Expanding your portfolio is easy with a Personal Lines Client Small Business Insurance Cross-Sell Letter. This strategy helps insurance agents target existing homeowners or auto clients who also own companies. By highlighting the convenience of bundling professional and personal protection, you increase retention and revenue. To help you start, below are some ready to use templates.

Image cover: Strategic Cross-Sell Templates: Transitioning Personal Lines Clients to Small Business Coverage

Letter Samples List

- Home-Based Business Discovery Cross-Sell Letter

- Side Hustle To Small Business Protection Letter

- Personal Auto To Commercial Fleet Transition Letter

- Loyal Client Business Exposure Review Offer Letter

- New LLC Formation Inquiry And Coverage Letter

- Independent Contractor Commercial Auto Upgrade Letter

- Personal Umbrella To Commercial Liability Expansion Letter

- Residential Landlord Commercial Property Cross-Sell Letter

- Annual Policy Review And Business Inquiry Letter

- Growing Business Workers Compensation Introduction Letter

- Home Office Cyber Liability Protection Letter

- Personal And Commercial Lines Bundling Discount Letter

- Entrepreneur Identification And Consultation Letter

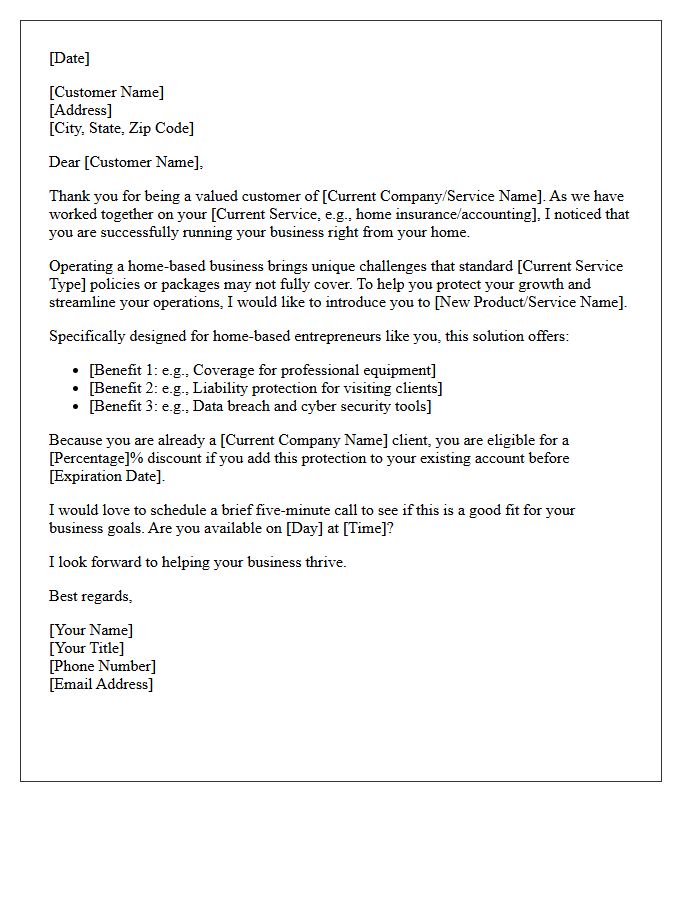

Home-Based Business Discovery Cross-Sell Letter

A Home-Based Business Discovery Cross-Sell Letter is a strategic marketing tool designed to introduce existing customers to new entrepreneurial opportunities. By leveraging established trust, this letter highlights complementary products or services that help individuals launch or grow their own ventures. The primary goal is to maximize customer lifetime value through targeted recommendations. Effective letters focus on revenue potential, low startup costs, and professional freedom, transforming a single-product buyer into a multi-level business partner or loyal brand advocate within a specialized niche.

