensuring families are better prepared for the high costs of long-term support and services.

Enhancing Your Life Insurance With A Long Term Care Letter

Adding a long-term care rider to your life insurance policy provides a dual benefit by protecting your death benefit while covering chronic illness expenses. This strategic enhancement allows you to accelerate a portion of your policy's face value to pay for home care or nursing facilities. By securing this living benefit, you safeguard your retirement savings from being depleted by medical costs. It is essential to understand the specific triggers for benefits, ensuring your coverage offers financial security and comprehensive protection for your future health needs and legacy.

Future Care Planning And Life Insurance Upgrade Letter

A Future Care Planning and life insurance upgrade letter is a formal notice advising policyholders to align their coverage with evolving long-term healthcare needs. It highlights essential updates to living benefits, ensuring financial protection against chronic illness or disability. This communication often outlines options to increase death benefits or add accelerated riders for terminal care. Reviewing these proposals is vital to secure your family's future and adapt to rising medical costs. Timely upgrades ensure your insurance portfolio remains robust, providing comprehensive security during aging or unexpected health transitions.

Long Term Care Solutions For Valued Life Insurance Clients Letter

Providing a Long-Term Care Solutions letter is essential for protecting your life insurance clients from future healthcare costs. Highlighting hybrid policies allows policyholders to access death benefits early for care expenses, ensuring financial security. Explain how these riders offer asset protection and peace of mind without losing the underlying value of their coverage. This proactive outreach demonstrates your commitment to their holistic financial well-being, helping clients preserve their independence while maintaining a legacy for their beneficiaries during vulnerable life stages.

Securing Your Retirement Health With A Long Term Care Letter

A Long Term Care Letter is a critical document for securing your retirement health and financial stability. It outlines your specific preferences for medical assistance and daily support should you become unable to care for yourself. By formalizing these wishes early, you protect your assets from rising healthcare costs and reduce the emotional burden on your family. Integrating this letter into your estate plan ensures your quality of life remains a priority, providing a clear roadmap for caregivers to follow during vulnerable times.

Life Insurance Policy Anniversary And Long Term Care Letter

A life insurance policy anniversary is the yearly milestone of your coverage, triggering an essential review of your death benefit and premiums. When you receive a Long Term Care letter during this period, it typically outlines your eligibility for accelerated benefits or optional riders. These features allow you to access your policy's value early to pay for chronic illness expenses. Understanding this correspondence is vital for ensuring your financial security aligns with evolving health needs, protecting your assets from the high costs of extended medical care over time.

Bridging The Gap With A Long Term Care Protection Letter

A Long Term Care Protection Letter is a vital document designed to bridge the gap between standard health insurance and long-term support. It serves as a formal notification to insurers or facilities, clearly outlining an individual's coverage rights and financial safeguards. By securing this letter, families can prevent coverage lapses and ensure seamless access to nursing care or assisted living. Understanding this protection is essential for preserving personal assets while maintaining a high standard of medical care throughout aging, effectively mitigating the risks of unexpected healthcare costs and complex policy exclusions.

Aging Gracefully Long Term Care Cross-Sell Letter

An effective Aging Gracefully Long Term Care cross-sell letter focuses on financial security and maintaining independence. It educates existing clients about the rising costs of extended medical assistance while highlighting how specialized coverage protects personal assets. By emphasizing proactive planning, the message transforms a complex insurance product into a compassionate solution for dignity in later years. Personalizing the offer based on current policy data ensures the communication feels relevant, timely, and supportive of their long-term well-being.

Family Wealth Protection And Long Term Care Advisory Letter

The Family Wealth Protection and Long Term Care Advisory Letter provides essential strategies for safeguarding assets against rising medical costs. It offers expert guidance on Medicaid planning, long-term care insurance, and estate preservation to ensure financial stability for aging relatives. By staying informed, families can prevent the depletion of their inheritance due to nursing home expenses. This resource simplifies complex legal regulations, helping you secure a legacy through proactive wealth management and specialized healthcare planning advice tailored for sustainable multi-generational security.