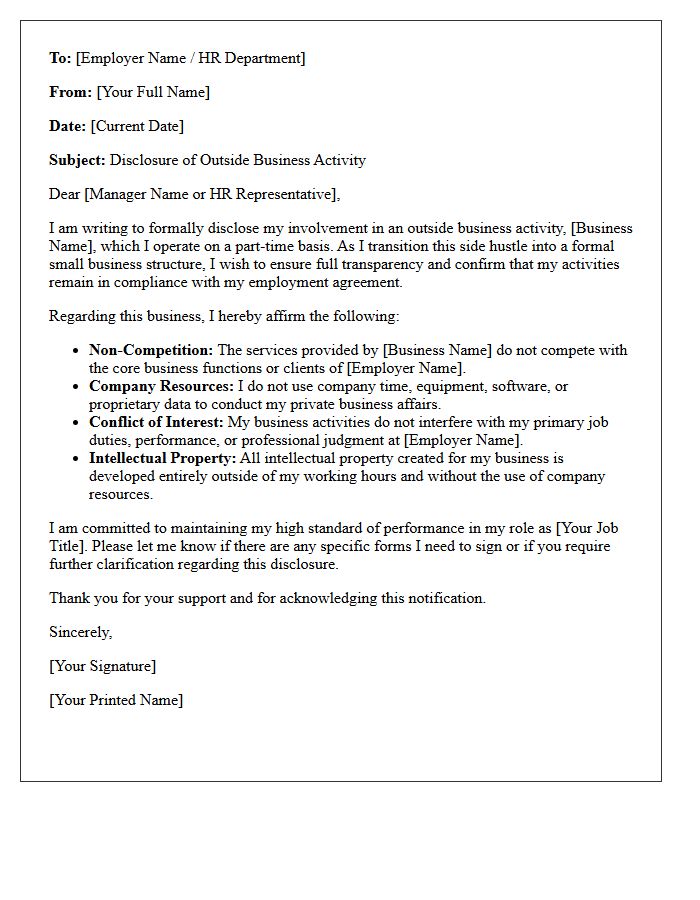

Side Hustle To Small Business Protection Letter

A Side Hustle To Small Business Protection Letter is a vital legal document used to formalize the separation between personal assets and professional operations. It establishes a clear liability shield, ensuring that your private wealth remains protected from business-related debts or litigation. By documenting this transition, you solidify your brand's status as a legitimate entity rather than a casual hobby. This proactive step is essential for safeguarding your financial future, enhancing professional credibility, and providing a formal framework for sustainable growth and long-term risk management.

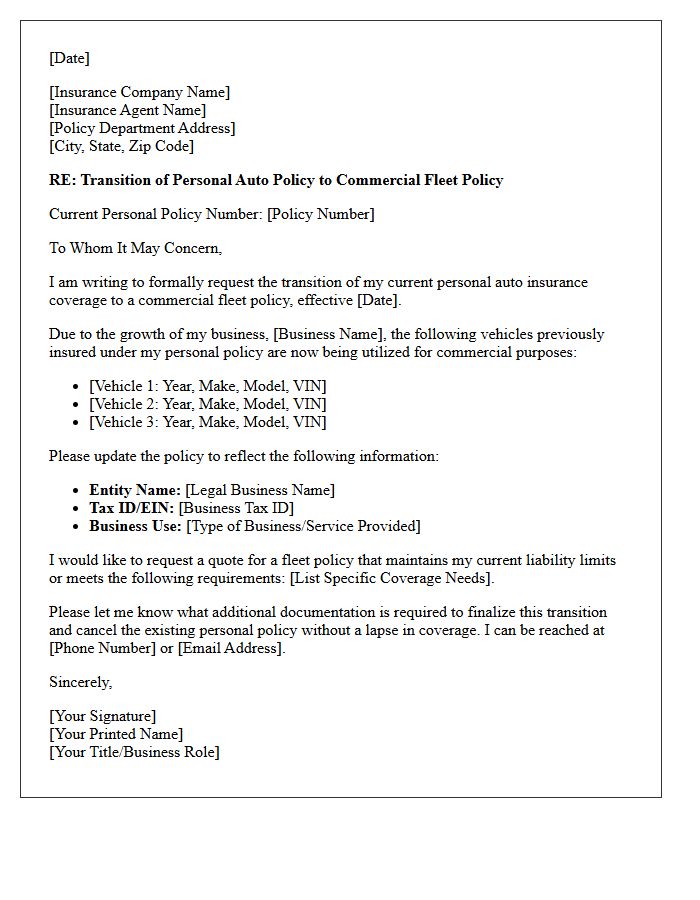

Personal Auto To Commercial Fleet Transition Letter

A transition letter effectively manages the shift from personal auto policies to a commercial fleet structure. It serves as formal notification that specific vehicles are moving to business coverage, ensuring continuous protection and regulatory compliance. Key details should include effective dates, driver lists, and updated liability limits tailored for business operations. This document is essential for maintaining accurate records, streamlining premium adjustments, and minimizing insurance gaps during the conversion process. Proper notification protects both the business entity and individual drivers under a unified corporate policy framework.

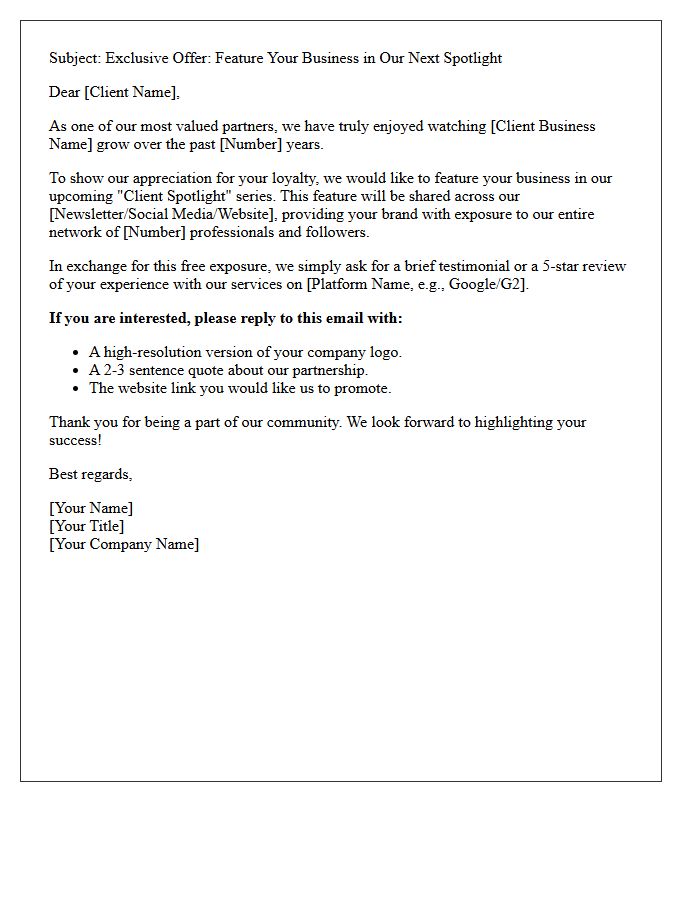

Loyal Client Business Exposure Review Offer Letter

A Loyal Client Business Exposure Review Offer Letter is a strategic communication designed to reward long-term partners while boosting your brand visibility. It invites trusted customers to provide authentic testimonials or case studies in exchange for incentives. This approach leverages social proof to build credibility and attract new leads. By highlighting successful collaborations, businesses can strengthen client retention and enhance their online reputation. Ensure the offer is personalized and clearly outlines the mutual benefits of the exposure to maximize participation and foster professional growth.