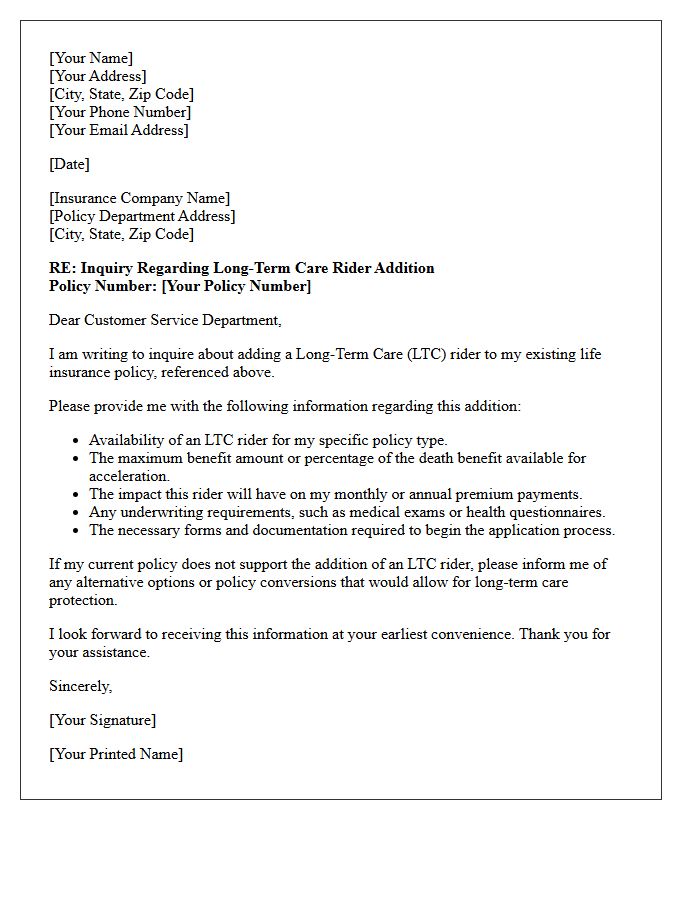

Long Term Care Rider Addition Inquiry Letter

A Long Term Care Rider Addition Inquiry Letter is a formal request sent to an insurance provider to evaluate adding living benefits to an existing life insurance policy. This document initiates the process of securing accelerated death benefits to cover chronic illness or nursing home costs. It is crucial to verify your eligibility, potential premium adjustments, and specific coverage triggers. Clearly stating your policy number and requesting a written illustration ensures you understand how this addition protects your financial assets against future medical expenses without requiring a separate, standalone policy.

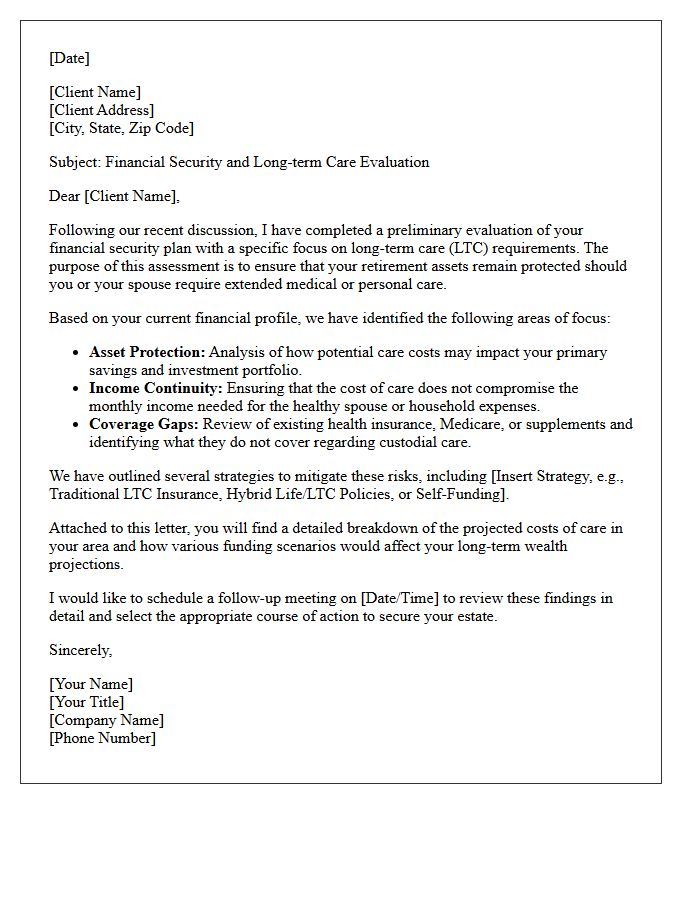

Financial Security And Long Term Care Evaluation Letter

A Financial Security and Long-Term Care Evaluation Letter is a formal assessment used to verify an individual's ability to fund extended healthcare services. This document evaluates assets, insurance coverage, and income streams to ensure sustainability against rising medical costs. It serves as a vital tool for families and estate planners to identify funding gaps and protect generational wealth. By analyzing potential risks, the letter provides a strategic roadmap for maintaining financial independence while securing quality care for aging individuals without depleting their entire life savings.

Why am I receiving information about long-term care from my life insurance provider?

As a current policyholder, we want to ensure your financial plan accounts for the rising costs of extended healthcare. Since many modern life insurance policies offer living benefits or riders for chronic illness, you may be able to leverage your existing coverage to protect your retirement savings from long-term care expenses.

Does my current life insurance policy already cover long-term care costs?

Standard life insurance policies primarily provide a death benefit; however, many plans can be enhanced with a Long-Term Care (LTC) rider or accelerated death benefit. We recommend a policy review to determine if your specific coverage allows you to access your death benefit early to pay for home health care, assisted living, or nursing home costs.

Can I add long-term care protection to my existing life insurance plan?

In many cases, yes. Depending on your policy type and current health status, you may be able to add a supplemental rider or convert a portion of your coverage into a hybrid life/LTC policy. This ensures that if you never need long-term care, your beneficiaries still receive the full death benefit, but if you do need care, you have immediate access to tax-free funds.

How does a hybrid life insurance policy differ from traditional long-term care insurance?

Traditional long-term care insurance is often "use-it-or-lose-it," similar to auto insurance. A hybrid life insurance policy is more flexible; it provides a pool of money for long-term care if needed, but if it remains unused, it pays out a tax-free death benefit to your heirs, ensuring your premiums always provide value.

What are the advantages of using life insurance to fund long-term care?

Using life insurance for long-term care provides premium stability, asset protection, and tax advantages. By integrating LTC protection into your life insurance, you lock in a death benefit while creating a financial safety net that prevents you from depleting your 401(k) or personal savings to pay for professional caregiving services.

Comments