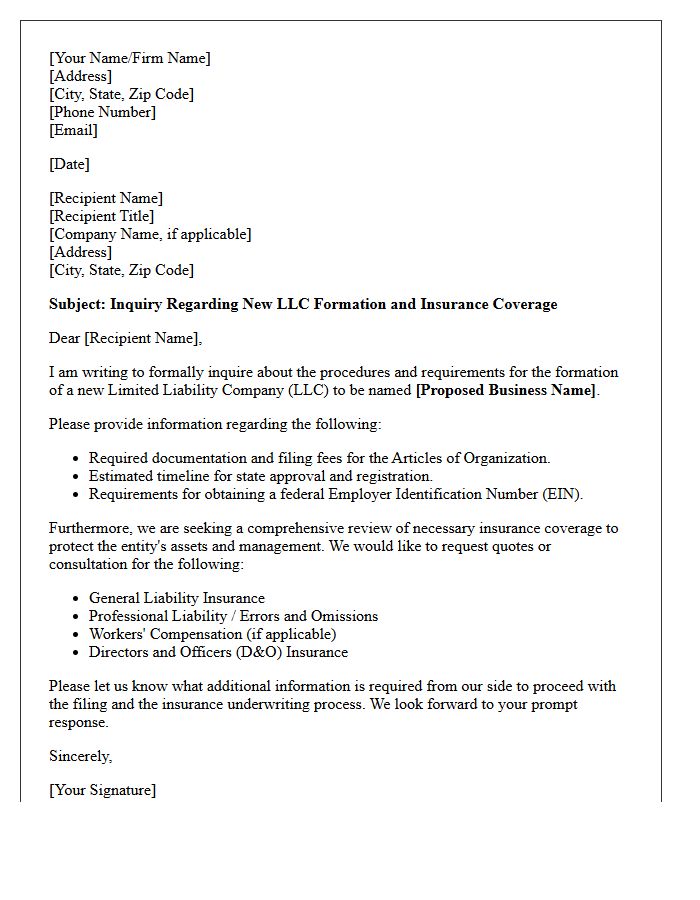

New LLC Formation Inquiry And Coverage Letter

A New LLC Formation Inquiry And Coverage Letter is a vital document used to verify a business's legal status and insurance eligibility. This letter formally requests information regarding the entity's structure while ensuring that professional liability coverage or general policies are active from the date of formation. It serves as essential proof for lenders, stakeholders, and regulatory bodies that the new company is compliant and adequately protected against potential risks. Promptly securing this documentation facilitates seamless operations and establishes legal credibility for your burgeoning enterprise during its initial startup phase.

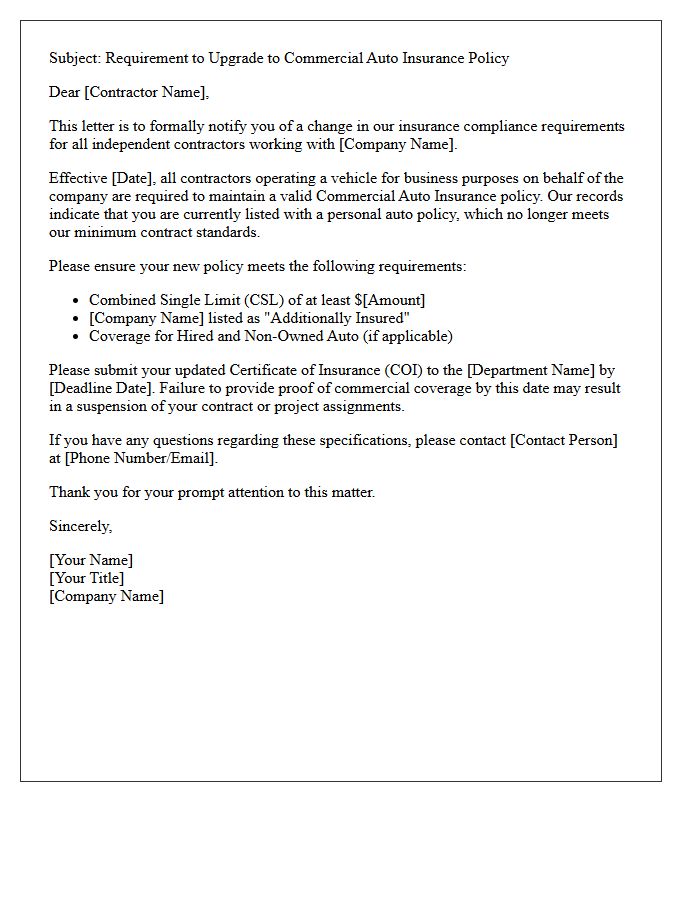

Independent Contractor Commercial Auto Upgrade Letter

An Independent Contractor Commercial Auto Upgrade Letter is a formal notification sent to hired contractors requiring them to upgrade their personal vehicle insurance to a commercial policy. This document ensures that the contractor maintains adequate liability coverage for business-related activities, protecting both the individual and the hiring organization from legal exposure during accidents. It typically outlines specific minimum coverage limits and requires proof of the updated policy. Failing to comply with this upgrade may result in contract termination or a breach of professional service agreements.

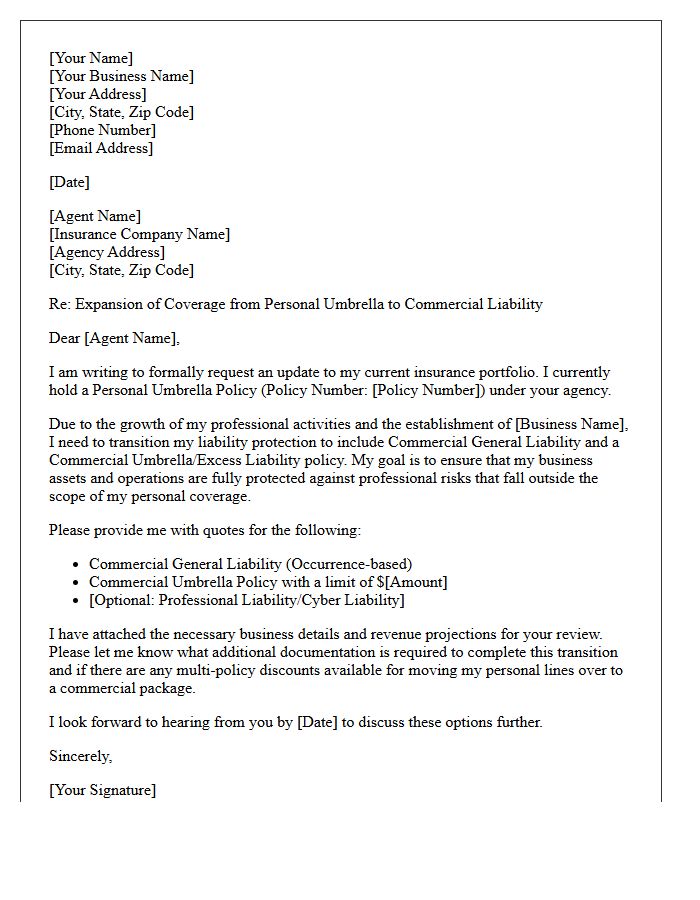

Personal Umbrella To Commercial Liability Expansion Letter

A Personal Umbrella to Commercial Liability Expansion Letter is a critical document used to extend secondary liability coverage over business activities. It formally requests that your personal insurer bridge the gap between private and professional risks. This expansion ensures that underlying commercial policies are properly scheduled within your umbrella's limits. Without this formal endorsement, personal policies typically exclude business-related claims, leaving you exposed to catastrophic financial loss. Use this letter to maintain seamless protection across both personal assets and evolving commercial ventures through integrated risk management.

Residential Landlord Commercial Property Cross-Sell Letter

A residential landlord cross-sell letter is a strategic marketing tool designed to convert residential property owners into commercial real estate clients. It highlights the benefits of diversifying investment portfolios by transitioning into retail, office, or industrial spaces. Effective letters emphasize higher yield potential, longer lease terms, and reduced management intensity. By showcasing your expertise in commercial brokerage, you position yourself as a comprehensive advisor. The goal is to build trust and demonstrate how commercial assets provide superior long-term appreciation and professional-grade stability compared to traditional residential rentals.

Annual Policy Review And Business Inquiry Letter

An Annual Policy Review is a vital process to ensure your insurance coverage aligns with current business needs and asset values. Using a Business Inquiry Letter allows companies to formally request policy updates, clarify terms, and identify potential coverage gaps. This proactive communication helps in mitigating risks and optimizing premium costs. Regularly reviewing your insurance portfolio ensures that your protection remains robust against evolving liabilities, protecting your financial stability. Keeping documentation accurate through formal inquiries is a best practice for effective risk management and long-term operational security.

Growing Business Workers Compensation Introduction Letter

A growing business workers compensation introduction letter is a vital document for onboarding new employees. It formally introduces your insurance coverage, outlining the steps to take if a workplace injury occurs. This letter ensures legal compliance and transparency, building trust within your expanding team. It should clearly list emergency procedures, contact information for the provider, and the worker's rights. Providing this information early minimizes confusion during accidents and promotes a culture of safety as your company scales.

Home Office Cyber Liability Protection Letter

A Home Office Cyber Liability Protection Letter confirms your insurance coverage against digital threats while working remotely. This document outlines essential protection for data breaches, ransomware attacks, and financial losses resulting from cybercrime. It serves as vital verification for employers or clients that your home workspace meets specific security standards and risk mitigation requirements. Understanding these terms ensures you maintain compliance and financial security in a professional telecommuting environment.

Personal And Commercial Lines Bundling Discount Letter

A personal and commercial lines bundling discount letter informs policyholders about savings achieved by consolidating individual and business insurance. The most critical element is the multi-policy discount, which reduces overall premiums when combining coverage like homeowners, auto, and general liability under one provider. This letter outlines streamlined billing and simplified management while highlighting potential cost reductions. By leveraging account rounding, clients receive enhanced protection and loyalty rewards. Understanding these integrated savings helps business owners maximize their budget while ensuring comprehensive risk mitigation across all personal and professional assets.

Entrepreneur Identification And Consultation Letter

An Entrepreneur Identification and Consultation Letter is a formal document used to verify an individual's business status for legal or financial purposes. It serves as official proof that an entrepreneur has received professional guidance regarding their business structure and compliance needs. This letter is often required by government agencies or financial institutions to validate the legitimacy of a startup. It confirms that the founder has undergone a comprehensive consultation to ensure their enterprise meets all regulatory standards and is prepared for sustainable growth within the competitive marketplace.

Why am I receiving an offer for small business insurance with my personal policy?

As a valued personal lines client, we want to ensure that your side business, freelance work, or home-based company is protected by a dedicated commercial policy, as standard homeowners or auto insurance typically excludes business-related claims.

Does my homeowners insurance cover my home-based business?

Most homeowners policies provide very limited coverage for business equipment and generally exclude liability for business-related injuries or professional errors. A small business policy fills these gaps to protect your personal assets from professional risks.

What types of business insurance are available for personal lines clients?

We offer a range of affordable options including General Liability, Professional Liability (Errors & Omissions), Business Owners Policies (BOP), and Cyber Liability insurance tailored specifically for consultants, contractors, and small boutique owners.

Can I get a discount for bundling my business and personal insurance?

Yes, by placing your small business coverage with the same agency that handles your home and auto insurance, you may be eligible for multi-policy discounts and the convenience of managing all your protection in one place.

How do I get a quote for my small business?

Getting a quote is simple; you can reply to your cross-sell letter, call your dedicated agent directly, or visit our website to provide a few details about your business operations for a customized coverage proposal.

Comments